China

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.

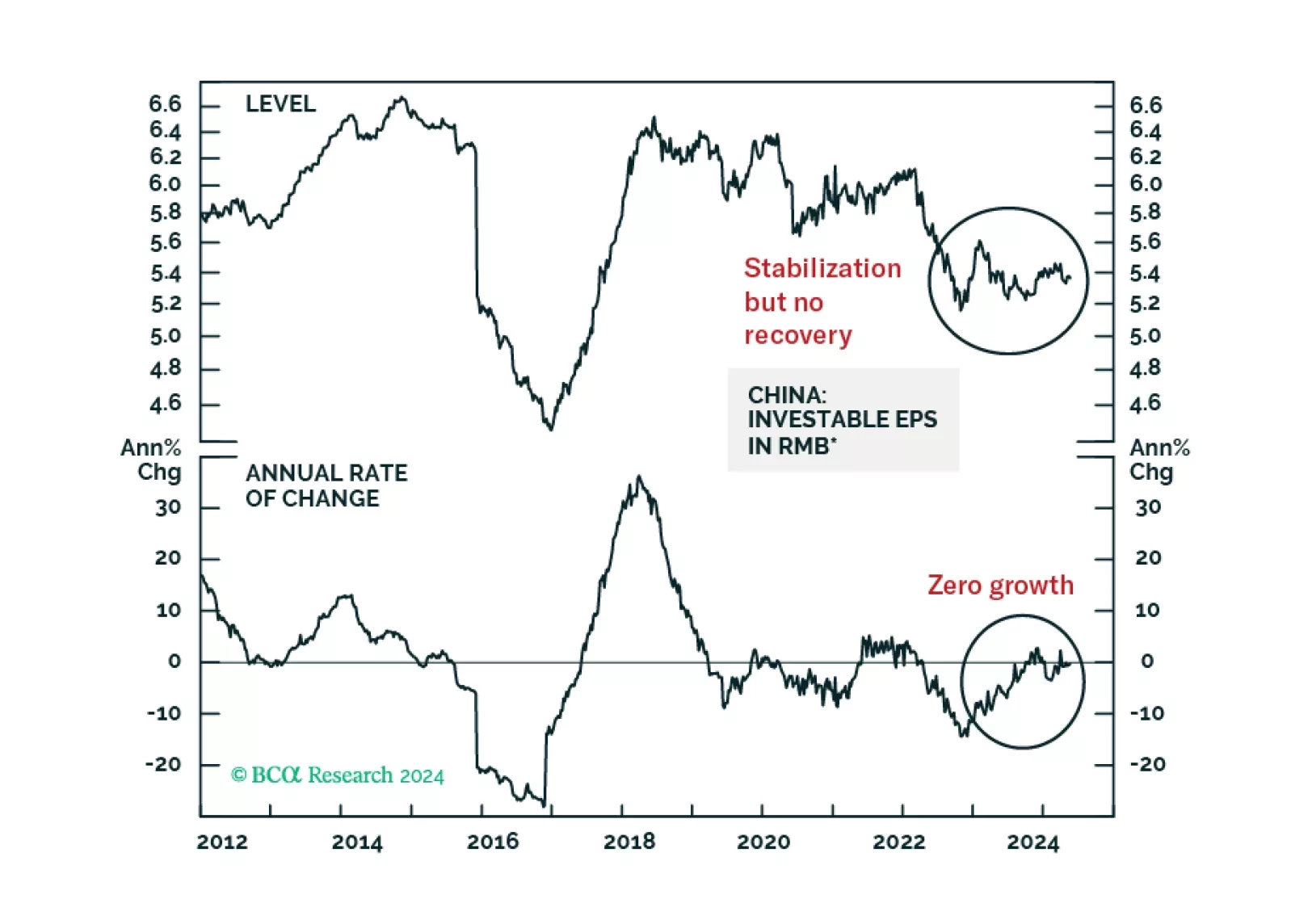

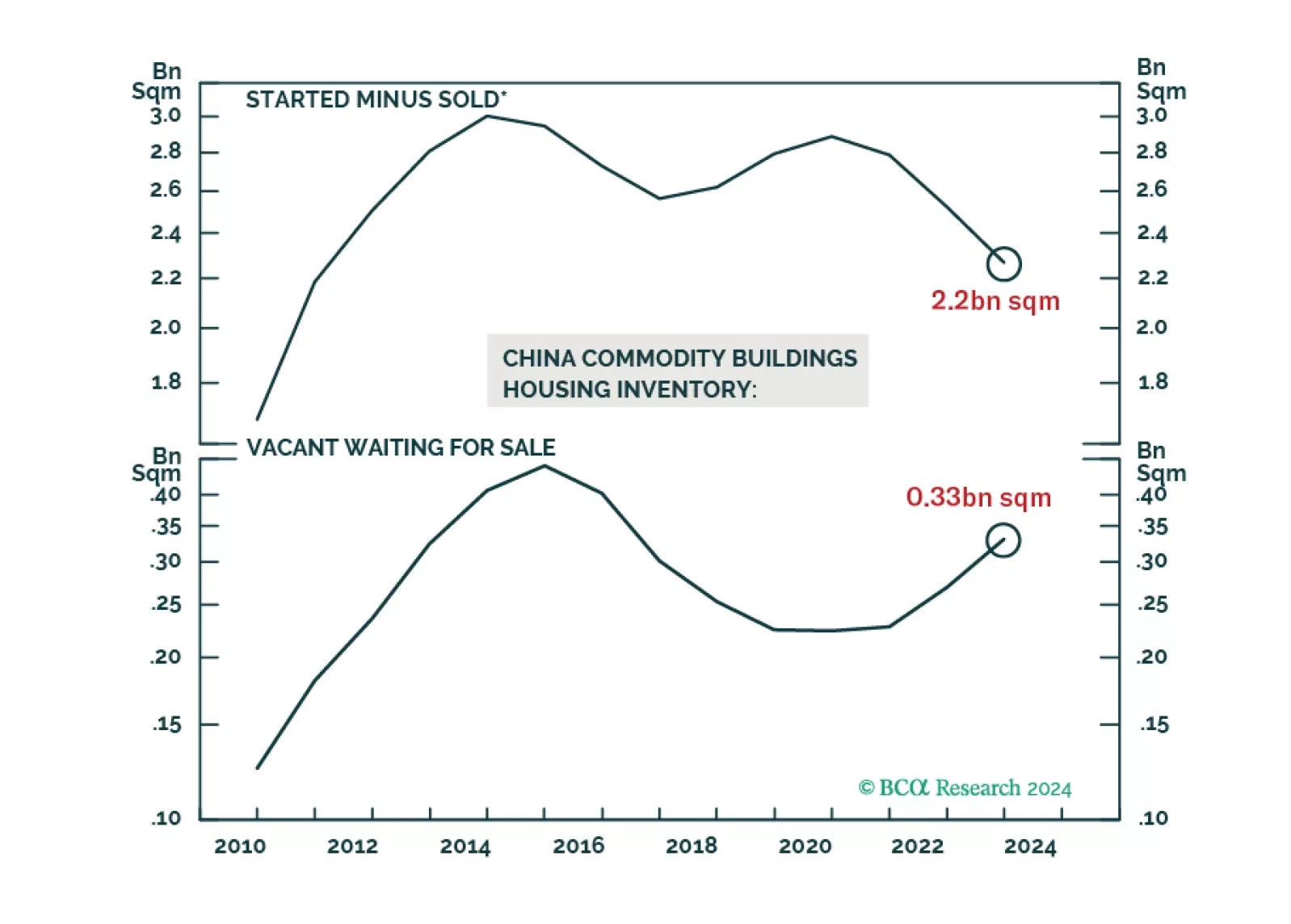

The RMB 500 billion program is small, as it is equivalent to only 4% of property developers' total funding from the past 12 months. This will preclude a recovery in property construction this year. Corporate profits will determine the path of China’s share prices on a cyclical time horizon. Deflation in China will persist for now, which will depress corporate profits even if volumes grow modestly.

The stock market will suffer a setback from the weakening labor market and a rebound in US and global policy uncertainty.

