Policy

A few preliminary measures of German inflation for April were released on Monday. The month-on-month headline inflation measure came in at 0.5% an increase from last month’s reading of 0.4% but below expectations of 0.6%. Meanwhile the year-on-year version…

The trimmed mean PCE was released on Friday by the Dallas Fed. This measure removes the top 31% of items with the highest inflation and the bottom 25% of items with the lowest inflation within the PCE basket. Historically, it has served as an accurate gauge…

EUR/USD has fallen by almost 5% since July last year. There are fundamental reasons why this move has taken place. The US economy has shown significant more resilience than the European one. Consumption continues to be strong, and GDP is still growing at a…

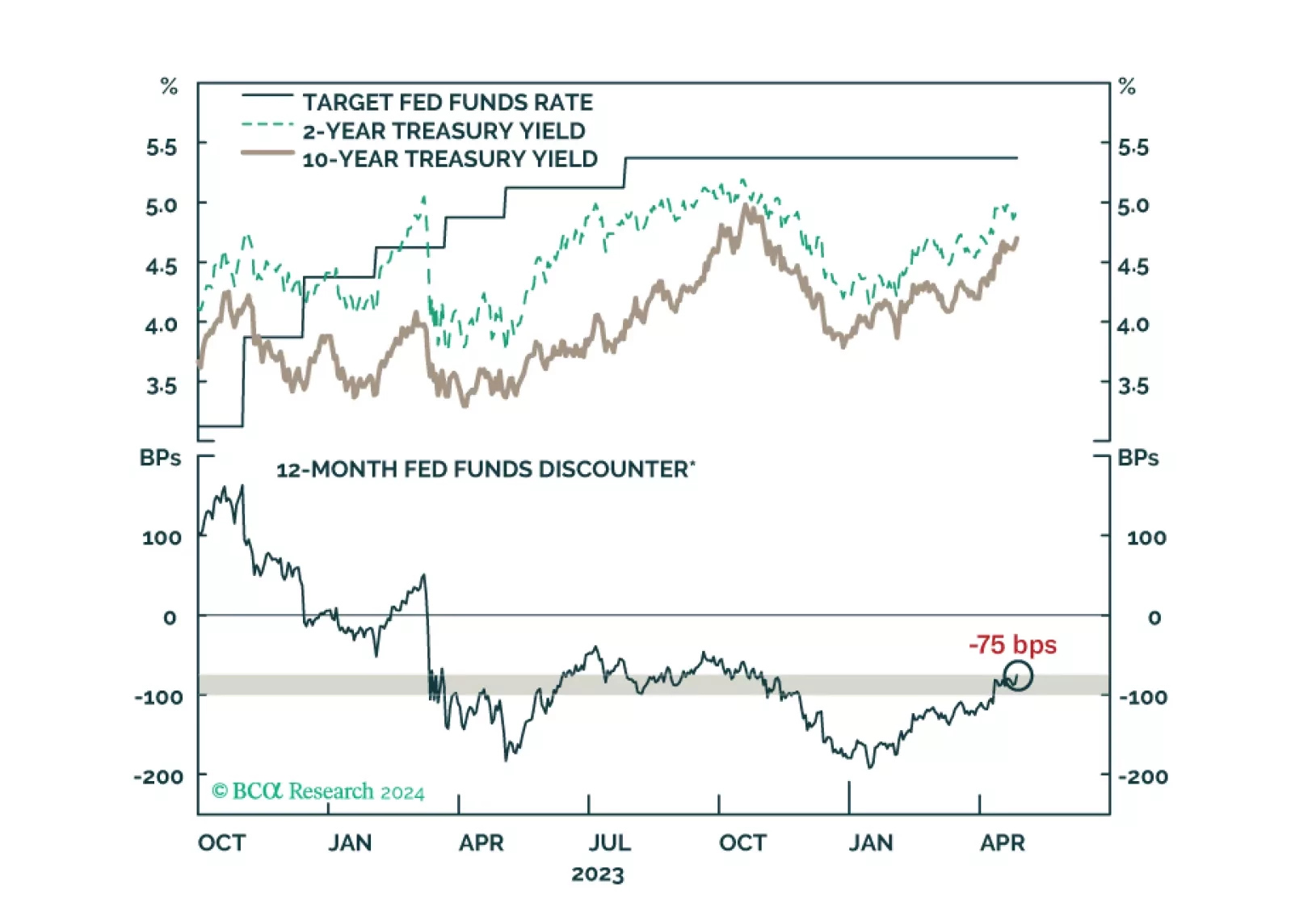

According to BCA Research’s US Bond Strategy service, the May FOMC meeting is unlikely to cause a stir in fixed income markets. The Fed will hold an FOMC meeting next week and while it will not update its economic or interest rate projections, we will be…

