United States

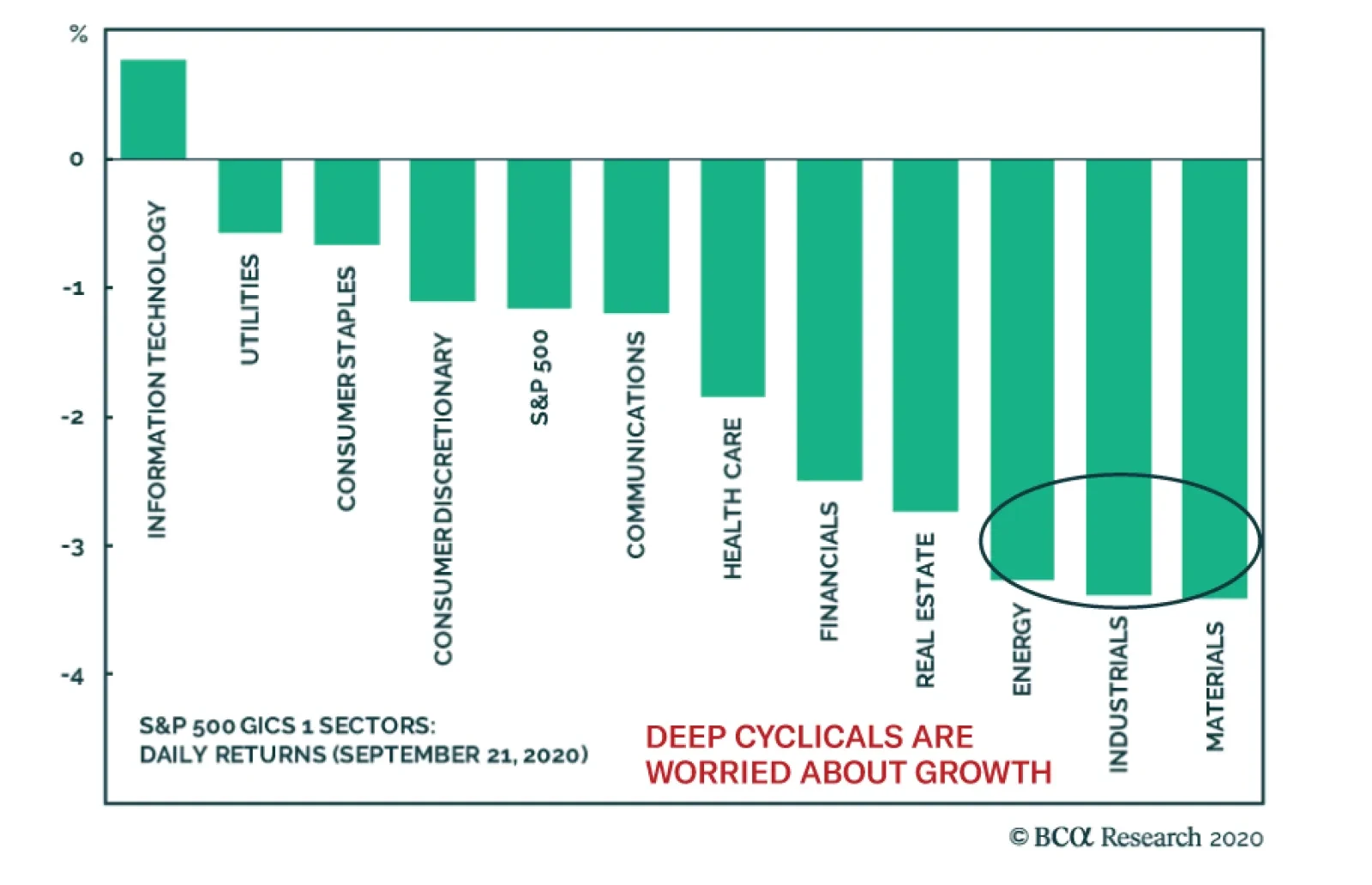

The market correction continues to deepen. More than the decline itself, the most worrisome element of yesterday’s 1.2% fall in the S&P 500 was its composition. Unlike in previous red days this September, the largest decliners were the deep cyclical…

