Economy

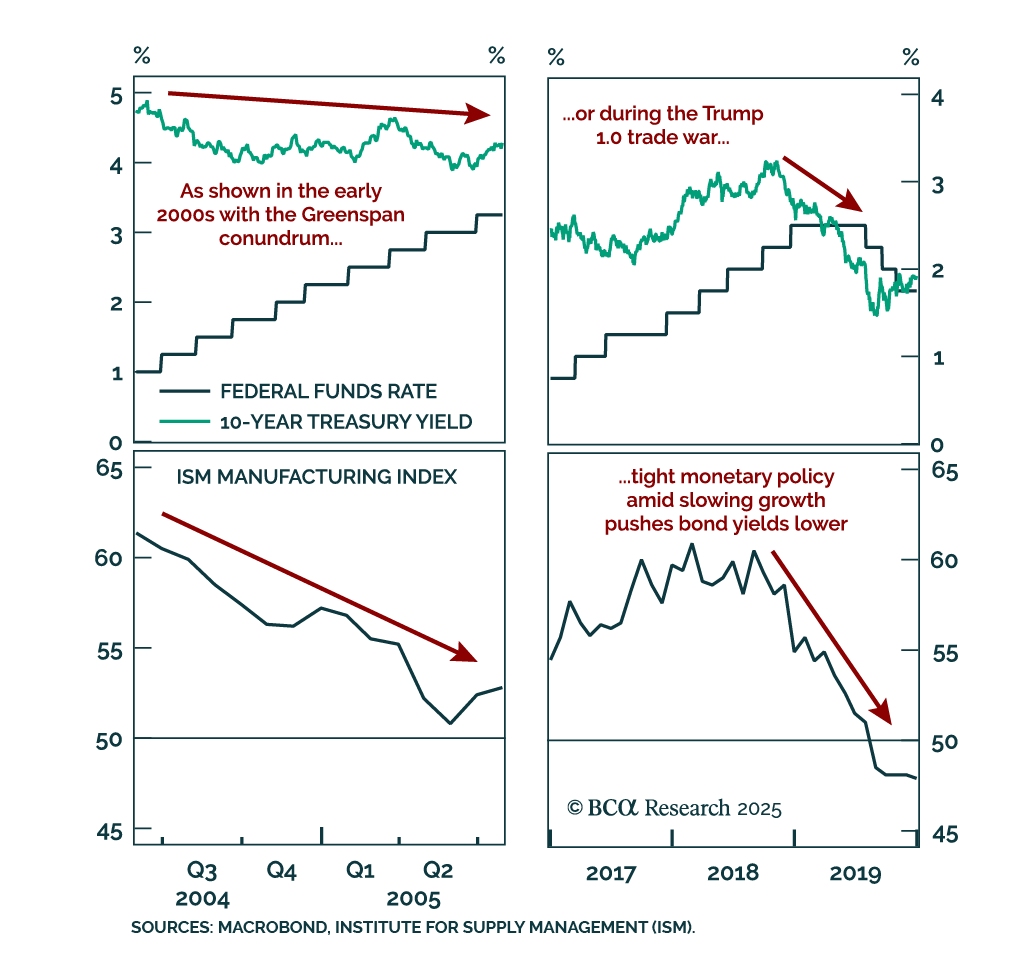

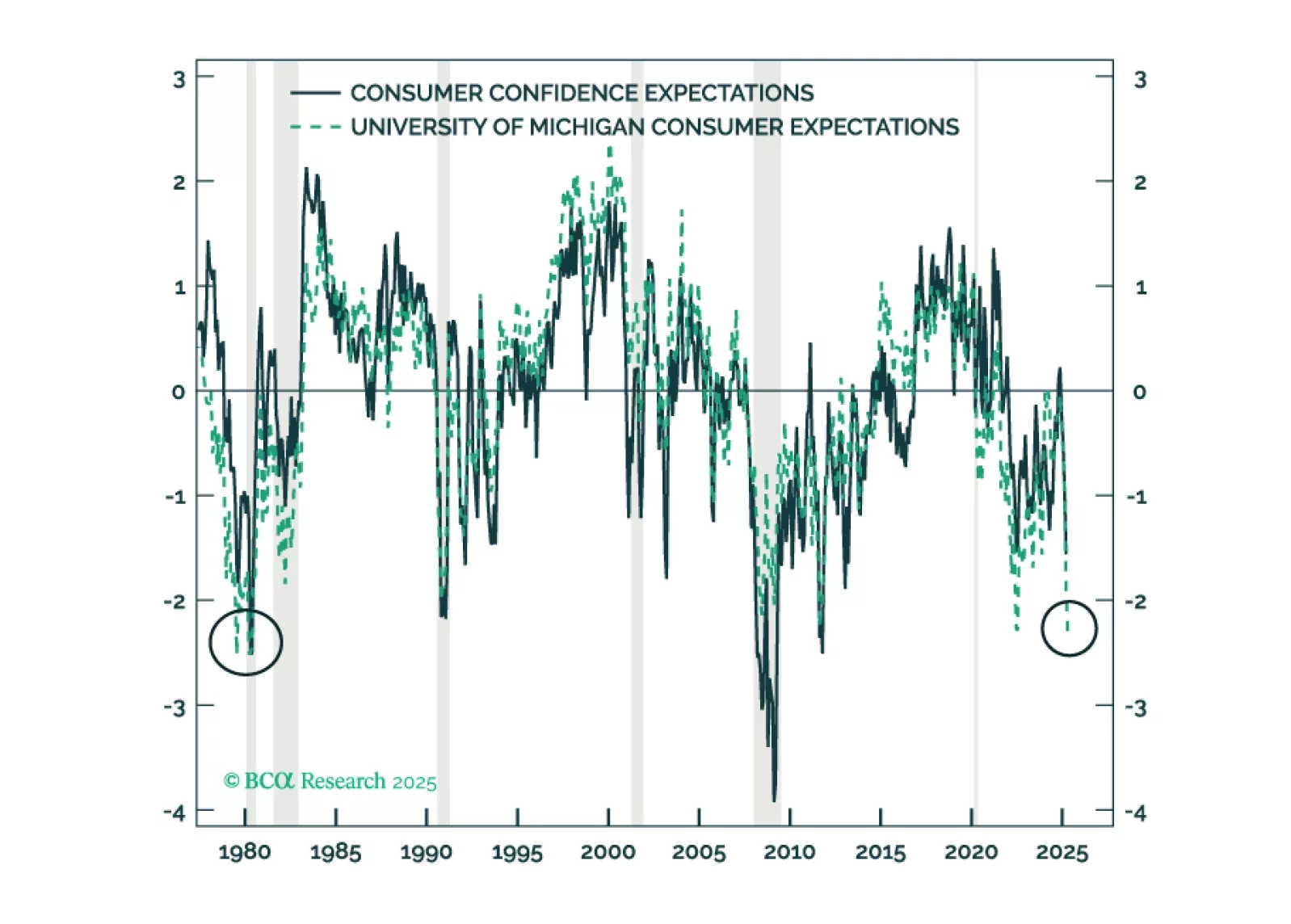

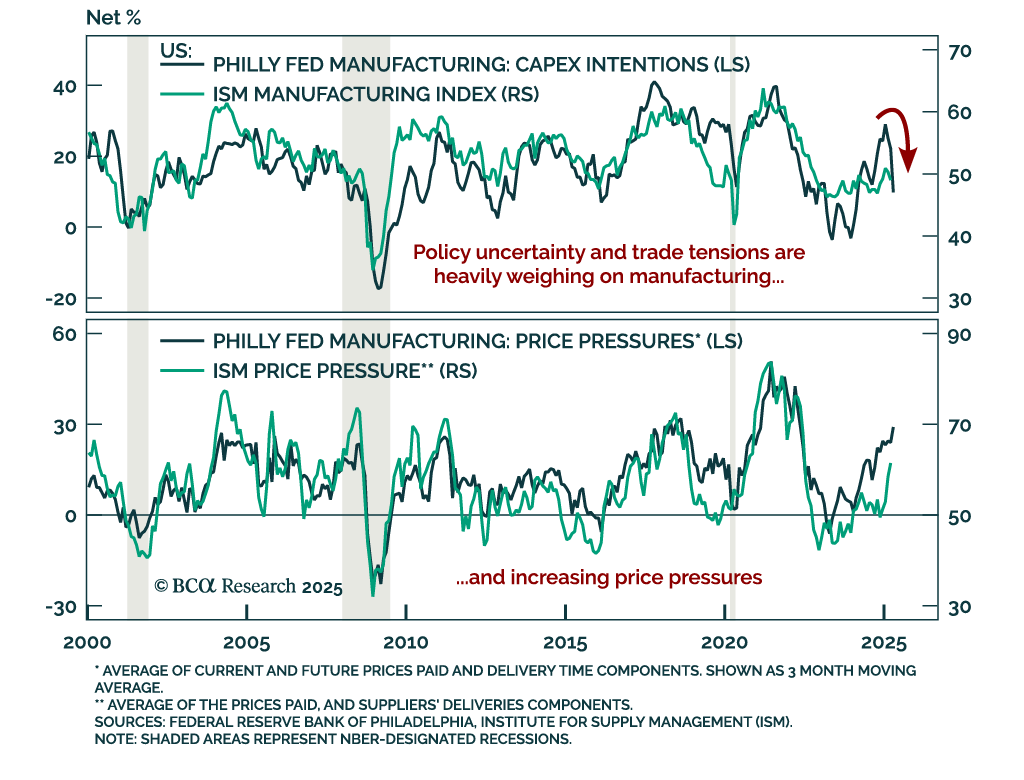

