Valuations

We close our overweights to Energy and Aerospace & Defense. The macroeconomic backdrop is deteriorating for Energy. As for A&D, the good news is already priced in.

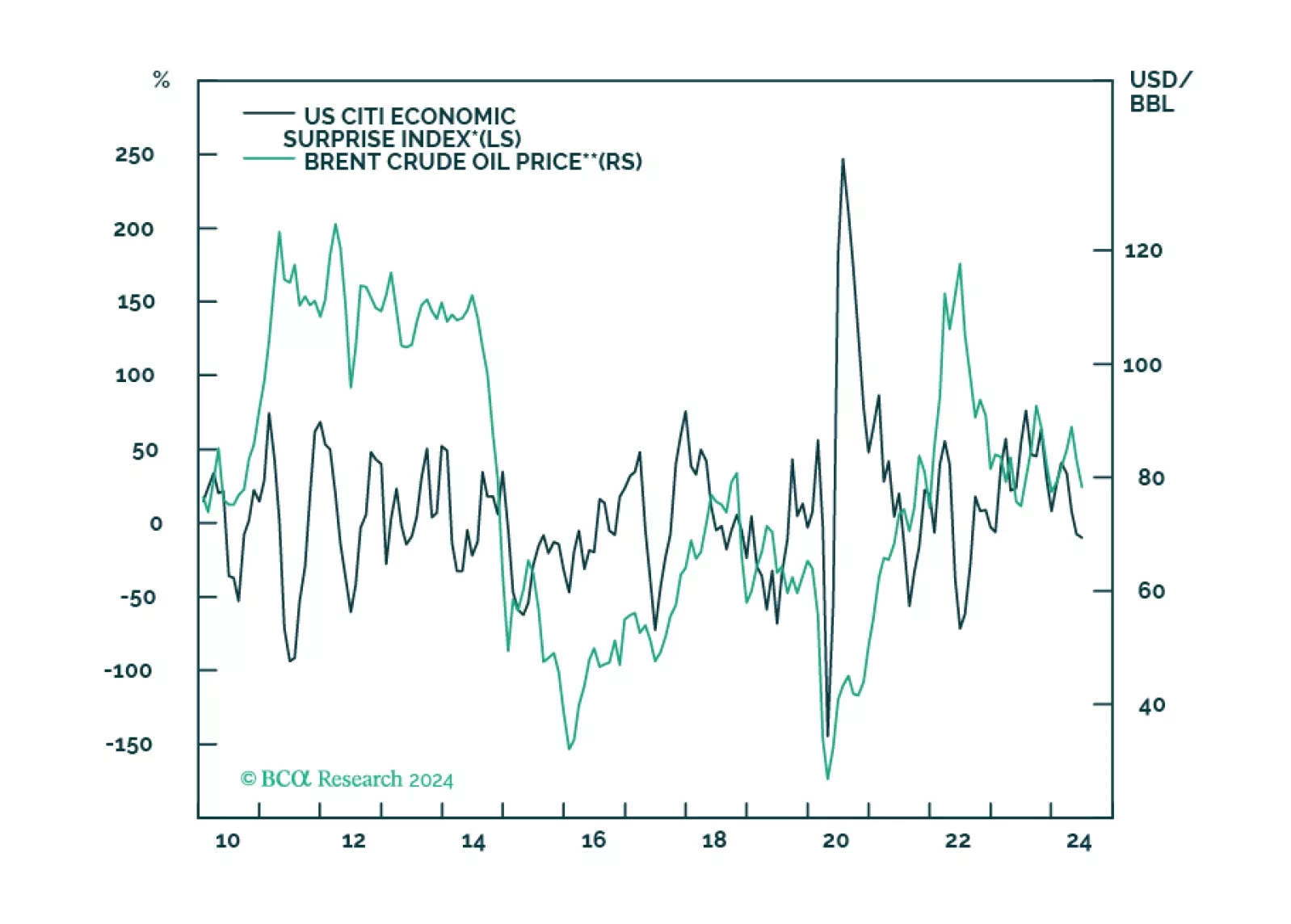

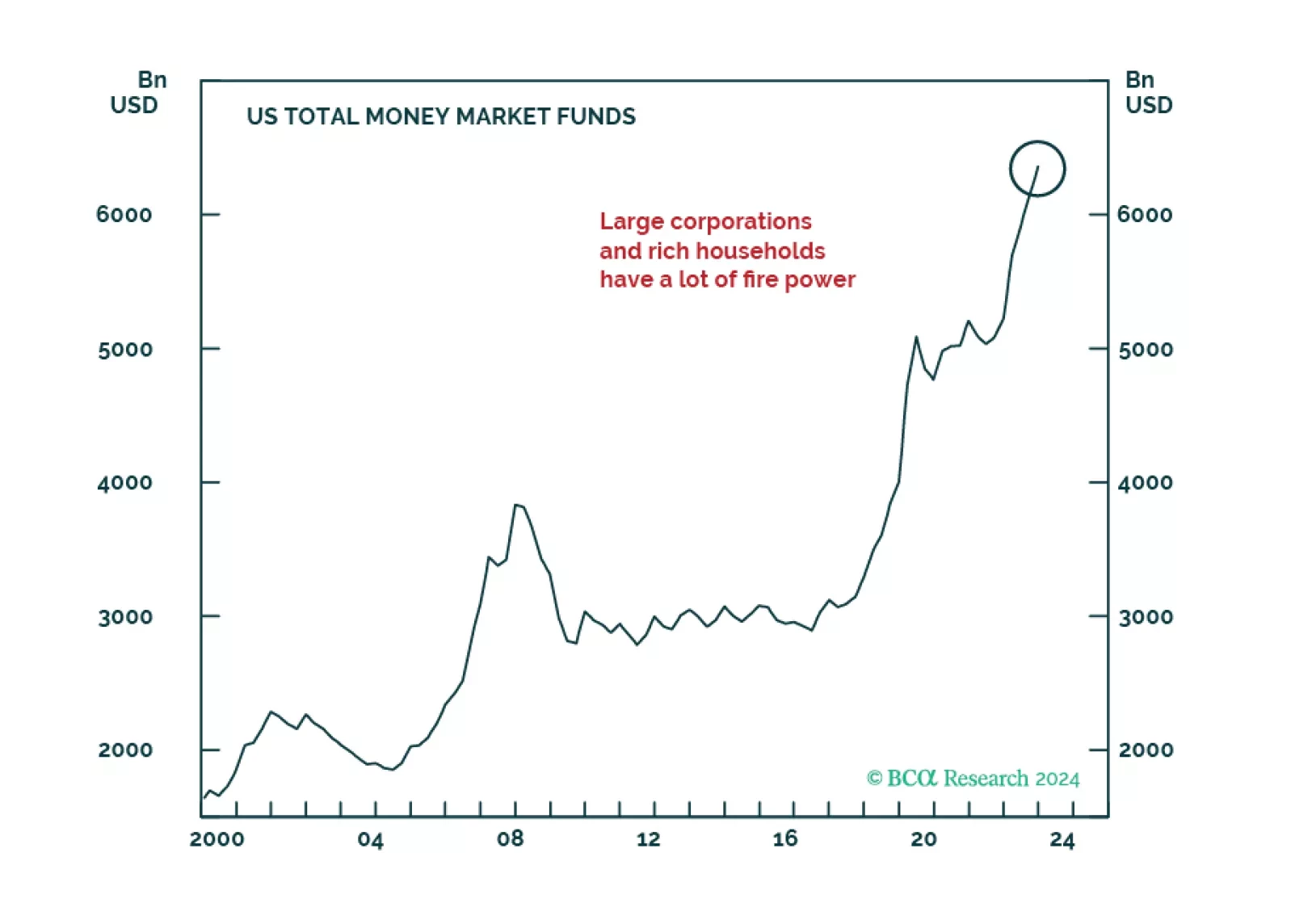

Generative AI-related rally resumed in May. Much of the recent market gains are down to excess liquidity that was begotten by the massive pandemic stimulus, creating a dichotomy between multiple economic challenges and exuberant markets. The Fed is unlikely to step in to prevent the bubble as it is currently more worried about the near-term downside for growth than financial stability.

