United States

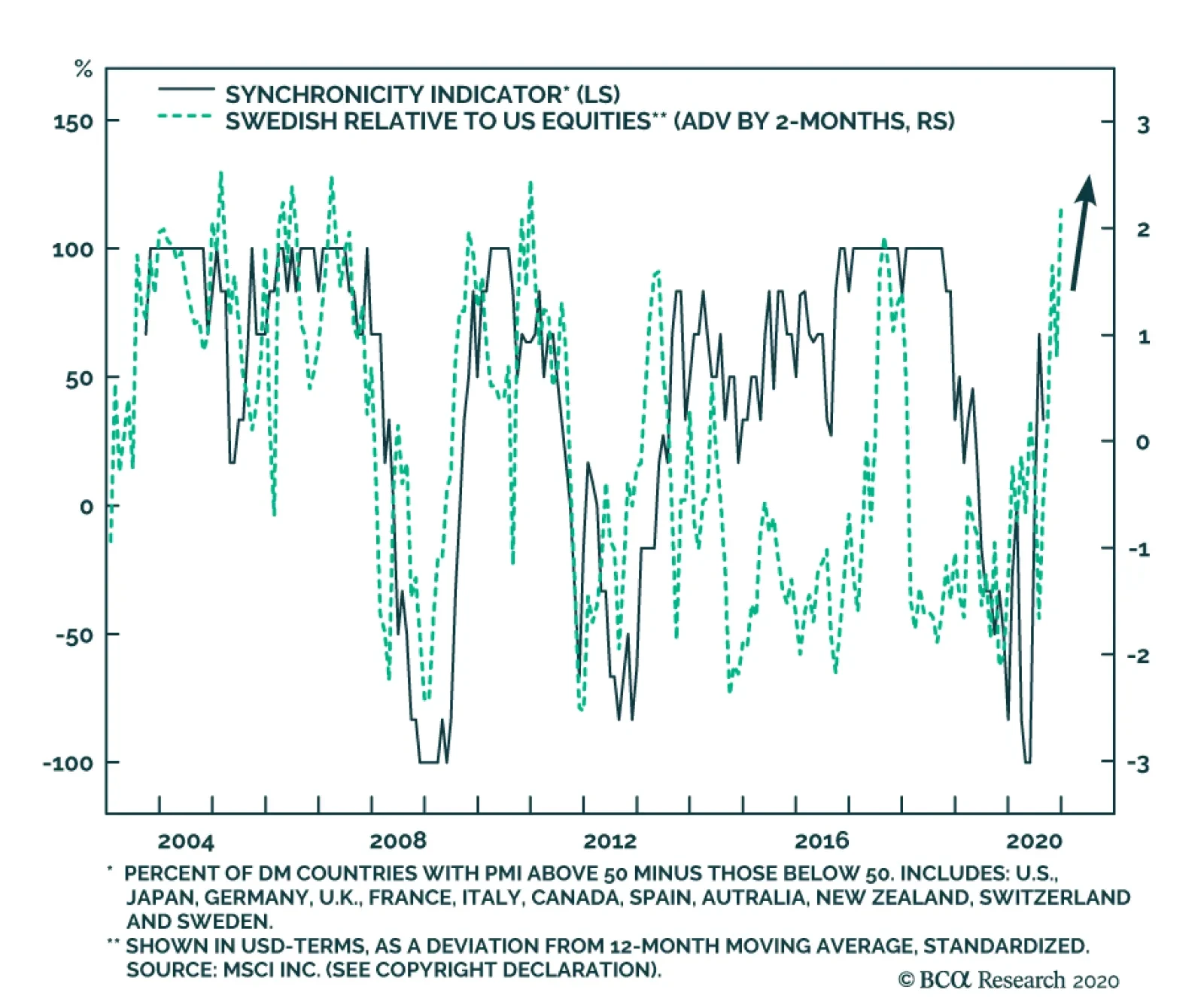

Our BCA Synchronicity Indicator was designed to capture the extent to which countries’ business cycles are moving in sync. To do so, we compute the proportion of countries that have PMIs above 50 versus those below 50. A 100% reading tells us that all the…

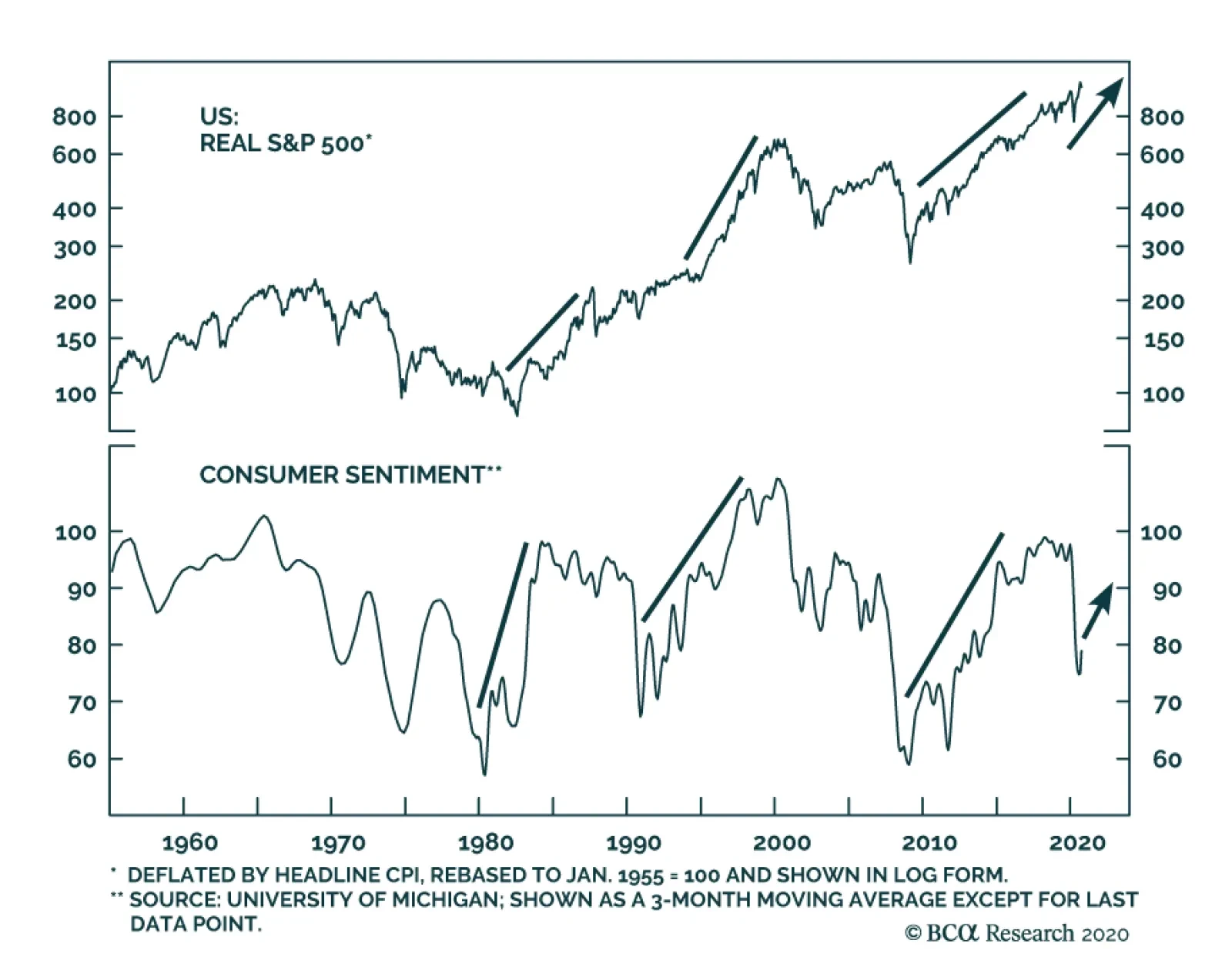

Despite the expiry of the CARES act, the University of Michigan's Consumer Sentiment index rose to 78.9, easily beating expectations of 75. Moreover, both the Current Conditions and Expectations components managed to best anticipations. This strong…

Languishing Buybacks

Languishing Buybacks

This summer we have been highlighting unsustainable trends in the US equity market and today we turn our attention to buybacks. As we first pointed out in the late-2019 Weekly Report, share buybacks have been a key pillar underpinning stocks since the GFC averaging roughly $500bn/annum since 2010, and reaching nearly the $1tn/annum mark in 2018 on the back of President Trump’s massive fiscal easing package. Clearly, such breakneck pace was unsustainable and a renormalization was overdue. Fast forward to Q2, and even our conservative quarterly $125bn equity retirement estimate proved overly optimistic. From the recent peak to just below $90bn/qrt, SPX buybacks have fallen by a whopping 67%. Such a corporate buyer’s strike is negative for the near term prospects of the S&P 500 (top panel). Drilling deeper beneath the surface is revealing. When we disaggregate the headline buybacks number into GICS1 sectors, we observe that once again the tech titans (comprising the S&P technology and the S&P communication services indexes) are doing all the heavy lifting accounting for 70% of the overall number (bottom panel). Q2 was the first time in recent memory that a cross has occurred where tech accounts for more buybacks that all the other sectors put together! Bottom Line: We continue to recommend investors keep some powder dry and refrain from deploying capital at the current juncture. A better entry point in the broad equity market will likely materialize in late Q4.