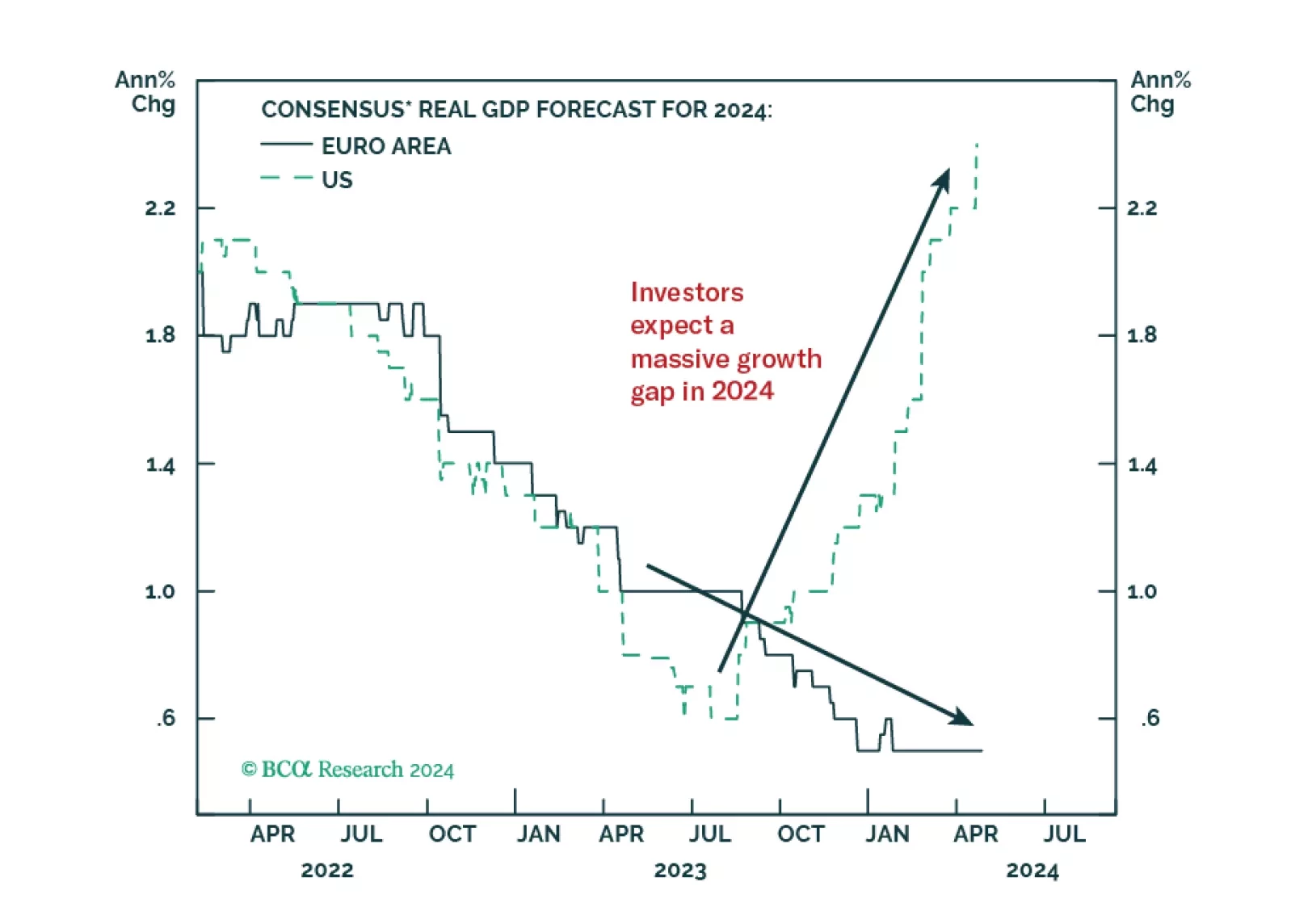

Investors anticipate a record growth gap between the US and the Eurozone in 2024. Does this skewed expectation create market opportunities?

The latest edition of our Big Bank Beige Book suggests the expansion remains intact, though weakness in C’s private-label credit card portfolio could be a harbinger of distress among lower-income consumers. We remain tactically neutral with a bias to turn defensive once clearer signs of a recession emerge.

The Tokyo inflation release for April came in on the soft side on Friday, with every single metric coming in below expectations. Tokyo headline inflation declined from 2.6% y/y to 1.8% y/y, versus expectations of a much more muted decline to 2.5% y/y.…

The Canadian dollar typically has two main drivers: interest rate differentials and commodity prices, especially oil prices. However, the relationship between the CAD and oil has broken down recently. As our FX strategists have highlighted, the key reason for…

According to BCA Research’s Global Fixed Income Strategy service, a hard landing is the only way to solve the UK inflation problem. Sticky inflation and lingering inflation pressures have made the BoE’s job much more challenging. The UK economy weakened in…

Our latest views on the recent increase in Treasury yields and some key things to watch at next week’s FOMC meeting.