War/Conflict

Simple games allow us to model several of the Trump administration’s most disruptive policies in 2025. We find that markets face an increase in volatility as Congress expands the budget, Trump implements tariffs on the world, China retaliates, and Taiwan tensions persist. A ceasefire in Ukraine is a marginally positive outcome for Europe, although it is not a long-term peace treaty.

In this Special Report, BCA’s Chief Geopolitical/US Political Strategist Matt Gertken discusses the top five “Black Swan” risks for 2025, from Trump to China.

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.

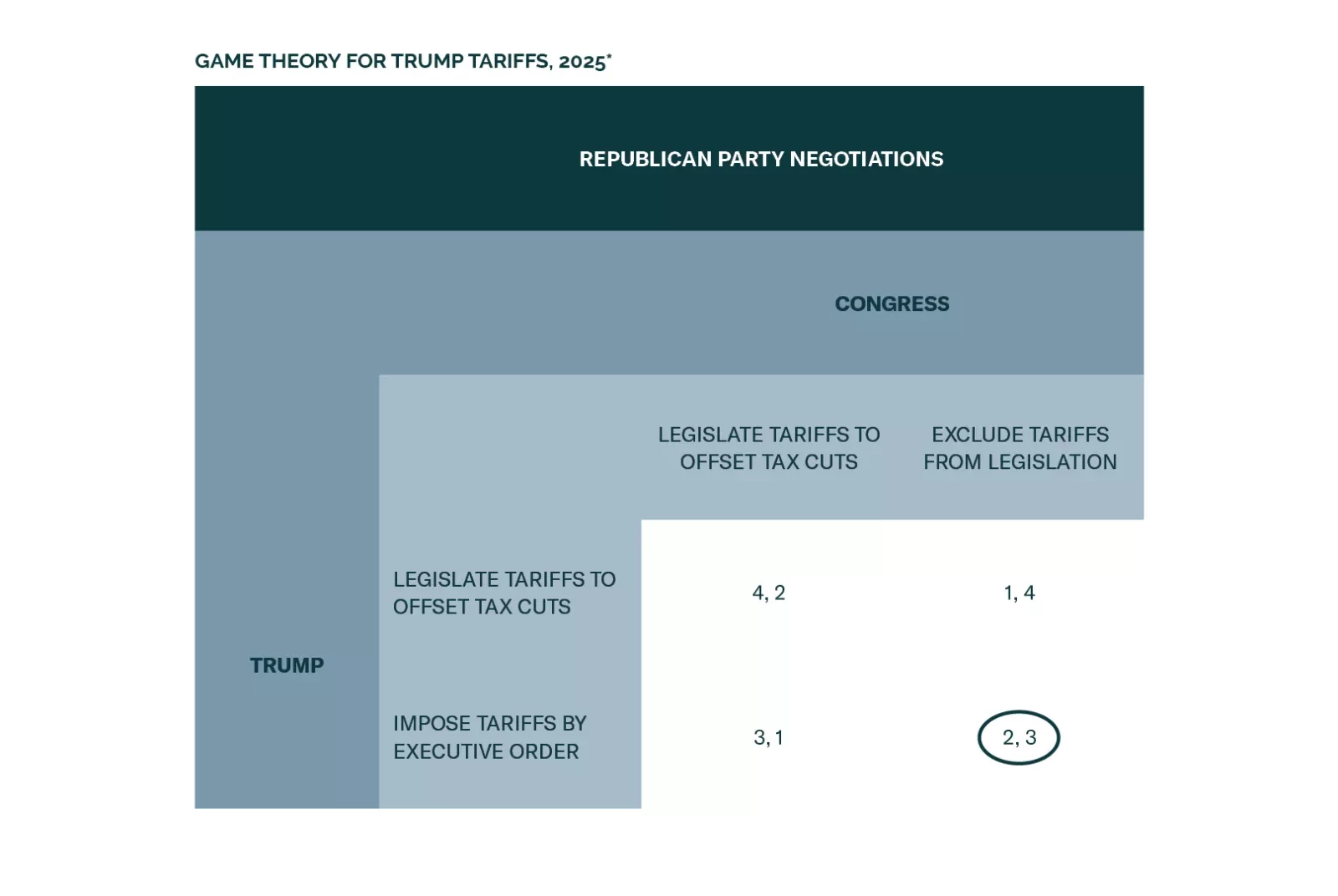

- Congress will pass tax cuts by end of 2025 producing a fiscal thrust of about 0.9% of GDP in 2026.

