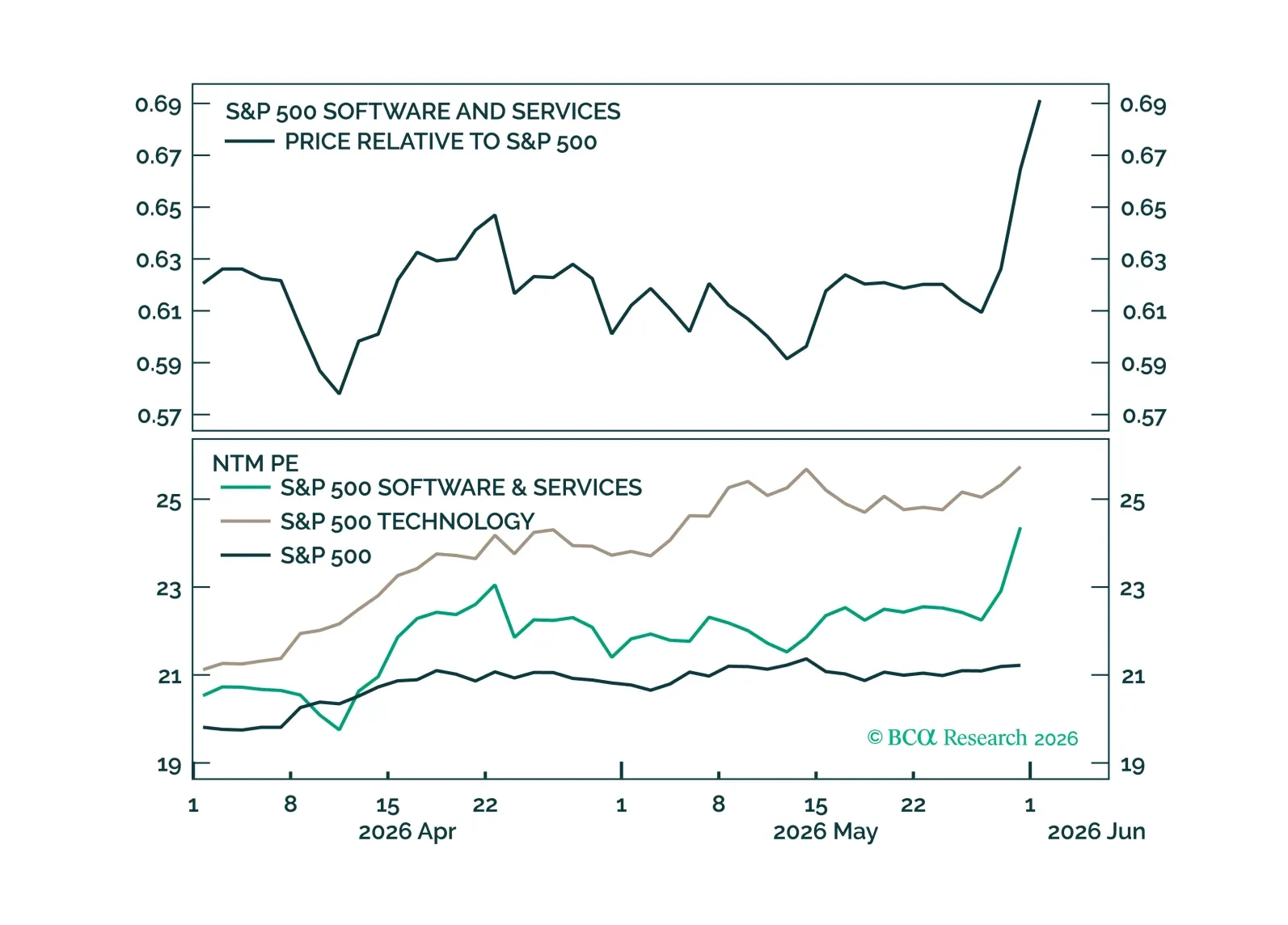

Software and Services

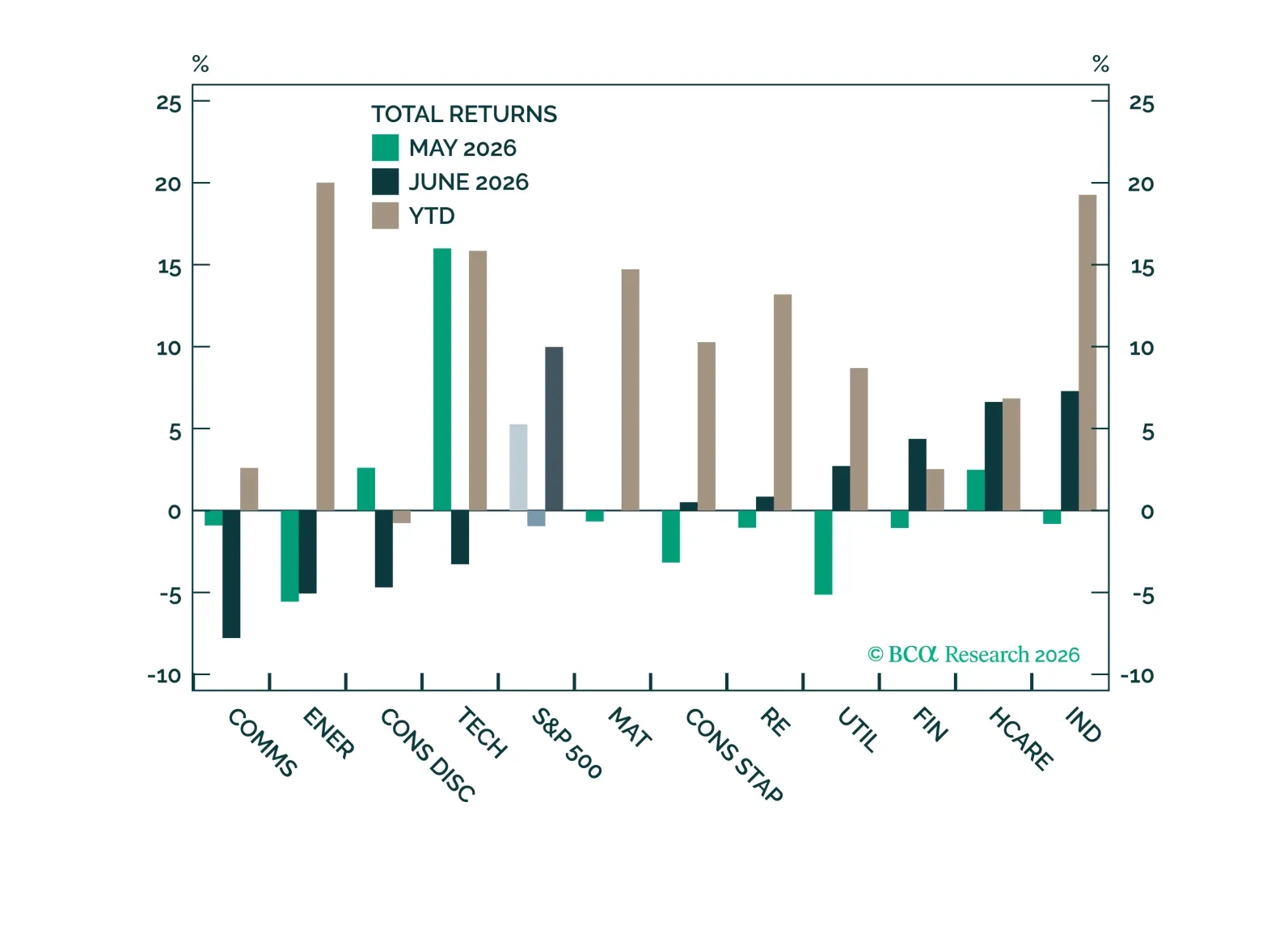

S&P 500 performance rotated in June, but fundamental growth remains strong across sectors, with earnings and revenue growth extending well beyond the largest mega-cap companies.

The US economy is moving back toward Expansion, supported by strong investment, improving earnings, and record margins. We are taking profits on our tactical Software long after achieving our target and rotating into Materials, where commodity strength and earnings momentum continue to support the sector.

