Corporate Bonds

The ECB is changing its tone, but don’t call it a pivot. Slower cuts, sticky disinflation, and a soft growth patch shift the opportunity set. We break down the tactical bond trades and why EUR/USD dips are still for buying.

Our Portfolio Allocation Summary for June 2025.

Our Portfolio Allocation Summary for May 2025.

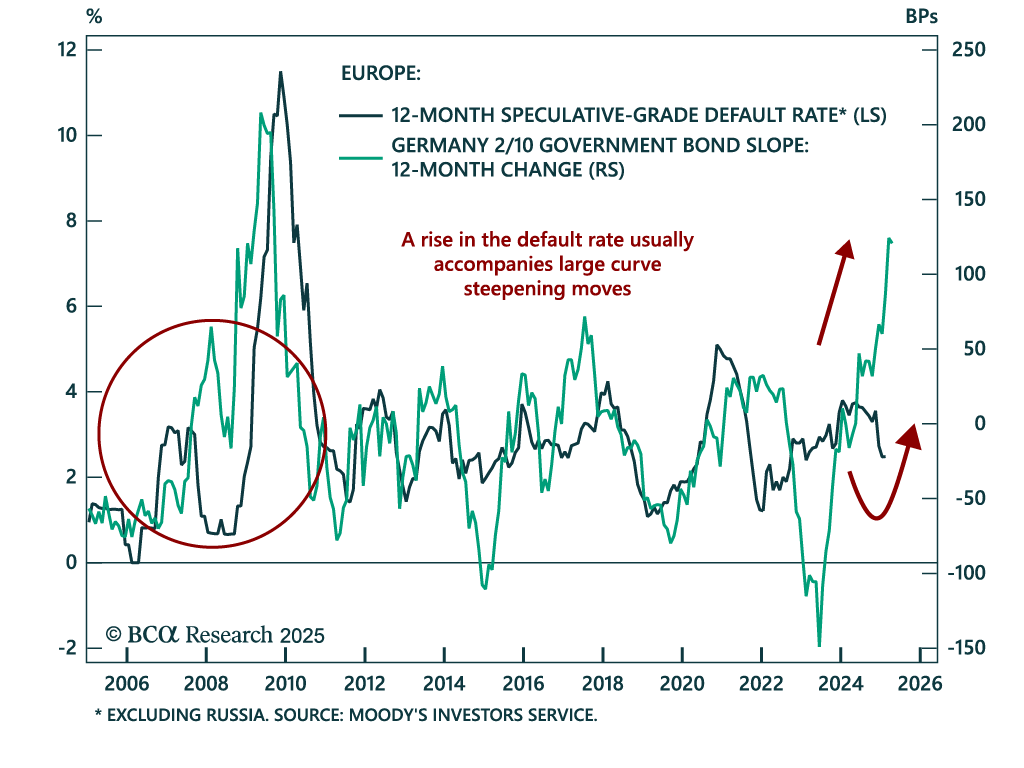

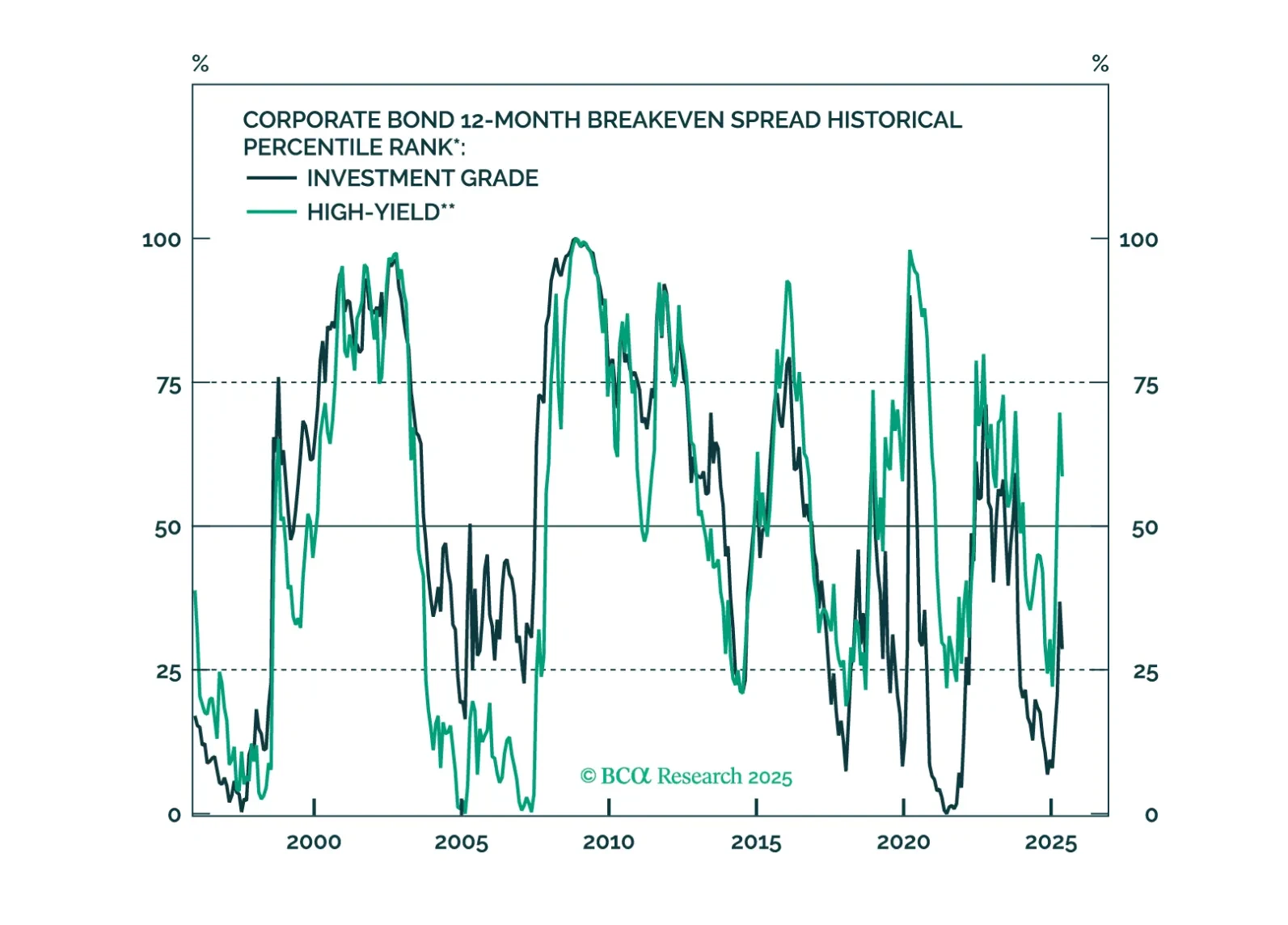

This year’s corporate bond sell off has hit high-yield more than investment grade, and high-yield spreads have turned relatively more attractive as a result.

