US Election

Dear Friends,

As part of our new and improved GeoMacro service, please find attached our Global Risk Outlook, a quarterly digest of scenario probabilities and estimated market impacts for all the major geopolitical topics in the world today.

Our strong record of forecasting geopolitical events with numerical probabilities — including the Russian invasion of Ukraine in 2022, Liberation Day tariffs in 2025, Iran oil shock this year, and last few US elections, among others — is reflected in the constraints-based, Bayesian, and empirical method that we use to produce this report.

The Global Risk Outlook minimizes text and narrative, instead focusing attention on our risk matrixes, with bullet points to explain each scenario. It compiles our global coverage into a single document organized by Red Alerts, Gray Rhinos, Black Swans, and Red Herrings. The forecasting horizon is 12 months, while the financial assets covered are treasuries, the dollar, US and global equities, oil, and gold. Asset allocators and risk managers around the world have found these tables useful as inputs into their investment process, including portfolio stress tests.

On the first page you will find our subjective global geopolitical risk score on a scale of one to ten. Right now the score stands at eight, pending a downgrade whenever durable ceasefires in Iran and Ukraine are settled without spreading to larger conflicts between the great powers — a positive outcome that we ultimately expect, albeit not within the next three months.

Markets have grown accustomed to a high level of geopolitical risk in recent years and are mostly trading on macro and tech themes, but they will respond to significant changes up or down from that level. In the third quarter, we expect the shaky Iran ceasefire to hold together and we give fair odds of a Ukraine ceasefire, which is neutral-to-positive for global risky assets. But we expect Russian provocations to precede a ceasefire, and Iran threats — as well as US-China trade tensions — to escalate again after the US midterm elections, preventing us from being purely optimistic in the third quarter.

Our detailed study of financial market history amid past geopolitical crises informs our estimates of market impacts — and we update our historical table of geopolitical events and market reactions over different time horizons in the appendix of every issue for your convenience.

As always, we welcome any feedback — and we appreciate your readership!