A reality check on credit data and announced property sector support measures indicates that the recent surge in Chinese share prices is unjustified based on the country's economic fundamentals.

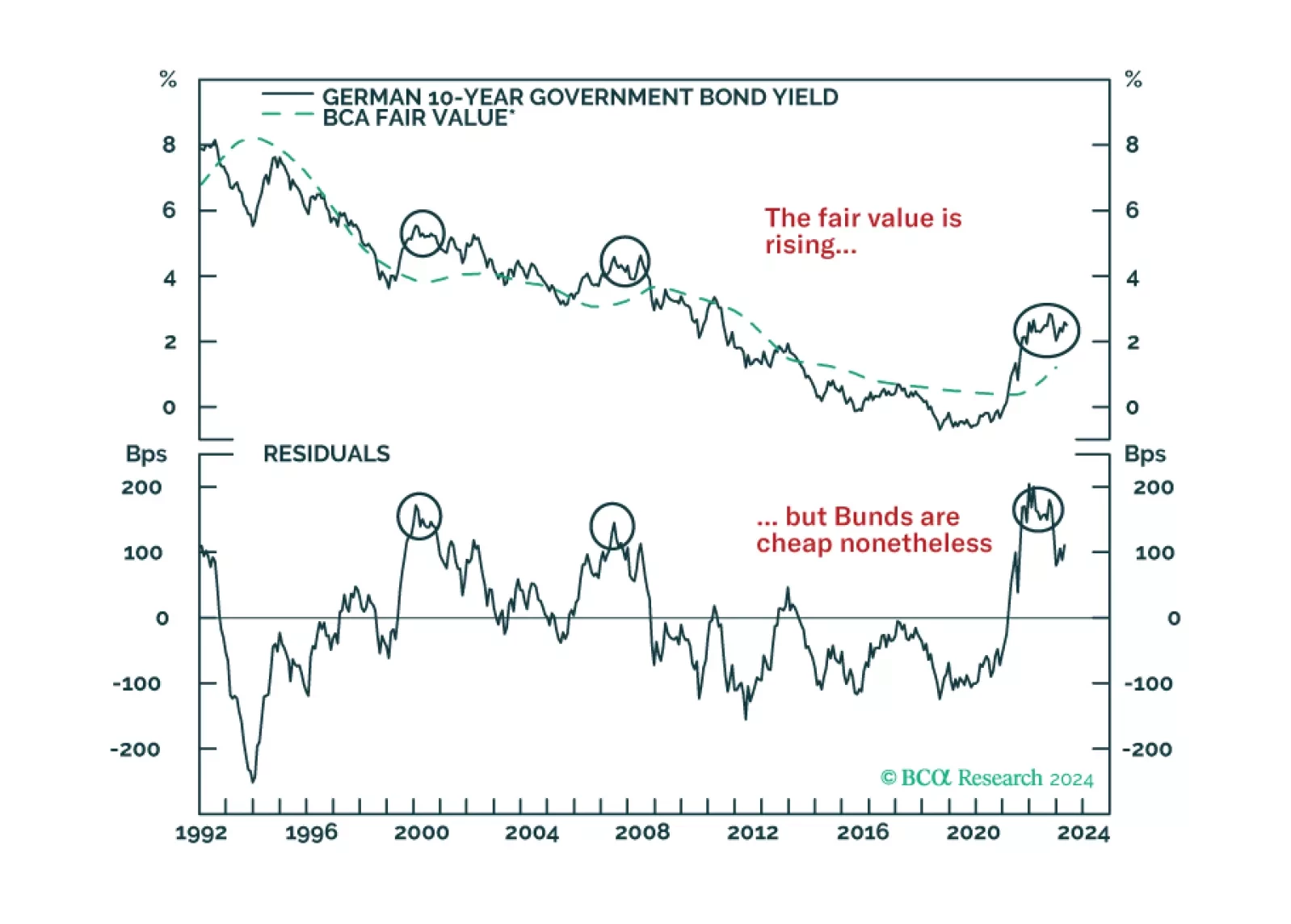

German Bunds have cheapened considerably, and the ECB is about to start cutting rates. Does this combination guarantee immediate profits from buying these bonds?