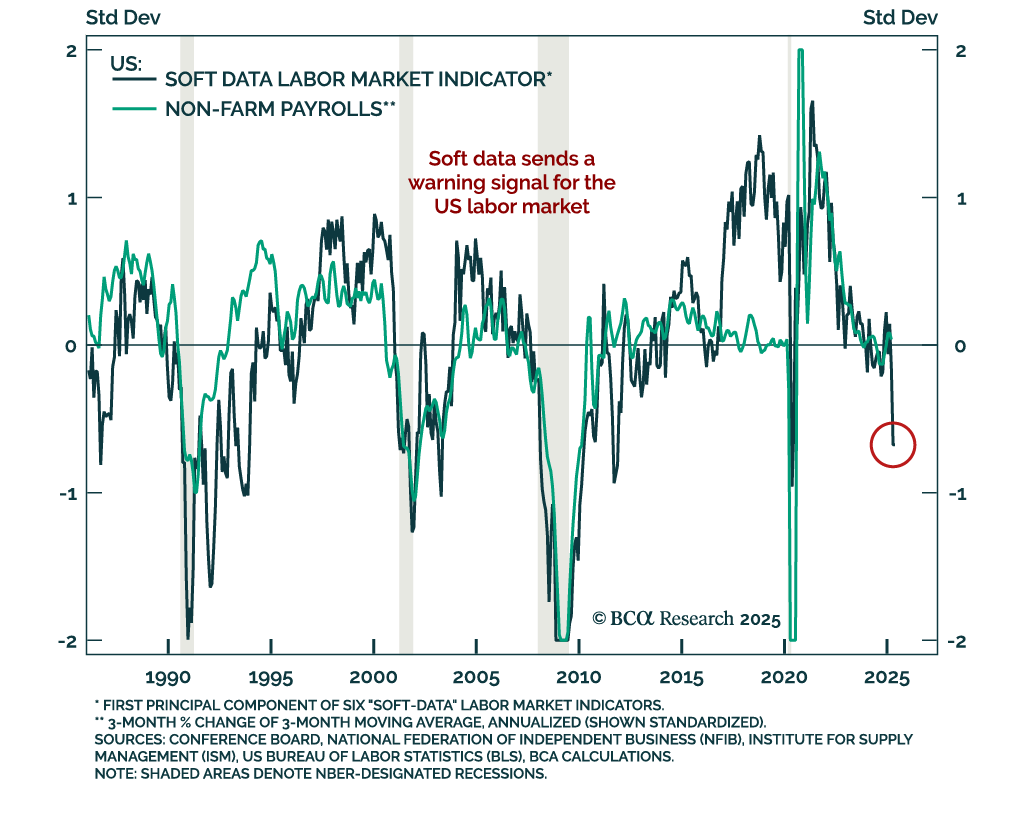

The policy-induced decline in consumer confidence has spread to businesses and investors, increasing the probability of a recession even if the administration reverses field on its aggressive tariff measures. We reiterate our defensive asset allocation recommendations.

