Policy

Our Emerging Markets strategists put together a hypothetical conversation between President Trump and Treasury Secretary nominee Scott Bessent on what economic policy would look like for the Trump 2.0 administration. Secretary Bessent is expected…

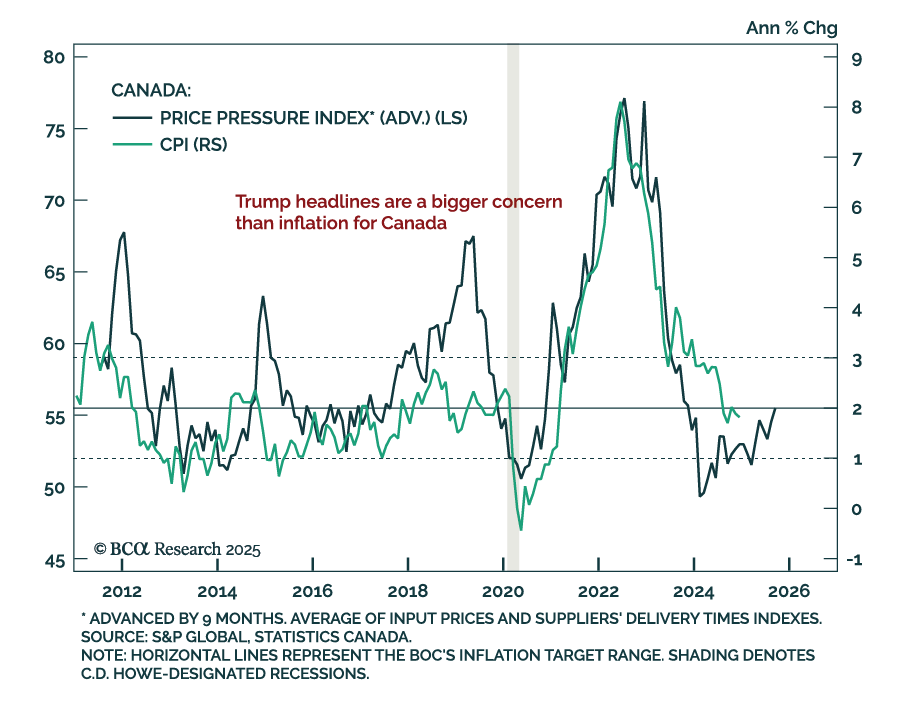

The December Canadian CPI was roughly in line with estimates, with headline inflation ticking down to 1.8% y/y from 1.9% in November. The BoC’s core inflation measures, median and trim, also decreased from 2.6% to 2.4% and 2.5%,…