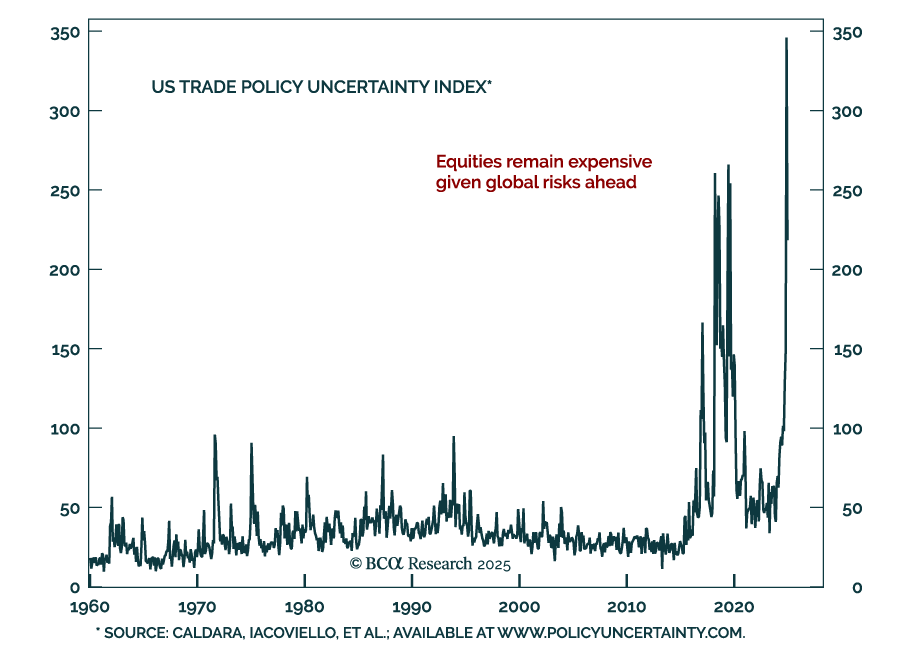

- Trump will count on that stimulus as a basis for slapping tariffs on leading trade partners.