“Based on a broad set of indicators, it is hard not to see a certain amount of daylight between risky asset prices and economic prospects” – Claudio Borio, Head of Monetary and Economic Department, BIS, September 14, 2020 A pandemic, the resulting sharpest downturn in modern times and soaring government debt have made 2020 an annus horribilis for the US and world economy. Growth has rebounded strongly as economic lockdowns have ended, but most forecasts suggest that the level of activity will not return to its pre-virus level before the end of next year. That implies a lingering problem of high unemployment and there will be ongoing concerns about the eventual consequences of policymakers’ extreme monetary and fiscal actions. The long-run outlook for the US economy was already challenging before Covid-19 appeared on the scene. And this year’s events cannot have improved prospects relative to pre-crisis expectations. Thus, it is reasonable to wonder why the S&P500 hit a new all-time high in early September and currently is only slightly below that level. Is it a classic case of irrational exuberance or a sign that the economic outlook is much better than generally assumed? If we cannot come up with a convincing case for the latter then irrationality is left as a likely explanation. The sharp decline in interest rates certainly supports higher equity valuations, but a bull market that depends largely on stimulative monetary policy is problematic. The Stock Market Is Not The Economy, But… Finance theory states that equity prices should reflect the discounted long-run stream of expected dividend payments. In turn, those payments should be correlated with earnings growth which one would expect to have a close relation to underlying economic conditions. While prices often deviate significantly from so-called fundamentals, it is perfectly reasonable to assume a long-run correlation between the stock market and the performance of the economy. In practice, there is a loose relationship with occasional large deviations. Chart 1The US Economy vs. The Market

The US Economy vs. The Market

The US Economy vs. The Market

Chart 1 shows the five-year annualized growth in US real GDP versus both real total returns from the S&P500 and real earnings.1 In making these comparisons, there are a few issues to consider. The stock market only represents quoted companies while GDP also includes the economic contribution of unincorporated businesses and the government. The sectoral composition of the S&P 500 is different from that of businesses at large. Many large US companies earn a significant share of their earnings from overseas operations that may be uncorrelated with domestic economic conditions. The price performance of stocks can reflect large swings in valuations driven by investor sentiment rather than fundamentals. Starting with the first point, corporate sector GDP accounts for only slightly more than half of total GDP, moving within a range of around 55% to 60% for the past 50 years (Chart 2). Yet the real growth in corporate GDP has moved in lockstep with that of total GDP. And aggregate sales of S&P500 companies have broadly tracked the swings in GDP. Thus, it cannot be argued that quoted companies can somehow miraculously avoid the ups and downs of the overall business cycle. The economy is based on a complex set of interconnected relationships and it would be remarkable if the performance of the country’s major corporations could deviate significantly from the economy at large for any length of time. Chart 2The Corporate Sector And Total GDP

The Corporate Sector And Total GDP

The Corporate Sector And Total GDP

There certainly is an issue with the second point because the sectoral breakdown of the S&P500 does not exactly match that of the overall economy. While that does not always protect the stock market from general economic trends, it can help explain occasional large equity price moves. Table 1 shows the sector composition of the S&P500, weighted by market capitalization, sales and earnings, versus the composition of GDP. It is difficult to break down GDP exactly in line with the sector classifications of the market, but we have done as close a job as the data allows. Notable differences between the structure of the market and GDP are the relative weightings of the health care, industrials and information technology sectors. The following explanations seem plausible. Table 1Sector Composition: A Comparison

The US Economy vs. The Stock Market: Is There A Disconnect?

The US Economy vs. The Stock Market: Is There A Disconnect?

For health care, the GDP weighting shown in the table is understated because it also is a significant part of the government sector’s contribution via Medicare and Medicaid. Other data show that total spending on health care accounts for around 18% of US GDP, broadly in line with the S&P index weighting. The large weighting of industrials in GDP compared with its share of the equity index probably reflects the fact that this broadly-defined group has a very large number of small and unquoted companies. On that point, it should be noted that unincorporated businesses account for 21% of national income – a non-trivial share. Last, but not least, there is the huge discrepancy in the weightings of information technology. This is a bit harder to explain, but two reasons come to mind. First, the S&P index market cap weighting has been boosted by the strong share price performance of these companies and high valuations thus flatter their index importance relative to underlying business activity. The IT weights based on sales and earnings are much lower, but still significantly exceed that in GDP. Secondly, some of these companies (Apple being a prime example) produce very little in the US relative to what they sell in the country. As GDP measures domestic output, this affects the relative weightings. Chart 3Growth In Overseas vs. Domestic Profits

Growth In Overseas vs. Domestic Profits

Growth In Overseas vs. Domestic Profits

Let’s explore the issue about overseas earnings more closely. According to national income data, 45% of the corporate sector’s after-tax profits come from overseas earnings. And that is broadly consistent with the overseas share of sales for S&P500 companies. While the relationship is not perfect, the growth of overseas profits roughly tracks that of domestic profits (Chart 3). And where there have been large divergences, such as in 2009, that often has reflected large swings in oil prices. Overall, it hard to make the claim that the large share of earnings coming from overseas has been a factor supporting the strong performance of stocks relative to the underlying economy. This is especially true given that the US has performed better than most other economies in recent years and the dollar has been a strong currency. In sum, our analysis does not give compelling support to the idea that the fundamental performance of large quoted companies can sustainably diverge from that of the underlying economy. But that does not mean that share prices cannot deviate because of large swings in valuation. Is The US Equity Market Overvalued? This should be a simple question to answer, but often is not. Alternative approaches to valuation are sometimes in conflict and that is the current situation. Various valuation measures are shown in Chart 4 with the following observations. Chart 4AMeasures Of US Equity Valuation

Measures Of US Equity Valuation

Measures Of US Equity Valuation

Chart 4BMeasures Of US Equity Valuation

Measures Of US Equity Valuation

Measures Of US Equity Valuation

All the measures based on earnings (trailing, forward and cyclically-adjusted) suggest that the market is very expensive. While current earnings are affected by the economy’s second-quarter collapse, there remains considerable uncertainty about the speed of recovery. The current forward price-earnings ratio (PER) assumes that earnings will increase by around 30% over the next 12 months and that could prove to be optimistic. The market also looks significantly overvalued based on the ratios of price-to-book, price-to-sales and total market capitalization to GDP. While the valuation of the aggregate index has been boosted by the exceptional performance of the technology sector, it is important to note that the ratios of price to trailing earnings and to sales also are very elevated using the medians of 58 sub-groups, as calculated by BCA’s US Equity Strategy Service (Chart 5). In other words, this is not a story about overvaluation simply reflecting the hot technology sector. Chart 5Overvaluation Is Not Just About Technology

Overvaluation Is Not Just About Technology

Overvaluation Is Not Just About Technology

The market looks much more attractive when comparing dividend and earnings yields with the returns available on cash and bonds. This is the so-called TINA argument (there is no alternative). It is hard not to prefer stocks when the dividend yield is above the yield on long-term government bonds. During the market overshoot of the late 1990s, the dividend yield was 500 basis points below the 30-year Treasury yield, highlighting that stocks were in a very risky phase. Moreover, the current environment of unusually low interest rates is unlikely to end any time soon. The Federal Reserve’s newly-released projections indicate that interest rates are expected to remain at current levels at least through the end of 2023. The Fed has made it abundantly clear that it is prepared to take risks with inflation in order to support a revival in economic activity. It is relatively straightforward when the different valuation metrics are all giving the same message, as was the case in the late 1990s. Even then, the market overshoot lasted longer and became more extreme than generally expected. Our composite valuation indicator takes account of 10 different measures and currently supports the idea that the market is indeed very expensive (Chart 6). Chart 6BCA Equity Valuation Indicator

BCA Equity Valuation Indicator

BCA Equity Valuation Indicator

It currently is very difficult for institutional investors to favor fixed-income instruments over a higher-yielding equity market. However, there is no free lunch here. We cannot ignore the argument that low interest rates reflect a very bleak long-run outlook for economic growth and thus for earnings and stock prices. The secular stagnation view put forward by Larry Summers looks even more apposite today than when he outlined it several years ago. We are fortunate to have Larry as the opening speaker for our virtual Investment Conference on October 6th and it will be extremely interesting to hear his latest thinking. Some Thoughts On The Economic Outlook Equities are a long-duration asset so it makes sense to consider valuations in the context of the long-run economic outlook rather than the near-term ups and downs of activity. Of course, short-run economic moves do affect investor sentiment so cannot be ignored. The near-term outlook is extremely cloudy because of uncertainty about the future path of the pandemic. While the virus appears to have become less virulent, infection rates could climb sharply over the winter months as schools re-open and people spend more time indoors. In addition, there are doubts about the scale and timing of much-needed additional government stimulus. Chart 7Mixed Data On The US Economy