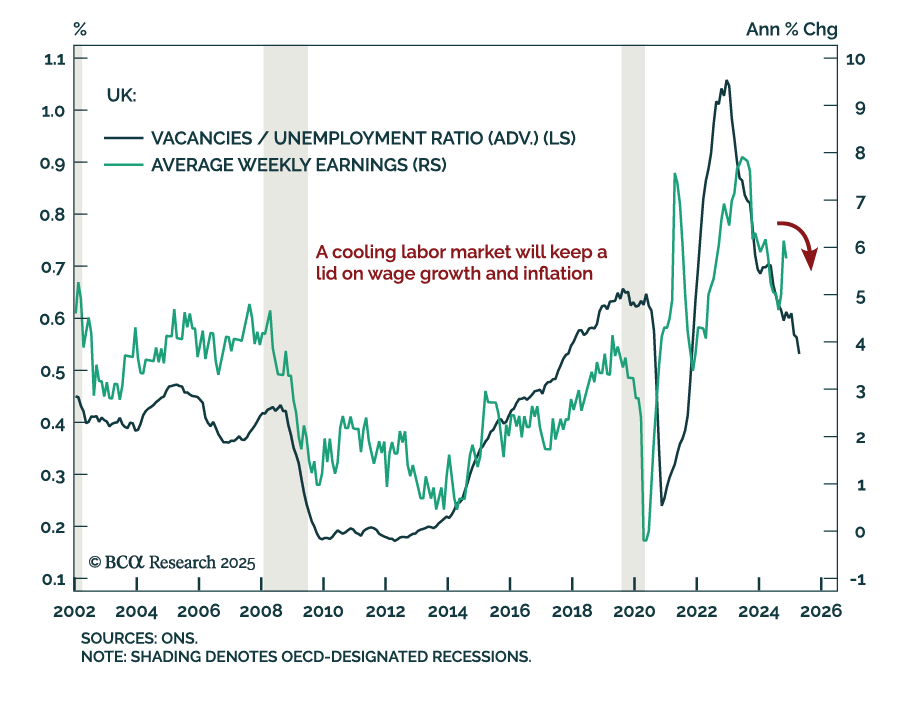

November/December UK employment data was mixed. The November unemployment rate rose 0.1% to 4.4%, in line with expectations. Payrolled employees decreased faster than expected at a 47k pace in December, surpassing the 35k contraction in November. However,…