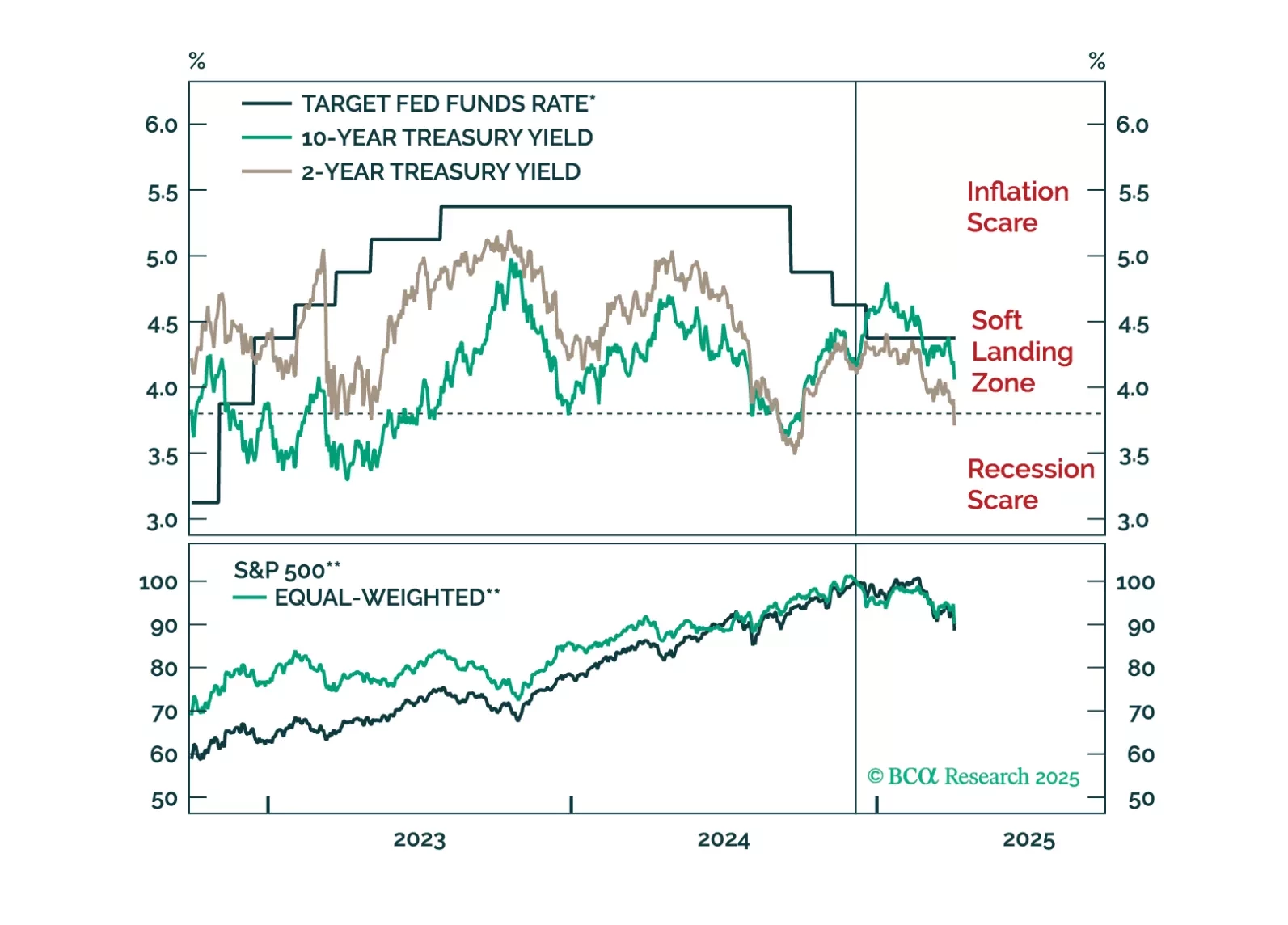

US Treasuries typically outperform both equities and global government bonds during downturns. Recent political shifts could lessen that outperformance this cycle, but we doubt it will disappear completely.