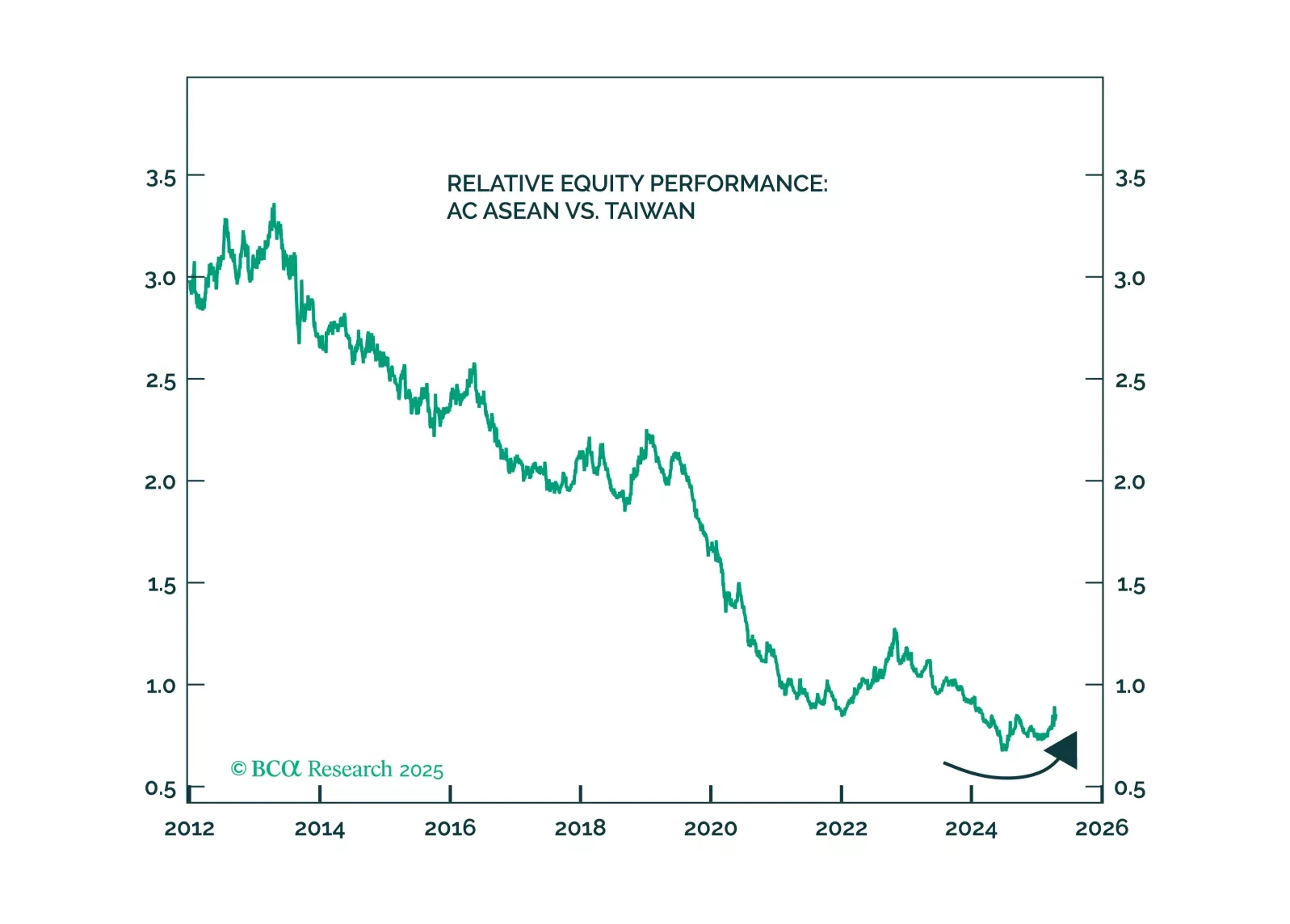

Upgrade the odds of a full-scale war in the Taiwan Strait from 5% to 10%. Rapid escalation of US-China economic war raises the probability of tensions spilling into the military-strategic domain. Investors should buy insurance against this tail risk while it is cheap. Meanwhile, use this year’s trade shock and equity volatility to increase allocation to EM manufacturing states.

