Commodities & Energy Sector

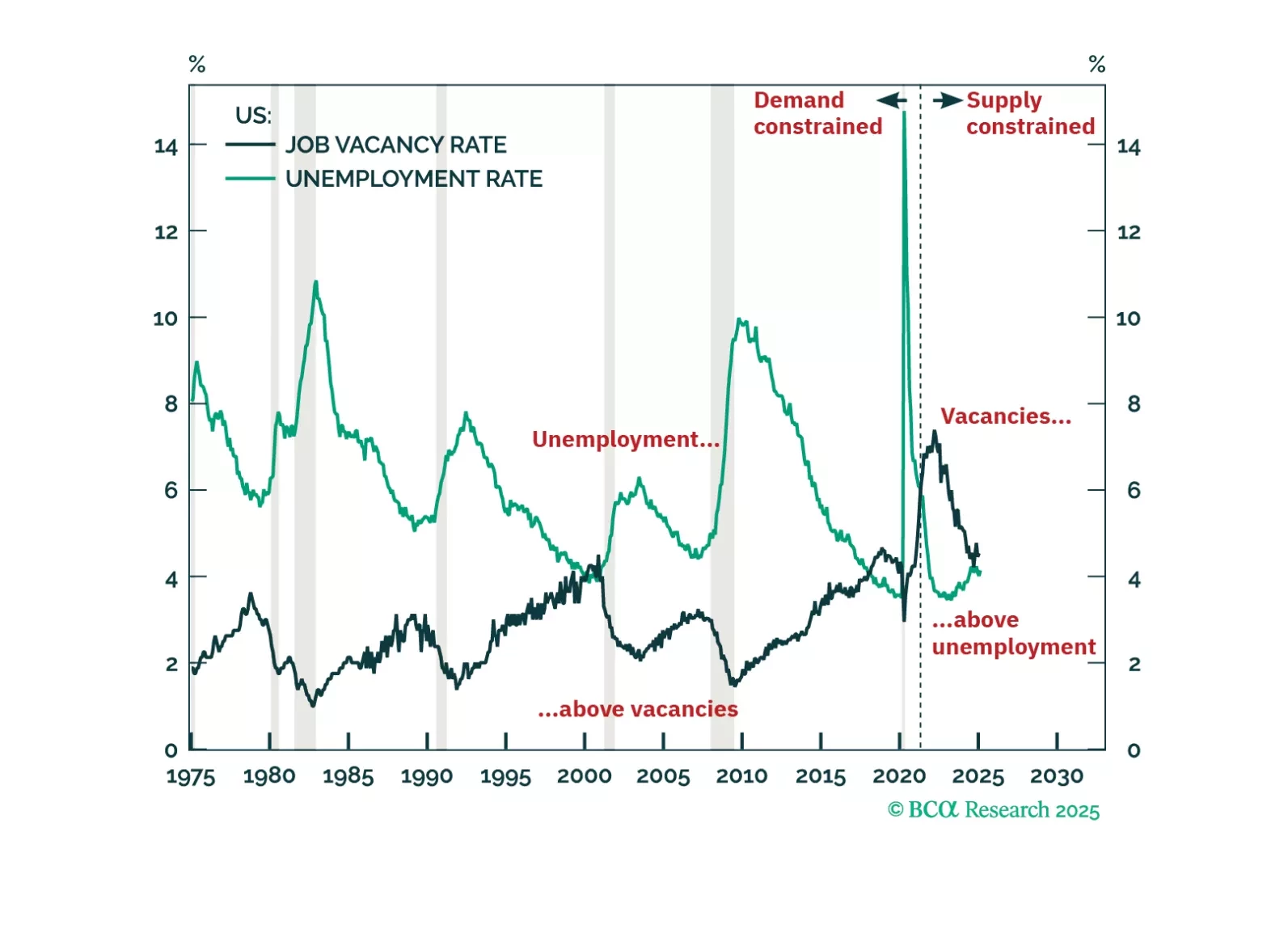

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.

