Financial Markets

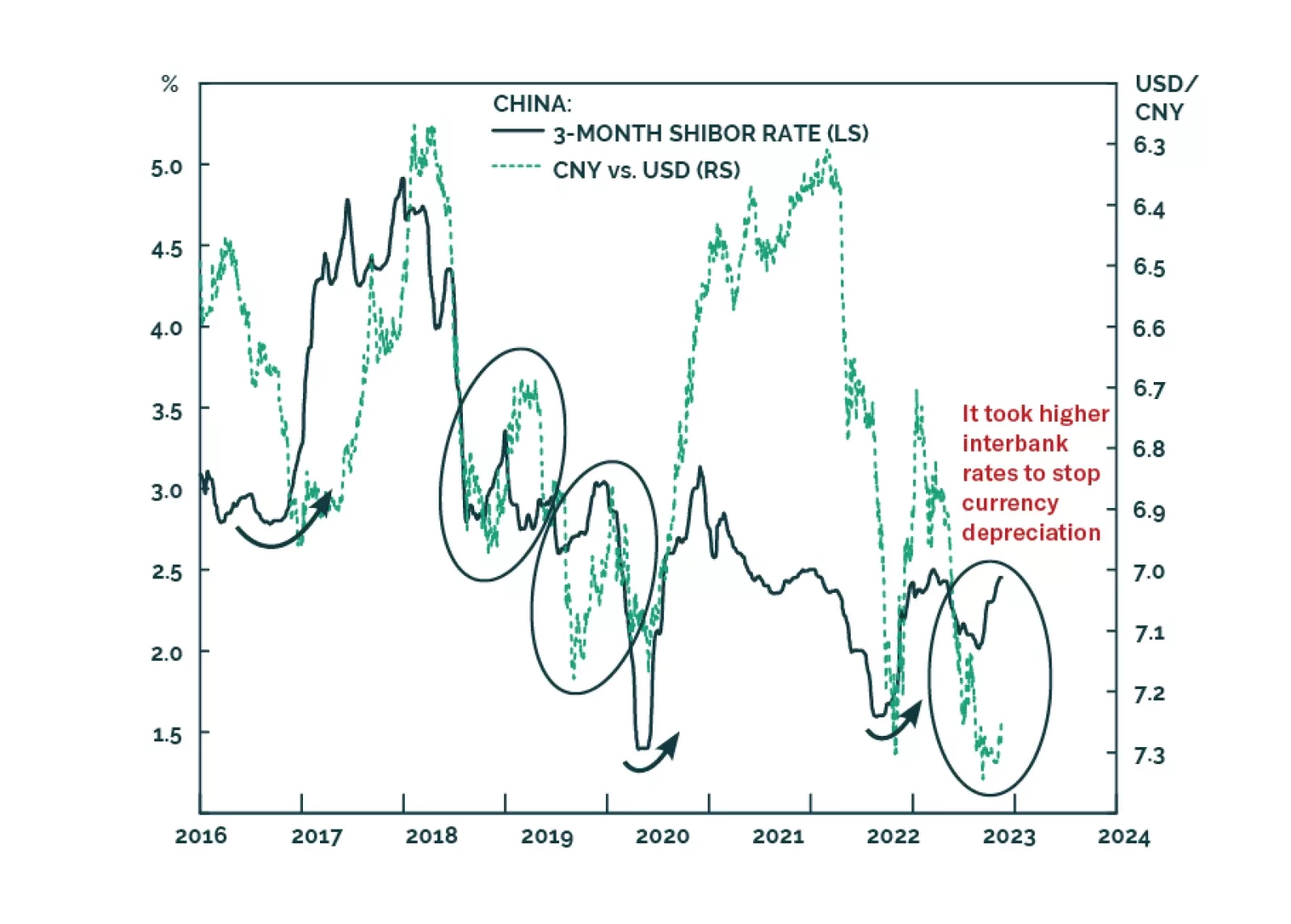

Many commentators have attributed the latest increase in Chinese interest rates to an improving economy, the large issuance of government bonds, the tax payments season, and other technical factors. Yet, these explanations are missing the key point: the PBoC has steered interbank rates higher to defend the currency. Higher borrowing costs are the last thing the mainland economy now needs.