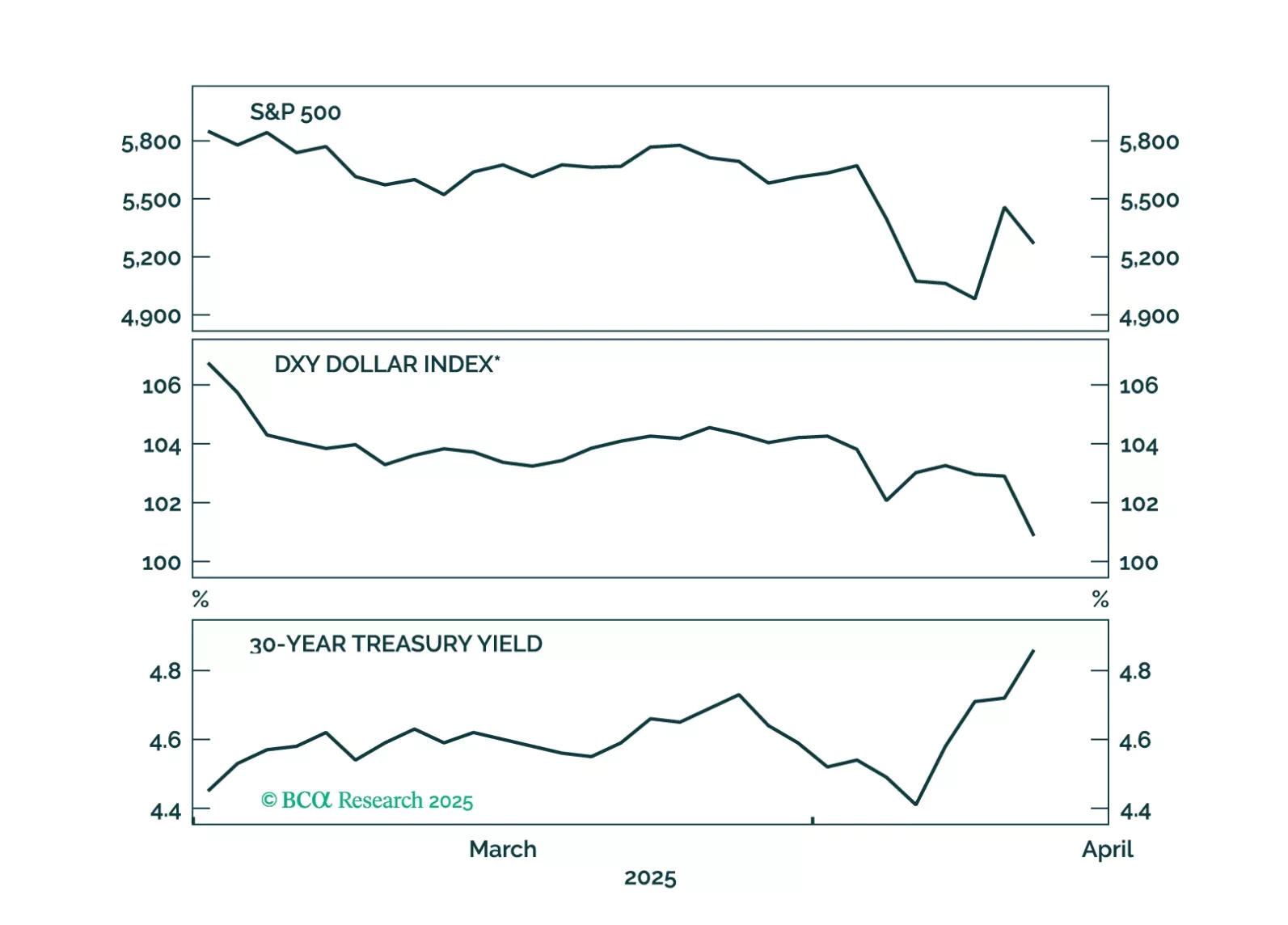

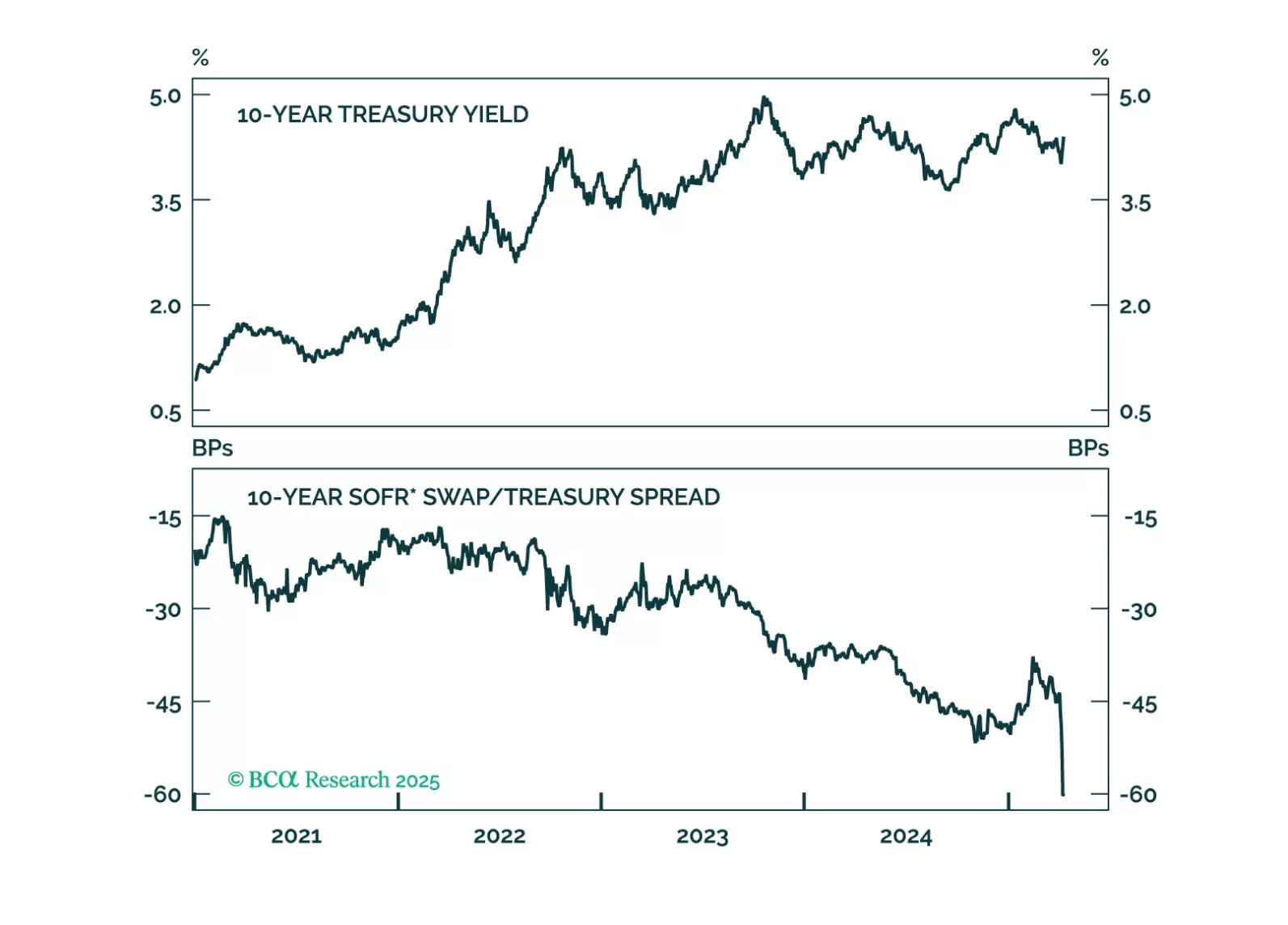

The combination of dollar weakness and rising US yields suggests global investors are questioning the safe-haven status of US Treasuries.

Our Portfolio Allocation Summary for April 2025.

