Financial Markets

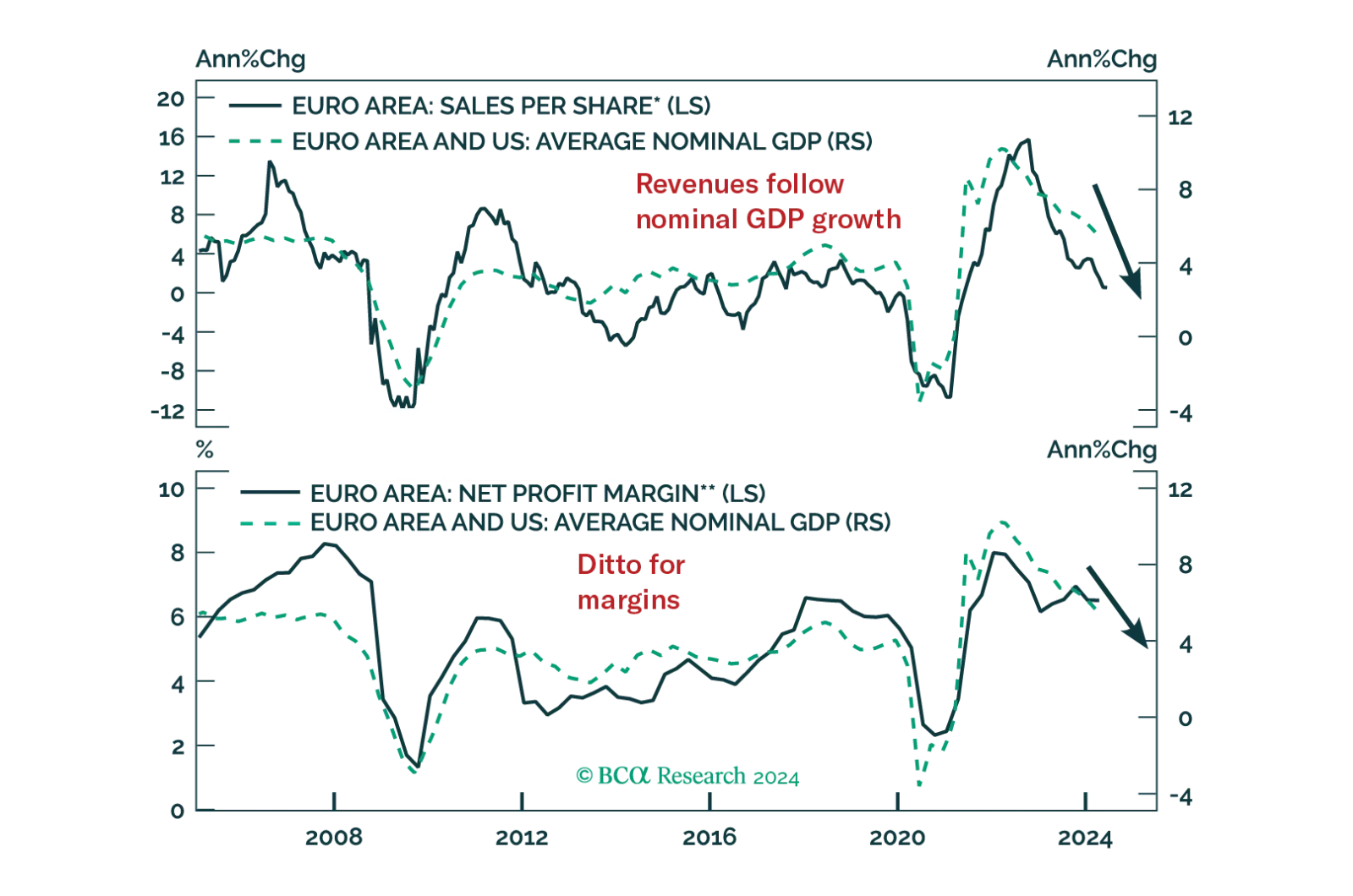

The real threat to European equities is growth, not political risk. How low will Eurozone earnings fall during the coming recession and how much will equities decline in response?

