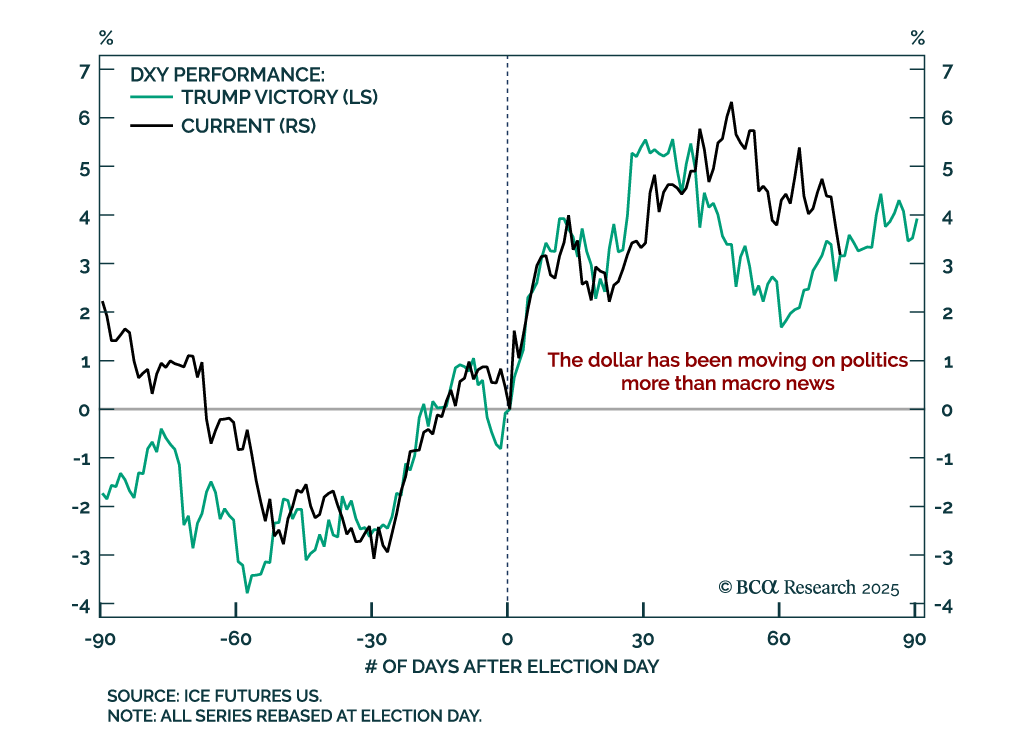

US Dollar

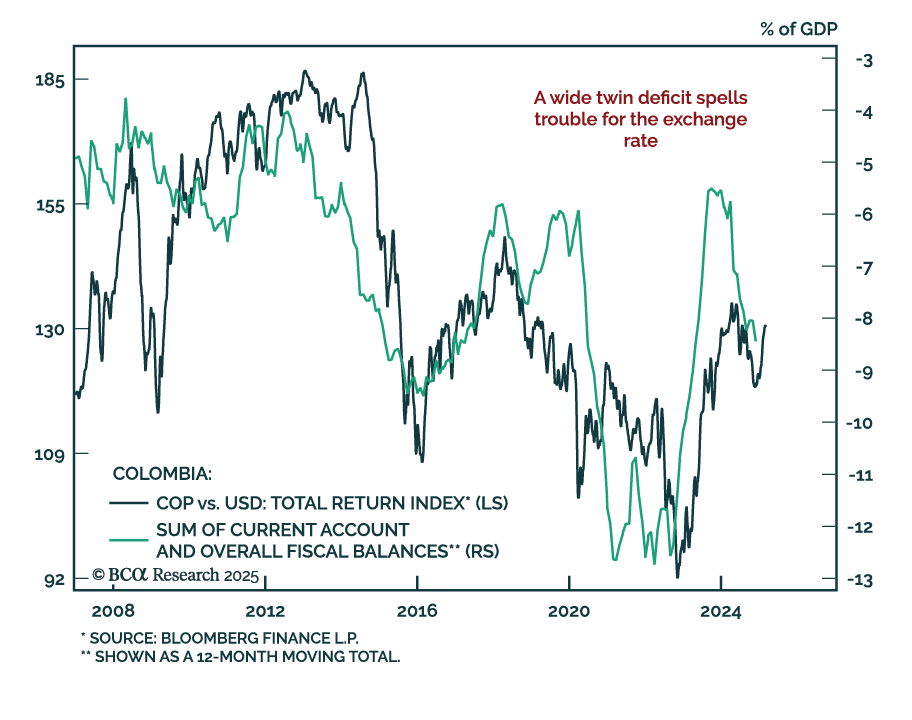

Our Emerging Markets strategists assessed Colombian assets after a significant rally. Colombia faces deep-rooted macroeconomic challenges that will not be easily reversed by a right-wing government in 2026. Public debt is on an unsustainable path, with…