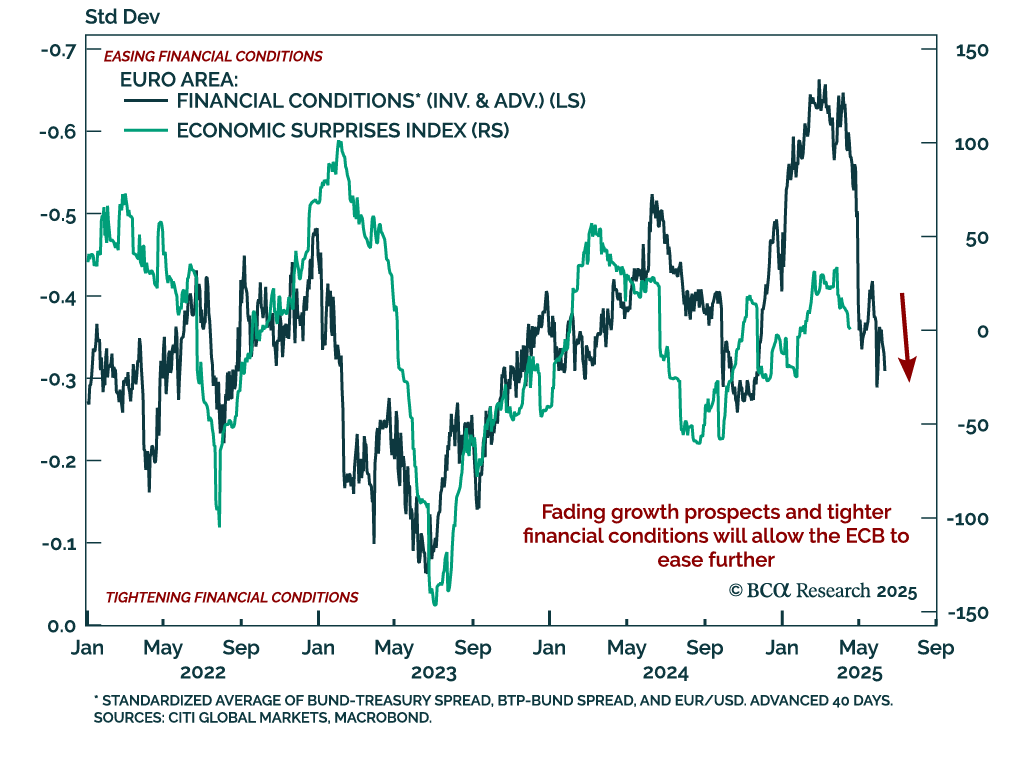

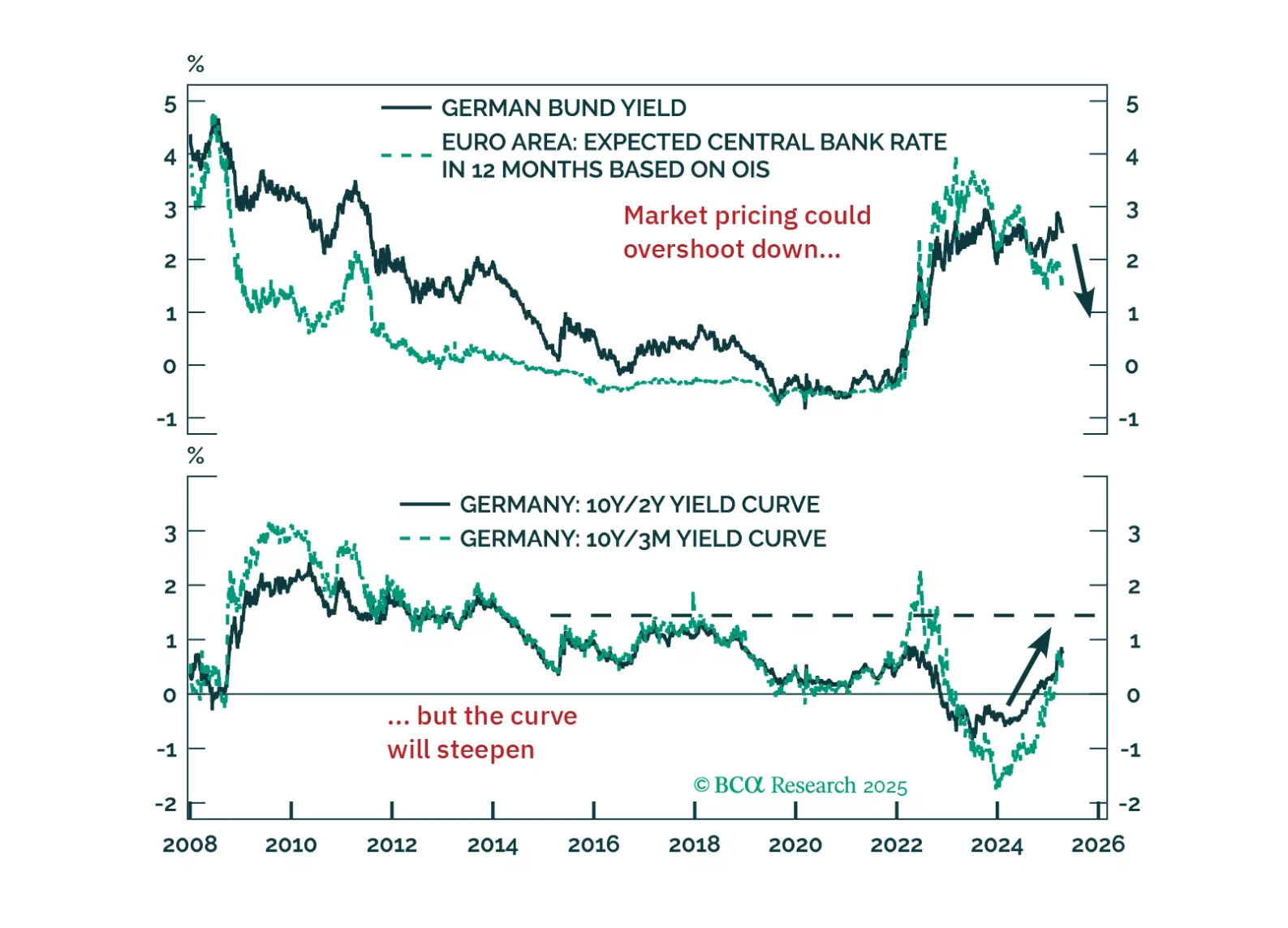

Europe’s deflation problem is getting harder to ignore. This week’s ECB cut is just the beginning — tariffs, the euro’s rally, and softening demand all point to more easing ahead. We explain what it means for yields, equities, and EUR/USD.