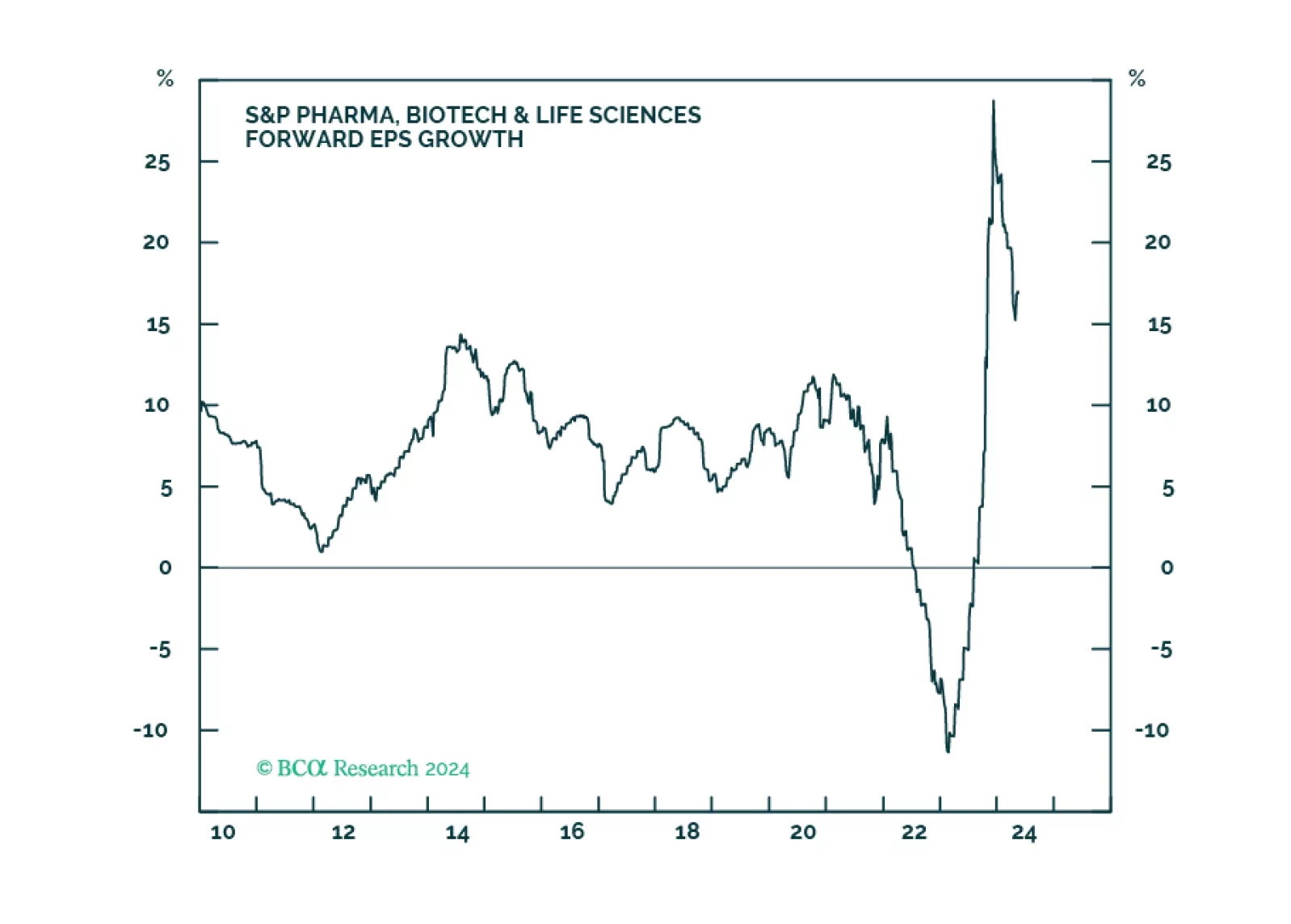

We recommend overweight in Pharma over a tactical and strategic investment horizon, as challenges, that have recently hampered the industry group’s performance, are dissipating. Likely election outcomes are positive for the industry, while major trends like generative AI applied to drug development and an aging population are long-term tailwinds.