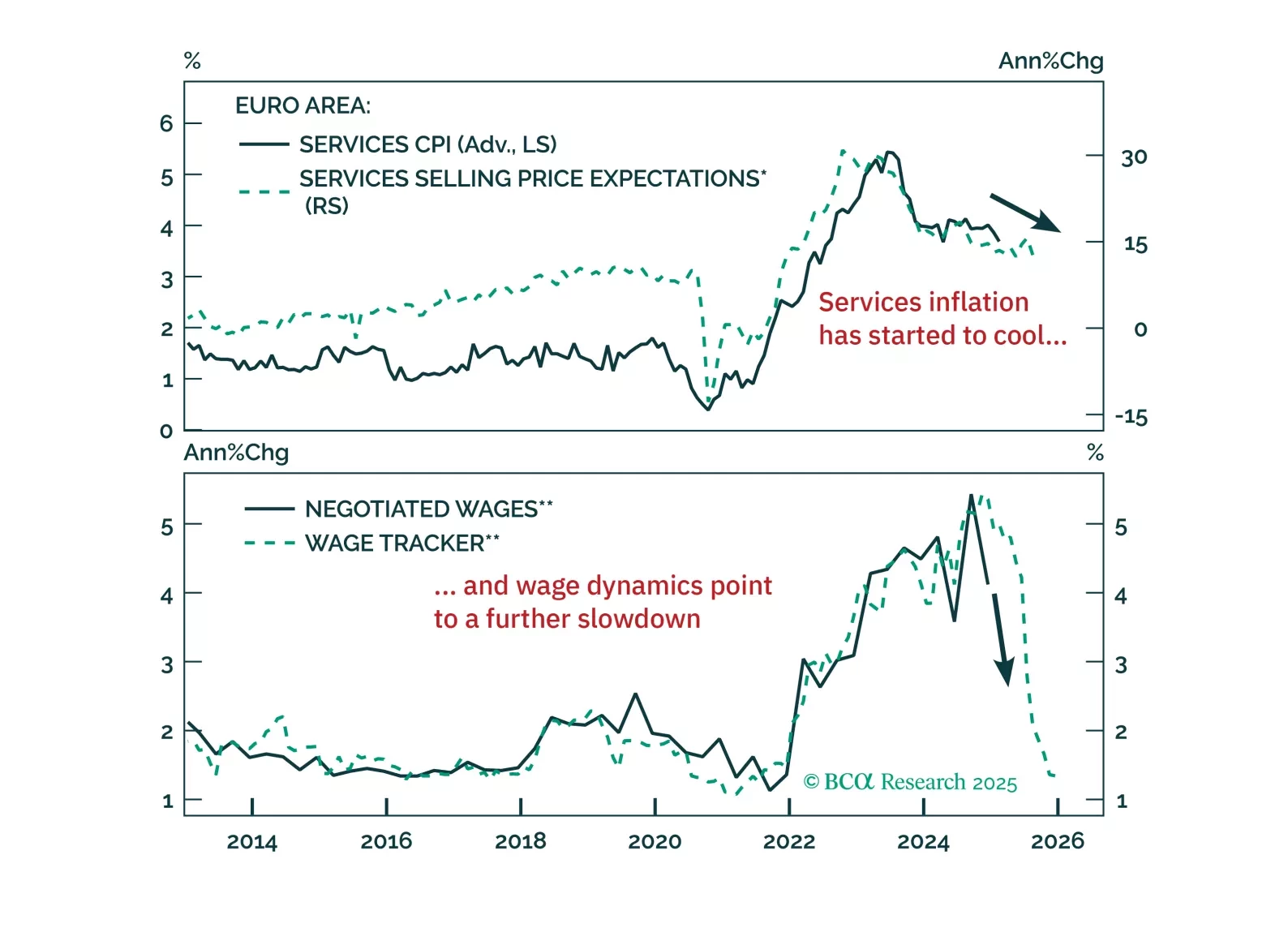

The ECB cut rates as expected, but rising yields and a stronger euro are tightening financial conditions just as fiscal policy shifts the macro landscape. With more rate cuts ahead and market positioning stretched, we outline the key risks, investment opportunities, and our updated call on the ECB’s terminal rate. Read our full report for actionable insights.