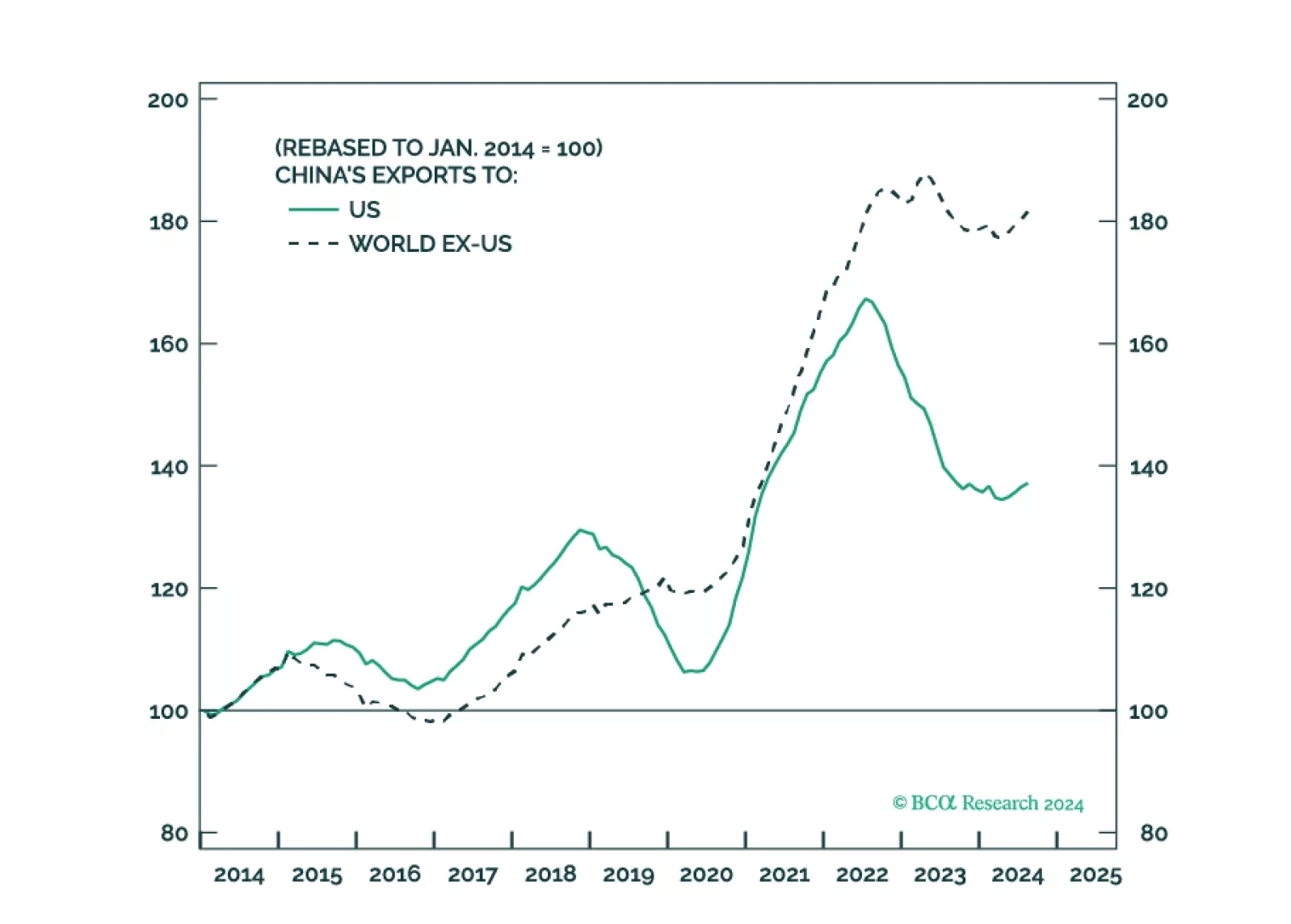

- China will retaliate against Trump and stimulate its domestic economy, while pursuing stronger trade ties with other countries. Europe will also retaliate.

