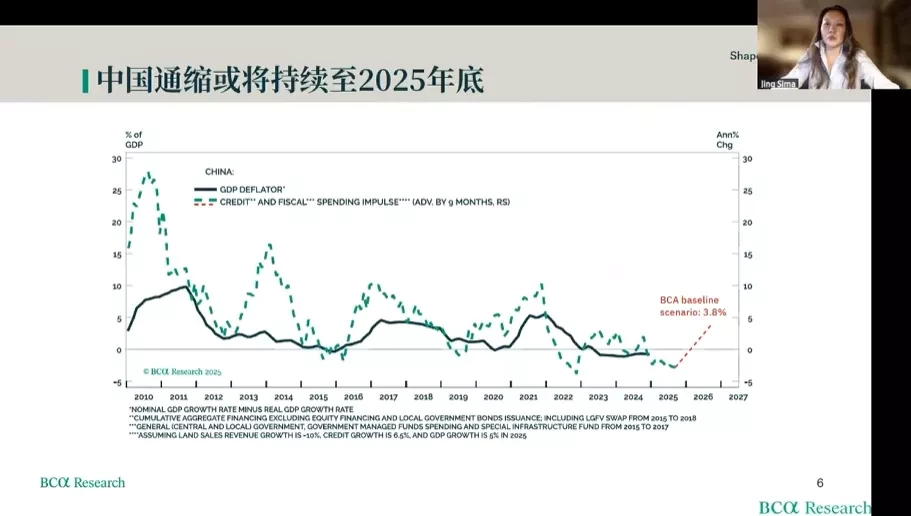

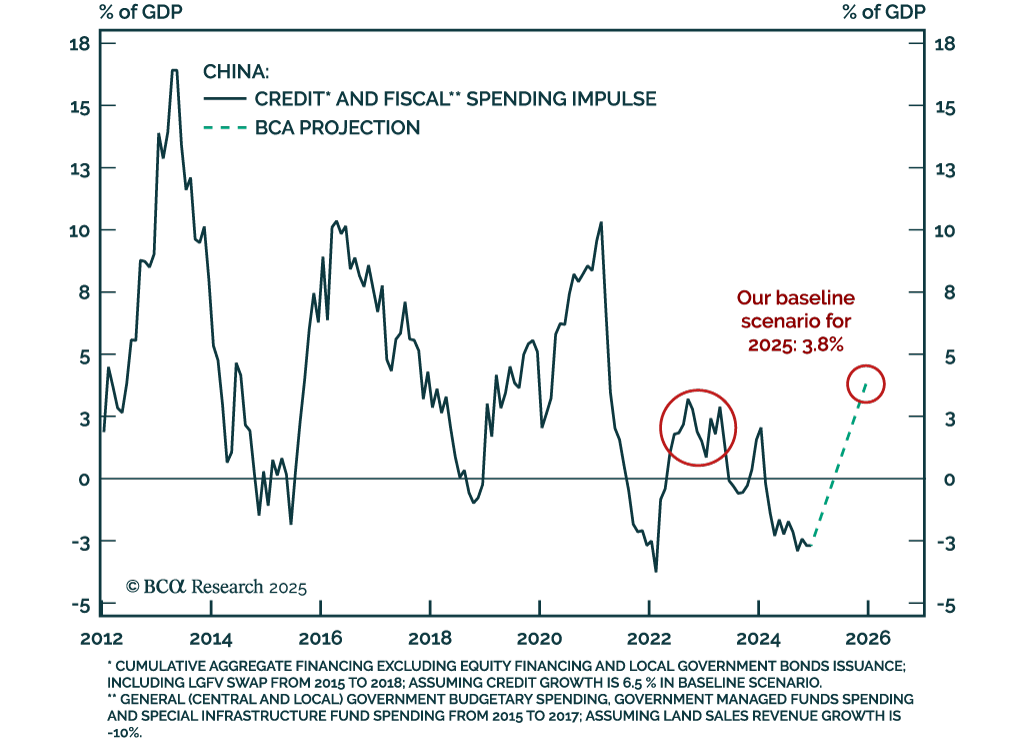

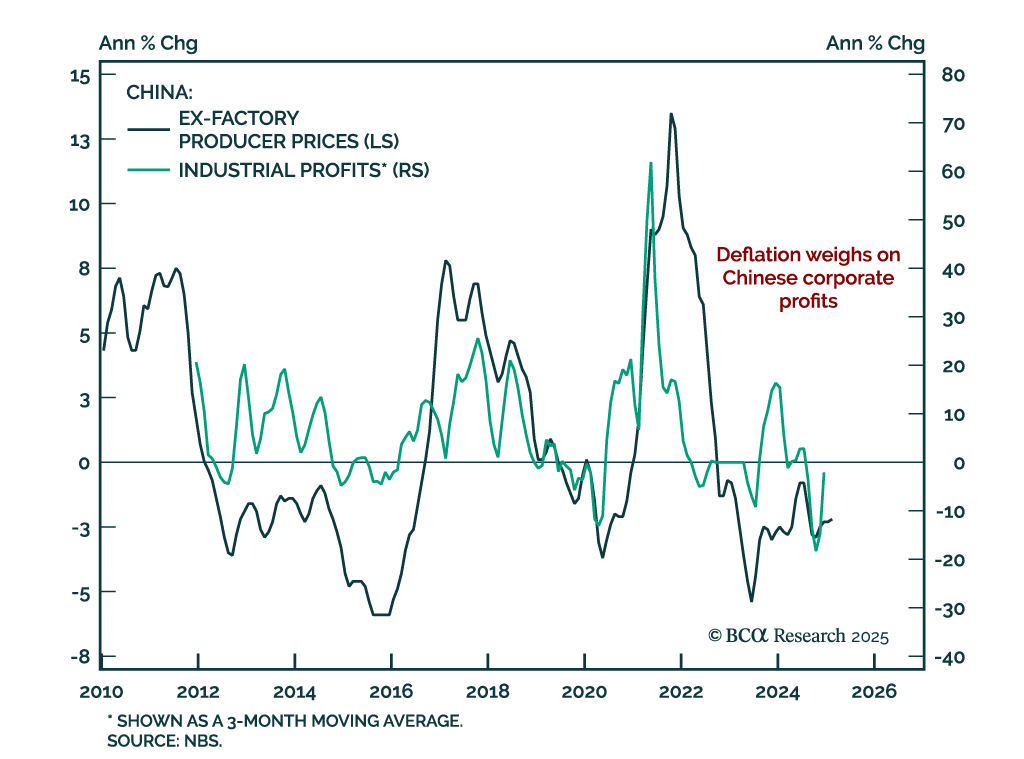