Mixed Data On The US Economy

Mixed Data On The US Economy

Some recent data have been impressively strong. The value of retail sales has surpassed pre-virus peaks as have new and existing home sales (Chart 7). On the other hand, manufacturing and construction output and overall employment remain far below previous peaks. And we have yet to see the impact of the ending of the $600 a week income support. There are legitimate concerns that early 2021 will see a surge in home evictions and a marked increase in small business bankruptcies. Most likely, the economy will experience a bumpy and moderate recovery after its post-lockdown strong third-quarter growth. The Fed forecasts US growth of 4% in 2021 after a 3.7% drop this year and the OECD’s latest projections are similar. That still means that it will take until the end of 2021 before real GDP gets back to its end-2019 level. And there are downside risks to that forecast if the virus remains a lingering problem. Our conference on October 6th will have what is sure to be a lively debate about the US economic outlook between Ed Yardeni and Dave Rosenberg. These two very smart economists have a very different take on how things are likely to play out and what it means for the markets. This debate will follow the presentation by Larry Summers and after that, Peter Berezin, our Chief Global Strategist, and myself will discuss our views and will be open for audience questions. Should be very interesting! Let’s talk about the longer-run economic outlook. As noted at the outset, it was less than inspiring even before the virus arrived on the scene. The two drivers of long-run economic performance are demographics and productivity and the growth in both has been trending lower. Chart 8Demographics Are A Problem

Demographics Are A Problem

Demographics Are A Problem

The demographics story is straightforward and essentially locked in place. A falling birth rate means that the working-age population will rise at a meager 0.2% a year over the next ten years compared with more than 1% a year in the 1980s, 1990s and 2000s. Moreover, growth is projected to remain low in subsequent decades (Chart 8). And even these forecasts may be optimistic if the current antipathy toward immigration leads to a more closed-door stance. Demographic trends not only imply a slow-growing workforce (impacting potential GDP) but also create a worsening picture for government finances. An aging population boosts spending on health care and pensions when the number of taxpayers is growing very slowly. This shows up in a dramatic drop in the ratio of the working-age population (i.e. potential taxpayers) to those aged 65 and above.2 This is happening when government finances are already in dire straits and implies that future tax rates can only go higher, regardless of which political party is in power. The issue of productivity is more contentious because it is hard to measure, and future trends are less predictable than for demographics.3 Nevertheless, the data present a relatively clear picture: the growth of output per hour in the non-financial corporate sector has slowed markedly after a tech-driven spurt in the second half of the 1990s (Chart 9). We show the trend as a five-year growth rate to smooth out the short-term noise in the series. Chart 9Productivity Growth Has Slowed

Productivity Growth Has Slowed

Productivity Growth Has Slowed

We discussed the outlook for productivity in a recent Special Report and highlighted some worrying trends.4 These include weak growth in business investment, a retreat from globalization, increased government involvement in the economy and friction caused by new pandemic-related protocols to protect the safety of customers and workers in several industries. On a more positive note, the virus has forced many businesses to streamline their operations and the move to remote working should boost productivity in some cases. What about the issue of technological advances such as artificial intelligence (AI) and autonomous vehicles? These clearly have the potential to boost productivity in many areas but with a caveat. Previous major technological breakthroughs (often called general purpose technologies or GPTs) such as steam power, the internal combustion engine, electricity, and the internet had major impacts on both supply and demand. Generally, they were associated with creating completely new activities. For example, steam power led to the locomotive which in turn allowed the opening of the country and the movement of goods to distant markets. Similarly, the automobile led to the development of the suburbs and the associated demand for housing and related services. More recently, the internet boosted the demand for a wide range of tech goods and services. While that is still ongoing, its peak effect has passed, helping to explain the decline in productivity growth from late-1990s level. In contrast, a lot of current ‘new’ technologies simply are associated with doing existing tasks more efficiently (3-D printing would be an example). That is still important but not on the same scale as GPTs. There is no doubt that AI will be a big disruptor in many sectors but its impact on demand is less clear. Maybe one day all households will have a domestic robot but that is still far enough away to be in the realm of science fiction. The bigger near-term impact will be job displacement. And the same can be said for autonomous vehicles. The demand for new self-driving cars will rise, but these will simply replace gas-powered ones and perhaps the overall number of vehicles on the road will decline. In sum, there will be both positive and negative forces acting on future productivity growth and any predictions need to be treated with caution. Nonetheless, a base case should probably assume any improvements will be relatively modest. Finally, any discussion of long-run economic prospects cannot ignore the alarming rise in government debt. The US was already running $1 trillion federal deficits before this year’s crisis led to a further extraordinary explosion of red ink (Chart 10). Chart 10Soaring Government Debt

Soaring Government Debt

Soaring Government Debt

Current large deficits are not fazing investors. In the past, the spread between 30-year and 10-year Treasurys widened as the deficit rose, but this relationship has weakened recently (second panel Chart 10). Fed buying of bonds may have had some impact, but it also reflects the weak economy and low inflation. It is hard to know at what point investors will take fright at US fiscal trends. The experience of other countries that faced sovereign debt crises suggests problems can arrive with little advance notice. One day investors seem complacent and the next they are running scared. The dollar’s status as the world’s main reserve currency gives the US more protection than other countries had when facing debt problems. And central banks’ willingness to be the bond buyers of first and last resort gives debt burdens more room to grow than in the past. However, debt arithmetic is relentless and will turn very ugly when bond yields eventually rise. It is futile to try and pin a date on when bond vigilantes might reassert themselves in the US. But it will happen at some point. Moreover, even before that happens, there will be political pressure to do something about soaring debt levels. Even without a market revolt, the burden of increased spending on entitlements and debt servicing will force the government to pursue austerity. Taxes will rise and spending growth will be curtailed. That is a further reason to be cautious about economic prospects. Increased debt is a way to bring spending forward but unless the money is used to invest in productive assets, the process eventually goes into reverse. Unfortunately, the surge in US government borrowing has been used to prop up consumption rather than to finance capital spending. The short- and long-run economic outlook would have been worse if there had not been a powerful fiscal response. Consumption would have suffered an even sharper decline with a catastrophic impact on employment, profits and capital spending. In that sense, the government really had no choice: the health of government finances becomes irrelevant in the midst of a pandemic-related economic collapse. Market Implications There are several explanations for the remarkable strength of the US equity market. Prime place goes to the Fed’s hyper-easy monetary stance. A policy of zero interest rates with a stated intention to keep them there for a long time has the desired effect of boosting risk-taking. A second factor has been excitement about technology that has created a bubble in that sector. And then there is the view that novice retail investors have been seduced into the market by online applications such as Robinhood that make day trading very easy. Missing from the above list is the suggestion that investors expect the economy to be strong enough to validate the market’s current level. That just does not seem plausible because it is not credible that earnings could grow strongly enough to lower valuations to more reasonable levels over the next five to ten years. If the bull case for stocks rests simply on the TINA argument, then it implies equities will remain in a bubble over the medium term. That certainly is possible but not the foundation for a sound investment strategy. It is not easy to come up with an investment strategy when no asset is cheap. BCA’s House View is still to prefer equities on a cyclical basis and the challenge will be timing when to jump off the train. In conclusion, my answer is that there is indeed a disconnect between the economy and equity market. This may persist for quite a while but does not appear sustainable. I am reminded of the late 1990s when the bull market lasted much longer and moved far higher than I and many others expected. Yet, fundamentals eventually did matter with the S&P500 dropping by almost 50% over the space of 30 months. I am not suggesting that a similar decline is imminent and if the 1990s example is relevant, then the market can continue to rise for quite a while, and I am sure the BCA view will prove to be correct. However, ever the skeptic, my bias is to err on the side of caution rather than try to maximize returns. Let me end by giving our upcoming conference another plug. The outlook for US equities will be discussed by Liz Ann Sonders and Ned Davis, two highly-respected market analysts and we will have a separate important session on coming up with the ideal investment strategy from three different perspectives: the buy side, the sell side and independent research In addition, over the four days of the event, we will have high-level discussions of all the other key issues that will drive markets including China, geopolitics, the US election, currencies, and policy challenges. Find out more at https://www.bcaresearch.com/conference2020. Martin H. Barnes, Senior Vice President Chief Economist mbarnes@bcaresearch.com Footnotes 1Total returns and earnings were deflated using the corporate price deflator. 2Obviously, not everyone of working age pays much in the way of taxes and there are many aged 65 above who pay lots of taxes. But that does not abstract from the dramatic change in the ratio. 3If you want to know how many 70-year old people there will be in 10 years’ time, simply count the number of 60-year olds today and apply an appropriate mortality rate. 4Please see BCA Special Report "Beyond the Virus," dated May 22, 2020, available at bca.bcaresearch.com