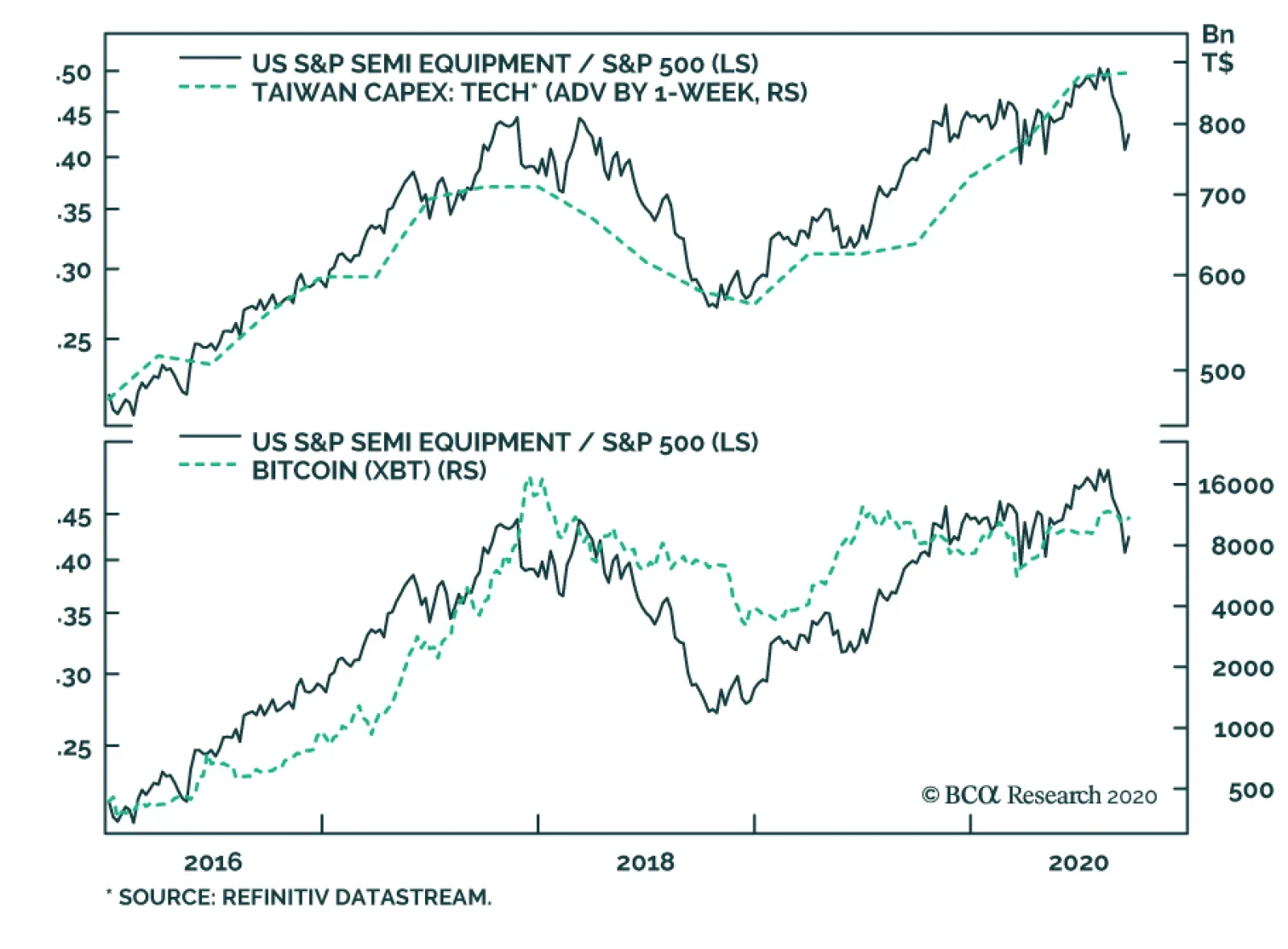

BCA Research's US Equity Strategy service recommends investors stay underweight the S&P 500 semiconductors equipment index because of the softening demand backdrop that is weighing on selling prices, the rekindling of the US/China tech-related trade war…

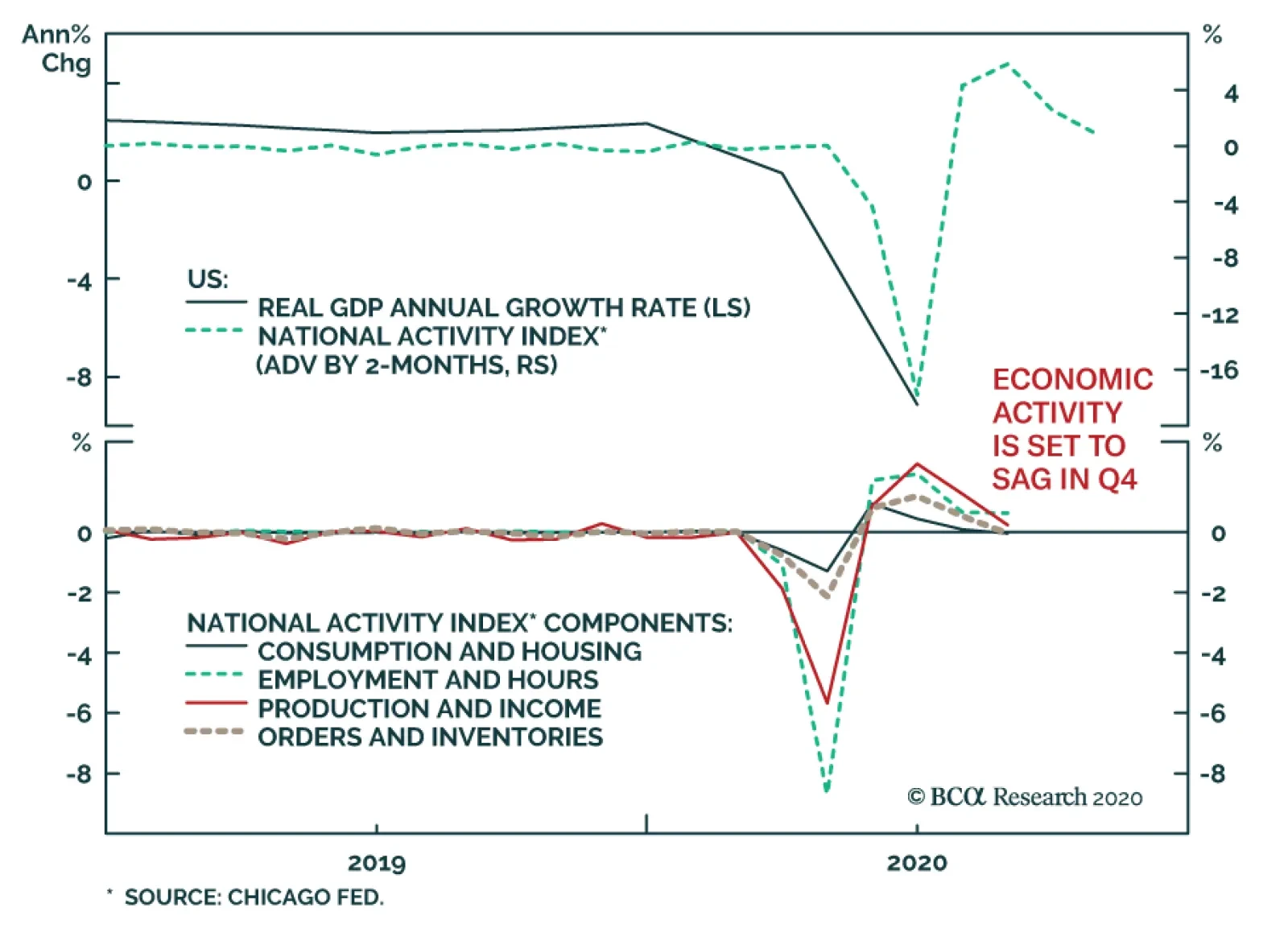

Yesterday, the Chicago Fed's August National Activity Index fell from July's revised print of 2.54 to 0.79, well beneath expectations of 1.19. This deceleration suggests that the economy will slow in Q4 following an incredible rebound in Q3, which reflected…

Highlights Portfolio Strategy We opt to stay patient and refrain from deploying fresh capital especially in the tech sector in the near-term; a better entry point will likely materialize between now and the end of the year. The softening demand backdrop that is weighing on selling prices, the rekindling of the US/China tech-related trade war and the risk of a reflex rebound in the US dollar, all warn to shy away from semi cap stocks. A balanced outlook keeps us on the sidelines in the S&P home improvement retail (HIR) index. Recent Changes There are no changes to the portfolio this week. Table 1

Churning

Churning

Feature Equities tried to regain their footing last week, but risks still lingering on the (geo)political front should sustain the tug of war between bulls and bears and rekindle volatility. While monetary and fiscal policies will remain loose, the intensity of easing is waning as both the Fed’s impulse (i.e. second derivative) of asset purchases has ground to a halt and Congress has hit a stalemate over the next round of stimulus. Crudely put, the thrust of monetary and fiscal policies is at heightened risk of shifting from stimulative to contractive (Chart 1). As a result, we remain patient with fresh capital and will wait to deploy it when the dust settles hopefully by the end of the year. Turning to equity market internals and other high frequency financial market data is instructive in order to get a clearer picture of the direction of the broad equity market. The value line arithmetic and geometric indexes and small cap stocks that led the March 23 SPX trough are emitting a distress signal (Chart 2). Chart 1Running Out Of Thrust

Running Out Of Thrust

Running Out Of Thrust

Chart 2Market Internals...