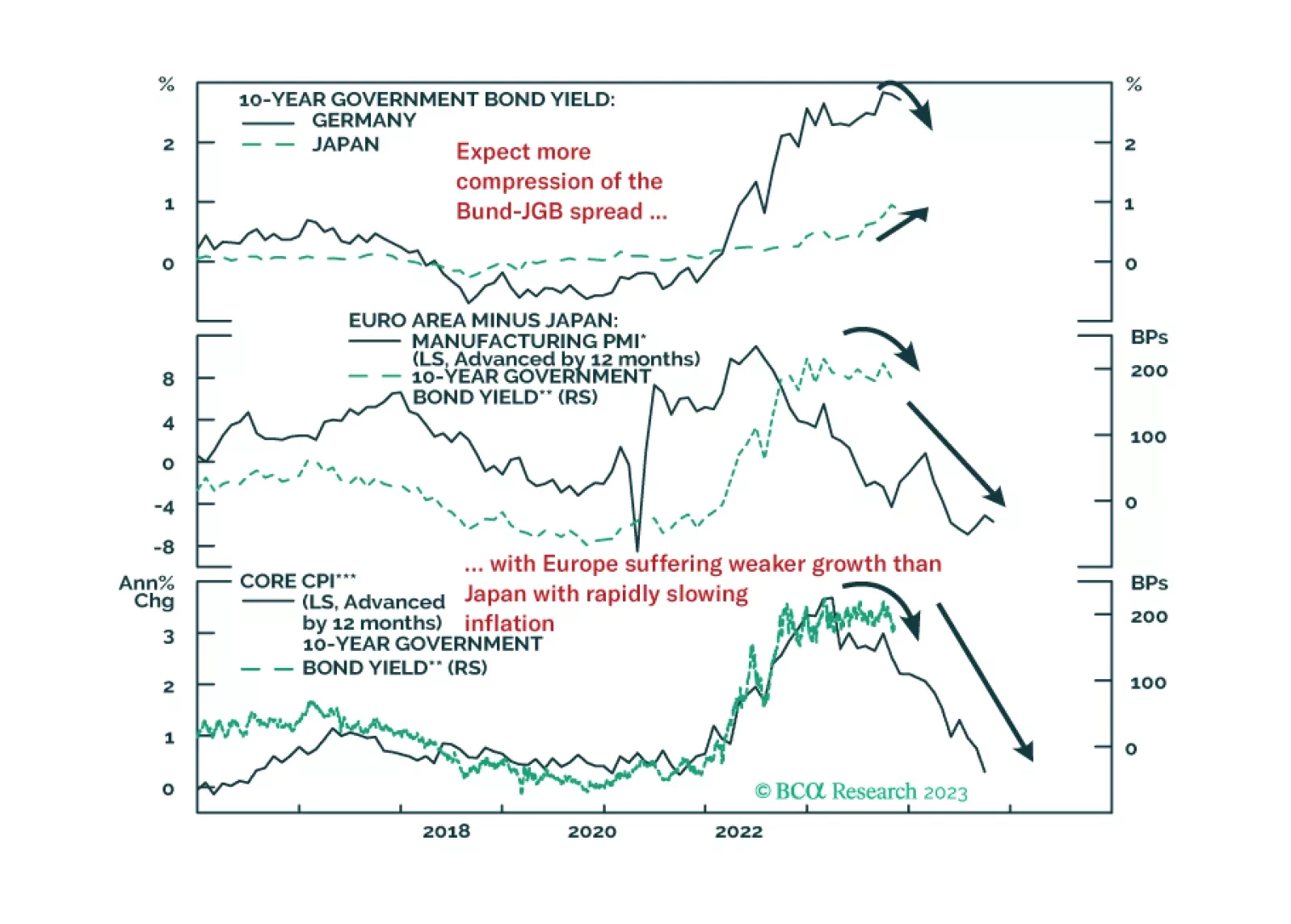

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.