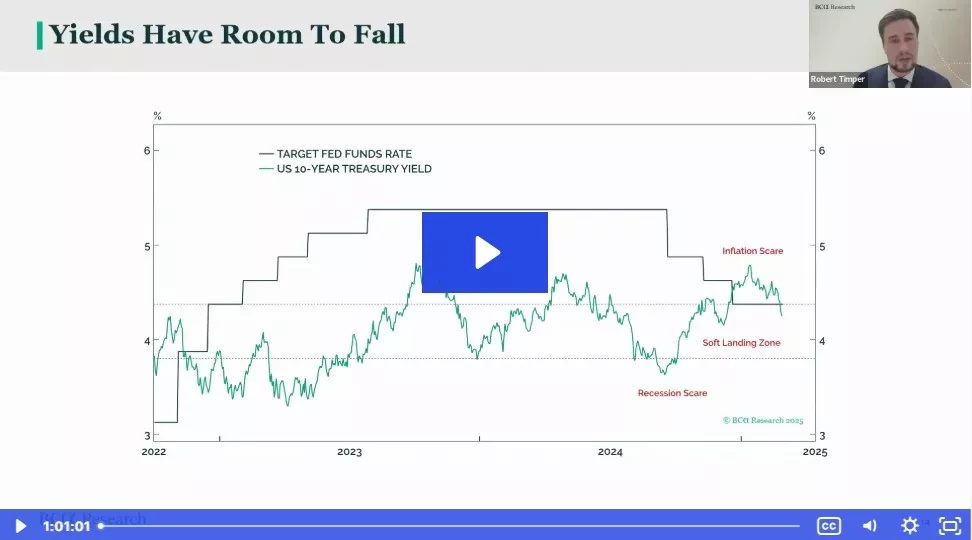

Please join FX and Global Fixed Income Strategist Chester Ntonifor and Associate Strategist Robert Timper for a Webcast on Thursday, February 27, at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET).

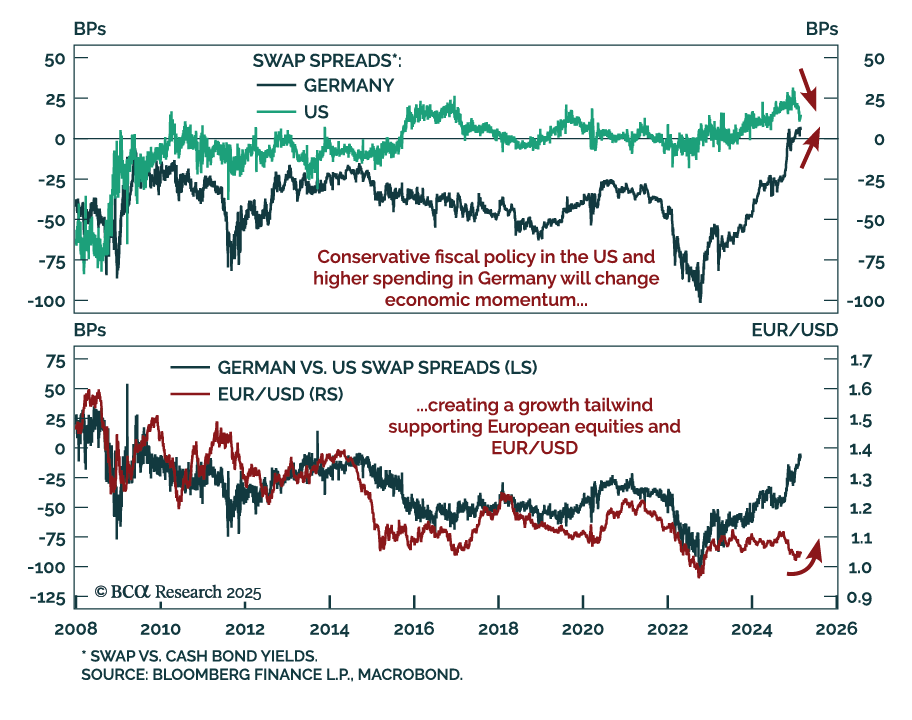

German election results were roughly as expected, but Europe’s biggest economy suddenly just got more interesting. While the details of the governing coalition have yet to be finalized, Chancellor Merz has floated options to ease the “debt brake”, which…

