Sectors

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.

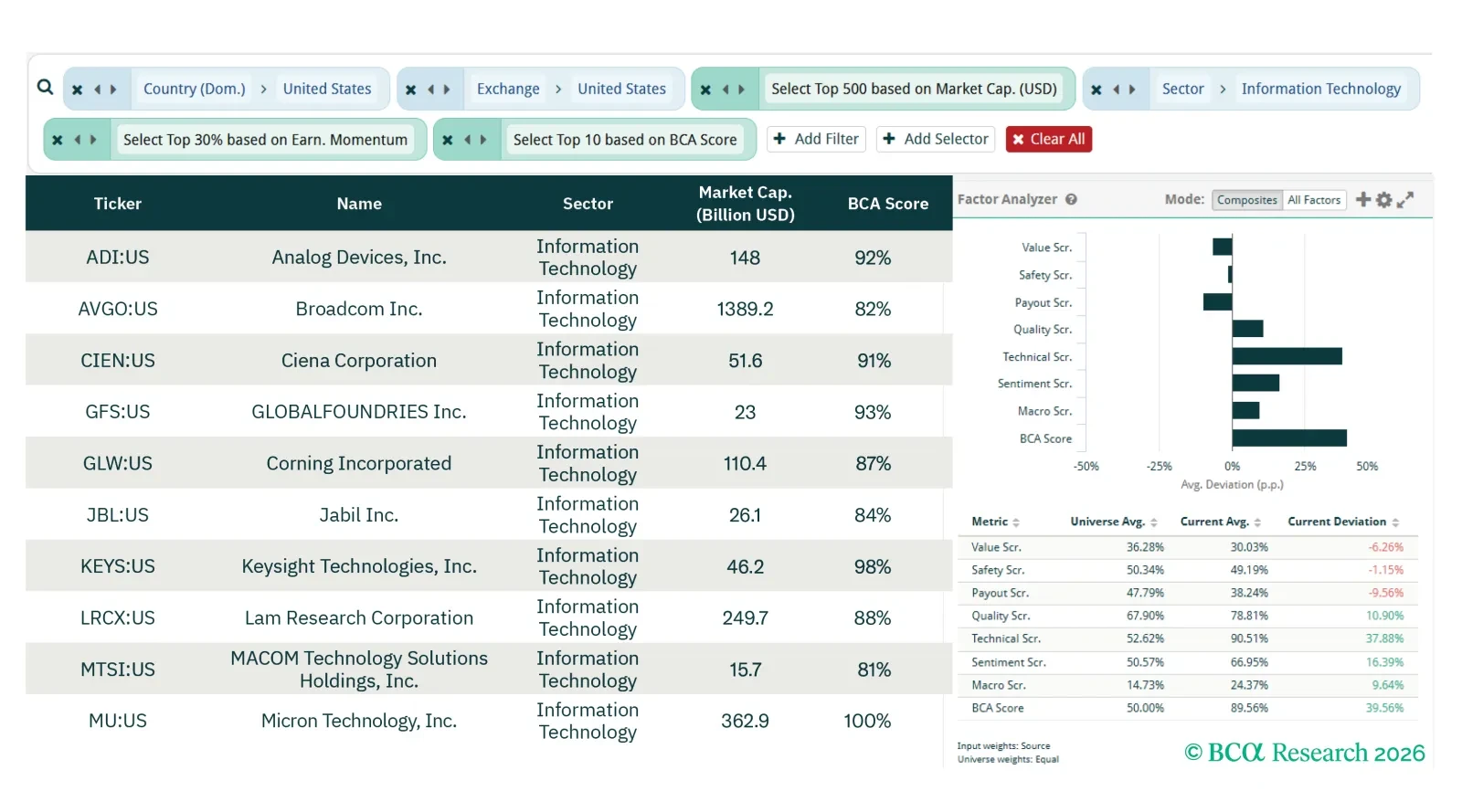

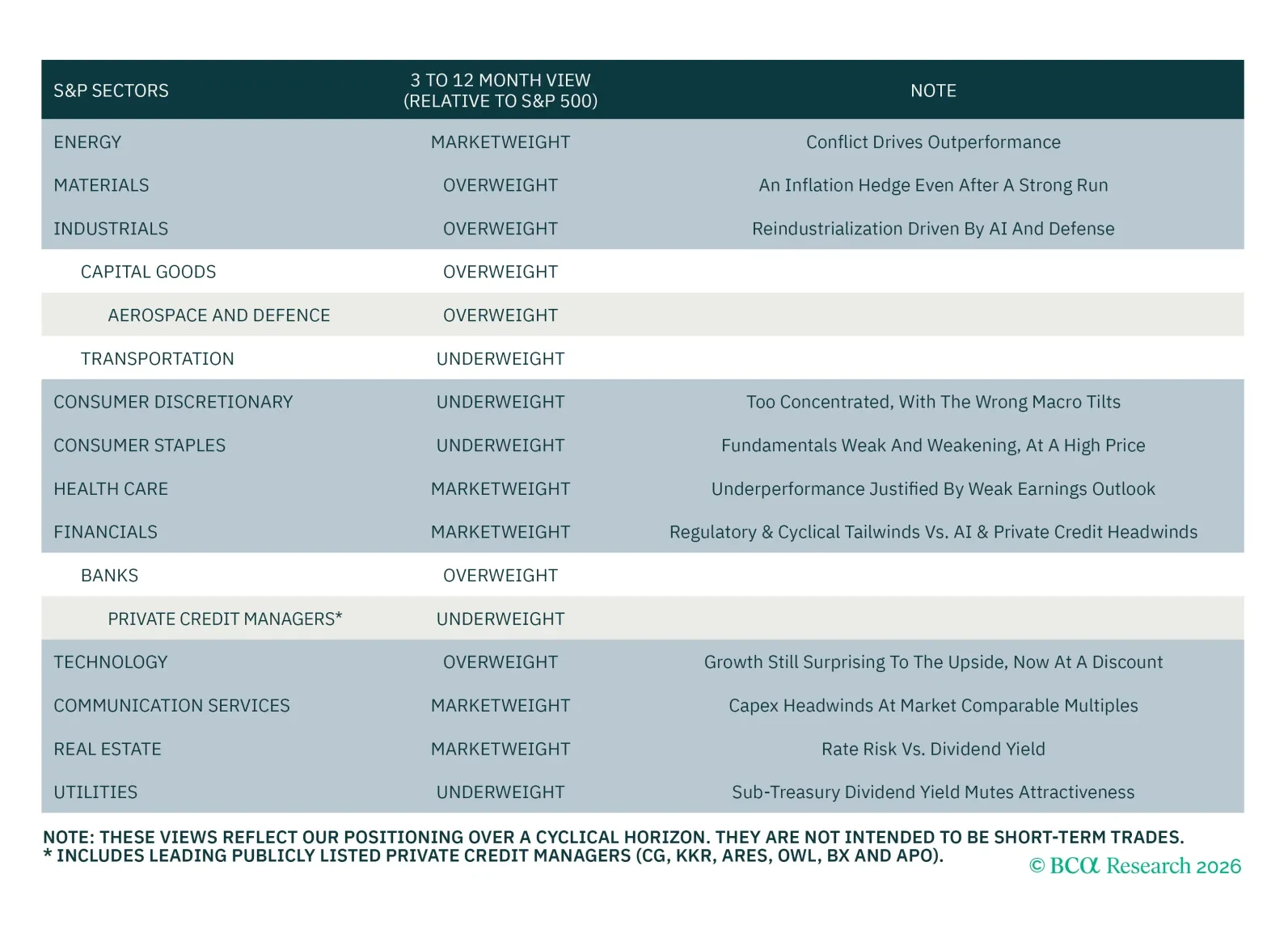

This screener report builds on the US Equity Strategy team's sector view published on 30 March 2026, where the team overweights Information Technology, Industrials, and Materials on a 3- to 12-month horizon. Here we utilize our screening tools to layer bottom-up stock selection onto their top-down sector views.

We continue to expect the S&P 500 to gain ground in 2026, driven by revenue growth, with limited scope for margin or multiple expansion. With cyclical upside tilted toward the investment side of the economy, we favor sectors with high-quality, revenue-driven earnings growth, leverage capex, and valuations that leave room for catch-up.