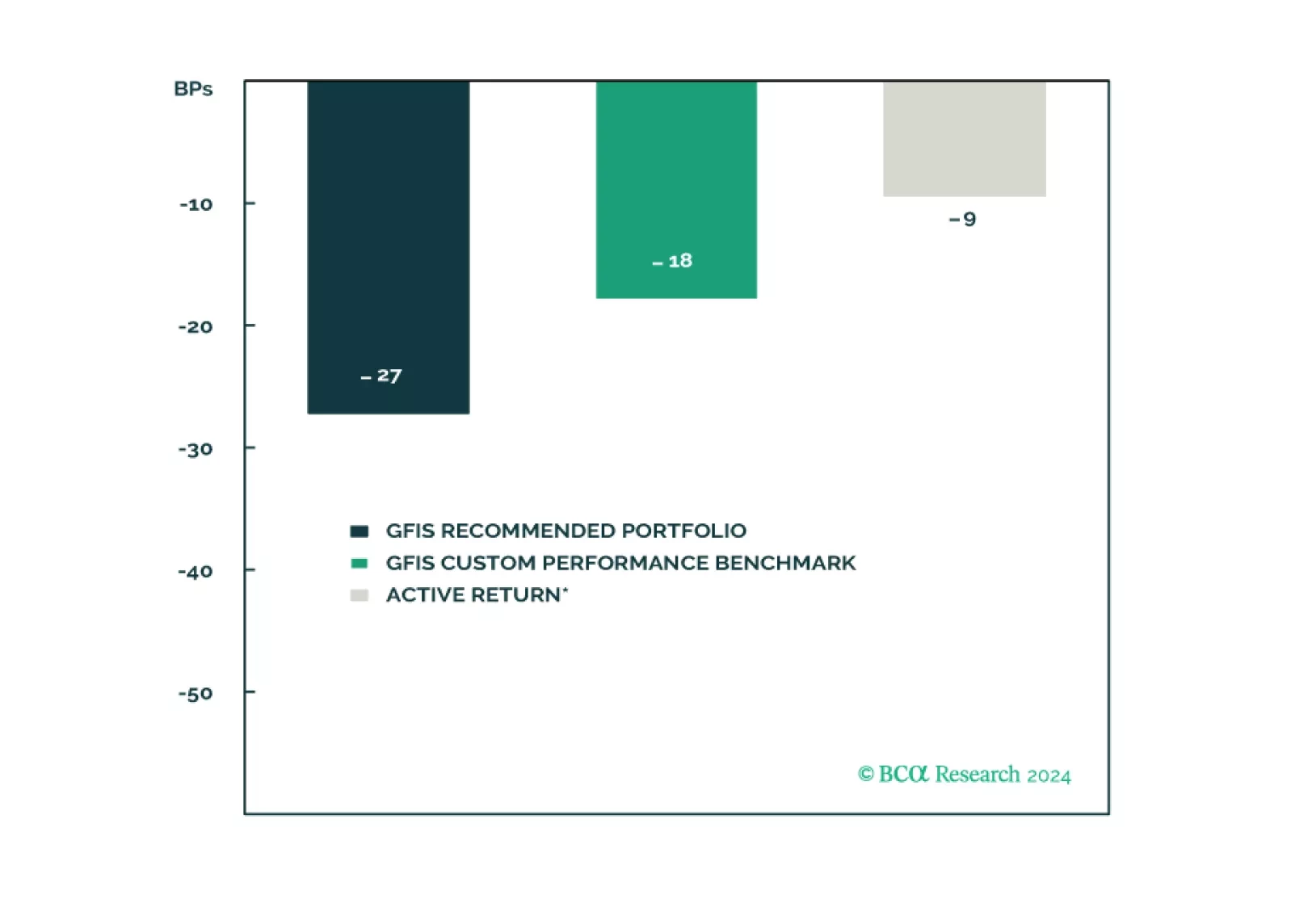

In this report, we present the quarterly review of our Model Bond Portfolio. Rebounding growth and political instability led to slightly negative portfolio performance in Q2/2024. As global growth starts to moderate, we continue to favor government bonds over credit. Maintain a defensive portfolio stance.

