Policy

Goods prices have been normalizing following the pandemic binge on goods spending. The May CPI release indicated that durable goods and nondurable goods prices both continued to contract. Investors and policymakers have thus turned their attention to other…

According to BCA Research’s Counterpoint service, job losers not on temporary layoff (‘bad’ unemployment) will need to rise further for the Fed to reach its 2 percent inflation target. Although prime-age participation has surged, the participation of older…

Our reaction to this morning’s CPI report and this afternoon’s FOMC meeting.

On Wednesday, the European Commission announced it would impose tariffs ranging between 17% and 38% on imports of Chinese EVs starting next month. These duties will be applied on top of existing 10% across-the-board tariffs on all Chinese EV imports, and…

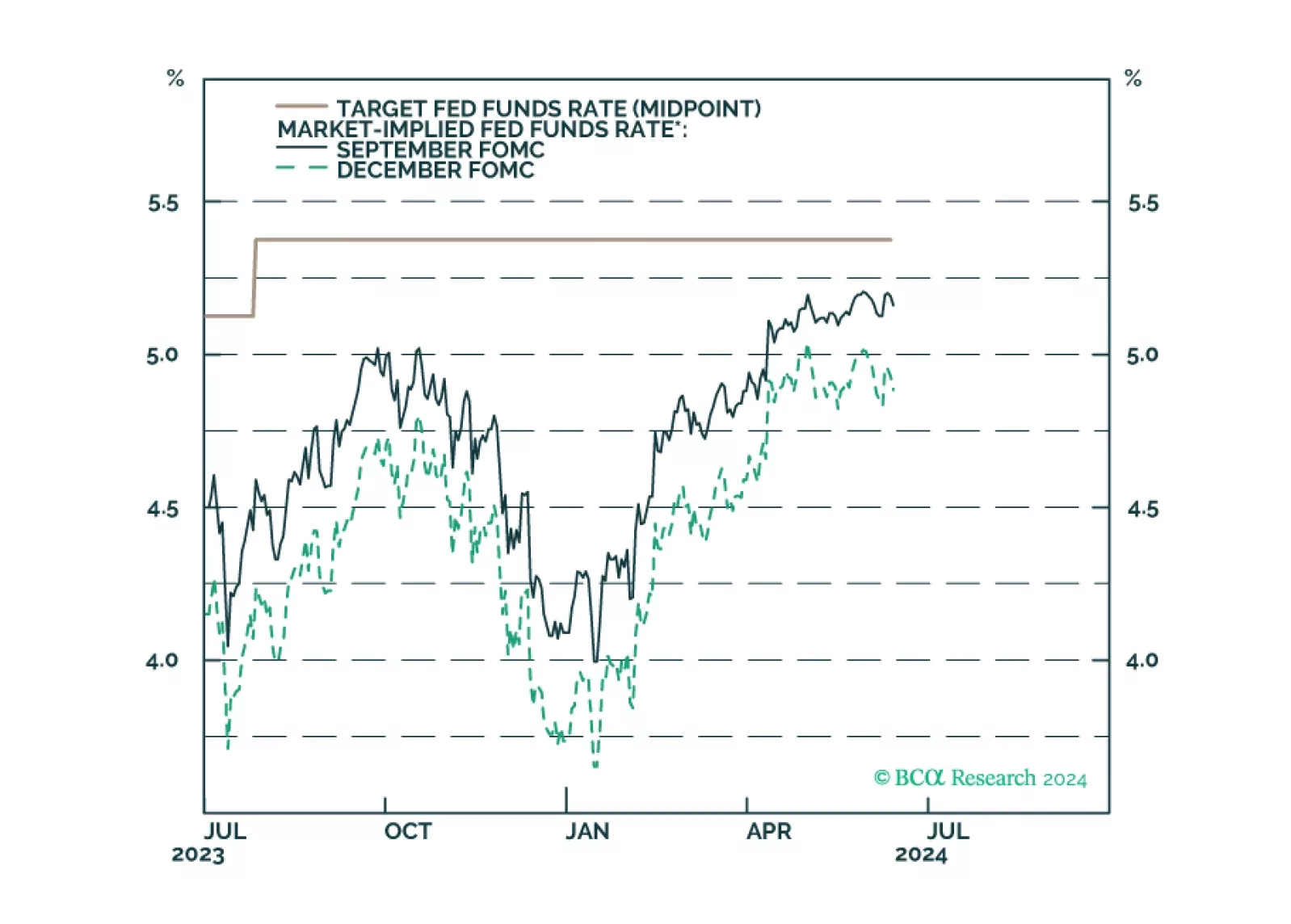

In a widely expected move, the Fed kept its policy rate unchanged within a 5.25%-5.5% range following its June 11-12 meeting. However, the median dots have moved higher for both 2024 and 2025. The median FOMC member now expects to cut only once this year…

US CPI inflation continued to ease in May. Headline CPI stagnated on a month-on-month basis (3.3% y/y) in May, down from April’s 0.3% m/m (3.4% y/y), and below expectations of a more muted rate of growth. Core CPI also slowed more than expected, rising…

The Bank of Japan exited negative interest rate policy in March, but subsequent softer-than-expected CPI inflation prints have complicated its path towards tightening. The central bank is widely expected to stay put when it meets this week. Governor Kazuo…

According to BCA Research’s China Investment Strategy service, it is an overstatement to assert that China’s subsidies are the main driver of its green energy industries’ competitiveness. It is commonly perceived that China heavily subsidizes its industry…

The UK unemployment rate surprised to the upside in the 3-month period ending in April, ticking up to 4.4% against expectations it would remain stable at March’s originally reported 4.3%. Concurrently, wage growth remains elevated. The 3-month measure of…

According to BCA Research’s Geopolitical Strategy service, the European parliamentary election was not an earthquake. It saw an improvement in right-leaning political groups and a deterioration in both centrist and left-leaning groups, as expected. …