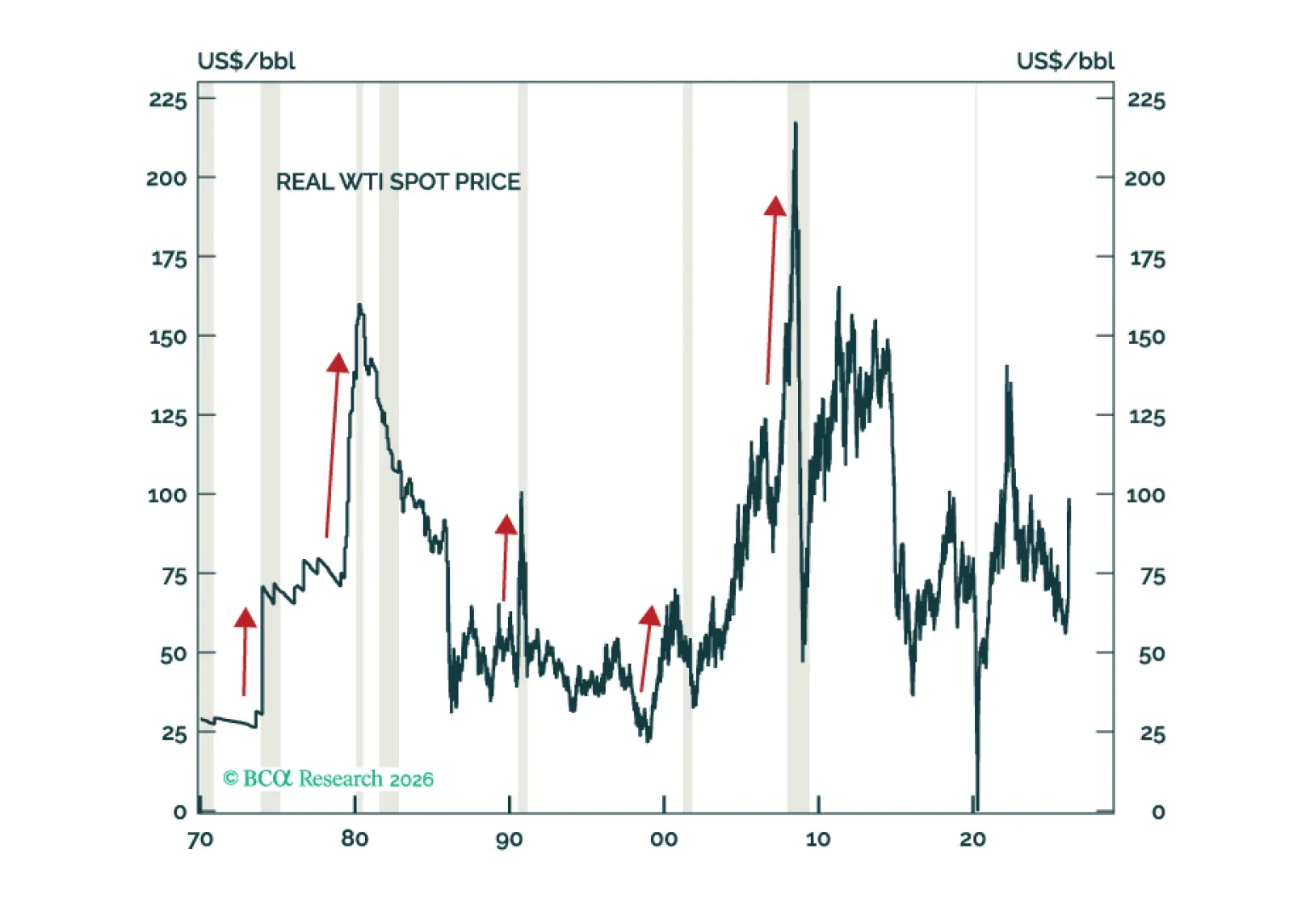

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

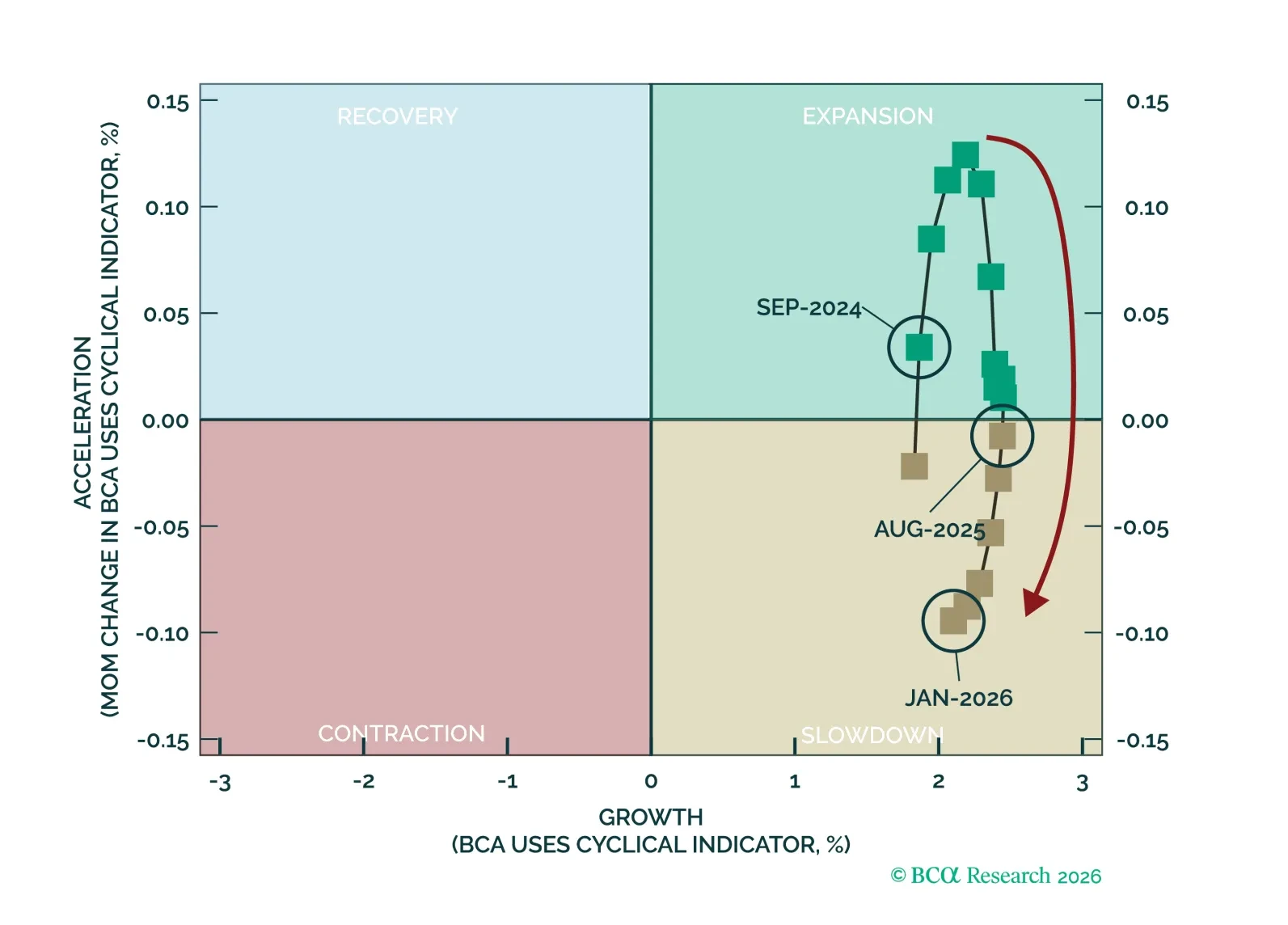

This screener report builds on the US Equity Strategy and Equity Analyzer collaboration published on 23 February 2026, where we introduced our latest framework for assessing the US business cycle. Here, we apply the framework to our screener to identify how bottom-up equity positioning should adapt as the cycle evolves.