Market Internals...

Market Internals...

Drilling deeper on a sector basis, hypersensitive chip stocks, energy shares, and discretionary versus staples equities will likely weigh on the prospects of the broad equity market (Chart 3). The VIX index, the vol curve and the yield curve, all excellent leading indicators of the S&P 500, have crested and warn that the shakeout phase has yet to run its course (VIX shown inverted ,Chart 4). Chart 3...Say It Is Prudent...

...Say It Is Prudent...

...Say It Is Prudent...

Chart 4...To Remain On The Sidelines

...To Remain On The Sidelines

...To Remain On The Sidelines

Trying to quantify the SPX drawdown, we turn to CBOE’s equity put/call (EPC) ratio. The EPC ratio is nowhere near recent extreme readings. SPX pullbacks since the early-2018 “Volmageddon” have corresponded to significantly higher EPC ratio readings. In the past 10 such iterations, the median EPC ratio has been 0.86, the mean 0.93, with a range of 0.77 to 1.28 (Table 2). Currently, the EPC ratio is hovering near 0.58 suggesting that downside risks persist (EPC ratio shown inverted, Chart 5). Chart 5Downside Risks Persist

Downside Risks Persist

Downside Risks Persist

Table 2Equity Put/Call (EPC) Ratio During Pullbacks Since 2018

Churning

Churning

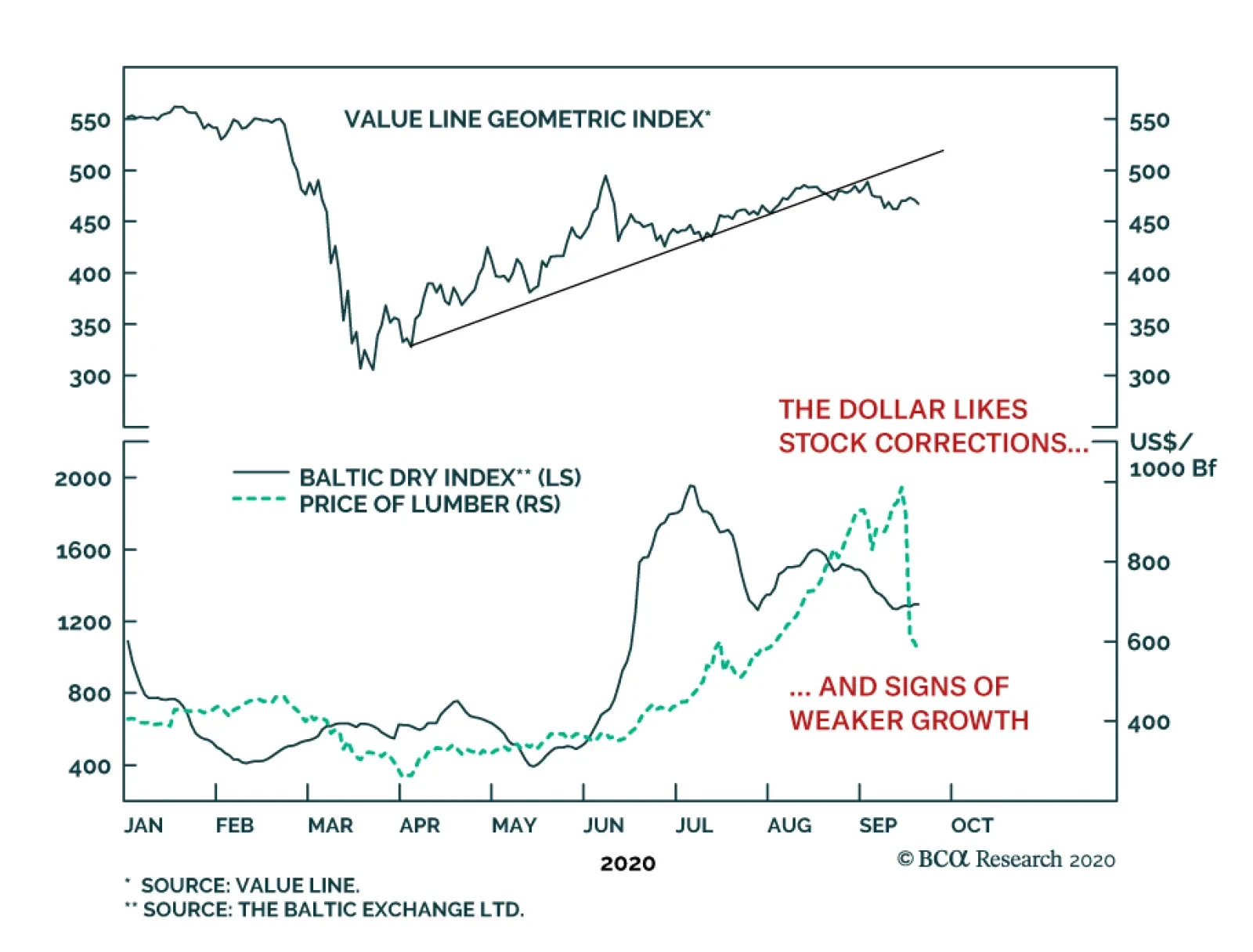

Finally, the commodity complex is also firing warnings shots. Lumber has collapsed nearly $300/tbf from the recent peak, oil is trailing gold bullion and silver is also cresting versus the yellow metal, iron ore is petering out and the Baltic dry index is wobbling. True, copper and materials stocks are holding their own, but overwhelmingly commodity market internals are waving a yellow flag (Chart 6). Chart 6Commodity Yellow Flags