Dear Client, We will be working on our Fourth Quarter Strategy Outlook next week, which will be published on Tuesday, September 29th. We will also be hosting a webcast on Thursday, October 1st at 10:00 AM EDT (3:00 PM BST, 4:00 PM CEST, 10:00 PM HKT) where we will discuss the outlook. Best regards, Peter Berezin, Chief Global Strategist Highlights Investors should favor global equities over bonds on a 12-month horizon. However, stocks remain technically overbought in the short term and vulnerable to a further correction. Investors are not fully appreciating the degree to which fiscal policy has already tightened in the US. While we ultimately expect a deal to be reached, it may take a stock market sell-off to force Republican leaders to accede to Democratic demands for more spending. US monetary policy will stay accommodative for at least the next two years, a view that this week’s FOMC meeting further validated. Investors should pivot into cheaper areas of the stock market – in particular, deep cyclicals and financials, non-US stocks, and value stocks. Value stocks are especially appealing, as they are now trading at the biggest discount on record relative to growth stocks. The “pandemic trade” will give way to the “reopening trade.” The latter will benefit value stocks. In addition, stronger global growth, ongoing Chinese stimulus, a weaker US dollar, and modestly steeper yield curves all favor value indices. Value investors who want to accentuate their returns should pay special attention to smaller value companies outside the US. Market Commentary Chart 1Drastic Drop In Weekly Unemployment Insurance Payments

Drastic Drop In Weekly Unemployment Insurance Payments

Drastic Drop In Weekly Unemployment Insurance Payments

We continue to favor global equities over bonds on a 12-month horizon. However, stocks remain technically overbought in the short term despite correcting modestly over the past few weeks. Tech stocks rallied hard into September. Aggressive buying of out-of-the-money call options helped fuel the rally. While some big institutional players such as Softbank have reportedly scaled back their positions, many retail investors remain unfazed. The triple leveraged long Nasdaq 100 ETF, TQQQ, experienced the largest weekly inflow on record in September. In addition to being technically stretched, equities face near-term risks from the impasse in the US Congress over a new stimulus bill. Investors are not fully appreciating the degree to which fiscal policy has already tightened in the US. Chart 1 shows that weekly unemployment payments have fallen by $15 billon since the end of July, representing a drop of more than 50%. At an annualized rate, this amounts to 3.7% of GDP in fiscal tightening. On top of that, the funds in the small business Paycheck Protection Program have run out, while many state and local governments face a severe cash crunch. BCA’s geopolitical strategists expect a fiscal deal to be reached over the next few weeks. The fact that Speaker Nancy Pelosi has said that Congress will stay in session until both sides agree on an aid package is good news in that regard. Nevertheless, given all the acrimony in Washington in the run up to the November election, there is still a non-negligible chance that a deal falls through. Why, then, are we still bullish on stocks on a 12-month horizon? Partly it is because voters want more stimulus, which means that fiscal policy is likely to be loosened again, even if this does come after the election. It is also because the pandemic seems to be receding. While the number of new cases is rising again in the EU and some other regions, fatality rates remain much lower than during the first wave. Progress also continues to be made on developing a viable vaccine. According to The Good Judgment Project, about 60% of “superforecasters” expect a mass-distributed vaccine to be available by Q1 of 2021, up from 45% just four weeks ago. Only 2% expect there to be no vaccine available by April 2022, down from over 50% in May (Chart 2). Chart 2High Odds Of A Vaccine Within 6-To-12 Months

Pivot To Value

Pivot To Value

Lastly, monetary policy remains exceptionally accommodative. The Fed this week formally incorporated its new flexible average inflation targeting strategy into its post-meeting statement. The FOMC promised to keep rates at rock-bottom levels until the economy has reached “maximum employment” and inflation “is on track to moderately exceed two percent for some time.” The dot plot indicated that the vast majority of FOMC members did not expect rates to rise until at least the end of 2023. As Chart 3 shows, the global equity risk premium remains quite elevated. This favors stocks over bonds. Not all stocks are equally attractive, however. Four weeks ago, in a report titled “The Return of Nasdog,” we made the case that investors should pivot away from growth stocks towards value stocks. The report generated quite a bit of interest from readers. Below, we review and elaborate on some of the issues raised in a Q&A format. Q: Being long value stocks relative to growth stocks has been a widowmaker trade for more than a decade. Why do you think we have reached an inflection point? A: Value stocks are cheaper now compared to growth stocks than at any point in history – even cheaper than at the height of the dotcom bubble (Chart 4). Chart 3Global Equity Risk Premium Remains Quite Elevated

chart 3

Global Equity Risk Premium Remains Quite Elevated

Global Equity Risk Premium Remains Quite Elevated

Chart 4Value Stocks Are Extremely Cheap Relative To Growth Stocks

Value Stocks Are Extremely Cheap Relative To Growth Stocks

Value Stocks Are Extremely Cheap Relative To Growth Stocks

Admittedly, valuations are not a good timing tool. One needs a catalyst to unlock those valuations. Good news on the virus front may end up being such a catalyst. The “pandemic trade” benefited tech stocks, which are overrepresented in growth indices. It also favored health care stocks, which are similarly overrepresented in growth indices, at least globally (Table 1). The “reopening trade” will support companies such as banks, hotels, and transports that were crushed by lockdown measures and which are overrepresented in value indices. Table 1Breaking Down Growth And Value By Sector

Pivot To Value

Pivot To Value

Chart 5 shows that retail sales at physical stores are rebounding, while online sales growth is coming down from highly elevated levels. Bank of America estimates that US e-commerce penetration doubled in just a few short months earlier this year. Some “reversion to the trend” is likely, even if that trend does favor online stores over the long haul. Meanwhile, PC shipments soared during the pandemic as companies and workers rushed out to buy computer gear to allow them to work from home (Chart 6). To the extent that this caused some spending to be brought forward, it could create an air pocket in tech demand over the next few quarters. Chart 5Are Brick-And-Mortar Retailers Coming Back To Life?

Are Brick-And-Mortar Retailers Coming Back To Life?

Are Brick-And-Mortar Retailers Coming Back To Life?

Chart 6The Pandemic Has Caused Global Server And PC Shipments To Surge

The Pandemic Has Caused Global Server And PC Shipments To Surge

The Pandemic Has Caused Global Server And PC Shipments To Surge

Q: How are investors positioned towards value versus growth? A: According to the September BofA Global Fund Manager Survey, tech and pharma were the two sectors with the largest reported overweights. Thus, there is significant scope for money to shift out of these sectors. Q: What about the overall macro environment underpinning growth and value? A: While the relationship is far from perfect, value stocks tend to outperform growth stocks when the US dollar is weakening (Chart 7). Recall that growth stocks did very well during the late 1990s, a period of dollar strength. In contrast, value stocks outperformed between 2001 and 2007, a period during which the dollar was generally on the back foot. As we have spelled out in past reports, we expect the dollar to weaken over the next 12 months, which should benefit value stocks. Value stocks also tend to do best when global growth is accelerating (Chart 8). Provided that governments maintain adequate levels of fiscal support and a vaccine becomes available by early next year, global GDP should bounce back swiftly. Chart 7Value Stocks Tend To Outperform Growth Stocks When The US Dollar Is Weakening

Value Stocks Tend To Outperform Growth Stocks When The US Dollar Is Weakening

Value Stocks Tend To Outperform Growth Stocks When The US Dollar Is Weakening

Chart 8Value Stocks Also Tend To Do Best When Global Growth Is Accelerating

Value Stocks Also Tend To Do Best When Global Growth Is Accelerating

Value Stocks Also Tend To Do Best When Global Growth Is Accelerating

Q: Won’t lower real bond yields favor growth stocks? A: By definition, growth companies generate more of their earnings further in the future than value companies. As such, a decline in real yields will tend to increase the present value of cash flows more for growth companies than for value companies. We do not expect real yields to rise significantly over the next two years. However, given that real yields are already deeply negative in almost all countries, they probably will not fall either. Q: You seem to be making the cyclical case for the outperformance of value stocks. But what about the secular case? It appears to me that the stronger earnings growth displayed by growth stocks will ultimately translate into higher long-term returns. A: Historically, that has not been the case. As Chart 9 and Table 2 illustrate, value stocks have outperformed growth stocks by a wide margin over the past century. In particular, small cap value has clobbered small cap growth. Chart 9Value Stocks Have Outperformed Growth Stocks By A Wide Margin Over The Past Century