The February Ifo Business Climate index for Germany slightly missed estimates, staying unchanged from 85.2 in January. While respondents’ assessment of the current situation weakened, expectations rebounded to 85.4 from 84.3. The improvement in…

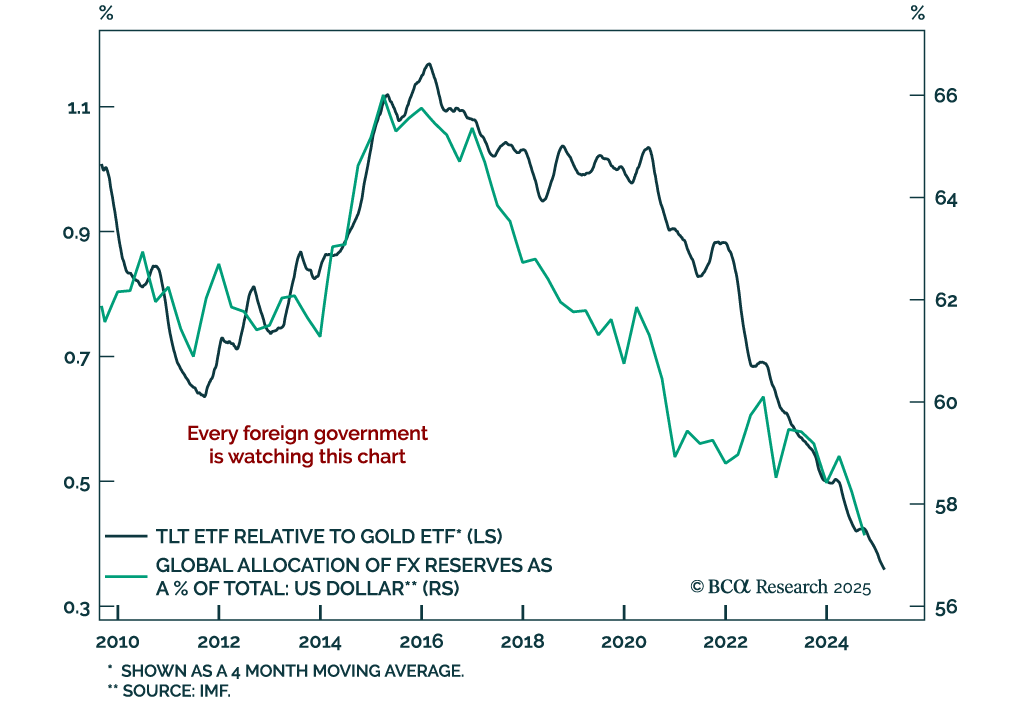

Our Chart Of The Week comes from Chester Ntonifor, Chief Strategist for our Foreign Exchange and Global Fixed Income Strategy services. A big macro trade over the last few years has been to shun US Treasuries, in favor of gold. The key driver has…