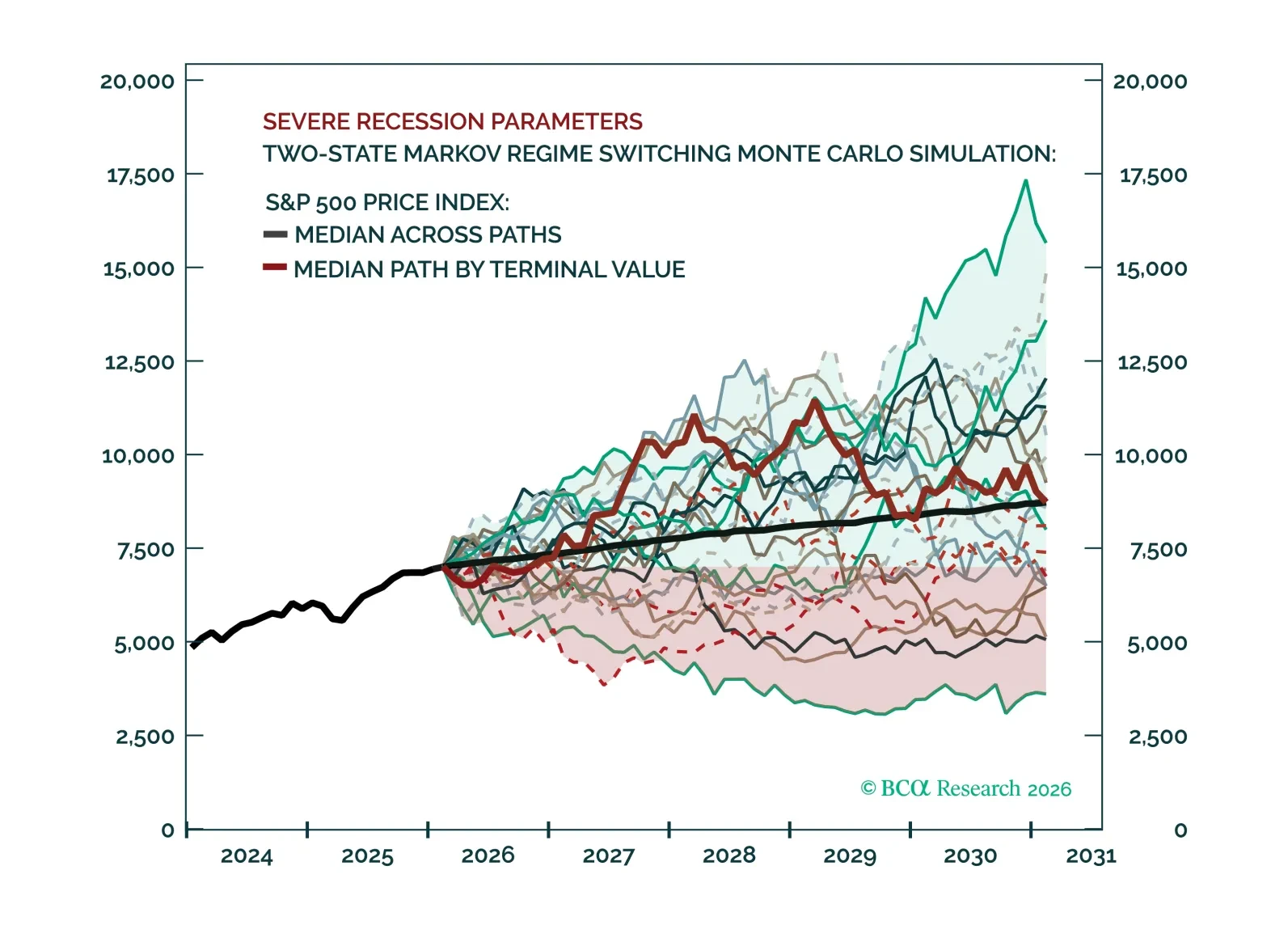

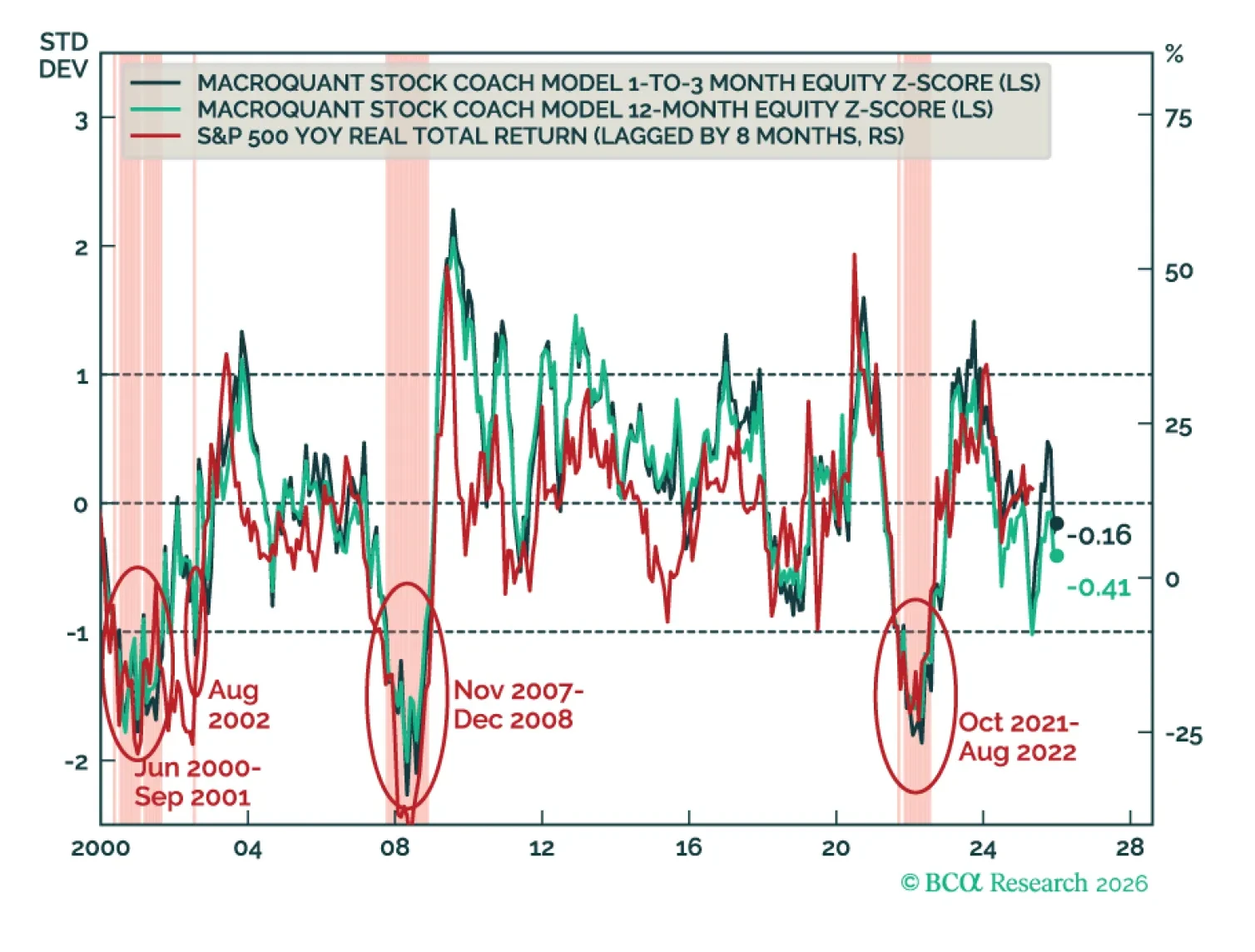

Recessions are inevitable but unpredictable. While earnings drive long‑term equity performance through the cycle, around turning points fundamentals follow a predictable sequence: multiples contract first, then prices, then earnings. Recessions can shift sector leadership, but simulations show that medium‑term index‑level upside remains intact unless future downturns are materially more severe than in history.

MacroQuant recommends a modest overweight position in equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has downgraded oil to neutral, and is bullish on copper and gold.