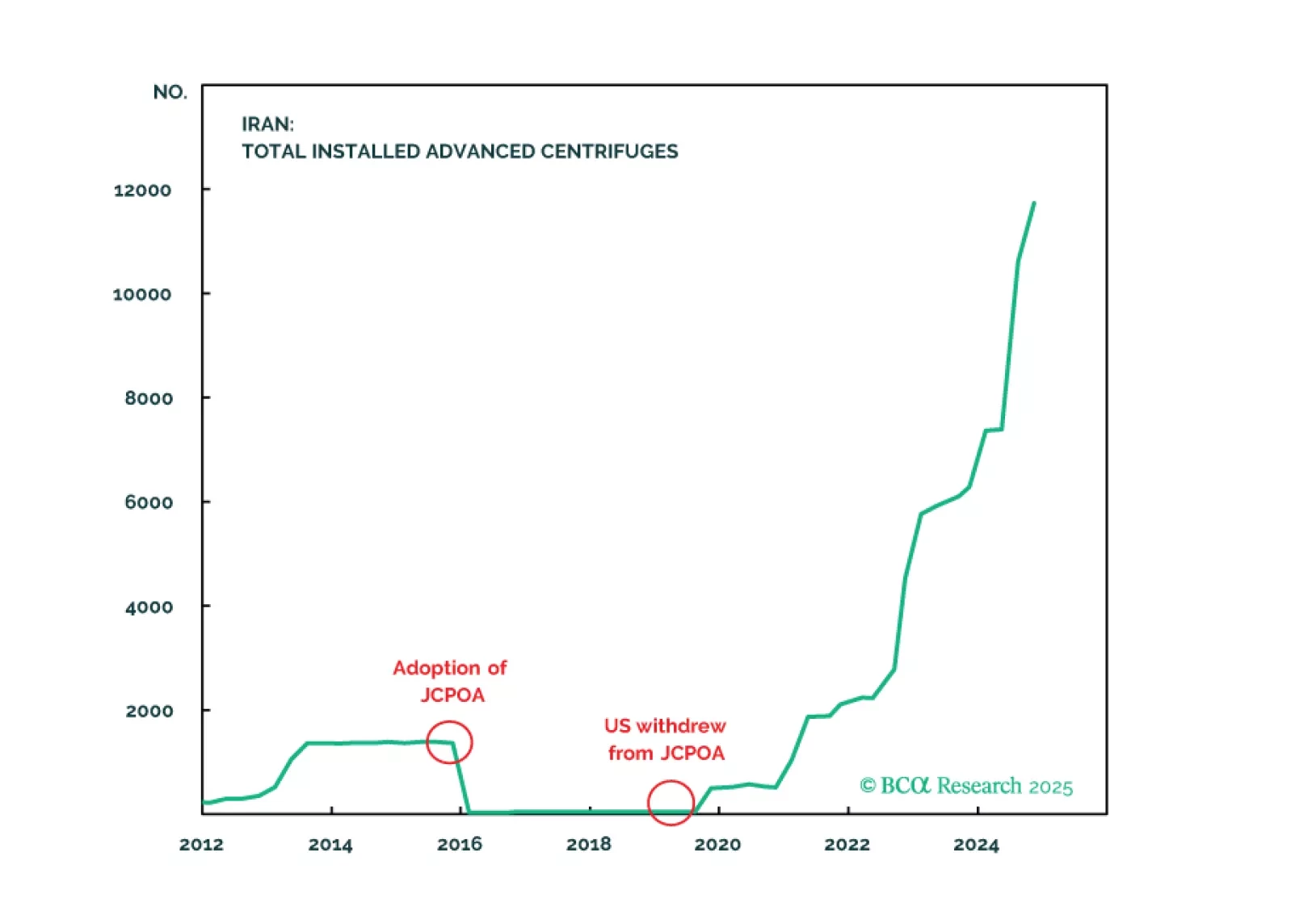

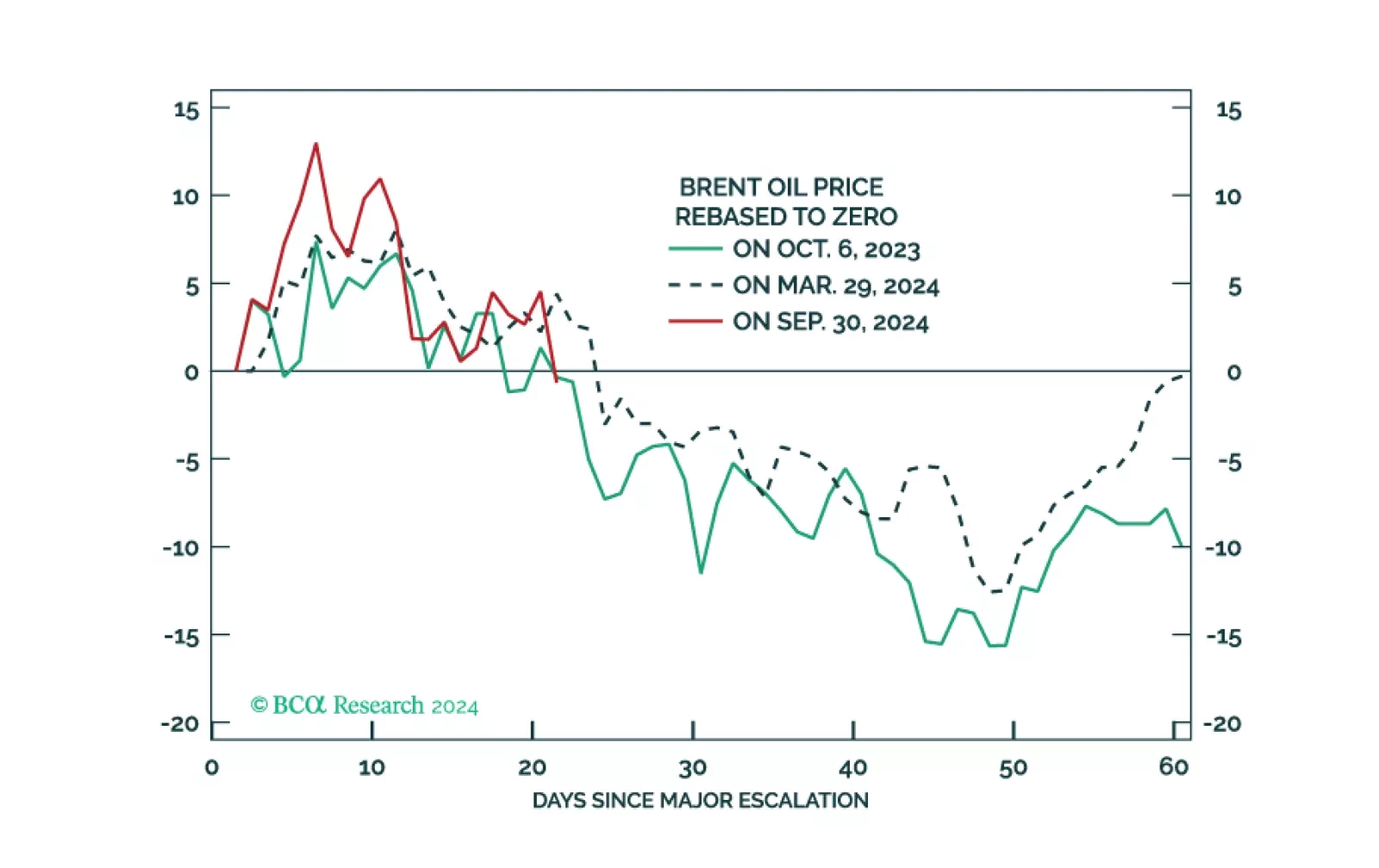

- Geopolitical risk will shift from Ukraine-Russia to Israel-Iran, where the conflict will continue to escalate until a crisis point is reached within 2025.

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

In this Special Report, Marko Papic, Chief Strategist of BCA Research’s GeoMacro Strategy, and Mathieu Savary, Chief Strategist of BCA Research’s European Investment Strategy, together argue that the conflict in Ukraine is already frozen, already losing support in the West, and is likely to taper off over the course of 2025. However, there is no easy alpha left to harvest from that conclusion, the market has already moved on. Some long-term investment opportunities remain in broad European assets.