Pivot To Value

Pivot To Value

Table 2Small Caps Vis-A-Vis Large Caps: Comparison of Total Returns

Pivot To Value

Pivot To Value

How did value stocks manage to triumph over growth stocks if, as you say, growth stocks usually experience faster earnings growth? The answer has to do with what is priced in and what is not. If everyone expects a company’s earnings to grow next year, this will already be reflected in its share price. It is only unanticipated earnings growth that should move share prices. For the most part, both analysts and investors have tended to overextrapolate near-term earnings growth. As we discussed in a special report titled “Quant-Based Approaches To Stock Selection And Market Timing,” while analysts are generally able to predict which companies will display superior earnings growth over the next one-to-two years, they systemically overestimate earnings growth on longer-term horizons (Chart 10). As a result, investors tend to overpay for growth, causing growth stocks to lag value stocks. Chart 10A Mug’s Game

Pivot To Value

Pivot To Value

Q: That may have been true historically, but it seems that more recently, investors have been guilty of underpaying for growth. A: Yes and no. If one looks at the period between 2007 and 2017, the superior performance of growth stocks was broadly matched by their superior earnings growth. As a result, relative P/E ratios did not change much. Since 2017, however, the P/E ratio for growth indices has soared relative to value indices (Chart 11). Chart 11AThe Outperformance Of Growth Stocks Over The Past Three Years Has Been Turbocharged By A Rapid P/E Multiple Expansion

The Outperformance Of Growth Stocks Over The Past Three Years Has Been Turbocharged By A Rapid P/E Multiple Expansion

The Outperformance Of Growth Stocks Over The Past Three Years Has Been Turbocharged By A Rapid P/E Multiple Expansion

Chart 11BThe Outperformance Of Growth Stocks Over The Past Three Years Has Been Turbocharged By A Rapid P/E Multiple Expansion

The Outperformance Of Growth Stocks Over The Past Three Years Has Been Turbocharged By A Rapid P/E Multiple Expansion

The Outperformance Of Growth Stocks Over The Past Three Years Has Been Turbocharged By A Rapid P/E Multiple Expansion

Q: What has happened since 2017 that has caused growth stocks to become so much more expensive? A: FANG, FAANG, FANGMAN, whatever acronym you want to use, it was mainly a story about investors becoming infatuated with mega cap tech stocks. After seeing these companies beat earnings estimates quarter after quarter, investors decided that they deserve to trade at much higher valuation multiples. Q: What about other tech companies? A: For the most part, they were left in the dust. Our proprietary Equity Analyzer system allows us to sort companies based on all types of fundamental and technical factors. Chart 12 shows that “value tech” companies trading in the bottom quartile of price-to-earnings, price-to-operating cash flow, price-to-free cash flow, price-to-book, and price-to-sales have gotten completely clobbered by “growth tech” companies trading in the top quartile of these valuation metrics. Chart 12Value Tech Versus Growth Tech

Pivot To Value

Pivot To Value

Interestingly, the opposite pattern was true among financials: “Value financials” – financials that trade cheaply based on the valuation measures listed above – have outperformed “growth financials.” The net result is a bit surprising: Since “value tech” underperformed the average tech stock, while “value financials” outperformed the average financial stock, the average “value tech” stock has delivered a return over the past decade that was almost identical to the average “value financial” stock. Chart 13There Was No Money To Be Made By Shifting Value Exposure From Financials To Tech In Recent Years

There Was No Money To Be Made By Shifting Value Exposure From Financials To Tech In Recent Years

There Was No Money To Be Made By Shifting Value Exposure From Financials To Tech In Recent Years

Q: This seems to suggest that value managers would not have made any money by shifting exposure from financials to tech? A: Correct. Consider the iShares MSCI USA Value Factor ETF (ticker: VLUE). It is structured to have the same sector weights as the overall US market. It currently has 27% of its assets in technology and 10% in financials. Compare that to the Vanguard Value Index Fund ETF Shares (ticker: VTV). It has 10% of its assets in technology and 19% in financials. As Chart 13shows, VTV has actually outperformed VLUE over the past five years. Year to date, VTV is down 10%, while VLUE is down 15%. Q: While value managers would not have made money by shifting capital from financials to tech, I presume the same thing could not be said for growth managers. A: You can say that again. “Growth tech” outperformed the average tech stock, while “growth financials” underperformed the average financial stock. Thus, shifting money from “growth financials” to “growth tech” would have supercharged returns. Q: This still leaves open the question of why mega cap stocks were able to grow earnings so rapidly? A: Two explanations come to mind. First, tech companies often gain from so-called network effects: The more people there are who use a particular tech platform, the more attractive it is for others to use it. Second, tech companies benefit from scale economies. Once a piece of software has been written, creating additional copies costs nothing. Even in the hardware realm, the marginal cost of producing an additional chip is tiny compared to the fixed cost of designing it. All of this creates a winner-take-all environment where success begets further success. Q: It seems this process could go on indefinitely? A: Not indefinitely. No company can control more than 100% of its market. There is also a limit to how big the overall market can get. Close to three-quarters of US households already have an Amazon Prime account. Slightly over half have a Netflix account. Nearly 70% have a Facebook account. Google commands 92% of the internet search market. Together, sites owned by Google and Facebook generate about 60% of all online advertising revenue. Q: These companies have plenty of cash. Can’t they try to enter new types of businesses if they want to keep growing? A: They can try, but there is no guarantee they will succeed. Kodak was one of the pioneers in digital photography. However, it could never really reinvent itself and ended up fading into oblivion. Moreover, while first-mover advantage is a powerful force, it is not invincible. At one point during the dotcom bubble, Palm’s market capitalization was over six times greater than Apple’s. The Blackberry superseded the PalmPilot; the iPhone, in turn, superseded the Blackberry. History suggests that many of today’s technological leaders will end up as laggards. Q: And I suppose government policy could also turn less friendly towards tech? A: That is a definite risk. Republicans have been cheap dates for tech companies. Republican politicians have showered tech companies with tax cuts and allowed them to exploit a variety of loopholes in the tax code. They also kept tech regulation to a minimum. All this happened despite the fact that many tech leaders have publicly panned conservative viewpoints, while tech company employees have rewarded Democratic politicians with the lion’s share of campaign donations (Chart 14). Chart 14Tech Company Employees Donate Heavily Towards Democrats

Pivot To Value

Pivot To Value

Going forward, Republicans are likely to sour on big tech. According to a recent Pew Research study, more than half of conservative Republicans favor increasing government regulation of tech companies (Chart 15). Tucker Carlson, a leading indicator for where the Republican party is heading, has frequently lambasted tech companies on his highly popular television show. Chart 15Conservatives Favor Increased Government Regulation Of Big Tech Companies

Pivot To Value

Pivot To Value

For their part, the Democrats are moving to the left. Alexandria Ocasio-Cortez, a leading indicator for the Democratic party, has voiced her support for Senator Elizabeth Warren’s calls to break up big tech. She has also accused Amazon of paying starvation wages, adding that "If Jeff Bezos wants to be a good person, he'd turn Amazon into a worker cooperative." Q: The political climate for tech companies may be souring. But couldn’t one say the same thing about banks and energy companies, which are overrepresented in value indices? A: One difference is that tech companies trade at premium valuations, while banks and energy companies trade near book value (Chart 16). Another difference is that banks have already felt the wrath of regulators. Thanks to Dodd-Frank and pending Basel III regulations, banks today function more like utilities than like the casinos of yesteryear. While private credit growth is unlikely to return to its pre-GFC pace, banks will still profit from a revival in global growth and increasing consolidation within their industry. Stronger global growth should also allow for modestly higher nominal bond yields and somewhat steeper yield curves. This will benefit bank shares (Chart 17). Chart 16Tech Firms Trade At Premium Valuations

Tech Firms Trade At Premium Valuations

Tech Firms Trade At Premium Valuations

Chart 17Modestly Higher Bond Yields Will Benefit Bank Shares

Modestly Higher Bond Yields Will Benefit Bank Shares

Modestly Higher Bond Yields Will Benefit Bank Shares

As far as energy stocks are concerned, again, we need to benchmark our views to what the market expects. Oil is not going back above $100 per barrel anytime soon, but it does not need to for energy stocks to go up. Bob Ryan, BCA’s chief commodity strategist, sees Brent averaging $65/bbl in 2021, $19 above what is currently priced in forward markets. Q: What about materials and industrial stocks? They are also overrepresented in value indices. A: Both materials and industrials tend to outperform the broader market when global growth accelerates (Chart 18). To the extent we expect global growth to rise, this is good news for these two sectors. They also trade at attractive valuations. Q: How does China figure into this value/growth debate? A: As we saw during the 2001-2007 period, strong Chinese demand for commodities and industrial goods benefits value indices. Even though trend Chinese GDP growth has decelerated over the past decade, the Chinese economy is five-times as large as it was back then. In absolute terms, Chinese consumption of most metals continues to increase (Chart 19). Chart 18Materials And Industrials Usually Outperform When Growth Accelerates