Commodity Yellow Flags

Commodity Yellow Flags

Netting it all out, we opt to stay patient and refrain from deploying fresh capital especially in the tech space in the near-term; a better entry point will likely materialize between now and the end of the year. This week we reiterate our underweight stance in a niche technology index and shed more light on our recent downgrade to neutral of a key consumer discretionary subgroup. Chip Equipment Update: Tangled Up In The Trade War We remain committed to our intra-tech strategy of preferring defensive software and services tech names to aggressive hardware and equipment tech stocks. In that light, we reiterate our underweight stance in the niche S&P semi equipment index. Recent news of the Trump administration’s potential tightening of the noose on Chinese chip company SMIC (the country’s largest foundry) was a net negative for US semi cap names, similar to export restrictions of American technology to Huawei was a net negative for US semi cap names. As a reminder, these manufacturers count China as one of their largest export market alongside Taiwan and South Korea. Thus, this flare up in the US/Sino trade war bodes ill for semi cap companies’ future sales and profit growth projections (Chart 7). There are high odds that relative share prices have plateaued earlier this month and a fresh down cycle has commenced. Under such a backdrop, this hyper-sensitive manufacturing group will likely overshoot to the down side as is evident in the historical tight correlation with the ISM manufacturing survey: these violent oscillations are warning that a cooling off in the ISM will be severely felt in this niche manufacturing intense index (Chart 8). Chart 7Lofty Expectations

Lofty Expectations

Lofty Expectations

Chart 8Violent Oscillations

Violent Oscillations

Violent Oscillations

On the global demand front, there is an element that COVID-19 is stealing sales from the future and bringing demand forward. Already global semi sales are rolling over, and a couple of industry pricing power proxies are deflating at an accelerating pace: Asian DRAM prices are topping out in the contraction zone and Taiwanese export prices are sinking like a stone, warning that a deficient demand down cycle will squeeze semi cap profit margins (Chart 9). Importantly, Taiwanese tech capex, which TSMC dominates, has crested, warning that all the euphoria behind 5G deployment and uptake is likely baked in the relative share price ratio. The implication is that semi cap names remain vulnerable to any global 5G-related hiccups (top panel, Chart 10). Chart 9Waning Selling Price Backdrop

Waning Selling Price Backdrop

Waning Selling Price Backdrop

Chart 10Cresting

Cresting

Cresting

Finally, the tight positive correlation between Bitcoin prices and the relative share price ratio remains intact. Were a knee-jerk rebound in the US dollar to knock down Bitcoin, at least temporarily, it would serve as a catalyst to shed chip equipment stocks (bottom panel, Chart 10). Moreover, 90% of the industry’s sales originate abroad, thus a rise in the greenback would eat into their P&L via FX translation losses. Adding it all up, a softening demand backdrop that is weighing on selling prices, the rekindling of the US/China tech-related trade war and a reflex rebound in the US dollar, all warn to shy away from semi cap stocks. Bottom Line: Stay underweight the S&P semiconductor equipment index. The ticker symbols for the stocks in this index are: BLBG S5SEEQ – AMAT, KLAC, LRCX. Home Improvement Retailers: Stay On The Sidelines Two weeks ago our trailing stop was triggered in the S&P home improvement retail index (HIR) and we monetized gains of 15% since the mid-April inception and moved to the sidelines. Today we reiterate our benchmark allocation in this consumer discretionary sub group. Clearly, HIR was a major beneficiary of the lockdown as the US and Canadian governments deemed these retailers “essential” and allowed them to stay open during the peak of the pandemic. These Big Box retailers saw their sales soar as the fiscal easing package replenished consumers’ wallets, and coupled with the lockdown, caused a surge in DIY remodeling activity. Our portfolio also greatly benefited from the stellar performance of the S&P HIR index, as existing home sales staged a significant comeback and inventories of homes for sale receded substantially thus further tightening the residential real estate market (top & middle panels, Chart 11). As reminder, historically a vibrant housing market is synonymous with handsome returns in relative share prices and vice versa. But now a number of stiff headwinds, which our HIR model encapsulates, signal that a lateral digestive move is in store in the coming months (Chart 12). Chart 11Unsustainable Front Running

Unsustainable Front Running

Unsustainable Front Running

Chart 12Stiff Headwinds

Stiff Headwinds

Stiff Headwinds

First, a repeat of the spike in demand for home improvement projects is highly unlikely, especially given that demand was brought forward. Also during the autumn and winter months there is a natural slowdown in the take-up of remodeling projects until the spring home selling season arrives. Second, the industry’s sales-to-inventories (S/I) ratio is literally off the charts (bottom panel, Chart 11). An inventory build-up and easing in demand will bring back the S/I ratio back to a more reasonable level. Lastly, lumber prices have taken a beating of late collapsing from over $900/tbf to below $600/tbf. This drubbing of this economically hypersensitive commodity directly cuts into HIR earnings. These Big Box retailers make a set margin on lumber sales so as prices fall they take a big bite out of profits (bottom panel, Chart 13). Nevertheless, a few offsets prevent us from turning outright bearish in this early cyclical retailers. Namely, the industry’s profit growth bar is on a par with the broad market and thus does not pose a large hurdle to overcome. Importantly, given that HIR earnings have kept pace with the massive run-up in stock prices (second panel, Chart 14), they have kept relative valuations at bay. While, the S&P HIR 12-month forward P/E trades at a market multiple, the relative forward P/E changes hands at a 20% discount to the historical mean. Thus, HIR enjoy a significant valuation cushion (bottom panel, Chart 14). Chart 13Timber!

Timber!

Timber!

Chart 14But There Are Powerful Offsets

But There Are Powerful Offsets

But There Are Powerful Offsets

Finally, the Fed just explicitly committed to stay on the zero interest rate line until 2023! This easy monetary policy as far as the eye can see is a powerful tonic to early cyclical and interest rate-sensitive home improvement retailers (fed funds rate shown inverted, top panel, Chart 14). Netting it all out, a balanced outlook keeps us on the sidelines in the S&P HIR index. Bottom Line: Stick with a benchmark allocation in the S&P home improvement retail index. The ticker symbols for the stocks in this index are: BLBG S5HOMI – HD, LOW. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Current Recommendations Current Trades Strategic (10-Year) Trade Recommendations

Drilling Deeper Into Earnings

Drilling Deeper Into Earnings

Size And Style Views July 27, 2020 Overweight cyclicals over defensives April 28, 2020 Stay neutral large over small caps June 11, 2018 Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, TSLA, V). January 22, 2018 Favor value over growth