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

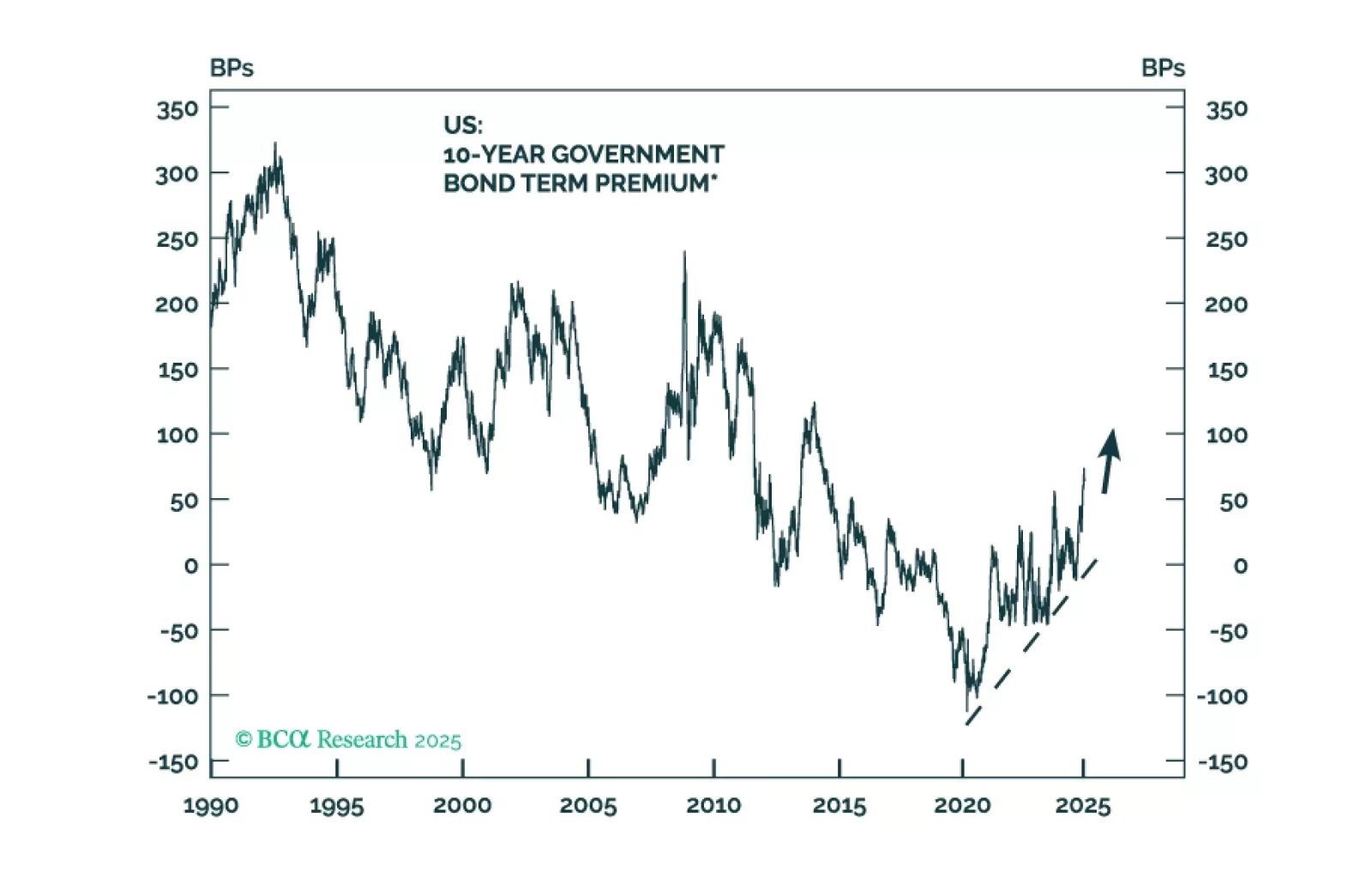

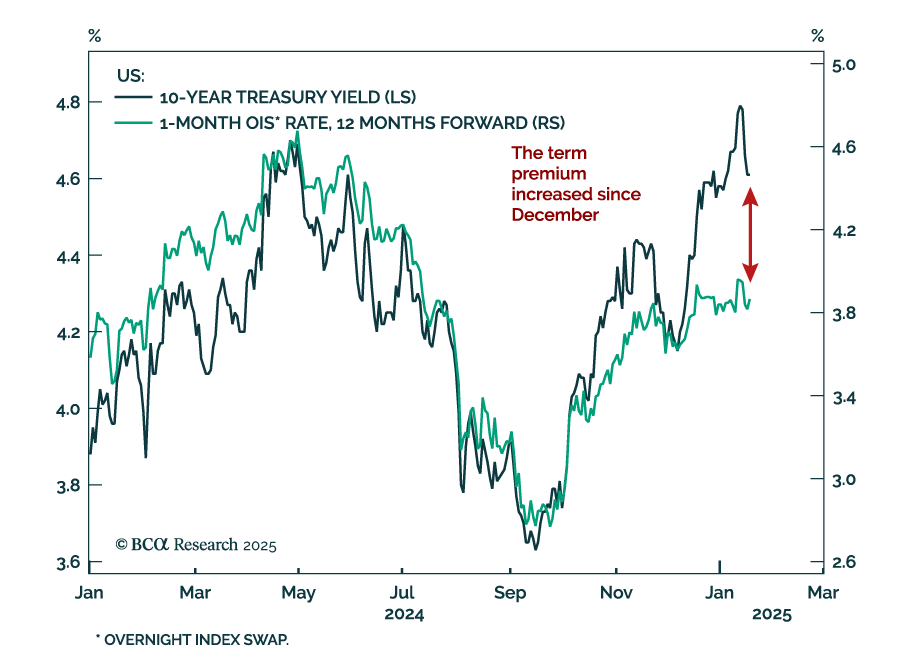

Our US Bond Strategy team put out a Strategy Insight outlining the value they see in the Treasury market. The recent rise in Treasury yields reflects increased inflation uncertainty and a higher term premium. Treasury yields now offer an attractive…