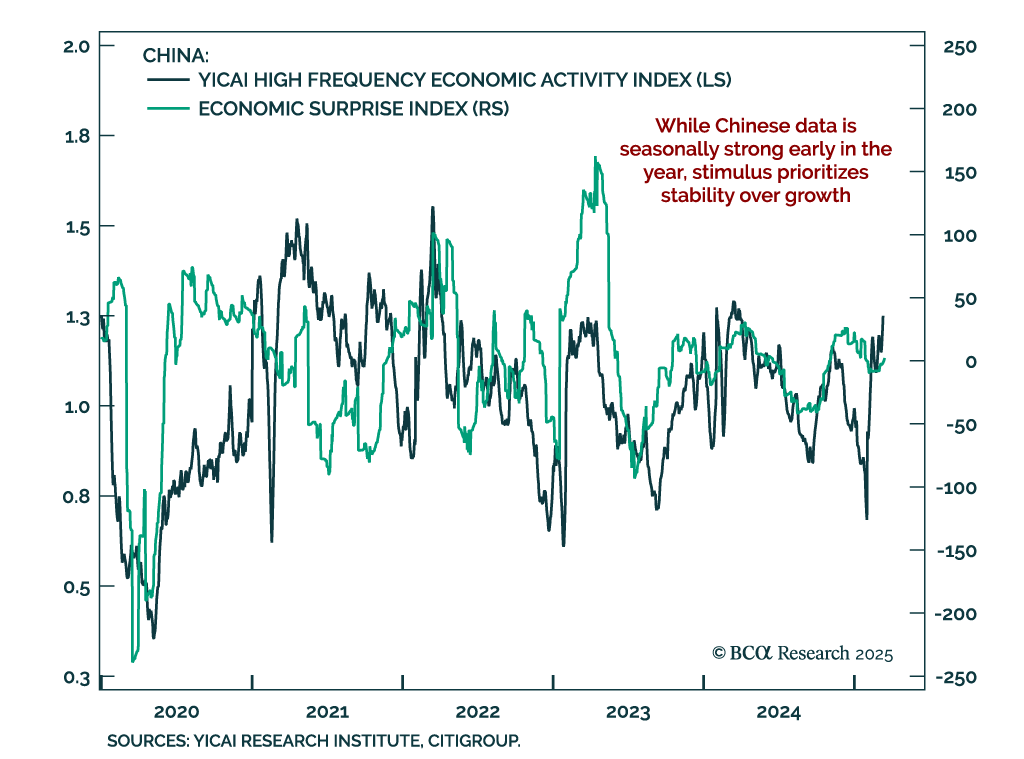

China

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