Feature In last week’s US Bond Strategy report, we presented the results of a scenario analysis on consumer spending.1 The goal of that analysis was to assess how much additional federal government income support is required to achieve consumer spending growth targets that won’t disappoint markets. The calculations regarding the amount of additional stimulus required to hit different spending targets are correct. However, a typo in our code (in fact, a missing letter “c”) caused us to specify the wrong targets. Last week, we targeted -3% 12-month over 12-month consumer spending growth for the period between March 2020 and February 2021. The rationale being that -3% was the worst spending growth seen during the 2008 Great Recession and would likely be the minimum that markets could tolerate this time around. As shown in the second panel of Chart 1, this number should have been -1.9%. Chart 1Consumer Spending Driven By Income & The Savings Rate

Consumer Spending Driven By Income & The Savings Rate

Consumer Spending Driven By Income & The Savings Rate

We also considered spending growth targets for the 12-month period between August 2020 and July 2021. Last week we set our target range for that period at between 2% and 6%, the growth rates seen during the recovery years that followed the Great Recession. That range should have been set at 2.5% to 5%. We present revised results from our scenario analysis in Table 1 and Table 2. These tables are identical to the ones presented last week, except that they now have the correct consumer spending targets. Table 1Without More Stimulus COVID's Impact On Consumer Spending Will Be Worse Than The GFC

A Correction To Last Week's Report

A Correction To Last Week's Report

Table 2At Least $600 Billion More Government Income Support Is Needed

A Correction To Last Week's Report

A Correction To Last Week's Report

Our conclusion remains similar, though our corrected numbers suggest that more income support from the federal government will be required to hit reasonable spending targets. Last week, we concluded that extra income support on the order of $500 - $800 billion is the minimum that will be required. Our corrected numbers suggest that more stimulus will be necessary, on the order of $600 billion to $1 trillion. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “More Stimulus Needed”, dated September 15, 2020, available at usbs.bcaresearch.com

Highlights Consumers are the beating heart of the US economy, … : By showering cash on the newly unemployed, and issuing checks to more than half of all taxpayers, the CARES Act arrested April’s free fall in consumption and helped households meet their financial obligations. … and if they’re waylaid by the pandemic, only a forceful fiscal response stands in the way of reduced future growth: Bankruptcies and widespread displacement of workers would turn a nasty cyclical shock into lower trend growth. How big does the next round need to be?: Applying a framework developed by our US Bond Strategy colleagues, we estimate that consumption growth will get back to trend if Congress provides $800 billion of aid to households through the first half of next year. Is it likely something that size can get through Capitol Hill?: Assistance for reeling states is a potential sticking point, but we continue to believe that a major aid package will pass. If it doesn’t, the election outcome will loom large over the 2021 outlook. Feature Over BCA’s 70-plus years, our research teams have developed hundreds if not thousands of proprietary indicators to project where financial markets and the major economies are headed. They are central to our process and we are continuously engaged in trying to improve them. Sometimes, though, it helps to take a step back and look at the landscape from the broadest and simplest perspective. When we do, we remind ourselves of what we have come to think of as macroeconomics’ fundamental lesson: My spending is your income and your spending is my income. Consumption isn't just four times as large as each of the other two main components of US GDP, it also exerts a gravitational pull on them. The truth of this simple formulation is especially easy to see in the United States, where consumption accounts for two-thirds of GDP (investment and government spending each contribute one-sixth, ignoring net exports’ modest drag). The US economy would shrivel if household spending were to fall sharply, and the second-order effects on investment and government receipts would prolong the agony. The former is a function of consumption; businesses only invest once it’s clear that demand has overtaken existing capacity or will soon do so. Reduced consumption would pressure employment and profits, squeezing federal revenues that are almost entirely composed of individual income taxes, payroll taxes and corporate income taxes (Chart 1). Transfers from the federal government account for one-third of the states’ total revenues (Chart 2); since most of them are forbidden to run budget deficits, they would face immediate cutbacks if the flows from Washington were to slow. Chart 1Consumption Exerts An Outsized Impact On Federal ...

The Fundamental Theorem Of Macroeconomics

The Fundamental Theorem Of Macroeconomics

Chart 2... And State Government Revenues

The Fundamental Theorem Of Macroeconomics

The Fundamental Theorem Of Macroeconomics

Plugging The Gap Recognizing that a wobbling consumer has the potential to topple several economic dominos, Congress undertook extraordinary measures to keep a vicious short-term shock from impairing growth into the intermediate and long term.1 The CARES Act included provisions to support ailing industries and small businesses, but its efforts at shoring up vulnerable households have been the most effective by far. Direct payments of $1,200 to every adult and $500 to every child in households earning less than $99,000 ($198,000 for married filing jointly taxpayers) and weekly $600 supplemental unemployment benefits helped push personal income well above February’s pre-pandemic level (Chart 3). Chart 3The CARES Act Gave Lower-Income Households An Enormous Boost