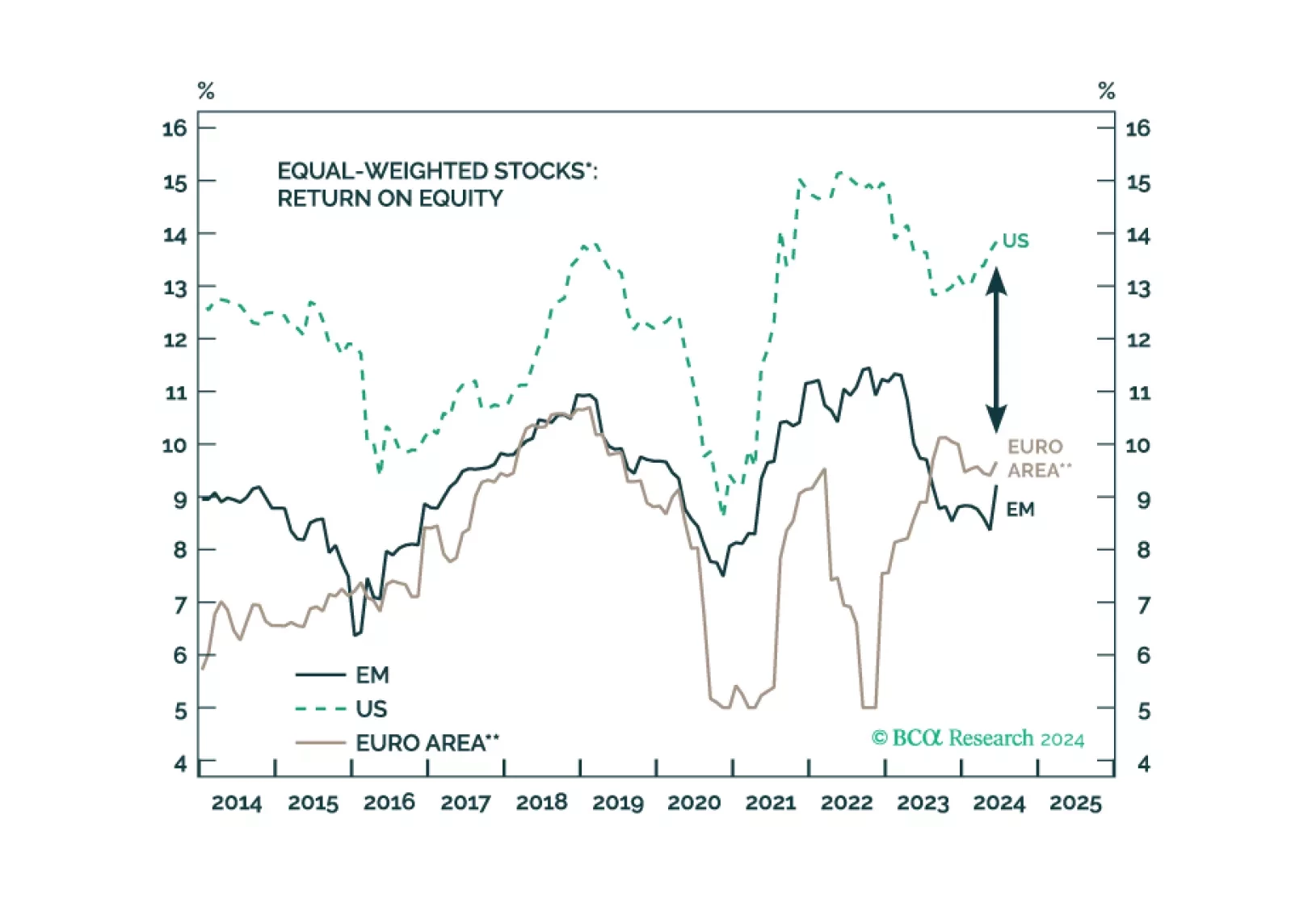

The failure of EM stock prices to rally over the past 13 years is rooted in their companies’ inability to grow their profits. Even though EM equities appear cheap based on their cyclically adjusted P/E ratio, there has been a regime change in EM corporate profitability. Therefore, the CAPE model should not be used to value EM stocks now.