All very best,

Matt Gertken

Head of GeoMacro

mattg@bcaresearch.com

Access BCA's US Midterm Election Dashboard

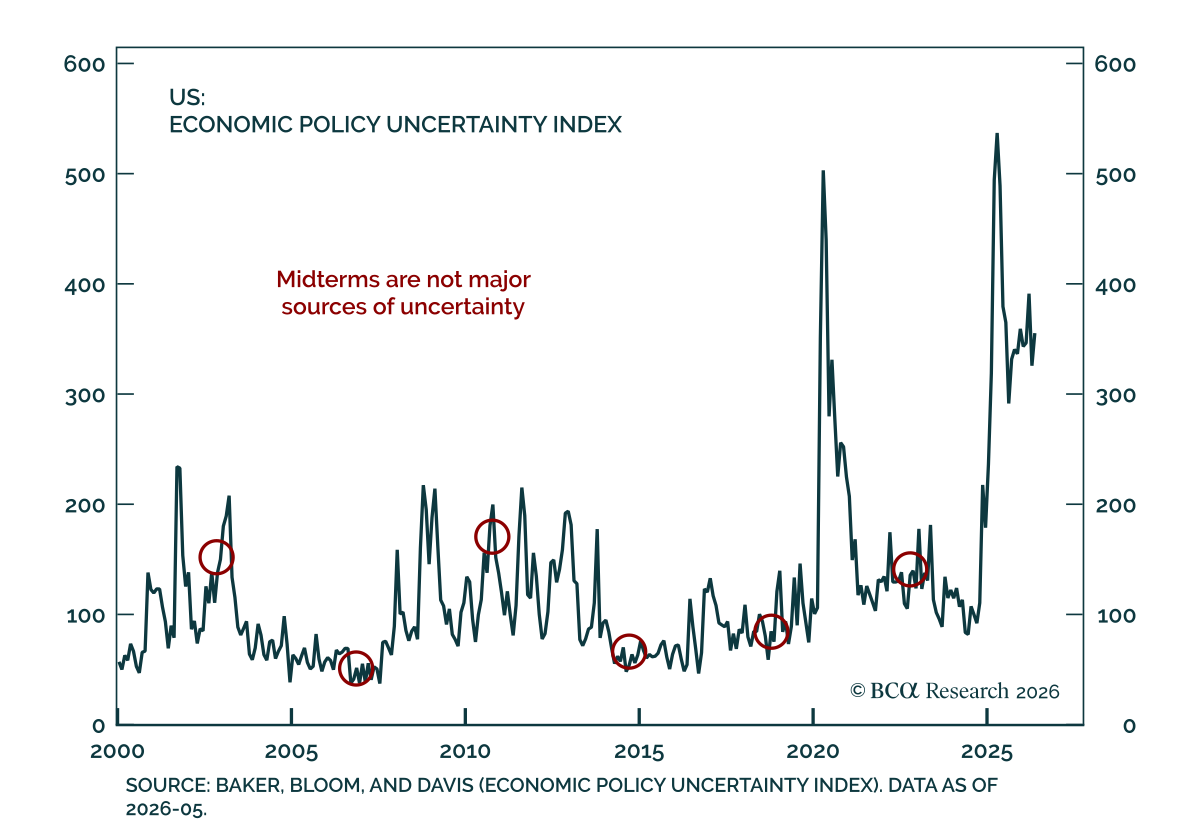

Midterms matter but geopolitics are the main risk this year. Markets will eventually refocus on geopolitical and inflation risks, raising Fed rate hike odds and supporting US dollar and stocks over global counterparts this year.