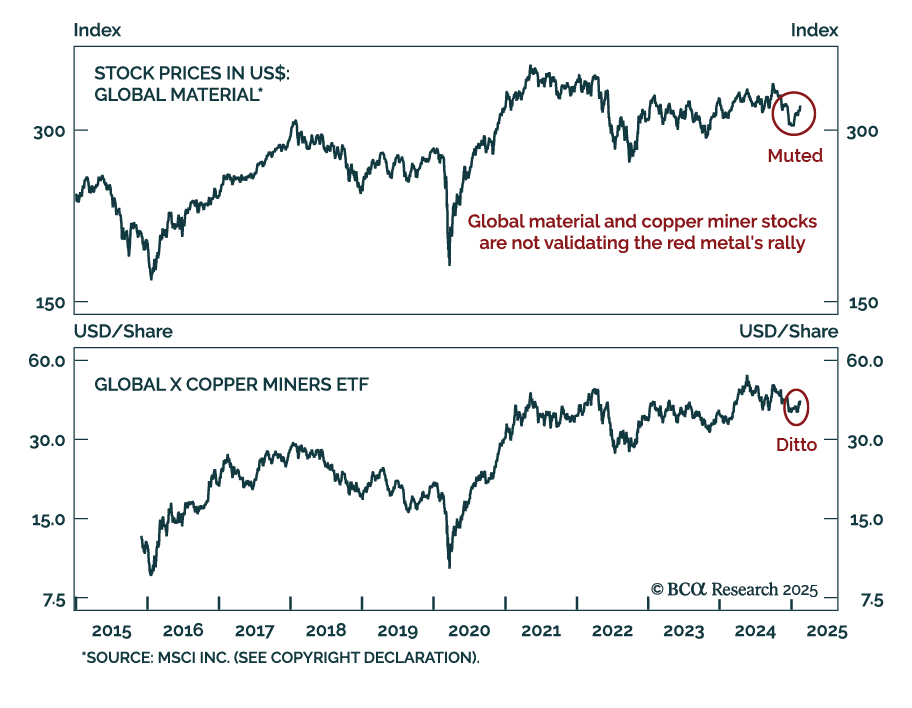

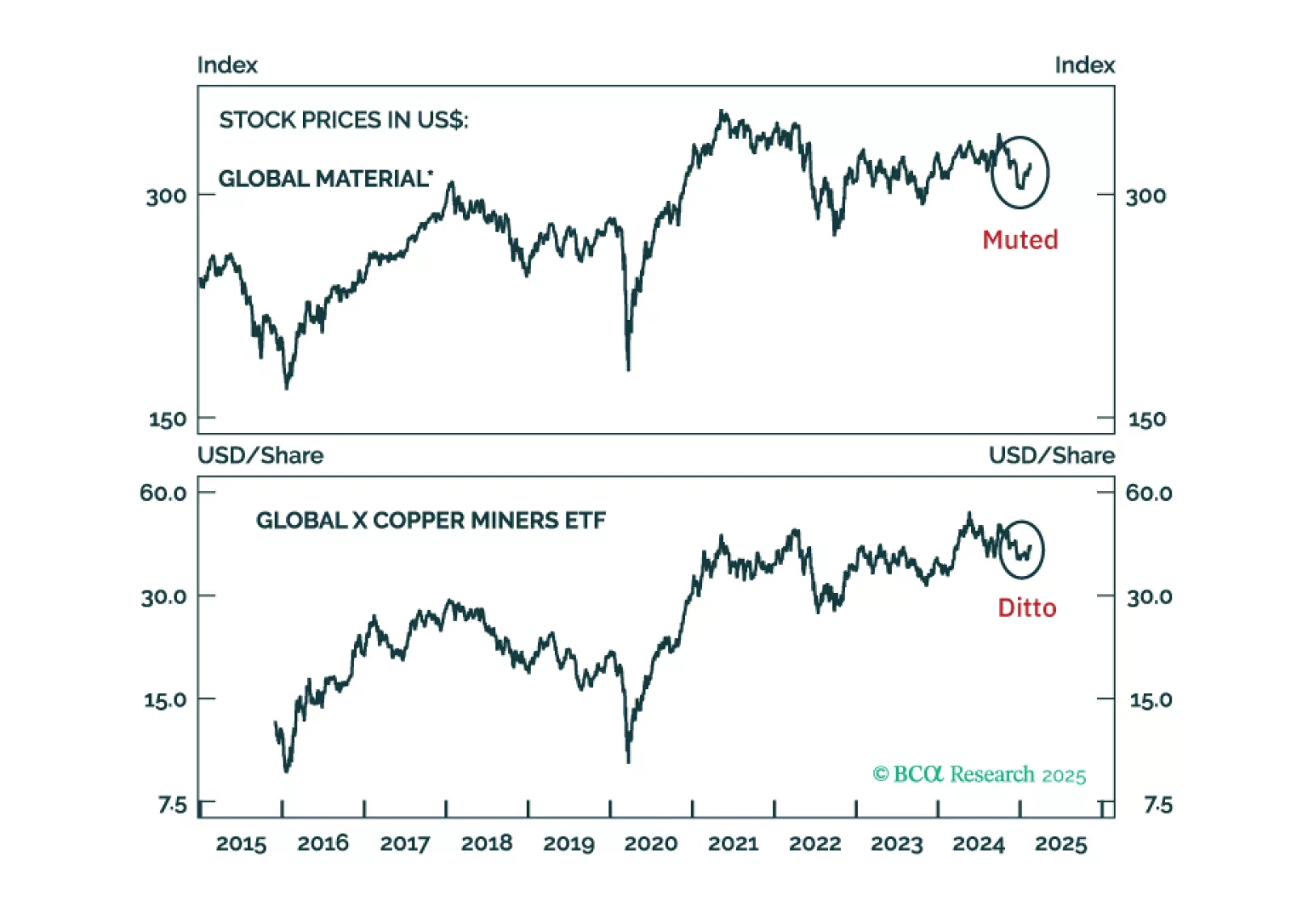

Expectations of US import tariffs drove the latest upleg in the prices of precious and industrial metals. However, there are no significant economic or political incentives for the US to impose import tariffs on these metals. Therefore, investors should fade the recent spike in gold, silver, platinum and copper prices. We are initiating a short position on silver as a tactical trade.

In lieu of all the geopolitical and economic news in media, this report looks at where next the dollar is likely to trend in the next one-to-three months. Our view is down, though on a cyclical horizon (six-to-twelve months), we would not be short the dollar, for now.