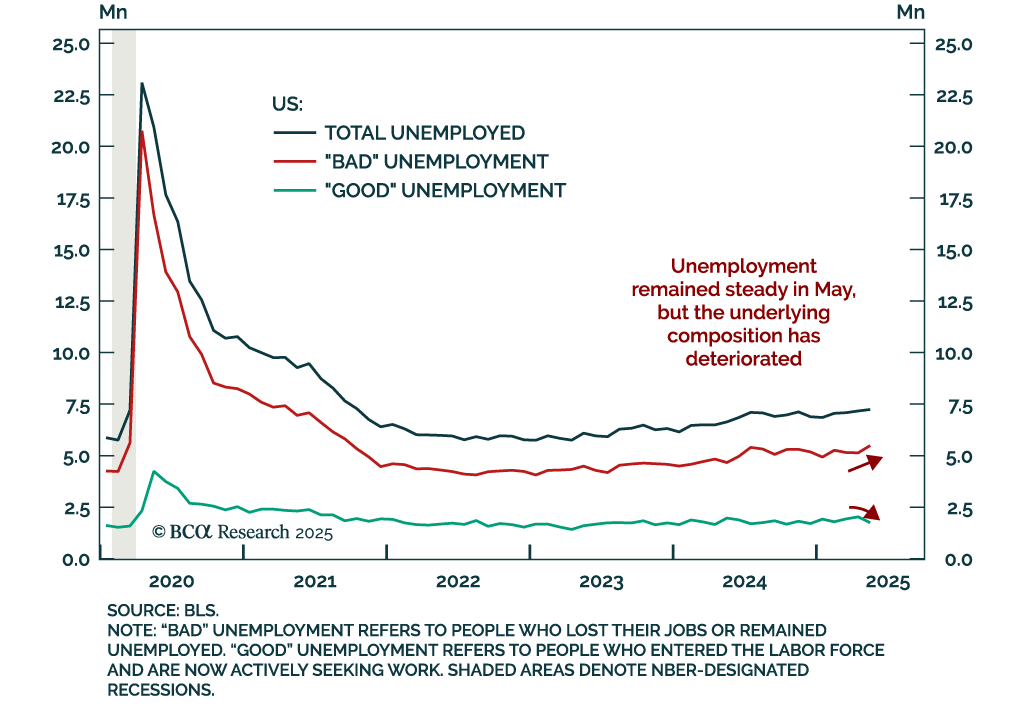

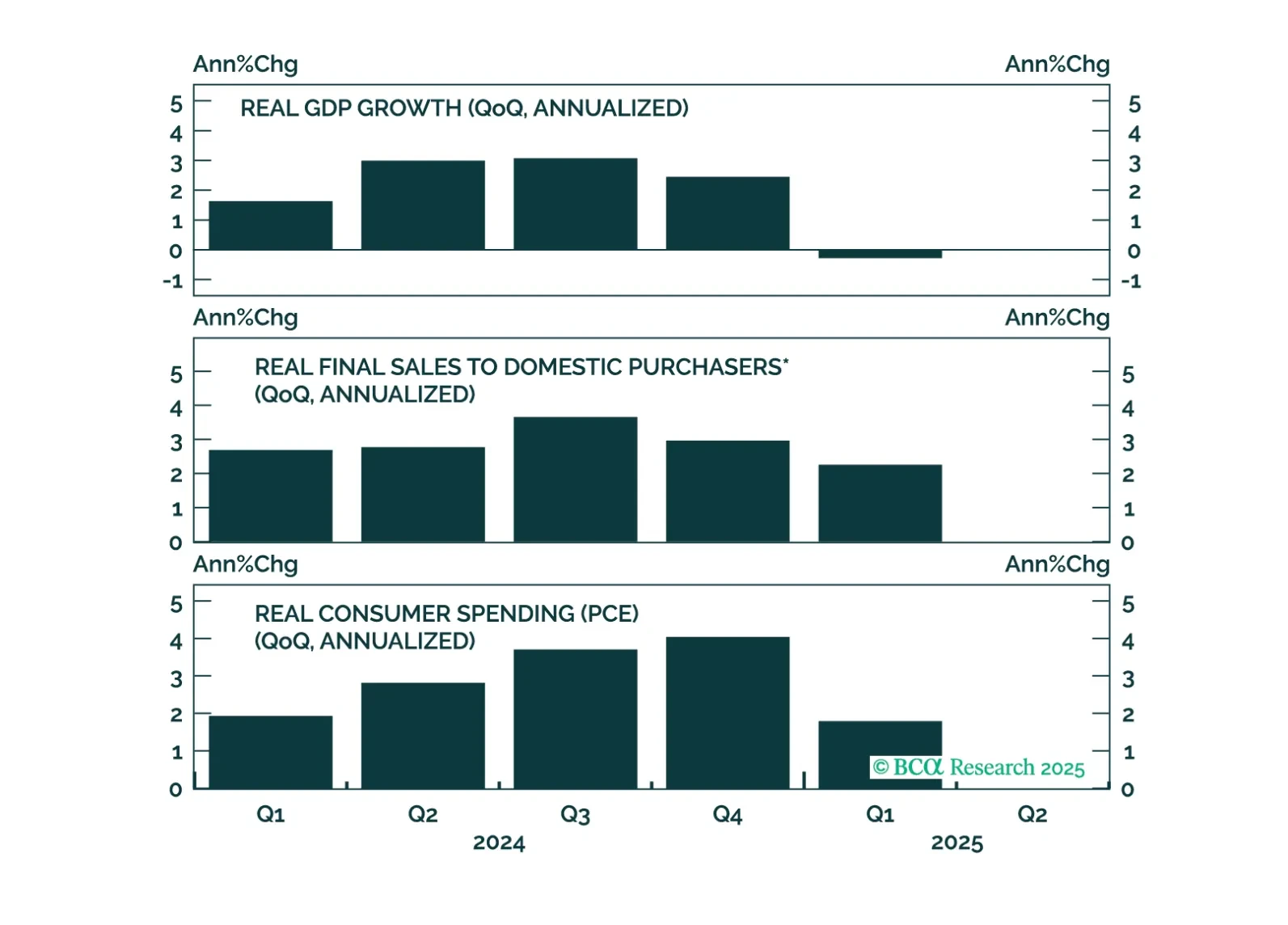

The March employment report showed strong job growth, but the labor market remains in a fragile state and the demand shock from tariffs could be the catalyst that tips it over the edge into recession.