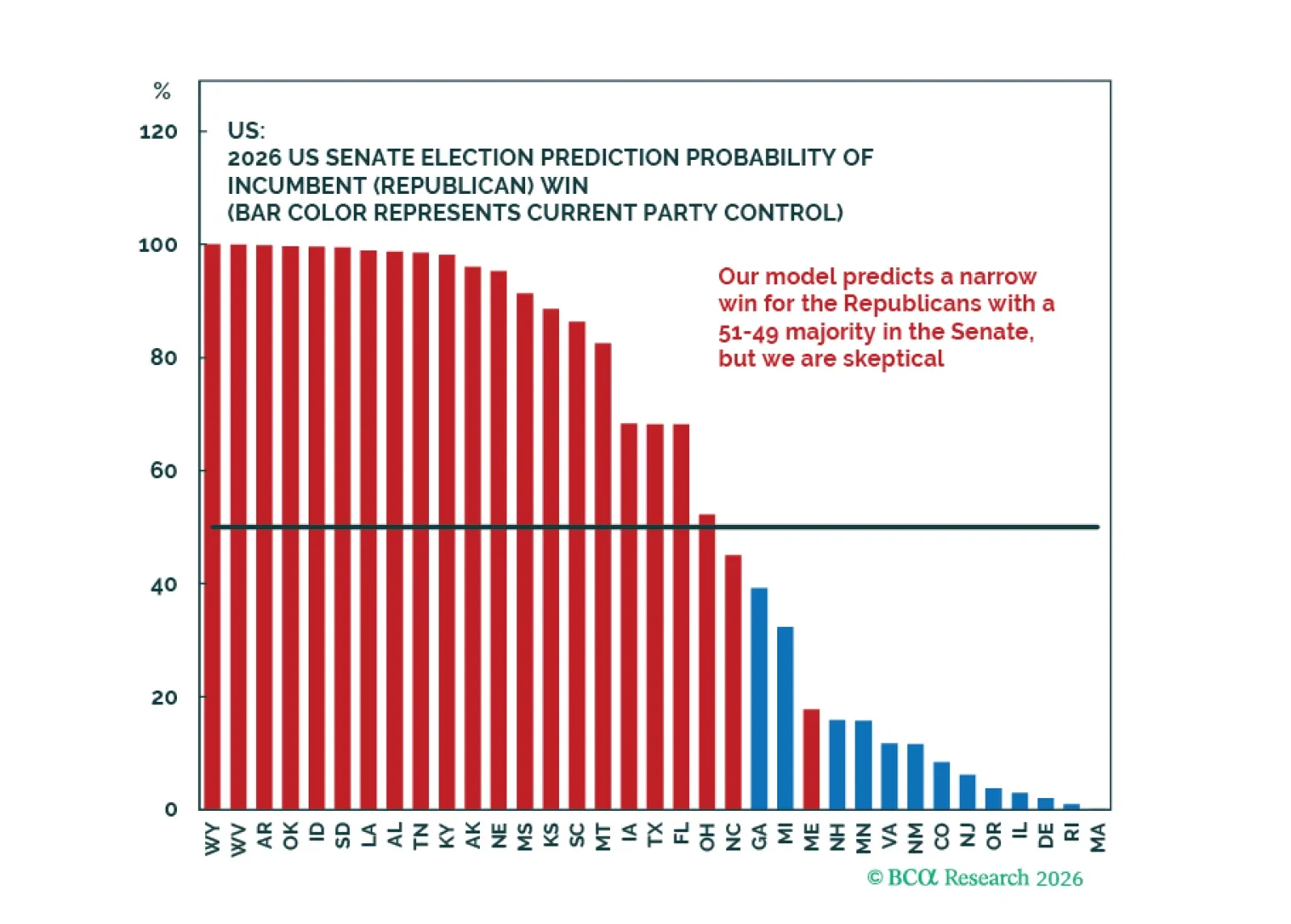

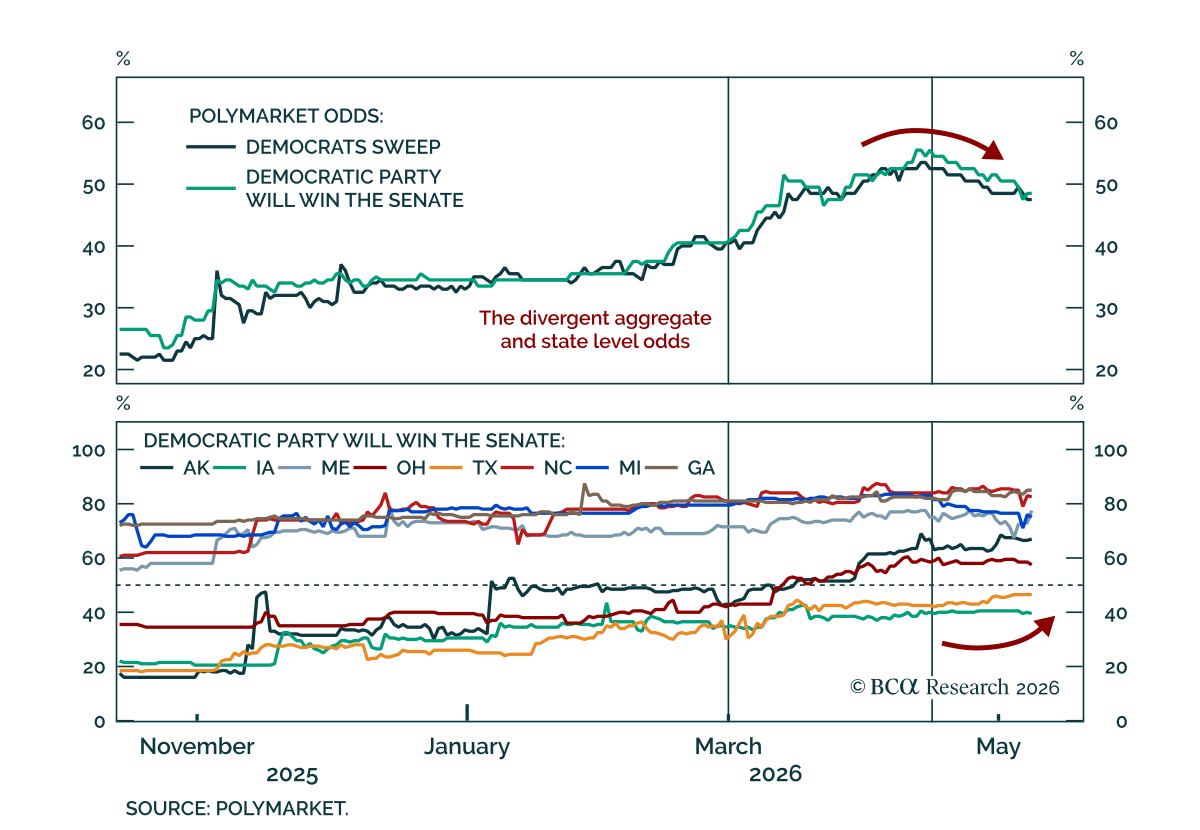

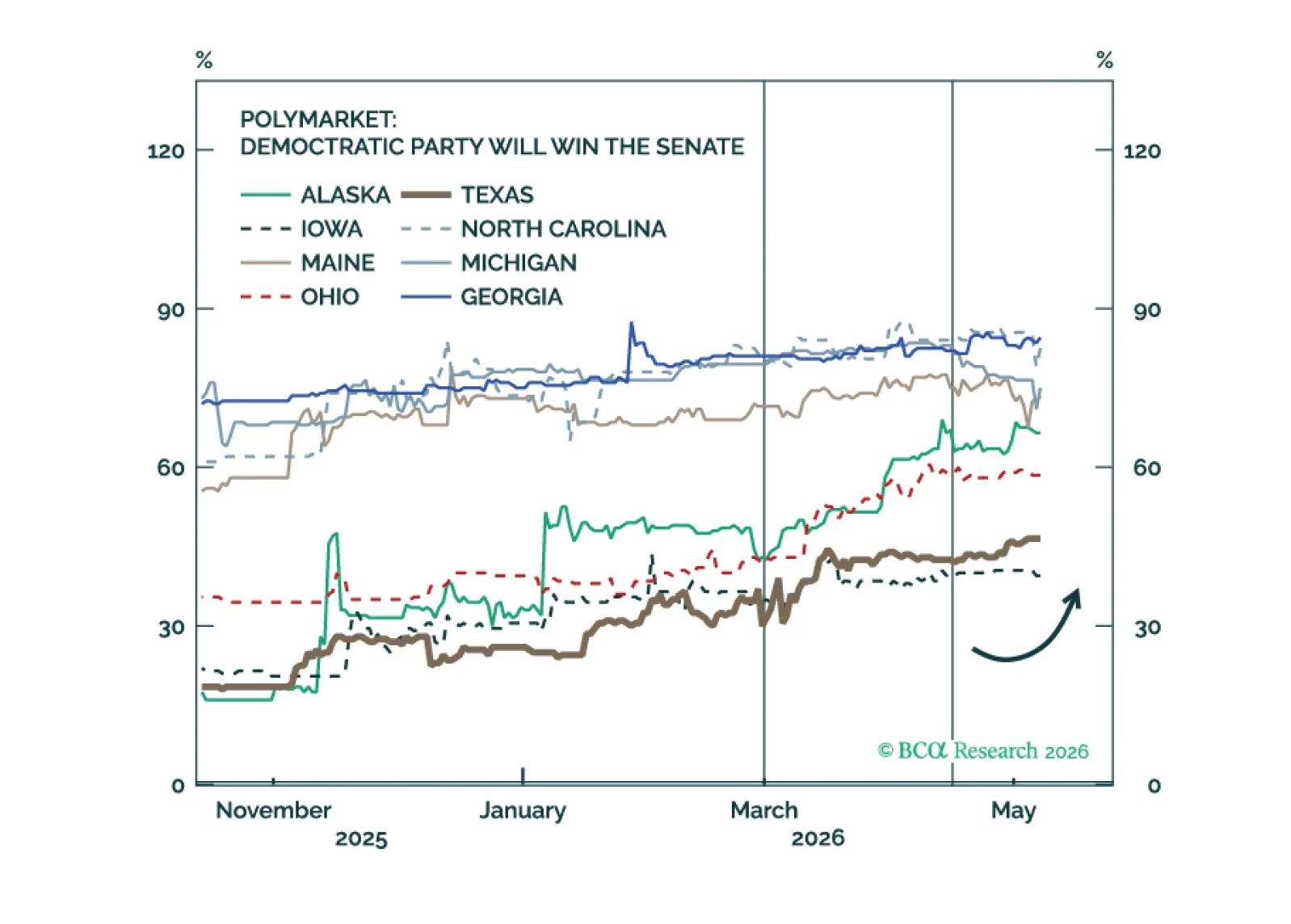