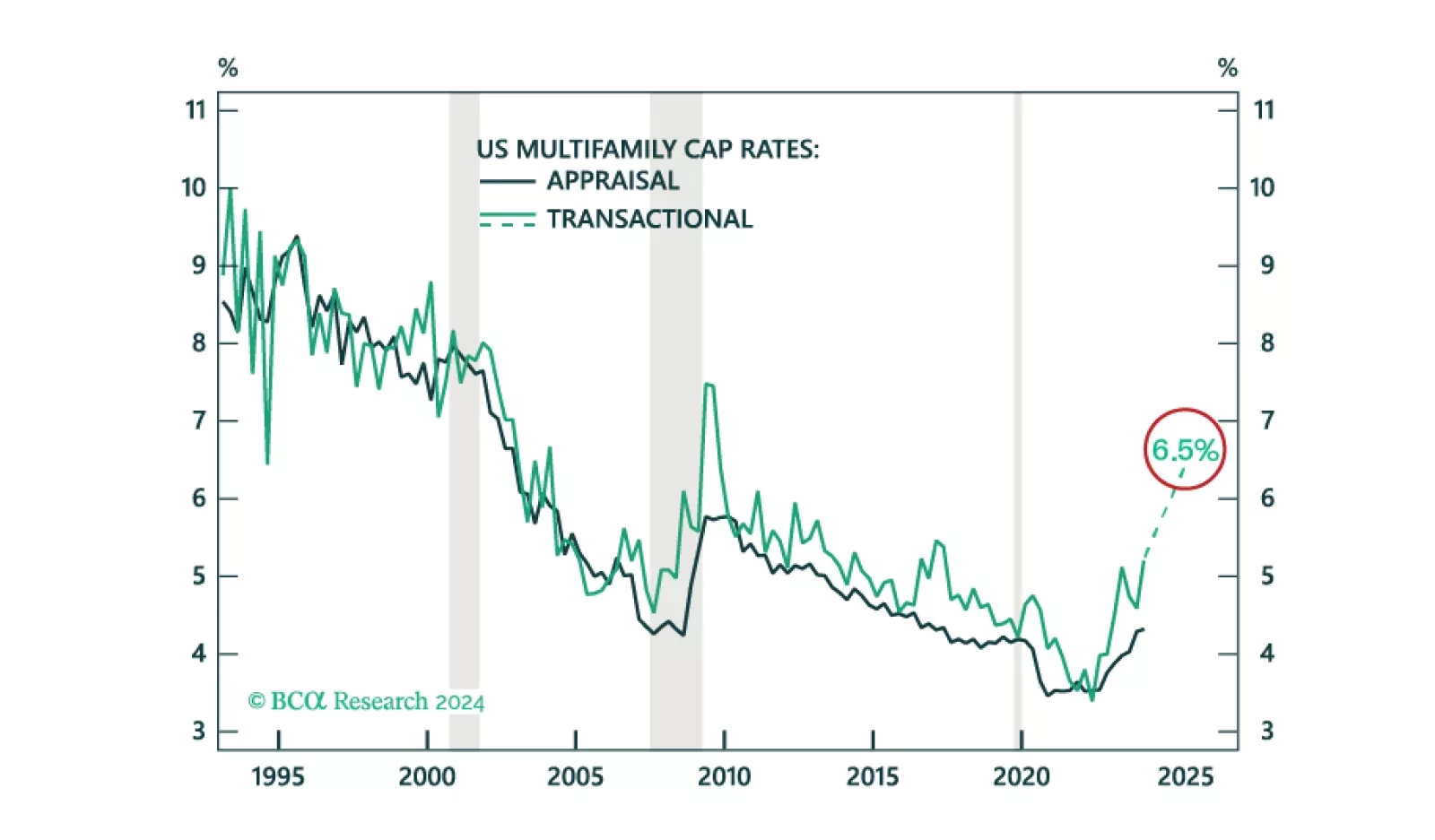

We project US Multifamily cap rates to increase from 5.2% to 6.5%. While we find an unfavorable risk-adjusted return on the asset, especially relative to other opportunities in CRE, cap rates are moving closer to peak.

At first glance, France has moved to the far left. However, this coalition is fragile, and Macron’s allies still hold the balance of power. What are the assets that will benefit from this new political setup, and those that will not?