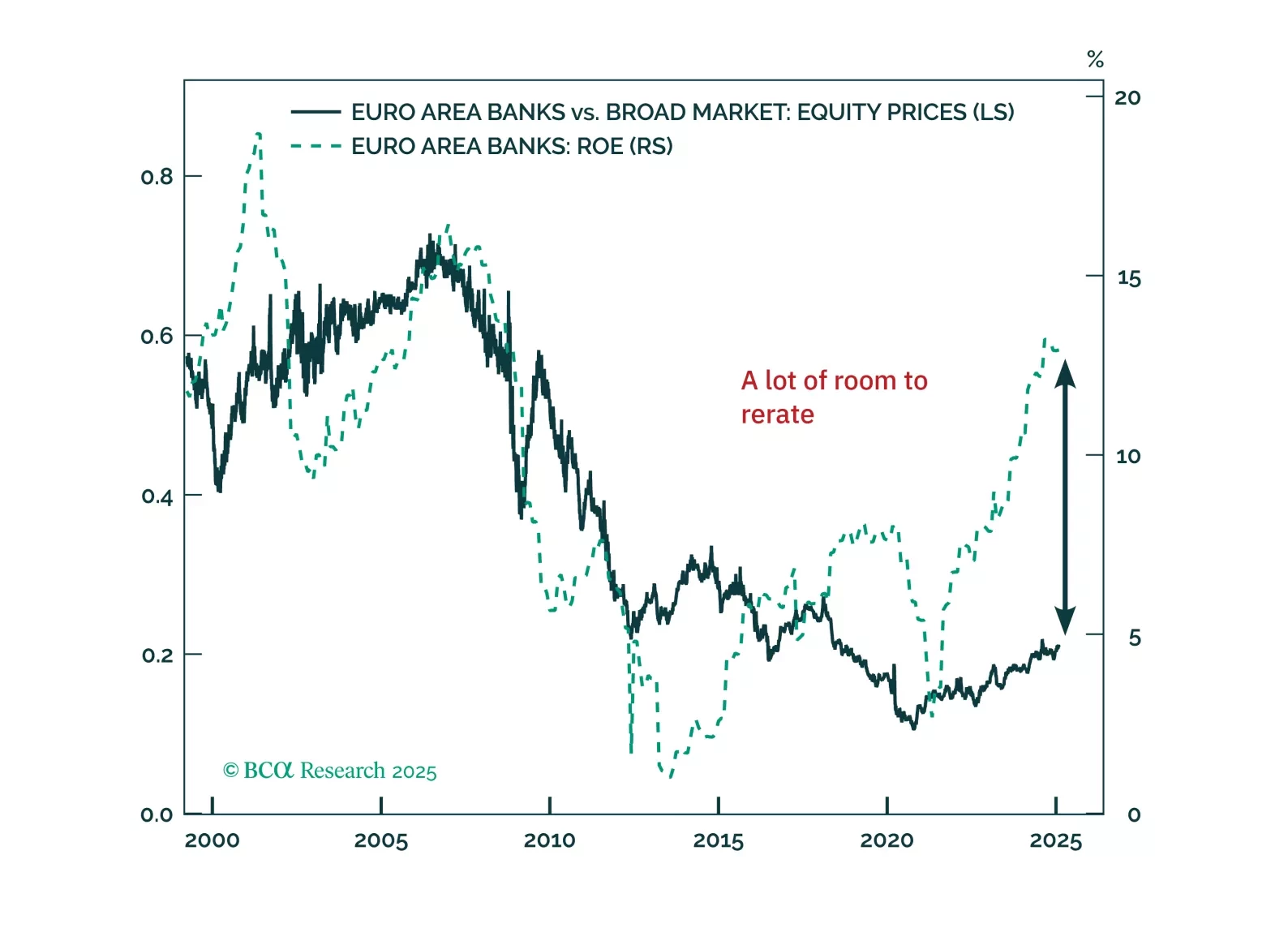

Eurozone banks have quietly outpaced the Magnificent 7—can they keep winning? With strong balance sheets, rising profitability, and structural tailwinds, European lenders still offer value despite short-term risks. Meanwhile, German equities continue to defy expectations, but is a near-term pullback on the horizon?