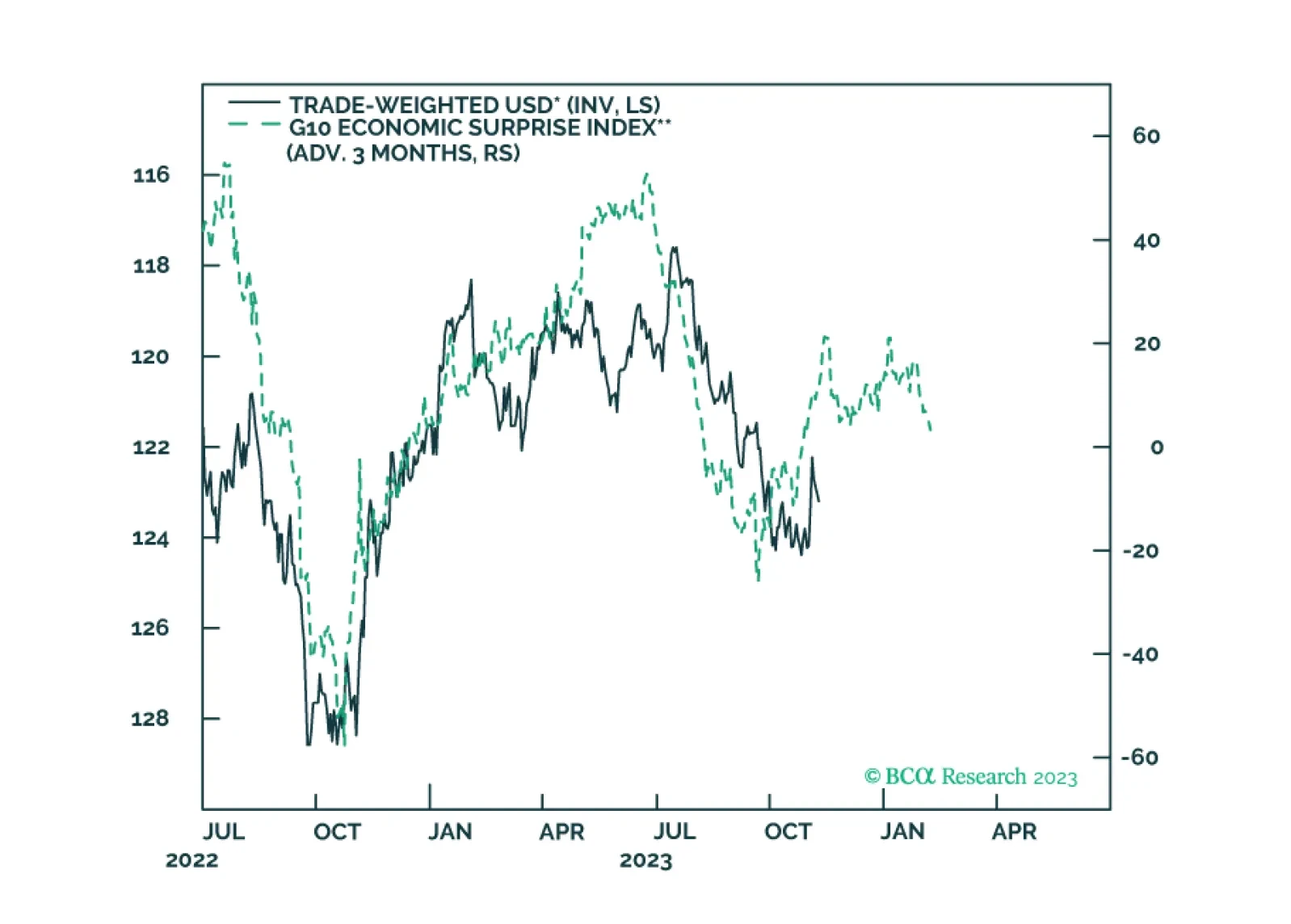

In this report, we go around the globe and survey the near-term outlook for G10 currencies. Our longer-term view on the dollar has been clear, we are sellers. In this report, we review if a tactical sell is also warranted given incoming data and the message from our models.