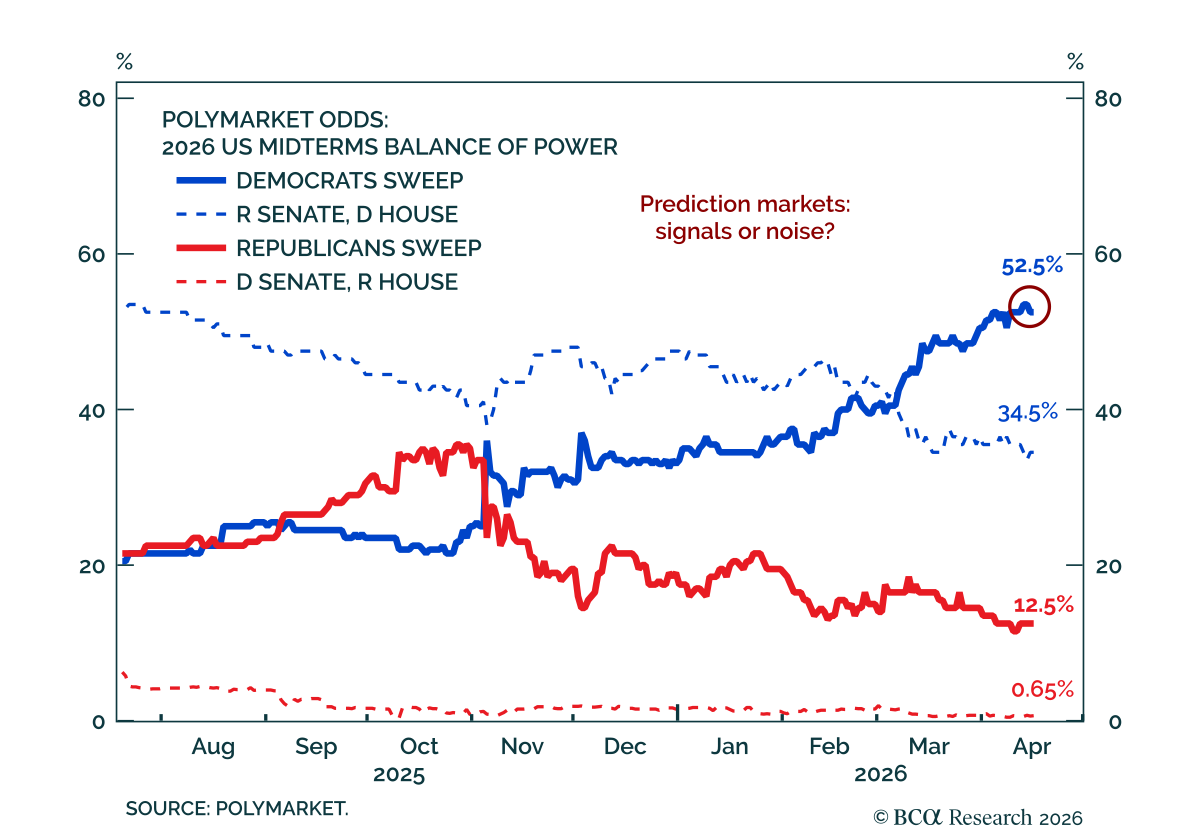

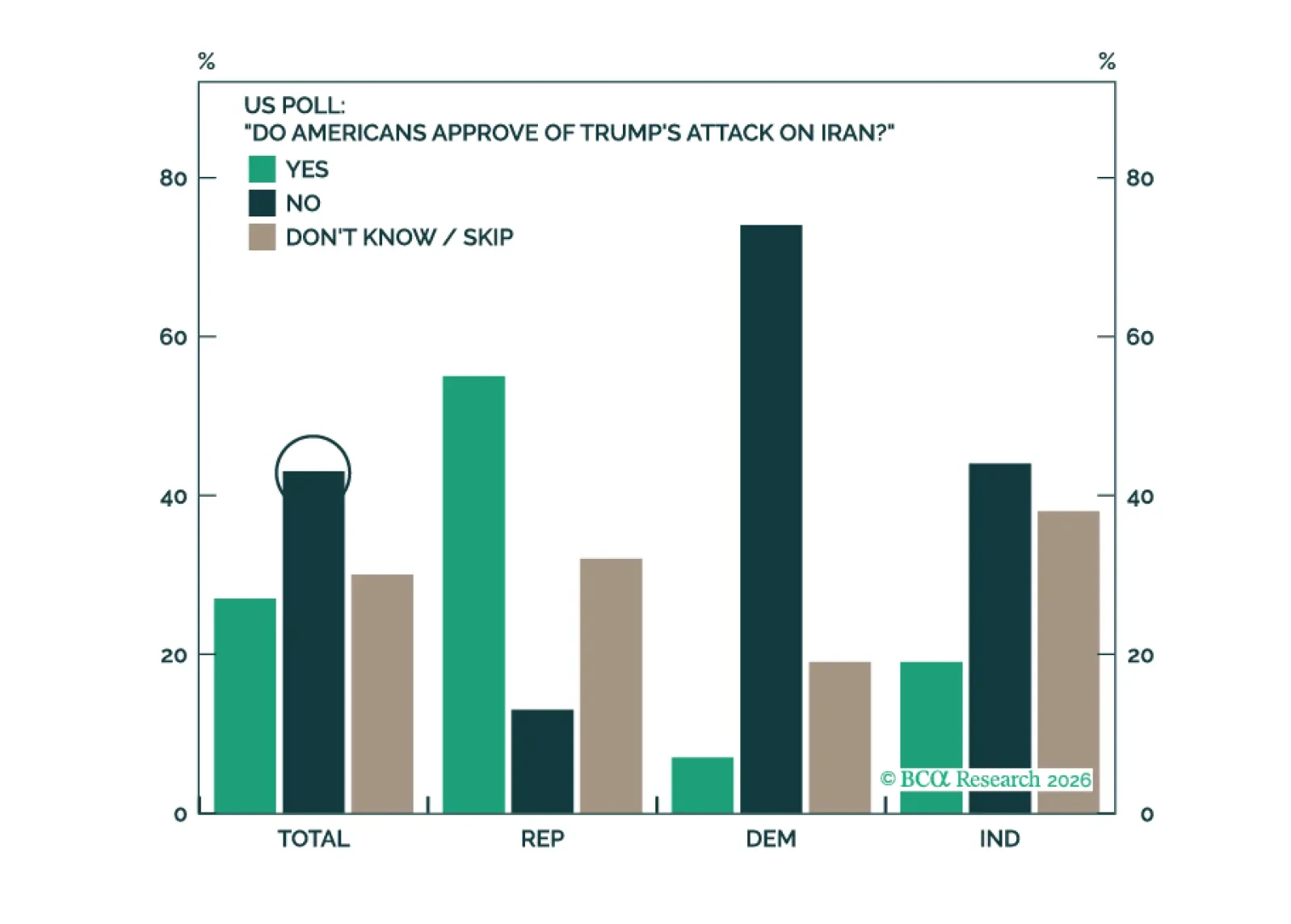

Aggregate Senate betting market pricing appears too pessimistic on Democrats relative to state-level odds and early polling, suggesting a potential mispricing and a relatively sanguine attitude towards the still-unresolved conflict in Iran and its aftermath.