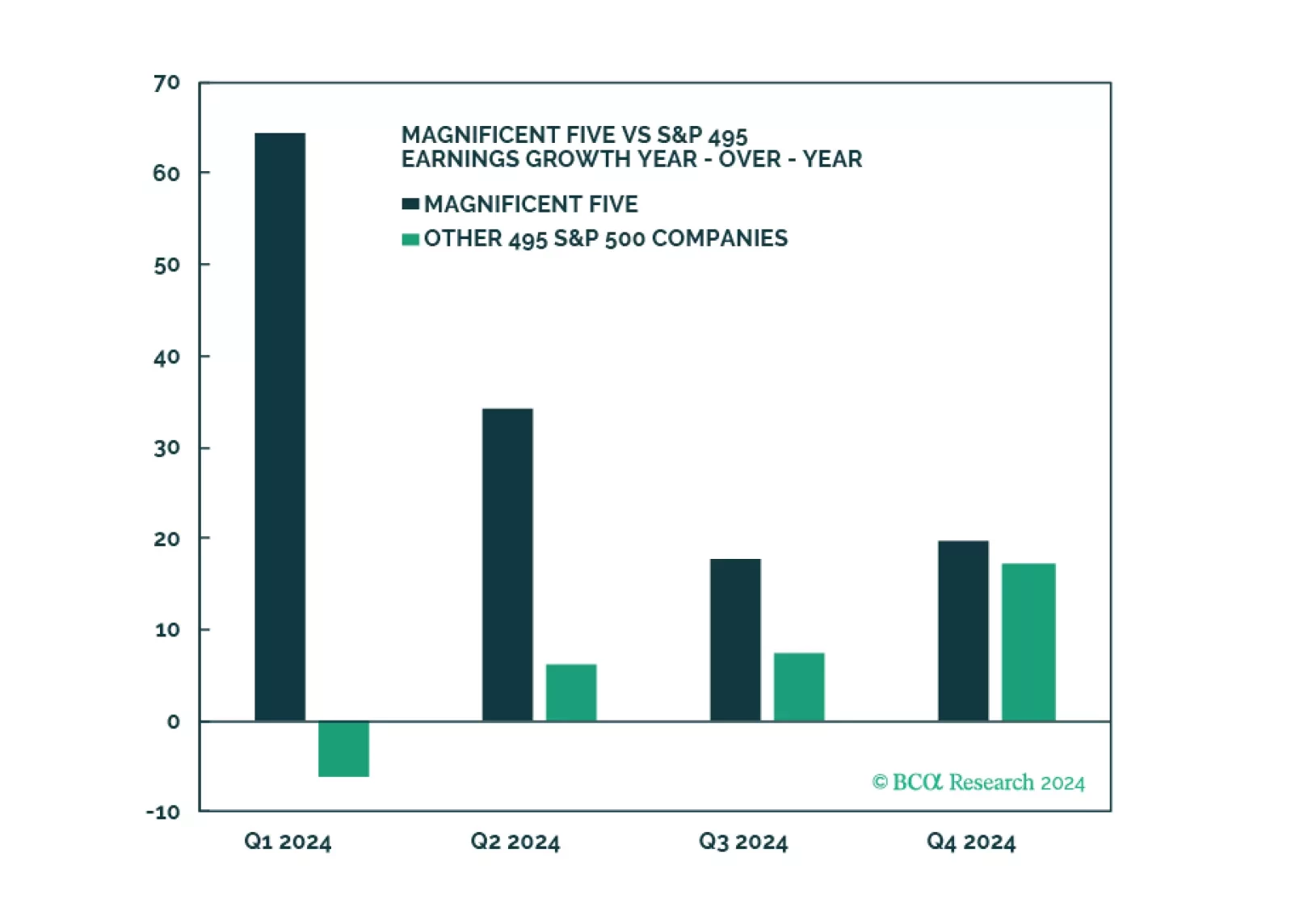

Q1 Earnings and sales growth were strong, but the devil is in the details: Without the Magnificent Five, earnings growth for the index would have been negative. On a positive note, margins have stabilized, and earnings growth is expected to broaden into yearend. Companies are optimistic about the economy. Development of AI applications is in full swing, but few companies are monetizing them yet. Consumer spending is strong but is slowing. We reiterate our underweight of consumer sectors, and overweight of Software and Services as the “don’t fight AI” adage holds.