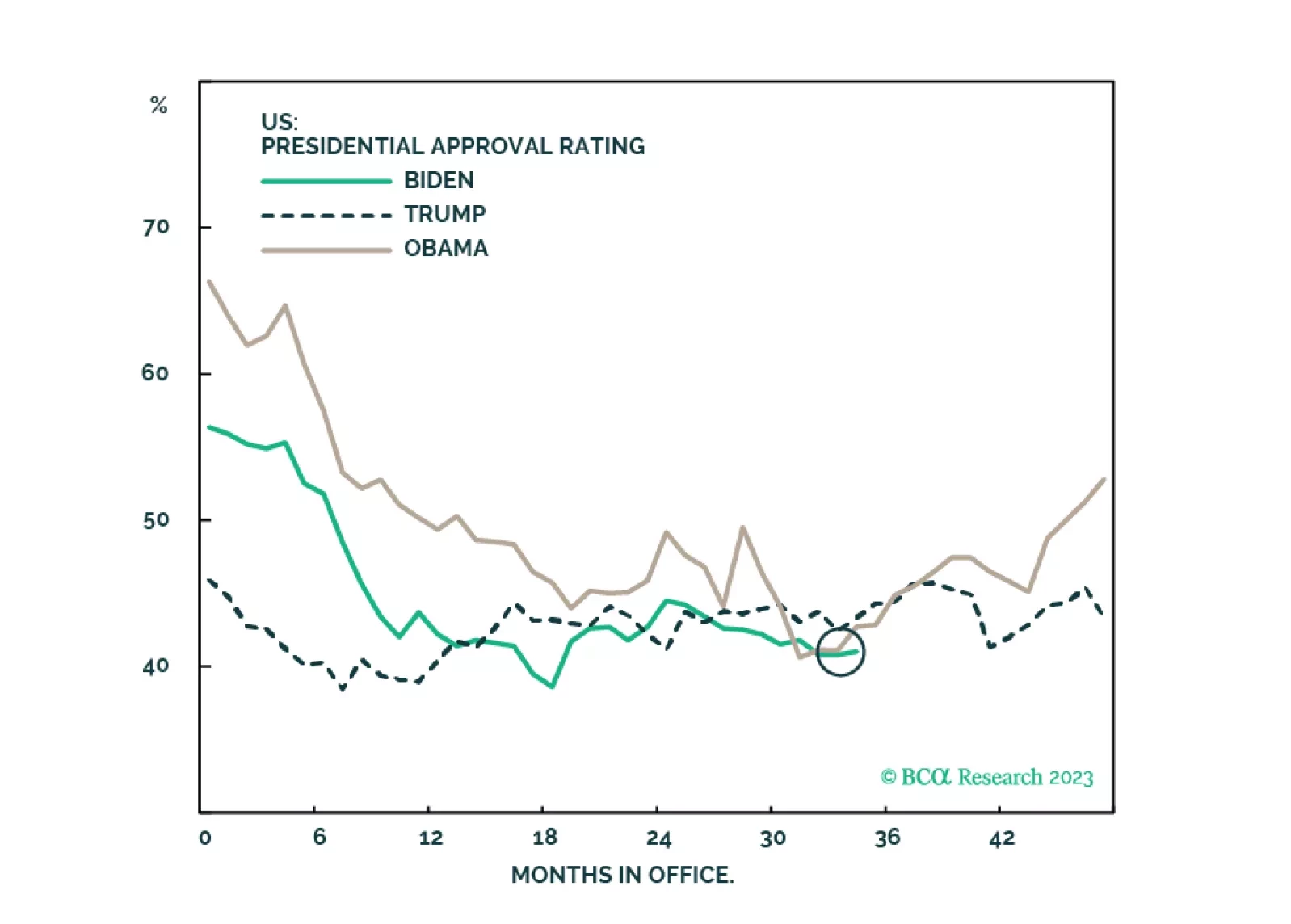

Results from Tuesday’s elections suggest that the Democrats are doing better than what their 2024 polling are showing. While the results are marginally positive for equities, investors should not overrate this off-year election, especially considering the slowing economy and the many foreign challenges facing the US.