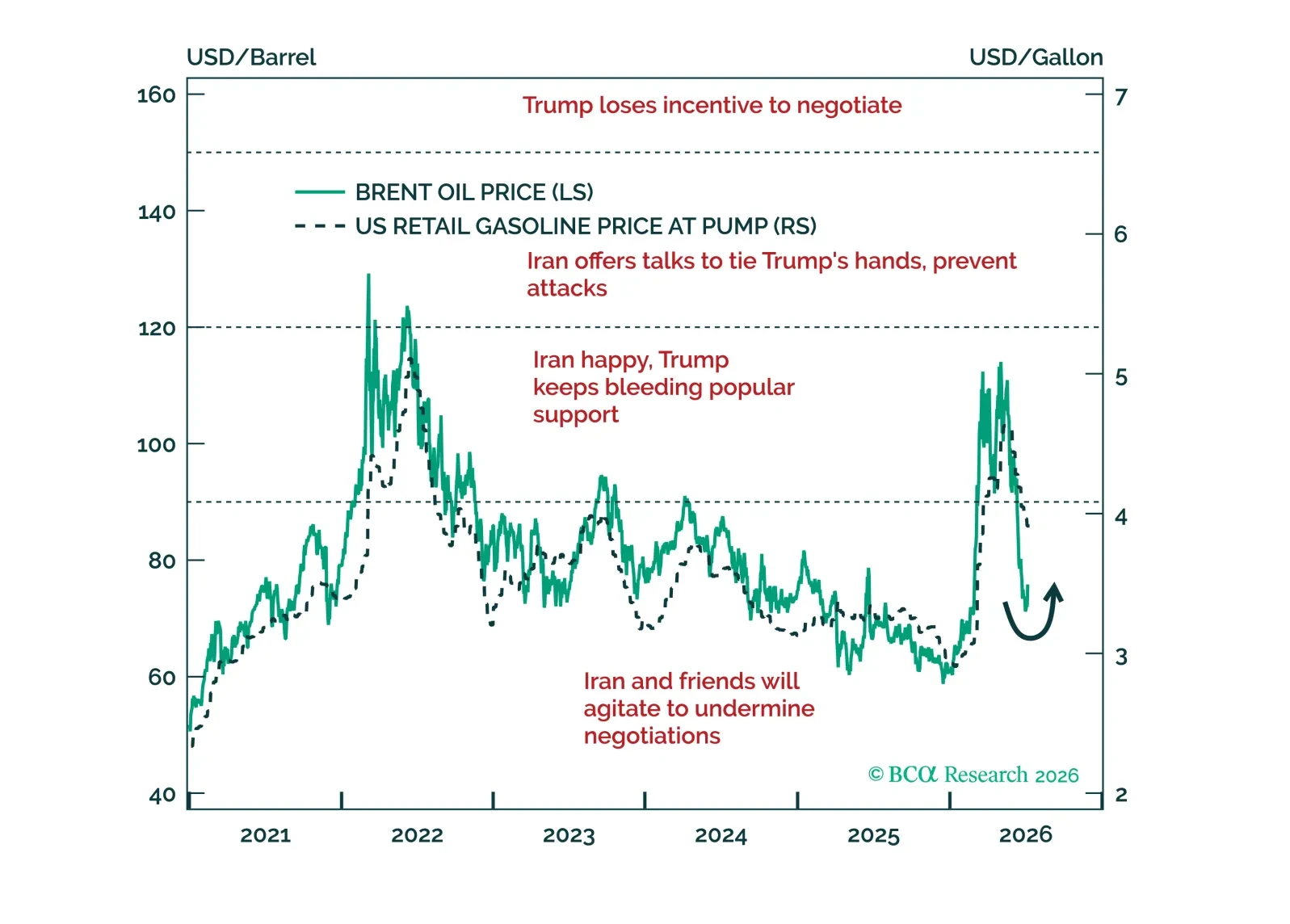

Markets may be underpricing a bifurcated political outcome. Unless the Iran deescalation succeeds, the delayed economic fallout from the energy shock could materially worsen Republican prospects and raise the probability of a Democratic Senate victory.