Materials And Industrials Usually Outperform When Growth Accelerates

Materials And Industrials Usually Outperform When Growth Accelerates

Chart 19Chinese Consumption Of Most Metals Continues To Rise

Chinese Consumption Of Most Metals Continues To Rise

Chinese Consumption Of Most Metals Continues To Rise

Chart 20 shows that Chinese GDP would need to grow by about 6% per year over the next decade to keep output-per-worker on track to converge with, say, South Korea by the middle of the century. Thus, Chinese demand for natural resources and machinery is unlikely to weaken anytime soon. Chart 20China Still Has Some Catching Up To Do

China Still Has Some Catching Up To Do

China Still Has Some Catching Up To Do

Q: Let’s wrap up. What final tips would you give investors who want to pivot towards value? A: There are a number of ETFs that track value indices. We expect them to outperform the broad indices over the coming years. For investors who want even higher returns, a selective approach would help. Distinguishing between value stocks and value traps is not easy. True value stocks have often congregated in the shadows of the market, where there is limited analyst coverage and thin institutional ownership. The small-cap sector offers more opportunities for finding such mispriced stocks. Hence, it is not surprising that historically, the value premium has been greater in the small cap realm. The same is true for emerging markets and smaller developed economies (Chart 21).1 Thus, investors who want to accentuate their returns should pay special attention to smaller value companies outside the US. Chart 21AHistorically, The Value Premium Has Been Greater In The Small Cap Realm In Emerging Markets And Smaller Developed Economies

Pivot To Value

Pivot To Value

Chart 21BHistorically, The Value Premium Has Been Greater In The Small Cap Realm In Emerging Markets And Smaller Developed Economies

Pivot To Value

Pivot To Value

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 Please see Global Asset Allocation Special Report, “Value? Growth? It Really Depends!” dated September 19, 2019. Global Investment Strategy View Matrix

Pivot To Value

Pivot To Value

Current MacroQuant Model Scores

Pivot To Value

Pivot To Value

Highlights The great political surprises of 2016 are approaching key deadlines on November 3 and December 31. Investors should not let Brexit take their eye off the US election. Globalization will retreat faster under Trump regardless of what happens in the United Kingdom. The market is starting to price several clear risks: a failure to extend fiscal relief in the US (25% chance); a surprise Trump tariff move (40%); a contested election (20%); or a failure of the UK and EU to seal a deal (35%). Trump is unlikely to pull off a landslide like Boris Johnson in December 2019. The backdrop has darkened and Biden is an acceptable alternative for voters, unlike Jeremy Corbyn. Go long GBP-USD at the 1.25 mark; go long GBP-EUR volatility. Feature The end game is approaching for the two great political shocks of 2016 – Brexit and Trump. November 3 is the US election and December 31 is the deadline for an UK-EU trade deal. Investor sentiment is starting to show some cracks for various reasons, some technical (Chart 1). But we do not believe near-term volatility and risk-off sentiment have fully run their course yet. Either the US election cycle or the UK’s brinkmanship with the EU, or both, will agitate markets as the deadlines approach. The former is a much weightier factor. Chart 1Market Starts To Price Bevy Of Near-Term Risks ... But Cyclical View Still Constructive

Market Starts To Price Bevy Of Near-Term Risks ... But Cyclical View Still Constructive

Market Starts To Price Bevy Of Near-Term Risks ... But Cyclical View Still Constructive

The risks in play are a failure to extend fiscal relief in the US (25% chance); a conflict between Trump and one of America’s foreign rivals such as China, whether due to Trump’s reelection or lame duck status (40%); a contested election (20%); or a failure of the UK and EU to seal a deal, setting back their economic recovery (35%). Maybe all of these risks will dissipate by mid-November, but maybe not. The market has not discounted any of them fully. So investors should buy insurance now. Vox Populi Is The Biggest Constraint For global investors Brexit is far less consequential than President Trump’s “America First” policy but the UK does punch above its economic weight in financial markets (Chart 2). Chart 2Brexit: Why Should We Care? UK Punches Above Its Economic Weight In Financial Markets

Brexit: Why Should We Care? UK Punches Above Its Economic Weight In Financial Markets

Brexit: Why Should We Care? UK Punches Above Its Economic Weight In Financial Markets

Geopolitical analysis teaches that limitations on policymakers should be the starting point of analysis. For democracies, the biggest constraint of all is the vox populi – the voice of the people, or popular will. The Brexit movement faced a vociferous “Resistance” that won over the media and financial market consensus until reality struck in the general election of December 12, in which the Conservative Party won a historic victory. Chart 3Joe Biden Is Not Jeremy Corbyn

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

The election vindicated Prime Minister Boris Johnson’s brinkmanship and “hard Brexit” terms, while once again chastening the elites and experts – including an innovative Supreme Court. Johnson’s single-party majority, combined with COVID-19 and the surge in domestic economic stimulus, have increased the odds that the UK will choose sovereignty over the economy and walk away from trade talks. Trump’s supporters show the same enthusiasm as Brexiteers and the same scorn for conventional wisdom and opinion polls. Will they be similarly vindicated? Beyond any knee-jerk equity rally, that would entail a “Phase Two” trade war with China – and possibly a new trade war with Europe or a global trade war. However, Trump faces much worse odds than Boris Johnson did. First, Johnson’s snap election took place at the top of the business cycle, back when a novel coronavirus was just starting to be discovered in Wuhan, China. This is how Harry Truman won his surprise victory in 1948, in defiance of all the opinion polls. Had Truman run in 1949, after a deep recession, the story would have gone differently – which is a problem for both Trump and the near-term equity market. Second, the political alternative was not acceptable in the United Kingdom but it is in the United States. Johnson led Jeremy Corbyn, a far-left rival for the premiership, by around 15%-20% in the polls. The Conservative Party itself led the Labour Party by 10%. By contrast, former Vice President Joe Biden is a center-left Democrat who has many flaws but is not out of the mainstream. He leads President Trump in the polling, as do Democrats over Republicans, though only by single digits. There is no contest between Biden and Corbyn (Chart 3). Trump might still win, but an American version of the UK landslide in 2019 is unlikely. Trump will lose the popular vote even if he wins the Electoral College, and Republicans have a very slim chance of winning the House of Representatives. The implication for financial markets is doubly negative, at least in the near term: there is about a 35% chance that the UK will leave without a deal and about a 35% chance that Trump will win. He could also kick China in the interim period if he loses. Won’t stocks cheer a Trump comeback and victory? Perhaps, but a data-dependent approach suggests that a “blue sweep” is still the base case, and that would be a good trigger for a full equity correction. Nor would a Trump win be positive for long-term equity returns in the final analysis. Trump is reflationary, but a larger trade war would hamper the global economic recovery and thus keep earnings suppressed. There is a 35% chance that Trump will win re-election. Trump is unlikely to win the national vox populi, like Brexit did, but he obviously can win the popular vote in the critical regions – the Sun Belt and the Rust Belt. If he does, the revolution in the global system will be confirmed: the retreat of globalization will accelerate. If he does not, then Brexit alone cannot confirm de-globalization; rather the UK will face even more pressure to make concessions and get a trade deal. Trump’s Path To Victory Chart 4Sitting Presidents Win Half The Time If Recession Ends In H1

Sitting Presidents Win Half The Time If Recession Ends In H1

Sitting Presidents Win Half The Time If Recession Ends In H1

We may well be forced to upgrade Trump’s odds of winning if his comeback gains momentum. Our subjective odds of a Trump win come from the historical record – incumbent parties only retain the White House amid recessions five out of 13 times in American history – but there are some important exceptions. First, the longest-serving American president, Franklin Delano Roosevelt, served during the Great Depression. So obviously a bad economy does not always disqualify a president. Nevertheless FDR got lucky with the timing of the fluctuations and he was personally popular, unlike President Trump. Second, an incumbent president wins 50% of the time if the recession ends before the election – namely in 1900, 1904, and 1924 (contrasted with defeats in 1888, 1912, and 1980). Today’s market performance looks similar to these cases, though premature fiscal tightening is now jeopardizing Trump’s bid (Chart 4). Assuming new stimulus passes, it is extremely beneficial for President Trump that COVID-19 cases are subsiding (Chart 5). Chart 5COVID-19 Subsides In Nick Of Time For Trump?