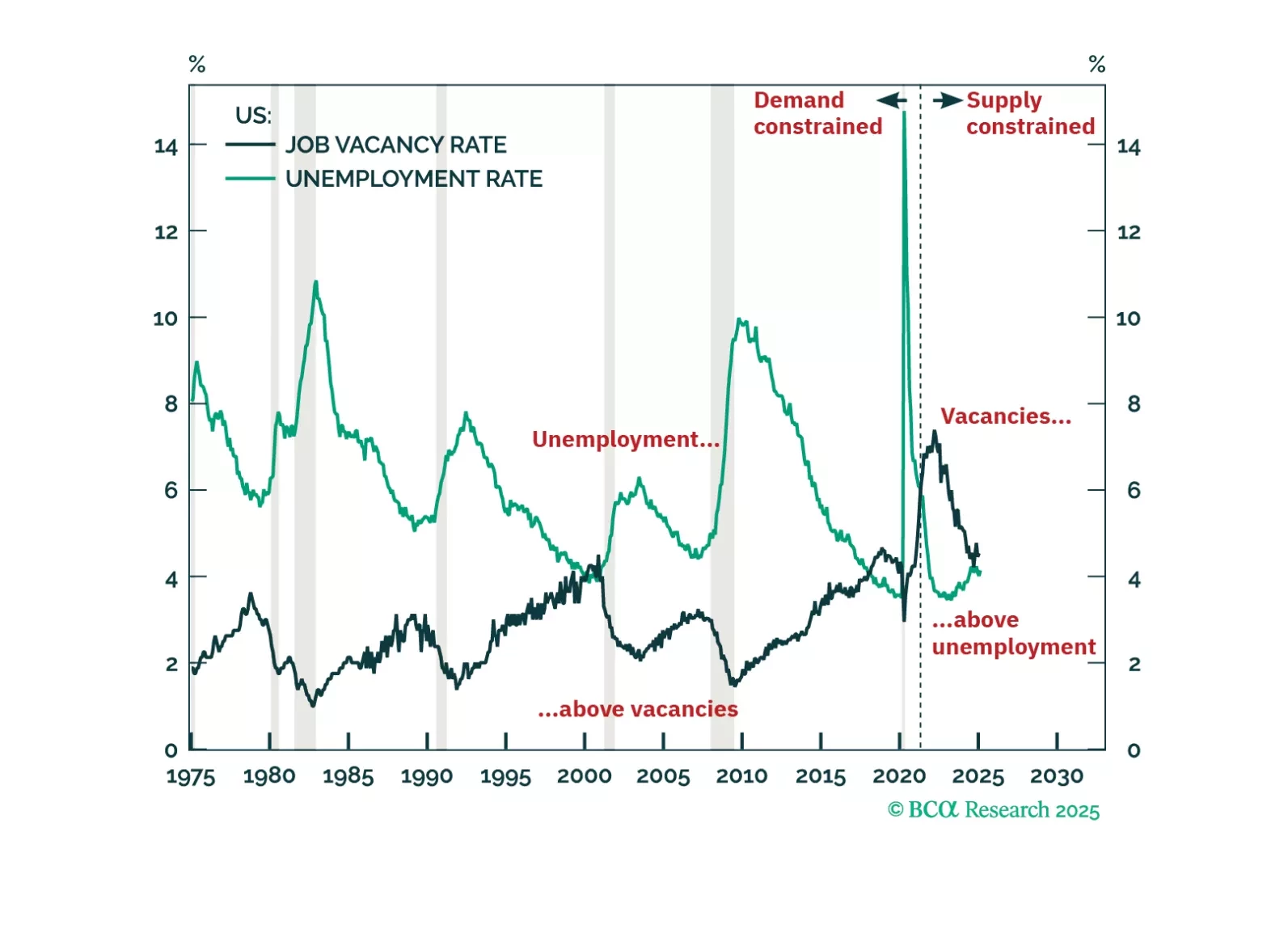

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.