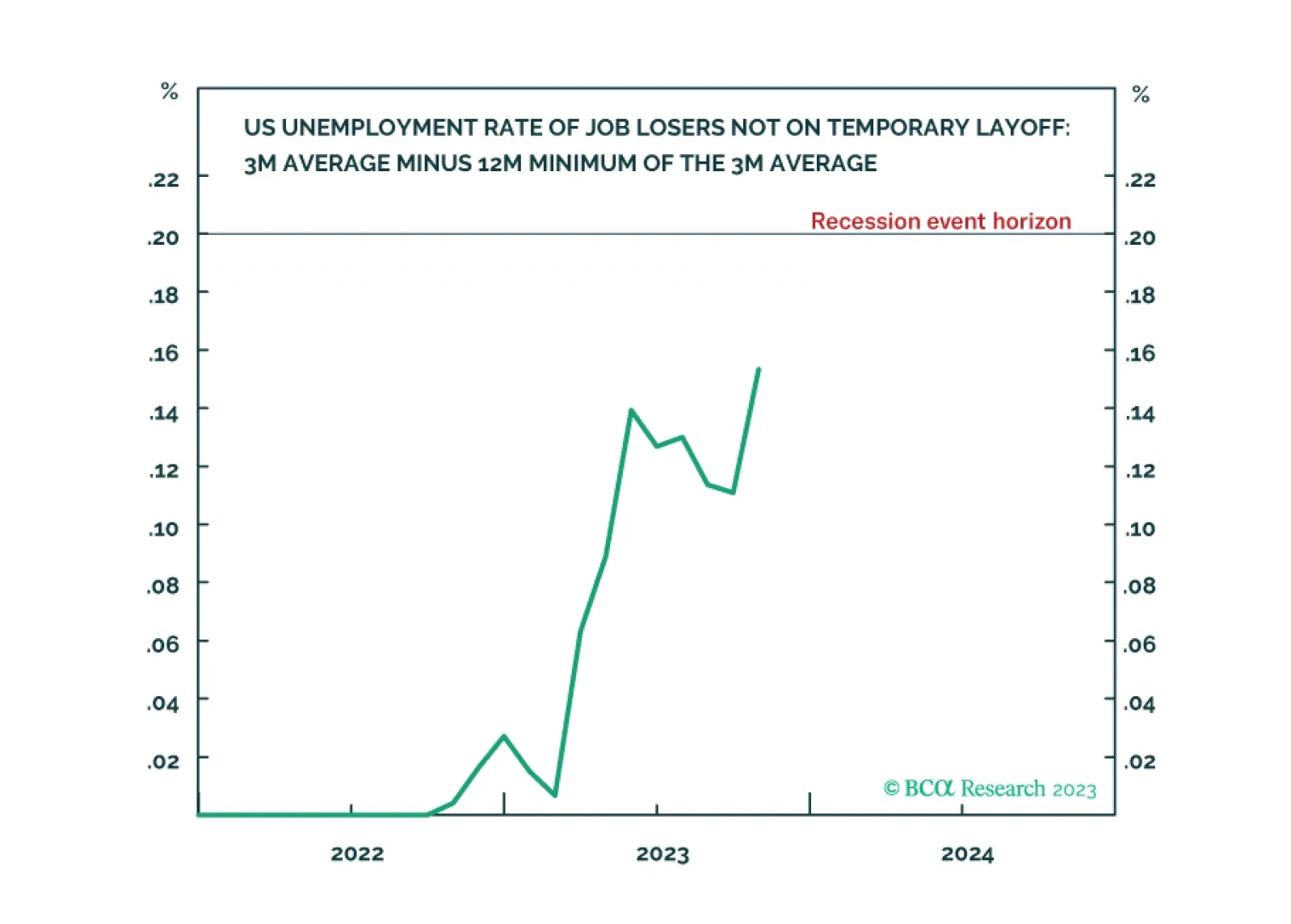

Following the October US jobs data, the ‘Joshi rule’ real-time US recession indicator increased from 0.11 to 0.15, meaning that it is fast approaching its event horizon of 0.20. We go through the investment implications. We also highlight a new long-term recommendation. Plus, the Norwegian krone is close to a potential rebound.