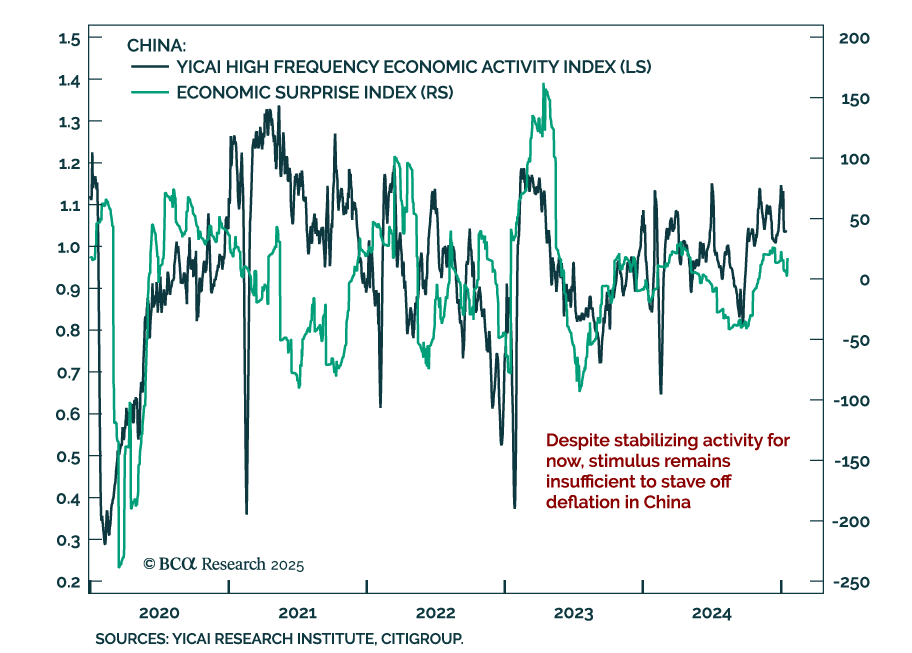

Chinese activity was decent in December, with GDP growth topping the 5% target for 2024. Industrial production growth ticked up to 6.2% y/y from 5.4% in November. Retail sales also picked up, increasing to 3.7% from 3.0% a month prior. New and used home…

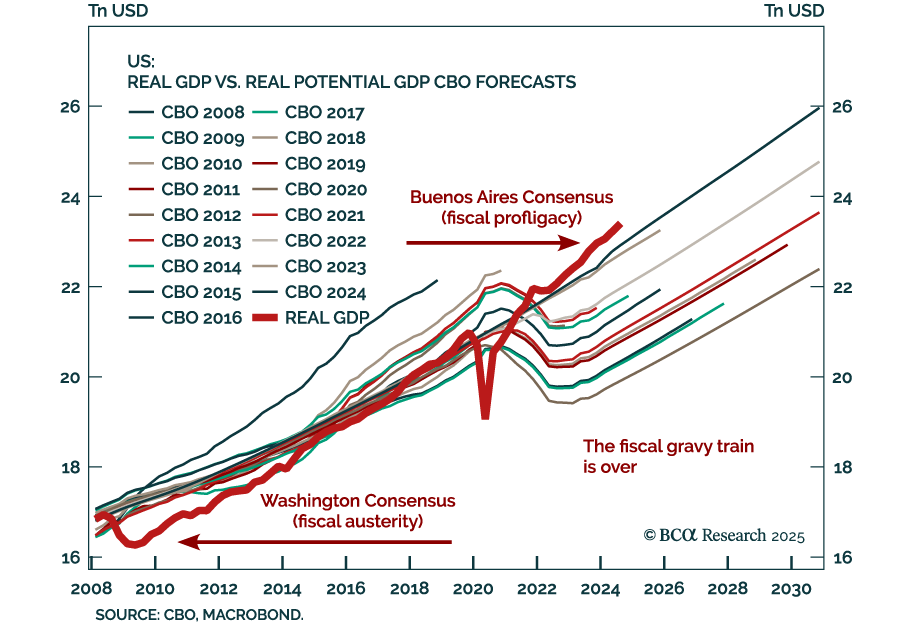

Our Chart Of The Week comes from Marko Papic, Chief Strategist of our GeoMacro Strategy service. Marko has argued that the most important macro story over the past decade has been the transition from the Washington Consensus, promoting fiscal conservatism, to…