The Fundamental Theorem Of Macroeconomics

The Fundamental Theorem Of Macroeconomics

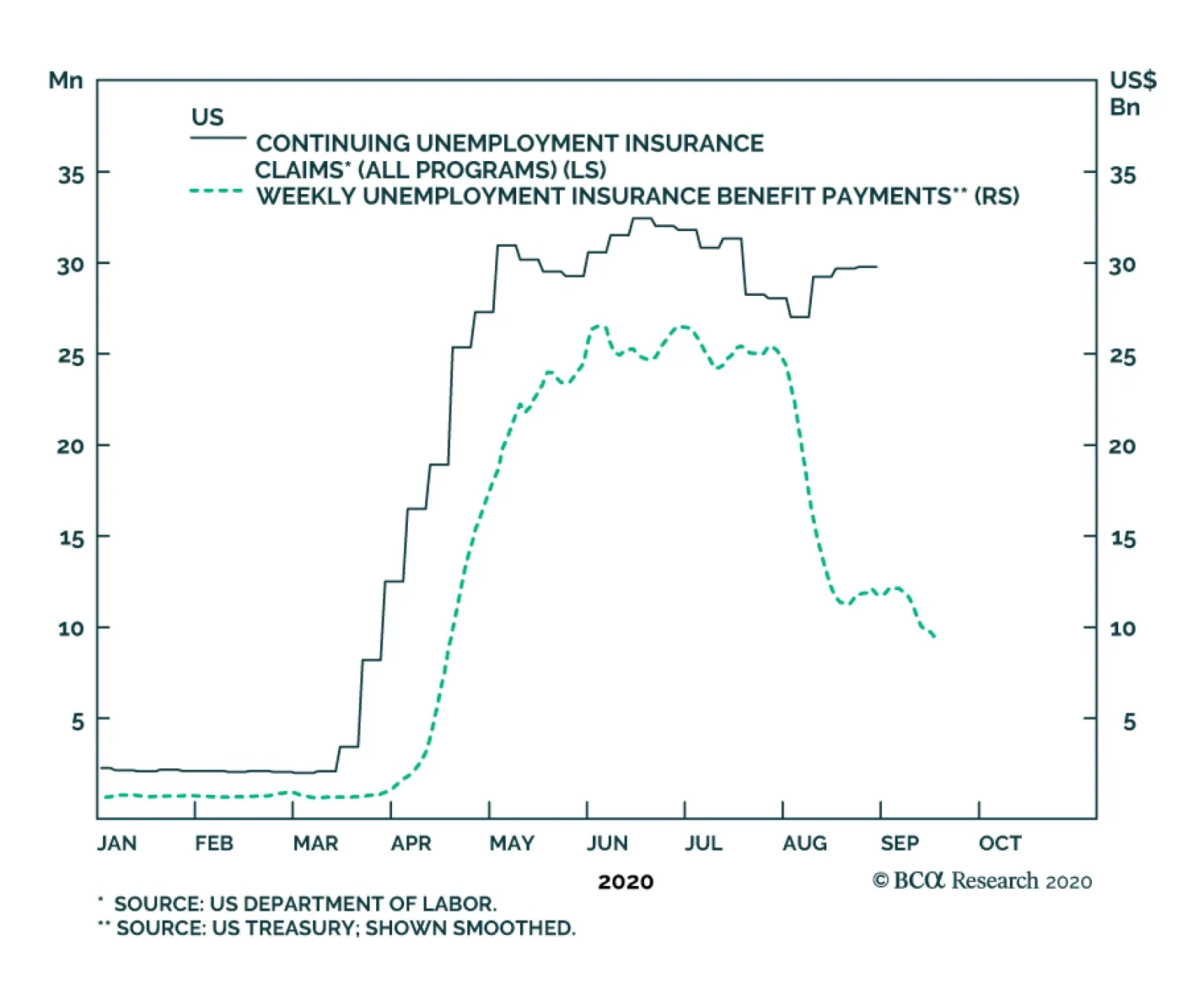

With income rising, especially for those at the lower end of the income distribution, households were able to stay current on their rent (Table 1), their mortgage and all their other obligations (Table 2). They were even able to pay down their credit card balances, an unusual occurrence at the start of a recession (Chart 4). Residential landlords and personal lenders breathed a sigh of relief, along with the entities that have lent to them, though they must be wondering how their obligors will fare now that the CARES Act’s supplemental unemployment benefit has expired. Households built up $325 billion of savings from March through July, which helped tide them over in August and is presumably doing so in September, but we expect that cracks may be beginning to show and that they will emerge in force in October if another round of aid is not forthcoming. Emergency CARES Act fiscal transfers were so large that they more than offset the drag from declining compensation as employees were laid off or worked less than full time during the lockdowns. Table 1September Slowdown?

The Fundamental Theorem Of Macroeconomics

The Fundamental Theorem Of Macroeconomics

Table 2Credit Performance Across Personal Loan Categories Was Solid Through July

The Fundamental Theorem Of Macroeconomics

The Fundamental Theorem Of Macroeconomics

Chart 4Strapped Households Usually Run Up Their Credit Card Balances When Recessions Hit

Strapped Households Usually Run Up Their Credit Card Balances When Recessions Hit

Strapped Households Usually Run Up Their Credit Card Balances When Recessions Hit

How Much Will It Take? Deficit spending is a charged issue, especially among those at the upper end of the income distribution who will ultimately be taxed to repay the debt to fund today’s deficits. However, we agree with the mainstream economic consensus that issuing another two or three trillion dollars of debt at negative real yields is preferable to suffering the hysteresis effects of an uncontained surge of bankruptcies. From a short-term perspective, vigorous fiscal support is the only thing that can preserve the seeming dichotomy between the real economy’s struggles and the equity and credit markets’ bliss.2 The key practical question is how big the next round needs to be to allow policymakers to extend the bridge over the gap opened by the pandemic. Our US Bond Strategy colleagues addressed that question head on last week.3 They proceeded from the assumption that a certain minimum level of consumer spending growth is necessary to meet market participants’ generally sanguine recovery expectations. They then focused on how household income (what comes in) and the savings rate (how much is held back) might evolve under pessimistic and optimistic scenarios and a base-case scenario that splits the difference between the two. Their estimates of required support from a new round of fiscal transfers are simply the difference between the spending that would occur without the transfers and the minimum required spending. Looking at the 12-month moving average of consumer spending to smooth out single-month swings, and comparing it to its year-ago level (a 12-month-over-12-month basis), we map out three nominal growth targets for the August 2020 to July 2021 period: 3%, 4% and 5%, consistent with the range that prevailed once the economy found its footing after the global financial crisis (Chart 5). Instead of performing the analysis under all three of our colleagues’ scenarios, we simply use the split-the-difference base case that has household income ex-CARES Act transfers (Chart 6, top panel) and the savings rate (Chart 6, bottom panel) returning to their pre-pandemic level by September 2021. Chart 5Outside Of Recessions, Consumer Spending Growth Typically Occupies A Tight Range

Outside Of Recessions, Consumer Spending Growth Typically Occupies A Tight Range

Outside Of Recessions, Consumer Spending Growth Typically Occupies A Tight Range

Chart 6Recovery Scenarios For Consumption's Drivers

Recovery Scenarios For Consumption's Drivers

Recovery Scenarios For Consumption's Drivers

The results are shown in Table 3. The 4% nominal rate of consumption matches the economy’s trend growth since the GFC (2-to-2.25% real plus 1.75-to-2% inflation), 3% allows for a sluggish recovery in which the virus only slowly loosens its grip and 5% covers the possibility of a burst of above-trend growth that might follow a better-than-expected virus outcome. We project that households will require an average of $70-to-94 billion of monthly income support to grow 12-month-on-12-month consumption by 3-to-5%. A repeat round of stimulus checks would chip in $23 billion, leaving supplemental unemployment insurance benefits and the extension of benefits to workers that would not otherwise be covered by their state unemployment insurance program to pick up much of the rest of the $50-to-70 billion tab. Once those programs were fully up and running in May, June and July, they distributed an average of $92 billion per month ($77 billion supplemental benefits and $15 billion expanded eligibility). Those numbers suggest that unemployment-related transfers amounting to 55-to-75% of the CARES Act transfers would suffice, which is encouraging because the Senate and the White House now view its $600 weekly supplement as too generous. The unemployment rate has fallen since the spring, however, with fewer households in line to receive payments, so lawmakers will have to devise other ways to get money into the hands of consumers. Given that states and municipalities face an acute cash crunch and Democrats have insisted on addressing it, there is a good chance that states will receive a healthy allocation and some of the state funds will eventually find their way to households. Table 3Another Round, Please