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

Chart 6Even Approval Of Trump’s Pandemic Response Improving

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

His approval rating on handling COVID-19 is somewhat recovering at the moment (Chart 6). Trump’s “law and order” message is also benefiting him amid the rise in vandalism, rioting, and homicide, judging by his improvement in national approval rating across almost all demographic groups, including many that are otherwise averse to Trump. Finally, Trump’s Abraham Accords – a potentially major peace deal between Israel and an expanding list of Arab states – could give his image another boost (Table 1). Foreign policy will not decide the election but these peace deals should not be underrated because they underscore a more important argument for voters: that the US should withdraw from its endless foreign wars and pursue peace and prosperity instead. If Trump’s typically weak approval rating on foreign policy starts to rise then his comeback gains breadth. Table 1The Abraham Accords Give Boost To Trump Image As Peacemaker

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

We will upgrade our 35% odds of Trump’s re-election if Congress passes a new fiscal relief package, assuming Trump’s polling continues to improve. Our quantitative model is now giving Trump a 45% chance, which is in line with the consensus view but well above our subjective odds (Chart 7). We will upgrade our view if Congress passes a new fiscal relief package, assuming Trump’s polling continues to improve. Chart 7Quantitative US Election Model Puts Trump Win At 45% Odds

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

Chart 8Stimulus Hiccups Cause Market To Sell

Stimulus Hiccups Cause Market To Sell

Stimulus Hiccups Cause Market To Sell

The stock market does not perform well during periods in which fiscal cliff negotiations are prolonged – the failure of the Emergency Economic Stabilization Act in 2008 is one thing, but today’s impasse is more reminiscent of the debt ceiling crises of 2011 and 2013. Trump is now directly pressuring Senate Republicans to capitulate to House Democratic spending demands. If Republican senators abandon him, market turmoil will undercut his argument that he is the best man to revive the economy and he will lose the election (Chart 8). We do not think they will – and House Speaker Nancy Pelosi’s pledge to keep the House in session until a deal is passed is very positive news – but until the deal is sealed the market is vulnerable. As mentioned above we give a 25% chance of a failure to pass any stimulus bill in September or October. The next chance for stimulus will be in late January or February. Trump stands for growth at all costs, which will be received well by equity markets, other things being equal. But a Trump victory implies more trade war and that the GOP will retain the Senate, creating a steeper fiscal cliff next year – so any relief rally will be short-lived. Meanwhile a Trump defeat raises the risk he will take aggressive actions on the way out to cement his legacy as the Man Who Confronted China, and bind the Biden administration to decoupling policy. This is not a favorable outlook for investor sentiment or the economic recovery over the next few months. Brexit: The Three Kingdoms Will Force A Trade Deal Chart 9Sterling Will Fall Before It Bounces Back On A Deal

Sterling Will Fall Before It Bounces Back On A Deal

Sterling Will Fall Before It Bounces Back On A Deal

In December 2016 we pointed to the three kingdoms – England, Ireland, and Scotland – as the origin of the geopolitical and constitutional crisis that would arise from the Brexit referendum and act as a powerful bar against a no-deal Brexit. That framework remains salient today as the risk of no-deal escalates due to quarrels over Northern Ireland Protocol, which was agreed in October 2019 as part of the formal Withdrawal Agreement that made Brexit happen on January 31, 2020. The implication is that the pound has not bottomed yet, though we see a buying opportunity around the corner (Chart 9). No one should doubt that the UK could walk away from the EU without a deal this December: The Tories’ single-party majority gives them the raw capability to push through plans they decide on – and raises the risk that they will overreach. The tariff shock of a no-deal exit is frequently exaggerated. The UK would suffer a tariff shock of about 1.38% of GDP, larger than what the US suffered in its tariff-war with China but hardly a death knell (Table 2). (The costs of losing single-market access would grow over time, however.) Table 2A No-Trade-Deal Brexit Would Create A Minimum Tariff Shock Of 1.4% Of GDP

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

COVID-19 has supplanted the worst-case outcome of a no-deal exit by producing a much worse recession than anyone feared. The US is using the disruption to decouple from China and the UK could do the same with the EU. The result of COVID-19 is massive domestic stimulus that raises the UK’s and Europe’s threshold for pain. Any failure of trade talks would spur more stimulus. The Bank of England still has some bond-buying ammunition left and parliament, again, is undivided. Given that Boris Johnson has until 2024 before the next election, there is theoretically time for his personal and party approval ratings to improve as the economy recovers from the pandemic and any messy Brexit (Chart 10). Chart 10Bojo Has Until 2024 To Recover From Crises

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

Chart 11UK Would Face WTO-Level Tariffs If No Deal

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

The UK’s position in the quarrel over Ireland is rational – but so is the EU’s. If the trade talks collapse, the UK will need to remove any regulatory or customs divisions with Northern Ireland. Yet in preparing to do so it vitiates trust with the EU and makes a trade deal less likely. However, weighing all these points up, an UK-EU trade deal is still the most likely outcome (65% chance), as the economic and political costs are crystal clear while the benefits of a hard break are not so clear. Allow us to explain. Northern Ireland is the latest cause of tensions, although it was inevitable that tensions would arise ahead of the end-of-year deadline for a trade deal. Westminster has proposed an Internal Market Bill, which has passed with solid majorities in two readings in parliament, to reclaim aspects of sovereignty over Northern Ireland that were traded away to clinch the Withdrawal Agreement last year. The Johnson government’s position should be seen as a negotiating tactic to build leverage in the talks but also as a real fallback position if the talks fail. The House of Lords could delay the bill by a year, meaning that it may not take effect until end of 2021 – but a trade deal would make it moot. The Northern Ireland Protocol solved the riddle of how to preserve the integrity of the EU’s single market after Brexit yet avoid a return to a hard customs border with the Republic of Ireland. Customs checks were removed with the Good Friday (or Belfast) Agreement in 1998, which ended the Troubles between the two Irelands. The Protocol introduces a pseudo-customs border on the Irish Sea, requiring declarations on exports to Great Britain and EU oversight of UK state aid for Northern Irish firms, so that Northern Ireland can stay in the EU customs area while the UK can leave and still preserve a semblance of its own customs area in Northern Ireland. If the UK and EU get a trade deal, then all trade is tariff-free and the Protocol becomes redundant. Also, the Protocol enables a Joint Committee to review disputes over exports to Northern Ireland that are “at risk” of making their way into the EU without duties. The Protocol is supposed to operate even if the UK and EU fail to get a trade deal. Yet it is politically untenable for the UK to subject trade within its own country to EU rules or duties, or allow the EU to supervise state corporate subsidies across the UK, if no deal is agreed. The UK is more likely to violate the treaty to preserve its internal integrity. As Northern Ireland Secretary Brandon Lewis admitted, “Yes, this [Internal Market Bill] does break international law in a very specific and limited way.” While the EU’s threat to slap tariffs on British food exports to Northern Ireland is the proximate trigger of the Internal Market Bill, another key reason for the UK’s aggressive shift is the issue of state aid. All governments are extending emergency aid to major corporations to keep them from insolvency amid the recession. This will be the case for some time and it is even more true of the EU than of the United Kingdom. However, under the Protocol, the EU would be able to penalize companies in Great Britain that receive subsidies if goods or firms in Northern Ireland can be shown to benefit. Northern Ireland is supposed to operate within the EU’s standards on state aid. London obviously bristles at this backdoor for letting in EU regulation, not least because, in the event that a trade deal is not reached, it will need to pump the country full of state aid to compensate for the shock of seeing exports to the EU rise by 3% across the board according to Most Favored Nation status under the World Trade Organization (Chart 11). An UK-EU trade deal is the most likely outcome. As Dhaval Joshi of BCA’s European Investment Strategy points out, Boris needs to keep his own Tories under his heel (Chart 12). The Internal Market Bill provoked a backlash among 30 moderates. If that number rises to 40 Johnson loses his majority. This is a problem that he is seeking to address by giving parliament a veto over any future uses of the bill that would violate international law (this is an acceptable compromise because he has a majority). But a failure to drive a hard bargain with the EU would cause a much bigger rebellion among hard Brexit Conservative MPs and threaten his job. Chart 12Bojo Must Balance Hard Brexit Tories

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

Geopolitics is about might, not right – the UK can assert its sovereignty and violate these international agreements, while the EU can then apply punitive tariffs, non-tariff barriers, and sanctions under the Withdrawal Agreement. Brexit is a power-political struggle that could devolve into a trade war. Obviously that would be a very bad outcome for the market, particularly for the UK, which is overmatched (Chart 13). But this risk is also a key limitation on the UK that will prevent this worst-case outcome. Indeed, despite all of the above, our base case is still that the UK and EU will get a deal. First, the economy will clearly suffer without a deal. After all, the US-China tariffs produced a negative effect for these two economies in 2019 and the impact on the UK would be bigger than that on the US (Chart 14). Chart 13The Brick Wall The UK Cannot Avoid

The Brick Wall The UK Cannot Avoid

The Brick Wall The UK Cannot Avoid

Chart 14UK Faces Trade Shock If No Deal

UK Faces Trade Shock If No Deal

UK Faces Trade Shock If No Deal

Second, the public doesn’t support a no-deal exit (Chart 15). Northern Ireland itself voted against Brexit in the referendum and as such would rather see an agreement that groups the UK and the EU under a single zero-tariff free trade agreement. Third, Boris faces a rebellion in Scotland if he pursues a hard break. The Scottish National Party would revive ahead of Scottish elections in May 2021 and demand a second independence referendum (Chart 16). The Irish Sea is a natural division that makes a more intrusive customs presence more supportable than otherwise. A little more paperwork is an acceptable cost to keep the United Kingdom from falling apart. Scotland is much more likely to go independent than Ireland is to unite. Chart 15Only 25% Think 'No Deal' A Good Outcome