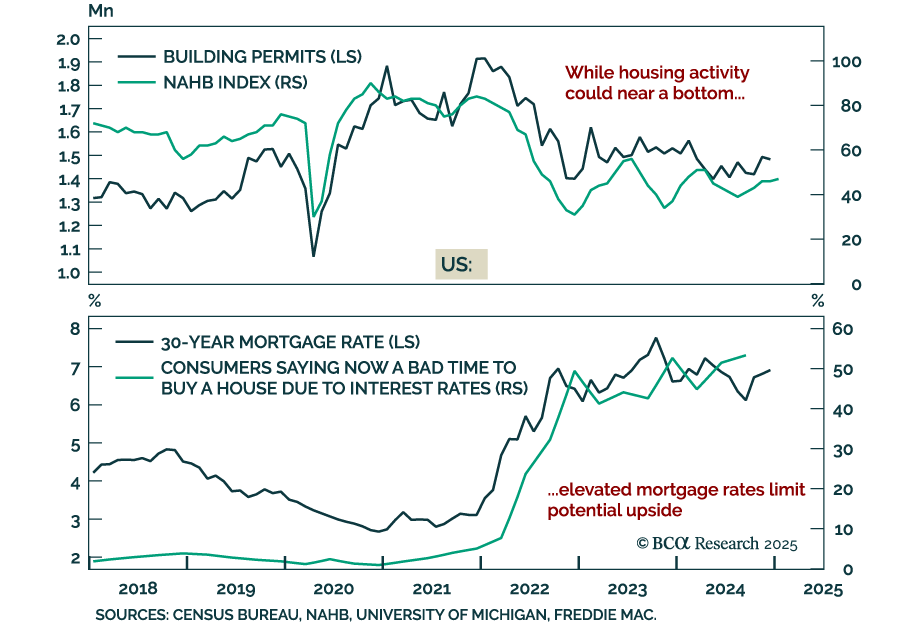

US December housing data was strong, with housing starts printing above estimates at 1.49m, an acceleration from an upwardly-revised 1.29m in November. Building permits also surprised positively at 1.483m, but still decreased from 1.493m a month prior. The…

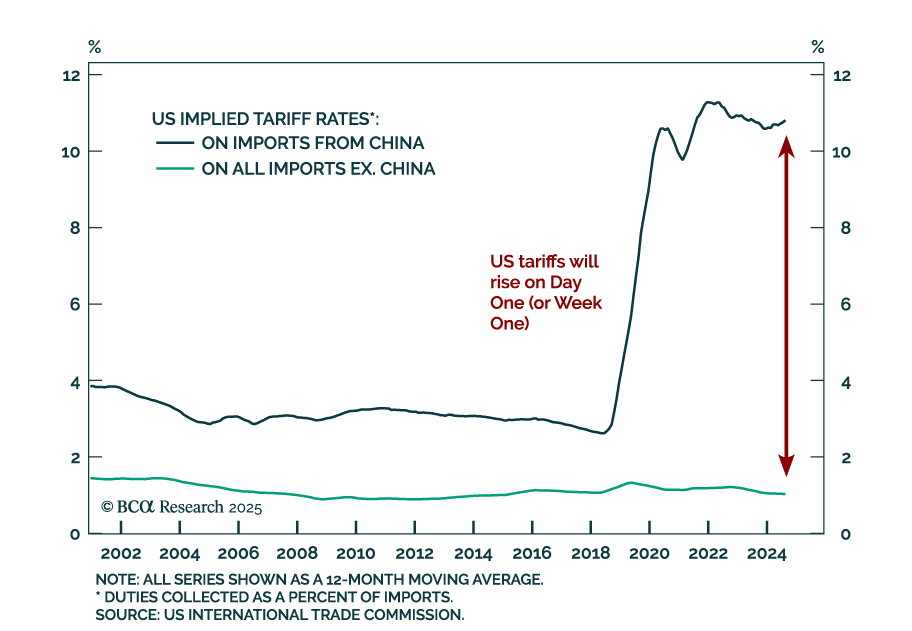

Our US Political strategists published a Special Report on the trade and fiscal policies likely to be implemented on Day One as the Trump administration takes over Washington. Trump is likely to implement significant tariffs early in his term,…

We examine Treasury market valuation and look for indicators that could help us time the next peak in yields. We also update the forecasts from our Treasury yield model.