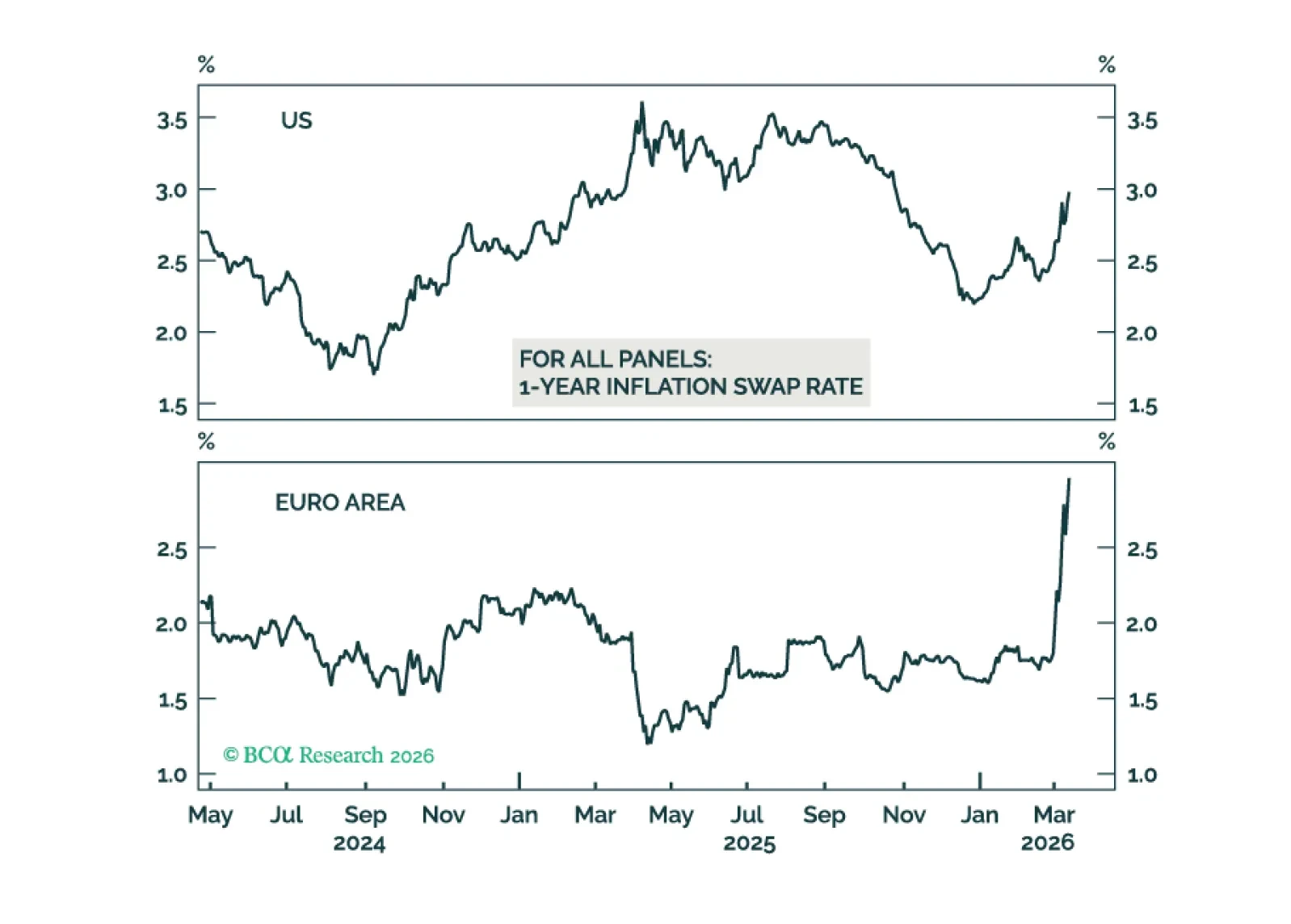

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

An energy price spike caused by a Middle Eastern war almost guarantees that Republicans will lose control of the House, and the chance of a Democratic Senate victory increases from 35% to 40%.

President Donald Trump’s political capital is moderate, as he frontloaded his most disruptive policies within the first year.