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

Boris is now prime minister, not just party leader, and he will ultimately have to decide whether he wants to be the last prime minister of a United Kingdom. Assuming Boris is at least focused on the next election, he will have to decide if he wants the rest of his premiership to be consumed with a self-inflicted double-dip recession and democratic revolt in Scotland, or a recovery on the back of a functional if uninspiring trade deal enabling him to head off the Scottish threat and save the union. Chart 16No Deal' Would Boost Scottish Independence Movement

No Deal' Would Boost Scottish Independence Movement

No Deal' Would Boost Scottish Independence Movement

Obviously the final deal may not be clinched until the eleventh hour. The October 15 deadline can be delayed but talks must conclude in November or December in time to be ratified by the EU member states by December 31. US Election Drives Geopolitics, But Not The Brexit Outcome One factor that will not play much of a role in the UK’s decision-making is the US election. It is true that the Johnson government would benefit from President Trump’s reelection. But the EU is a much bigger market for the UK and the UK’s best strategy is to focus on its national interest regardless of what the US does. The US election may not be decided in mid-December in time for the UK to agree to a deal that can be ratified by year’s end anyway. Moreover the UK’s best strategy is to conclude a deal with the EU first, and then pursue a deal with the United States. This is because President Trump will be inclined to sign at least an executive deal, while a congressional deal requires support from the Democrats, which is only possible if Northern Ireland is resolved without hard border checks. Because the EU makes up such a larger share of British trade, an American deal does not give the UK much leverage in negotiating with the EU, but an EU deal does give the UK greater leverage in negotiating with the US. As Diagrams 1 and 2 show, this strategic logic holds even if the UK knows the outcome of the US election ahead of time: the scenarios with the least benefit and the greatest cost would still be scenarios involving no deal with the European Union. Diagrams 1 & 2United Kingdom Wants An EU Trade Deal (Regardless Of Trump/Biden)

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

Diagram 3 boils all of this down to a single decision tree. First, the diagram shows that the economic costs are not prohibitive and therefore the risk of a no-deal exit is substantial – we would say 35%. Second, it shows that the risks of the negotiation are skewed to the downside. Third, it highlights that the UK will settle its affairs directly with the EU and not hinge its actions on the US election cycle. Diagram 3No-Deal Brexit Cost Not Prohibitive, But Best Strategy Is To Get A Deal

The End-Game For Trump And Brexit

The End-Game For Trump And Brexit

Clearly the best strategy and best outcome involve seeking a trade deal with the EU, and hence it is our base case. This means an opportunity to buy the pound and domestic-oriented British equities, and turn neutral on gilts, is just around the corner. Investment Takeaways The GBP-EUR is the best measure of the market’s sensitivity to Brexit risks, so it should fall in the near term and rally sharply after resolution. However, the US election complicates things. The euro’s response is fairly binary: it is one of the biggest winners if Biden wins and one of the biggest losers if Trump wins. Hence GBP-EUR volatility will rise in the coming months (Chart 17). We recommend going long 1-month implied volatility contracts for October and November. The pound sterling, by contrast, will ultimately rise regardless of US election result, since the UK will pursue a trade deal out of its own national interest. Trump is less negative for the US dollar than Biden and a comeback and victory will drive a counter-trend dollar bounce. However, in the medium term we expect the dollar to fall regardless due to debt monetization and global growth recovery. Thus we recommend going long GBP-USD on a strategic basis when political risks peak over the next two-to-three months and GBP-USD falls to around 1.25, as recommended by our Foreign Exchange Strategist Chester Ntonifor (Chart 18). Chart 17EUR-GBP Volatility Will Rise

EUR-GBP Volatility Will Rise

EUR-GBP Volatility Will Rise

Sterling bears are forgetting that the sound defeat of Corbyn ruled out a sharp left-wing turn in domestic economic policy (higher taxes), while the Tories have made a clear turn against fiscal austerity. Therefore the worst-case scenario is a failure to agree to a trade deal by the end of this year. But that is not the base case and the risk will be priced within a month or two. Chart 18Pound Will Rally After Deal Concluded In November Or December

Pound Will Rally After Deal Concluded In November Or December

Pound Will Rally After Deal Concluded In November Or December

Chart 19Yes, China Is Opening The Taps

Yes, China Is Opening The Taps

Yes, China Is Opening The Taps

We remain tactically cautious and defensive even though the US fiscal negotiations are improving. The market is underrating too many clear and concrete risks to sentiment and the corporate earnings outlook, so the current bout of volatility can continue until there is greater clarity on US fiscal spending, the US election cycle, associated geopolitical risks, and the Brexit showdown. Book gains on long Brent trade for a return of 69.7%. We initiated this trade on March 27 in our “No Depression” report, which marked our shift to a strategic risk-on positioning. We remain bullish on oil prices and commodities on the back of global stimulus and our assessment that the OPEC 3.0 cartel will maintain discipline overall, but the next three-to-six months are crowded with downside risk. Cyclically, we see a global economic recovery deepening and broadening. China’s stimulus is surprising to the upside, as we have long written and the latest credit numbers bear this view out (Chart 19), which is critical for global reflation. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com

Highlights If it can maintain production discipline over the next 2-3 years, OPEC 2.0 will be the oil market’s most important determinant of price levels for years. The massive increase in OPEC 2.0 spare capacity resulting from COVID-19-induced demand destruction, along with its low-cost production, global storage and distribution will allow it to bring crude to market quicker than US shale-oil producers, and to manage an orderly drawdown in global inventories, which remains its raison d'être. As spare capacity is drawn down over the next couple of years, Brent and WTI forward curves will backwardate in in 1H21, as spare capacity and the slope of the forward curve are inversely related (lower spare capacity leads to higher backwardation). This will keep spot prices realized by OPEC 2.0 states above the deferred prices at which shale producers hedge (Chart of the Week). Parsimonious capital markets will continue to deny funding to all but the most profitable producers, which will continue to limit E+P ex-OPEC 2.0. ESG-focused investments will increasingly favor energy producers outside the oil and gas sector. As demand growth resumes, this will sow the seeds for higher oil prices in the mid-2020s. We will be updating our oil balances and 2H20 and 2021 forecasts – $46/bbl and $65/bbl for Brent in 2H20 and 2021 – next week. Feature While the hit to oil producers’ revenues from the demand destruction caused by the COVID-19 pandemic has been severe – particularly for those states comprising OPEC 2.0, which are so heavily dependent on oil exports – it set the stage for the producer coalition to take control of global oil-price dynamics for the next couple of years. If the OPEC 2.0 coalition can maintain its production discipline, its member states could extend this control for years into the future, just as they are attempting to diversify their economies from this dependence on hydrocarbons. Once OPEC 2.0 member states manage to diversify a large part of their economies, the next optimal strategy will be to monetize their reserves and market share. Until then, it is our contention it is in these states' interest to have higher prices via gaining control of supply. The producer coalition led by the Kingdom of Saudi Arabia (KSA) and Russia today sits on some 7mm b/d of spare capacity that is a direct result of the global collapse in demand. This gives it a powerful lever to restrain the recovery of production growth in the US shales and elsewhere. Spare Capacity Turns The Tables On Shale Oil The enormous spare capacity now held by OPEC 2.0 – the majority of which is in KSA – allows the coalition to turn the tables on the US shales and producers ex-US Since its inception in late 2016, OPEC 2.0 has accommodated higher US shale production by reducing its output and then expanding it at a slower rate, as US production soared to meet domestic demand and, increasingly, global oil demand (Chart 2). OPEC 2.0 has been in operation since January 2017. Over that period, the coalition reduced its output growth ~ 0.37% for every 1% increase in crude and liquids output ex-OPEC 2.0. Within that adjustment, OPEC 2.0’s output falls by 0.16% for every 1% increase in US output, most of which was accounted for by the unprecedented growth of shale production.1 The enormous spare capacity now held by OPEC 2.0 – the majority of which is in KSA – allows the coalition to turn the tables on the US shales and producers ex-US (Chart 3). Chart of the WeekFalling OPEC 2.0 Spare Capacity Will Backwardate Brent Forward Curves

Falling OPEC 2.0 Spare Capacity Will Backwardate Brent Forward Curves

Falling OPEC 2.0 Spare Capacity Will Backwardate Brent Forward Curves

Chart 2OPEC 2.0 Accommodated US Shales

OPEC 2.0 Accommodated US Shales

OPEC 2.0 Accommodated US Shales

Chart 3OPEC 2.0 Would Benefit From Maintaining Spare Capacity At High Levels

OPEC 2.0 Would Benefit From Maintaining Spare Capacity At High Levels

OPEC 2.0 Would Benefit From Maintaining Spare Capacity At High Levels