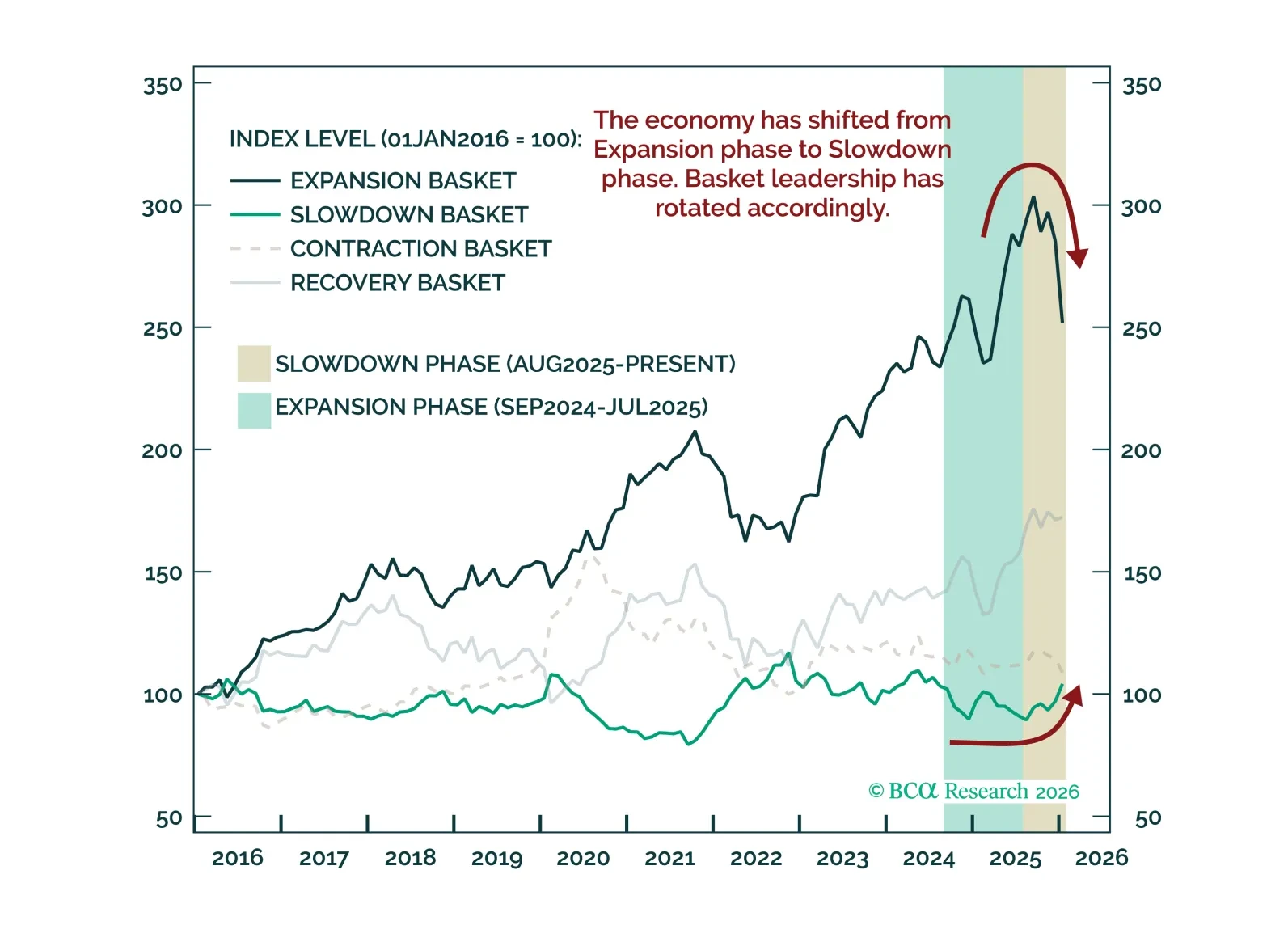

The US economy is in the Slowdown phase of the business cycle, according to our measure of aggregate US economic activity; growth remains positive but acceleration is negative. Historically, this phase more often resolves in reacceleration than recession. Recent market price action, from the index, to sectors, to relative industry performance, broadly reflects typical Slowdown phase dynamics.