The Fundamental Theorem Of Macroeconomics

The Fundamental Theorem Of Macroeconomics

The bottom line for investors assessing the adequacy of a stimulus bill is that we think it should allocate at least $800 billion to support household income. A bill in the mid-to-high $1 trillion range that would split the difference between Republican and Democratic proposals should suffice and it would leave ample room for desperately needed support for state and local governments. Public transit systems like the gasping New York city subway, which suffered ridership declines of as much as 80-90% at the height of the lockdown while incurring significant new cleaning costs, may otherwise have to impose draconian service cutbacks that undermine their local economies’ efforts to reopen. The Fundamental Theorem Of Microeconomics At the University of Chicago’s Booth School of Business, Introductory Microeconomics is called Price Theory to keep the central lesson of the course in every student’s mind: people respond to incentives. We have come to think of this as the fundamental rule of microeconomics. It is the foundation of public policy’s attempts to shape behavior: If you want more of something, subsidize it; if you want less of something, tax it. When mulling the prospects for the passage of a significant new aid bill, we begin and end with a consideration of the key players’ incentives. The Democrats want a bill to demonstrate that government can be the solution and to push back against the anti-government narrative that has taken root over the last 40 years. The administration should be doing its utmost to obtain a robust spending package since recessions have reliably sunk incumbent presidents’ re-election prospects. Republican senators, even those who are not up for election this year, should want a bill because control of the Senate is likely to go to the party that wins the White House and individual senators’ power and influence are magnified when they are in the majority. Despite months of posturing and foot-dragging, we second our geopolitical strategists’ view that an aid package aligning with all the major players’ interests will pass soon. Investment Implications Much of our constructive take on markets and the economy proceeds from our view that another significant round of fiscal aid is forthcoming. If it is not, we would revisit our bullish 12-month asset allocation recommendations and we would close out our overweight on the SIFI banks’ stocks. An assumption that humankind will find a way to tame COVID-19 on a timetable in line with market expectations is also embedded in our 12-month equity overweight. If a second wave of infections takes hold, the mortality rate moves significantly higher and treatment and/or vaccine progress unexpectedly reverses, our recommendations will get more cautious. If it is in the interests of all of Washington's key players to pass a bill, there's an awfully good chance that bill will get passed. Although those in the know have lately become more optimistic that the first installment(s) of an effective vaccine(s) will become available in the next two quarters (Chart 7), such an outcome is not assured. A client asked us last week what would ensue if a vaccine is not available until the third or fourth quarter of 2021. As we talked through it with her, we could not escape the idea that the election could be hugely consequential for markets if the lack of a vaccine coincides with a failure to pass a stimulus package before the election, or with a stimulus package that does not extend beyond the end of March. Chart 7Rising Odds Of A Vaccine Within The Next Six Months

The Fundamental Theorem Of Macroeconomics

The Fundamental Theorem Of Macroeconomics

If the next round of stimulus is not passed before the election, or if it is set to expire two or three quarters before an effective vaccine will be available in sufficient quantities to turn the public health tide, fiscal policy would become the single most important driver of the near-term market and economic outlook, given our view that the Fed has already done nearly all it can do. Congress would then take center stage, with the White House playing a secondary role based on its veto power and the influence of the bully pulpit. In that case, we would expect equity and credit markets to fare much better under a Blue Wave outcome in which the Democrats sweep the election than they would in any outcome that leaves Republicans in control of the Senate. Think of it like this: if the economy needed fiscal aid to counter six-to-twelve more months of pandemic disruptions two years before Congress again had to face voters, would you rather appeal to Pelosi, Schumer and Biden, champing at the bit to demonstrate how government can alleviate suffering, or Mitch McConnell, itching to teach profligate cities and states a lesson? Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 The Fed leaped into the breach as well, but we have already discussed its efforts in detail. This report focuses on fiscal policy. 2 Please see the September 18, 2020 BCA Research Special Report, "The US Economy vs. The Stock Market: Is There A Disconnect?" available at www.bcaresearch.com. 3 Please see the September 15, 2020 US Bond Strategy Weekly Report, "More Stimulus Needed," available at usb.bcaresearch.com.

BCA Research's Global Investment Strategy service still favors global equities over bonds on a 12-month horizon. However, stocks remain technically overbought and vulnerable to a further correction. Tech stocks rallied hard into September. Aggressive…

The risk of a dollar rebound is only getting larger. As we previously highlighted, our Dollar Capitulation Index is now consistent with an elevated chance of a counter-trend move in the Greenback. However, such a move requires a catalyst. The equity market…