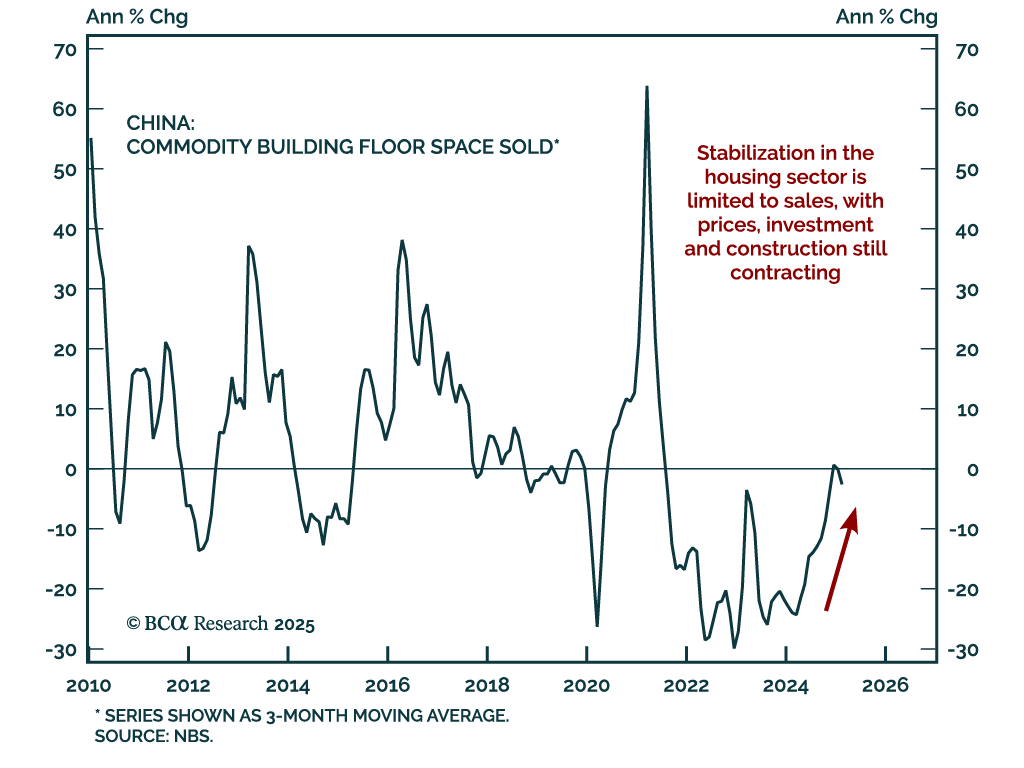

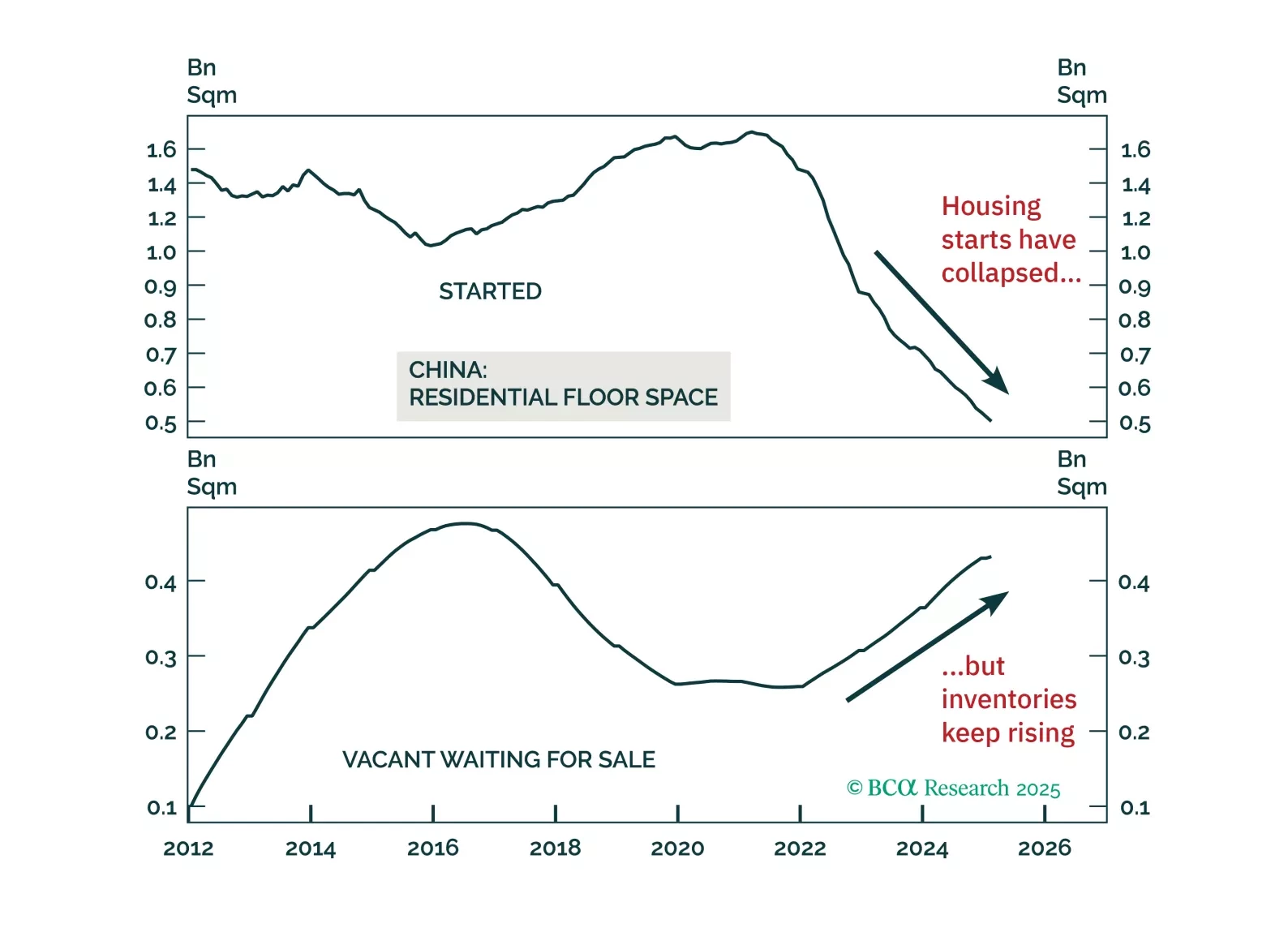

Data released this Monday suggests that while China’s housing market is no longer worsening, the secular adjustment remains ongoing. Although aggregate housing demand may be stabilizing at a low level, supply will continue to significantly outpace demand, indicating that home price deflation will persist. Additionally, property developers’ poor financing will hinder new project initiations, leading to a further decline in housing starts over the next six to 12 months.