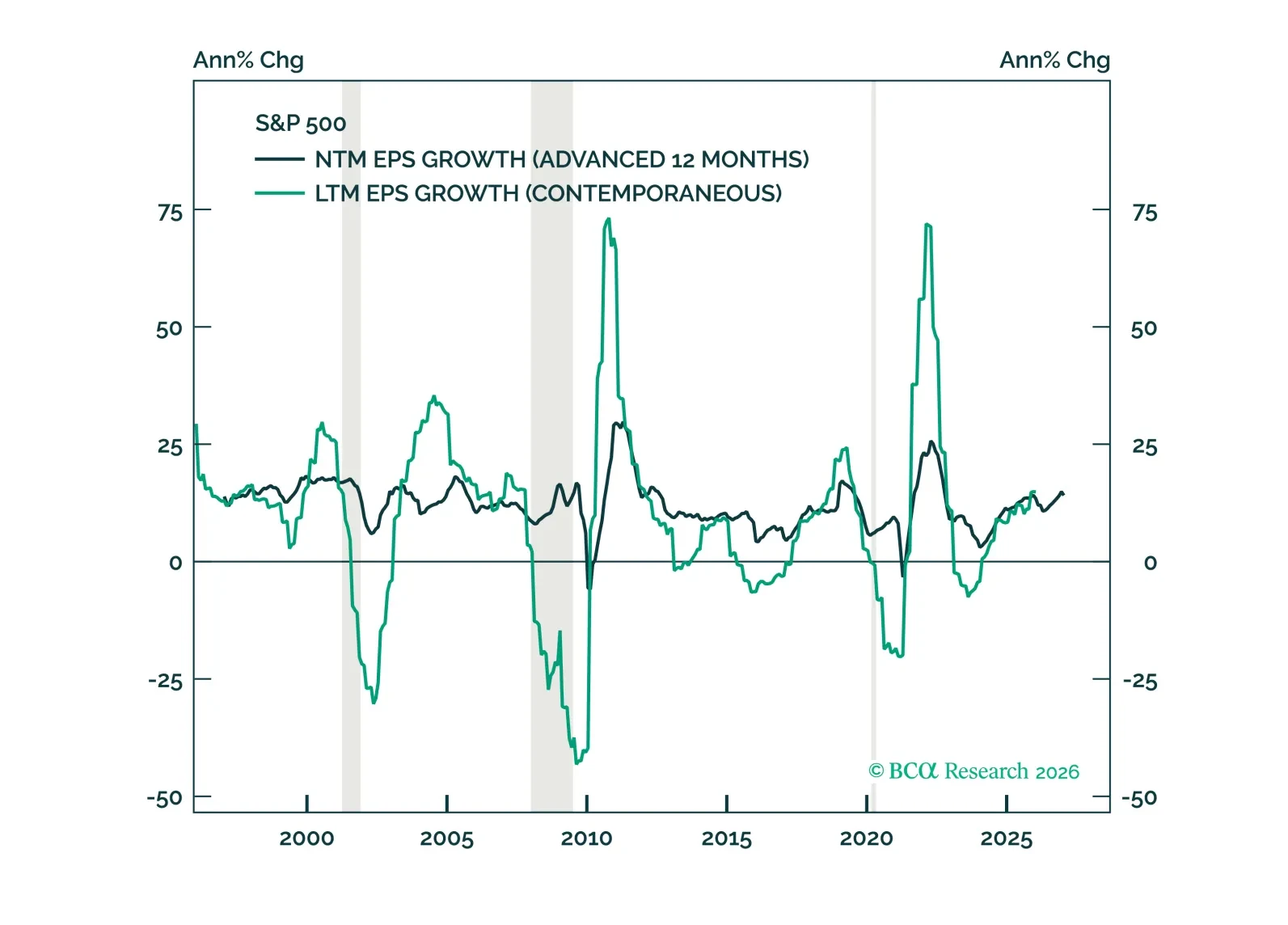

Earnings strength, durability, and breadth are all improving. As the market transitions from multiple-driven to earnings-driven returns, this backdrop supports continued gains in 2026—but with less concentration and greater scope for laggards to catch up rather than leaders to roll over.

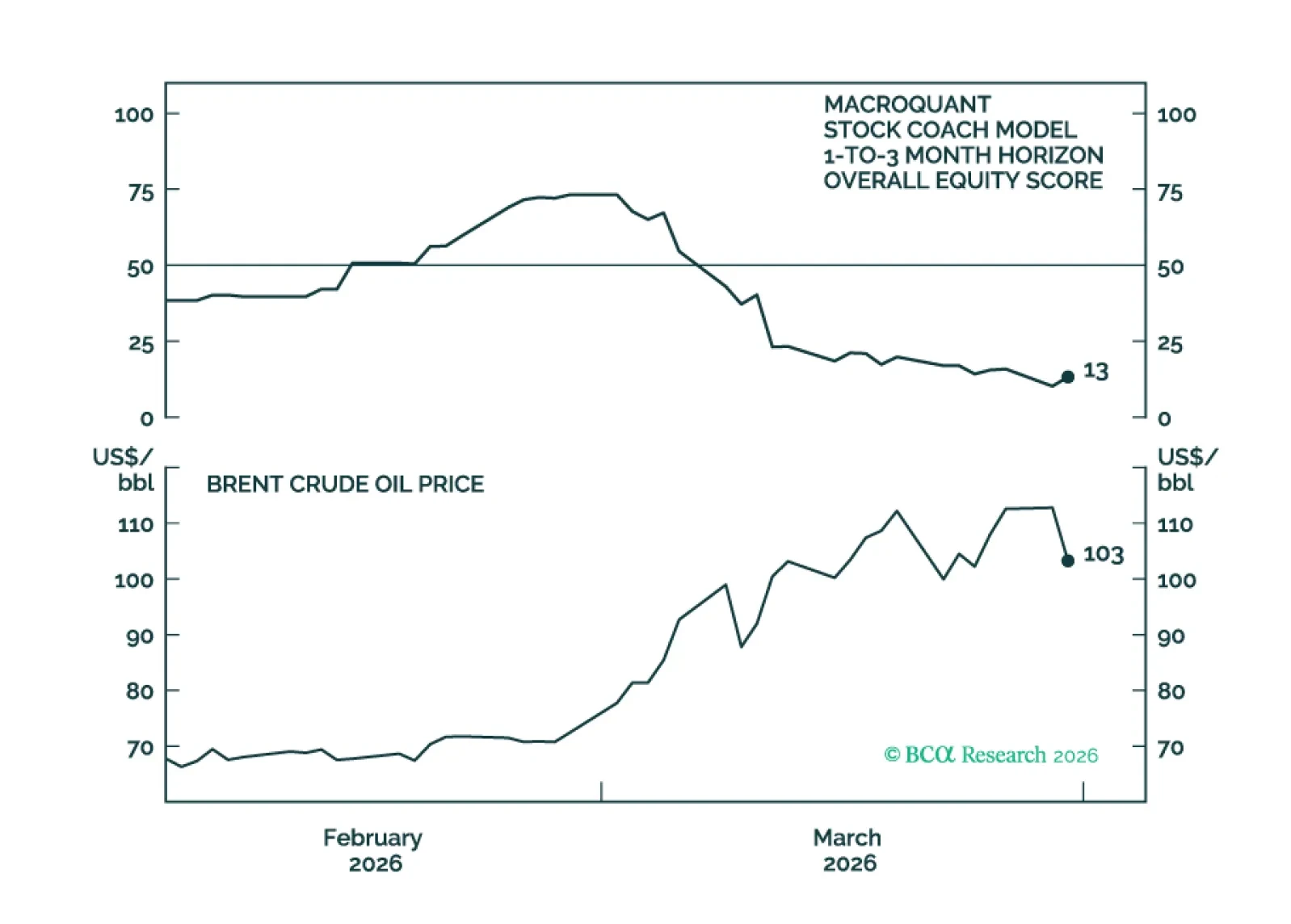

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.