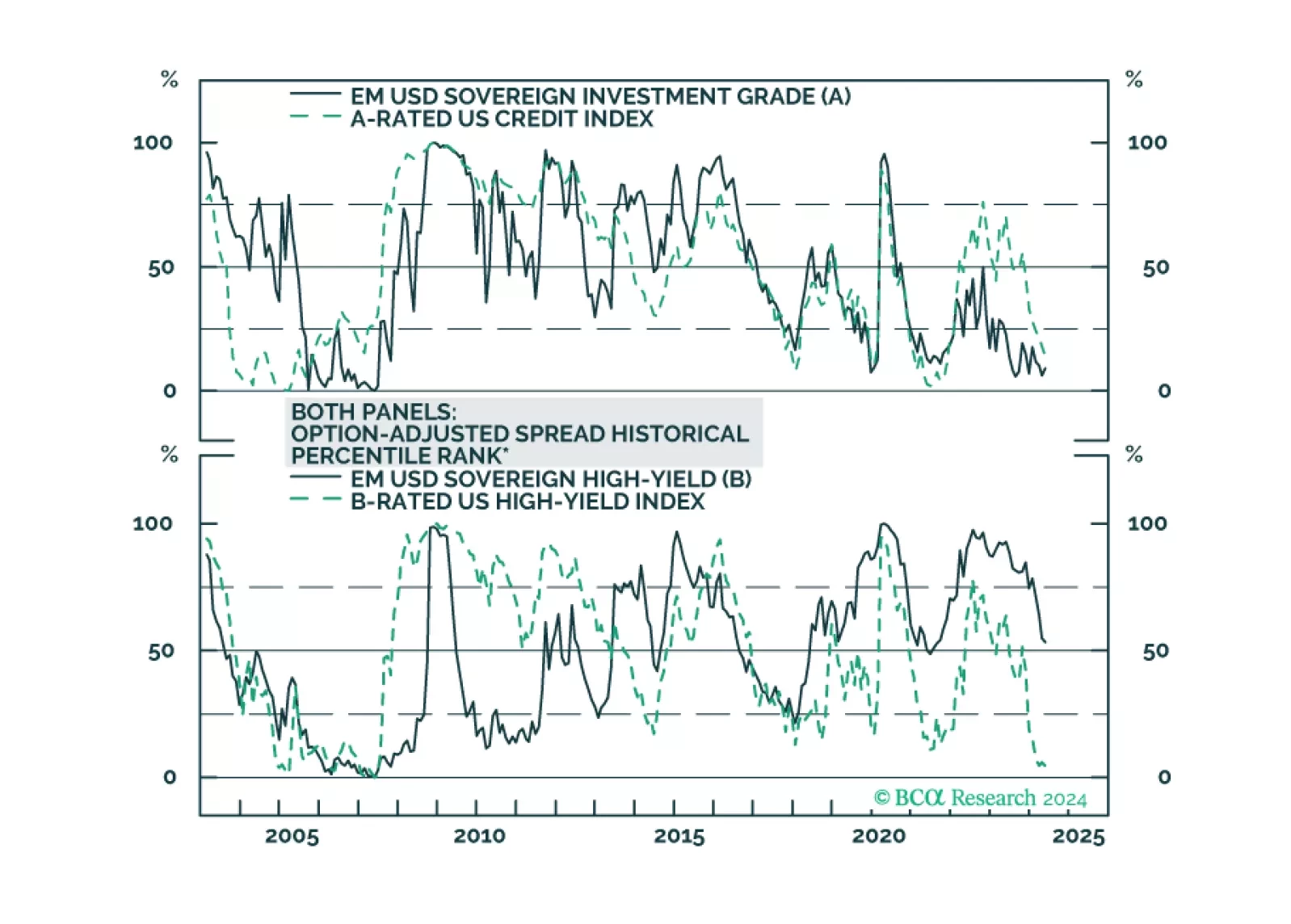

We dig into the USD-denominated Emerging Market Sovereign Index to see which credit tiers and countries offer value relative to US Credit.