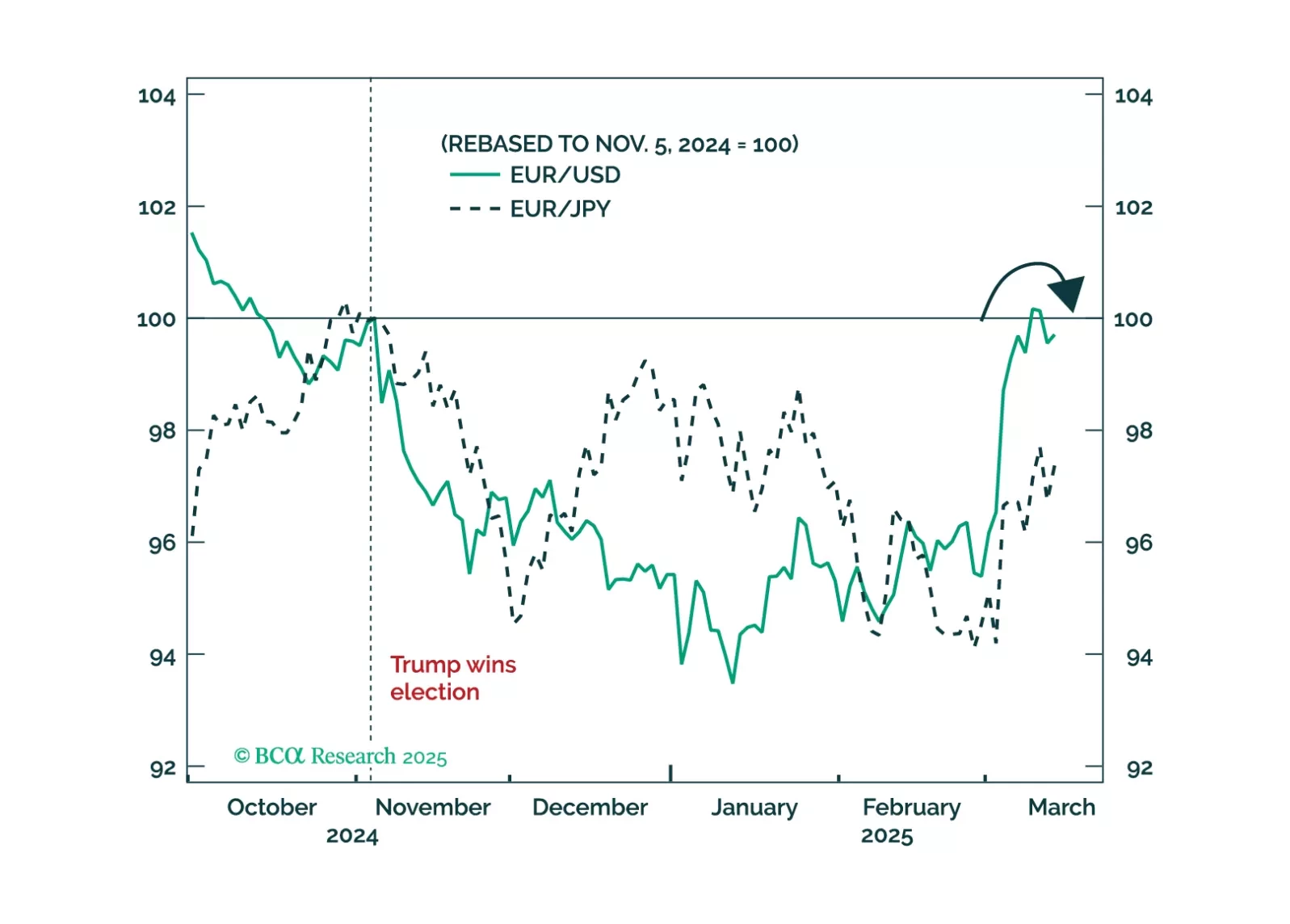

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.