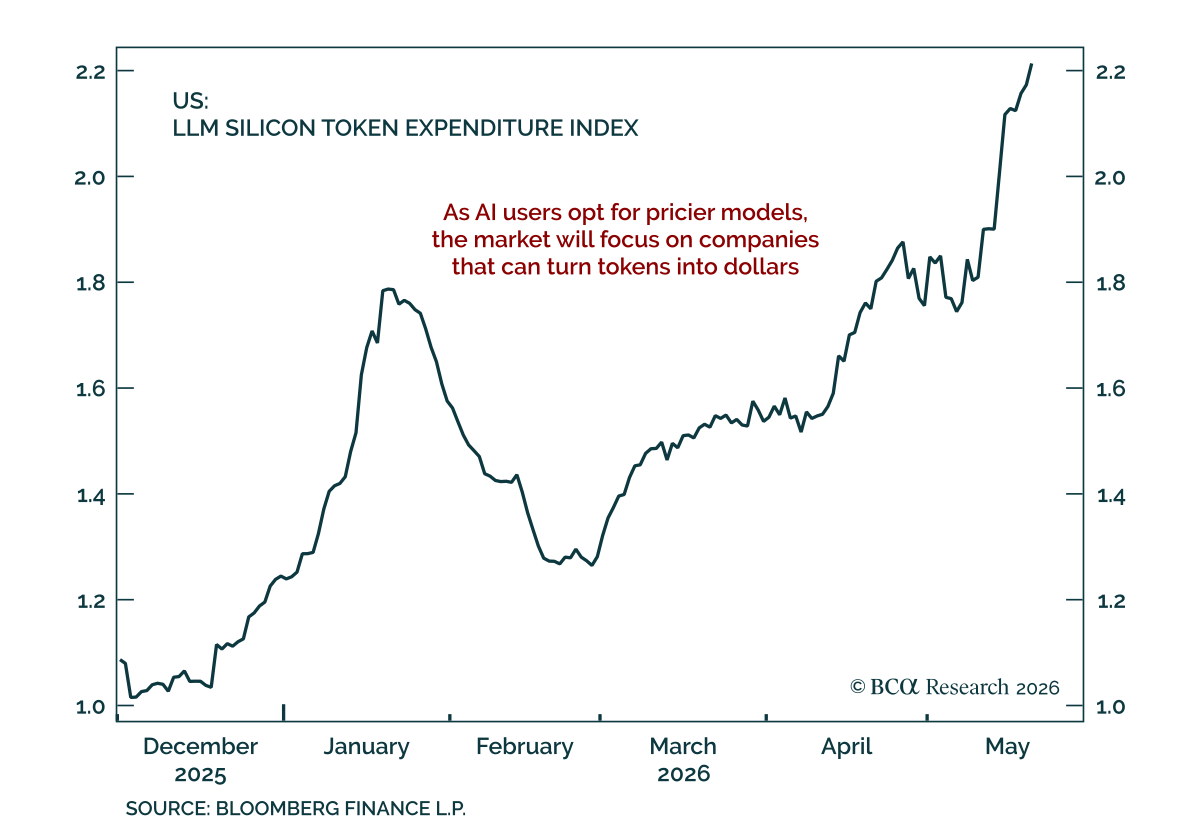

So far most of the value in the AI supply chain has been captured by hardware companies. However, as model providers shift to usage-based pricing, value will begin to accrue to models and applications. Communications Services and Software should benefit from this shift. This broadening of the AI story, along with solid economic momentum should keep the rally going for the rest of the year. Remain overweight equities. Downgrade Energy to Neutral. Buy Software.

Everyone has opinions on Private Credit, but few have the data, and fewer have the objectivity. We give you both. In under 5 minutes, you will understand how we got here and, more importantly, how to allocate from here.

India's IT service exports have been booming and will continue to do so despite wider AI usage. Indian IT stocks, however, will not benefit from it as the expanding Global Capability Centers (GCCs) in India compete with the nation’s IT companies, driving the latter's profitability down.

Cybersecurity is a strategic investment theme, which looks particularly interesting in light of the trade war and heightened geopolitical tensions. It is less exposed to tariffs than other industries and, if anything, benefits from geopolitical tensions as customers seek protection from international cyberattacks and cybercrime. The industry’s fundamentals are improving, while valuations are moderating. A recent pullback presents an attractive entry point into the theme.