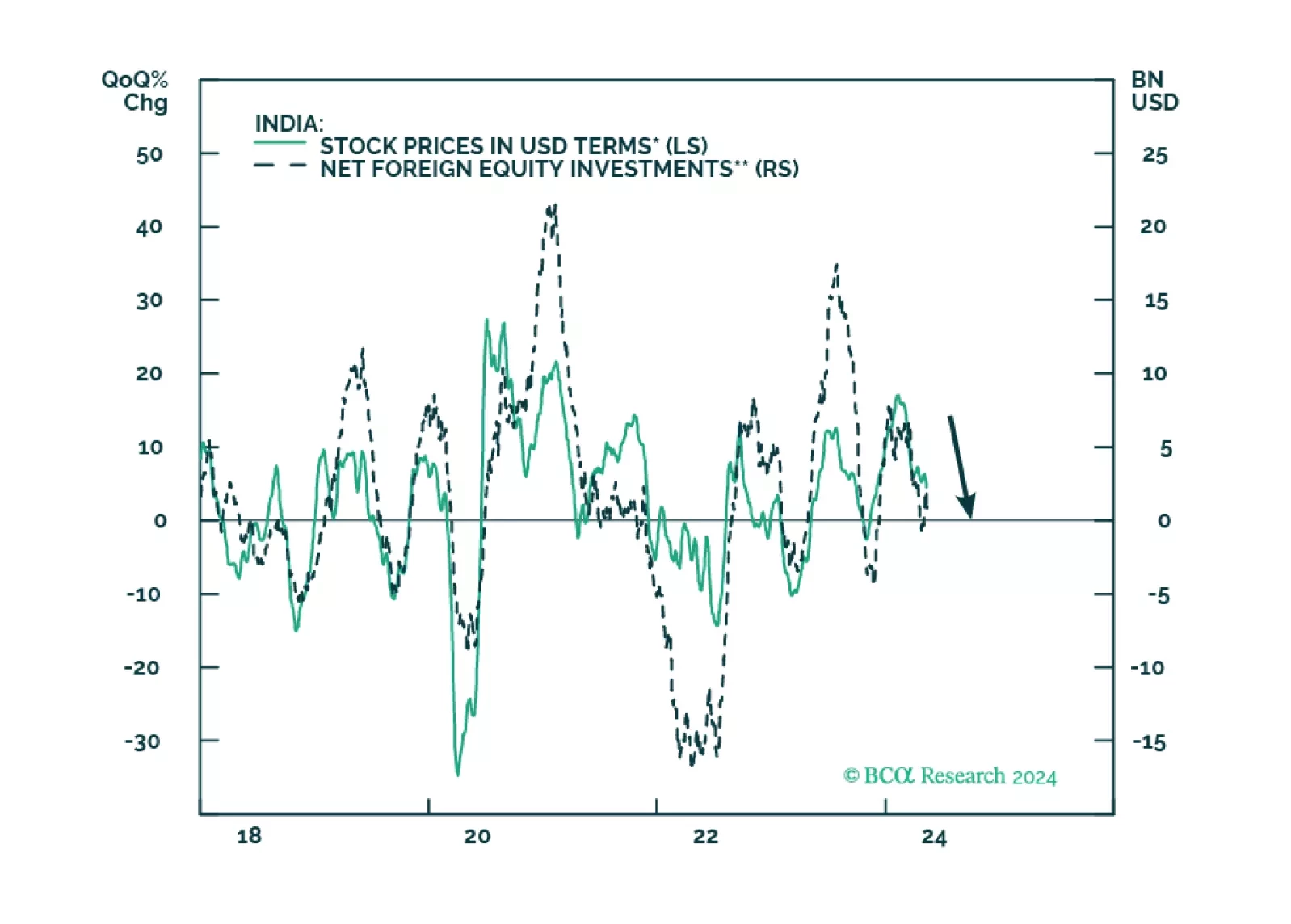

Modi and the BJP are at or near the peak of their political dominance, and their third term will be challenging as they must deal with harder reforms amidst a slowing domestic and global economic environment. In the long run, however, we remain constructive on India’s prospects, as its geopolitical and economic positioning are favorable and improving.