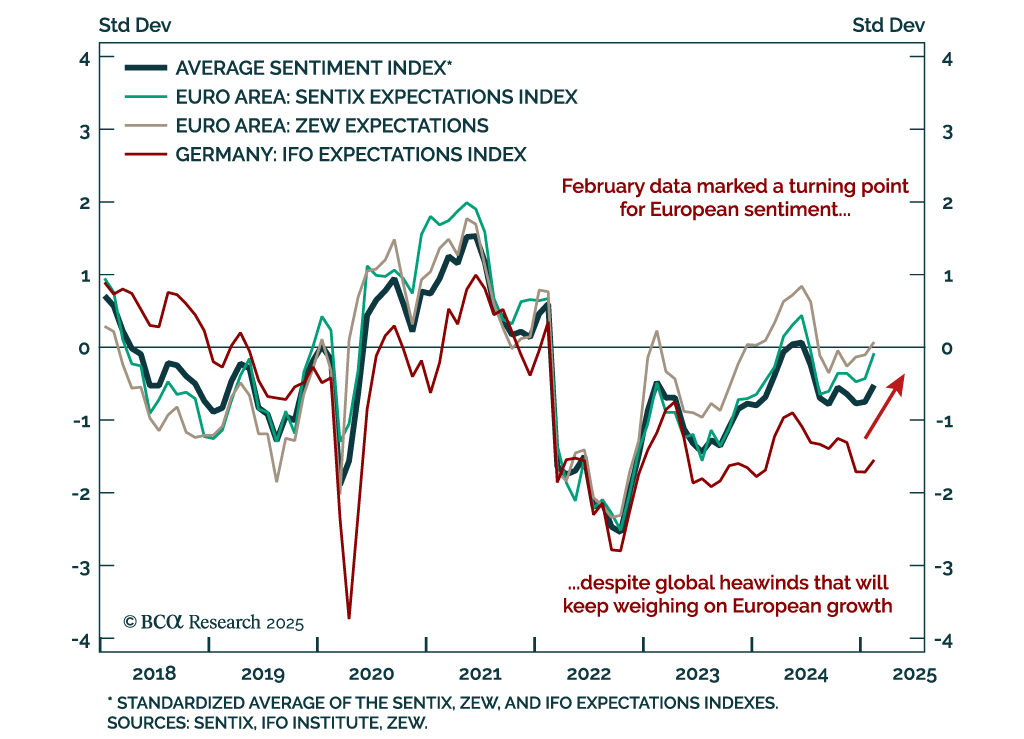

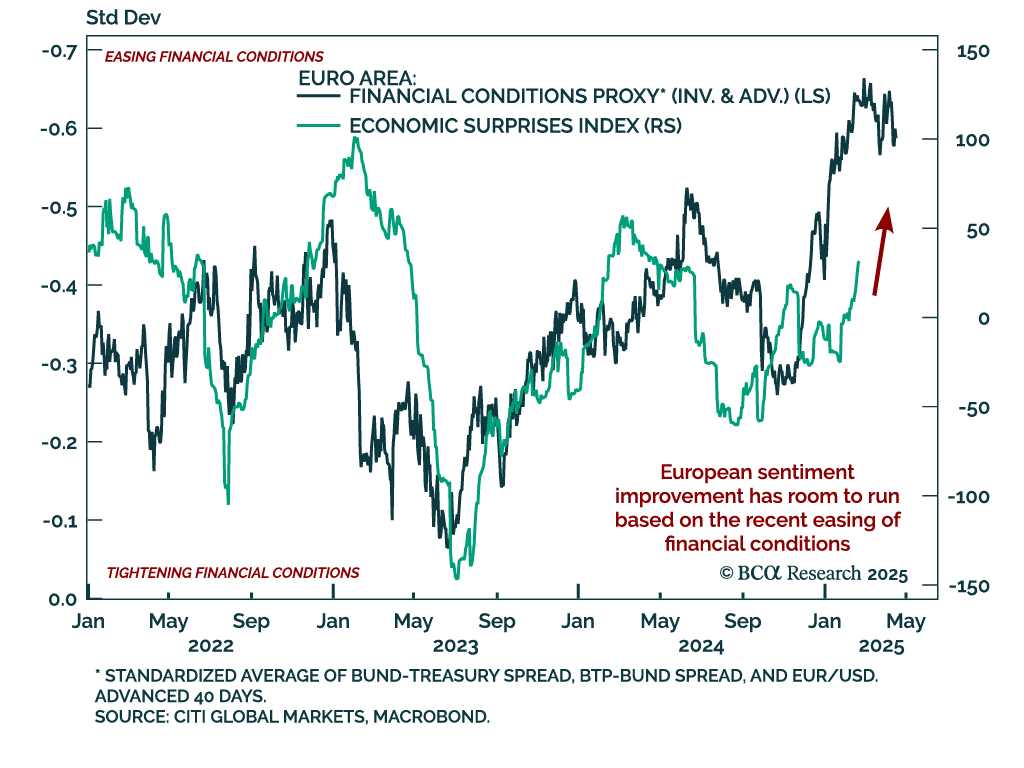

A nascent theme in the latest data is the broad improvement in European sentiment. The February Sentix and ZEW surveys both improved, and flash estimates for European consumer confidence beat estimates, ticking up to -13.6%. Confidence remains low, but…

The January UK CPI was slightly hotter than expected. Headline inflation beat estimates, rising to 3.0% y/y from 2.5% in December. Core inflation also jumped but was in line with expectations at 3.7%. Services were strong, albeit slightly lower than expected…

Our Foreign Exchange strategists reviewed the rationale to their short US dollar position as the DXY has been in a trading range with resistance near 110 and support around 100. The widening US budget deficit caps the dollar’s potential. It boosts…