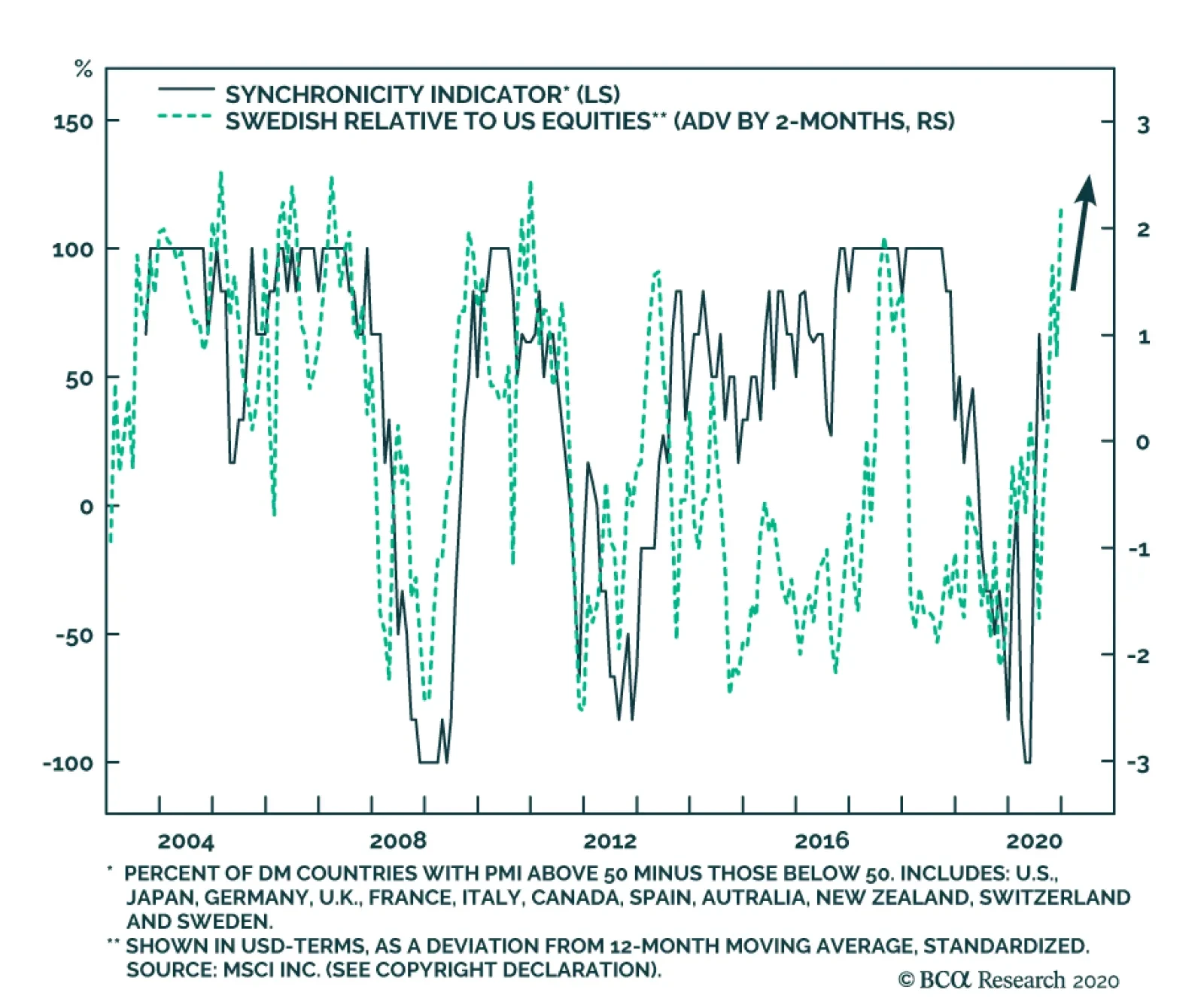

Our BCA Synchronicity Indicator was designed to capture the extent to which countries’ business cycles are moving in sync. To do so, we compute the proportion of countries that have PMIs above 50 versus those below 50. A 100% reading tells us that all the…

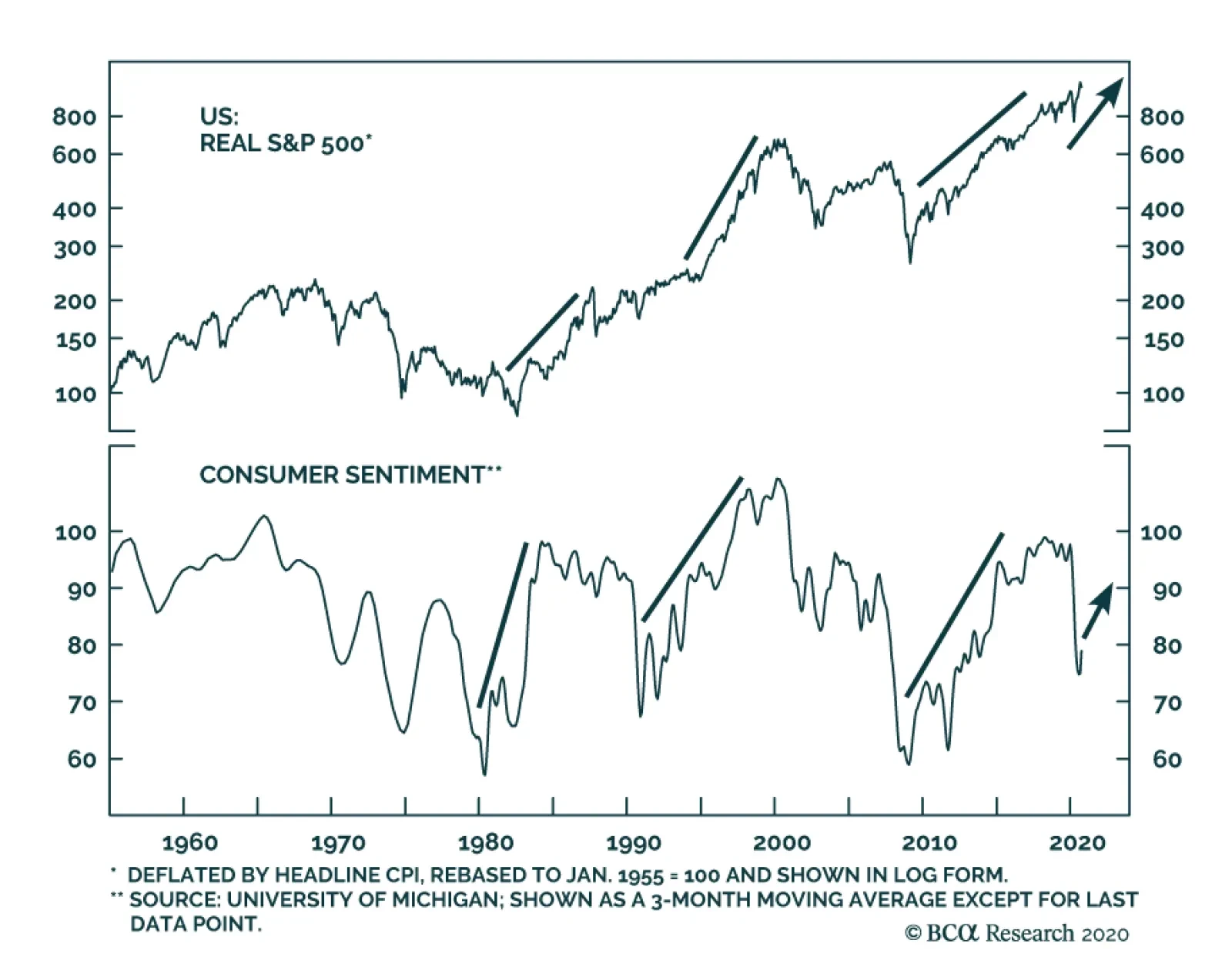

Despite the expiry of the CARES act, the University of Michigan's Consumer Sentiment index rose to 78.9, easily beating expectations of 75. Moreover, both the Current Conditions and Expectations components managed to best anticipations. This strong…