Financial Markets

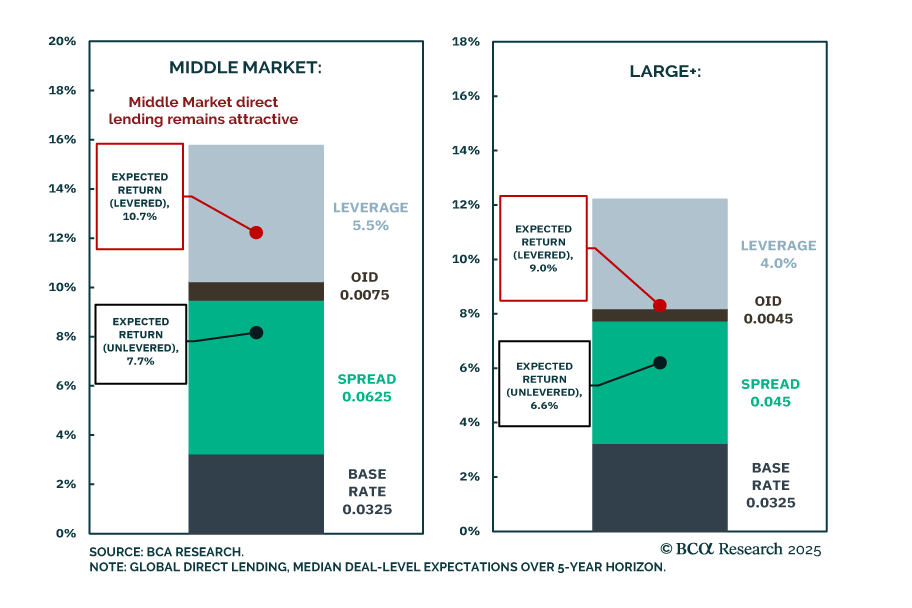

Our PMA strategists published Part 2 of their Capital Market Assumptions update, focusing on Direct Lending. They project gross annualized returns of 7.7% unlevered and 10.7% levered for Global Middle Market Direct Lending, and 6.5% and 8.7% respectively for…

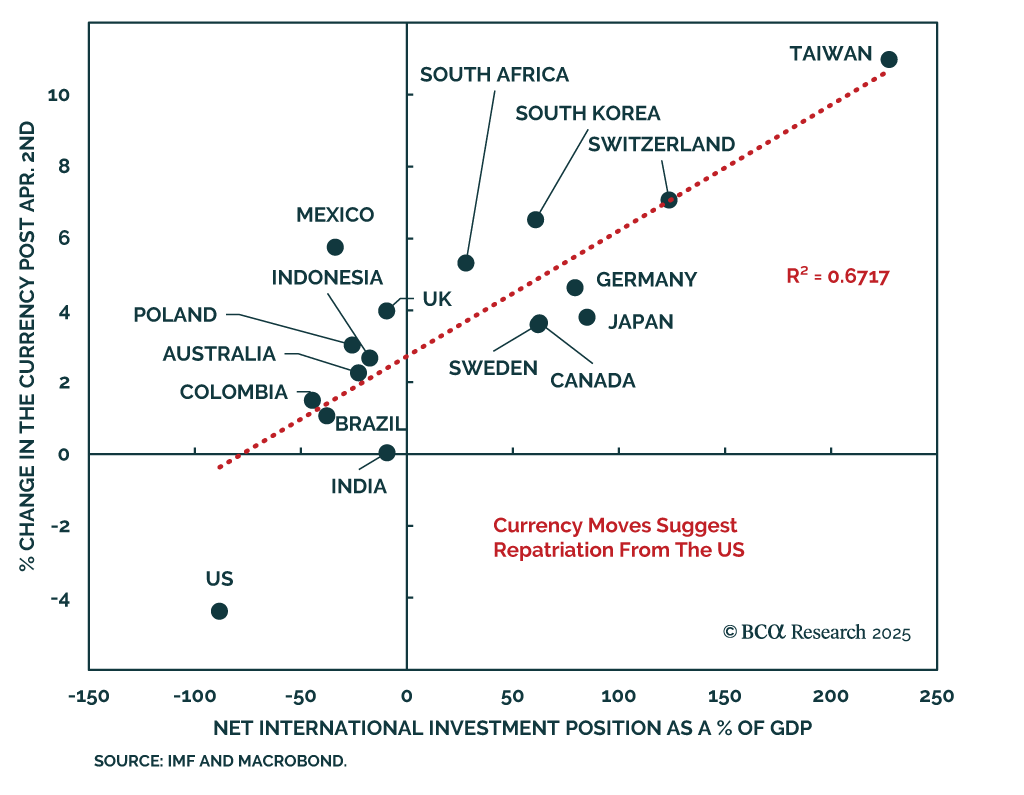

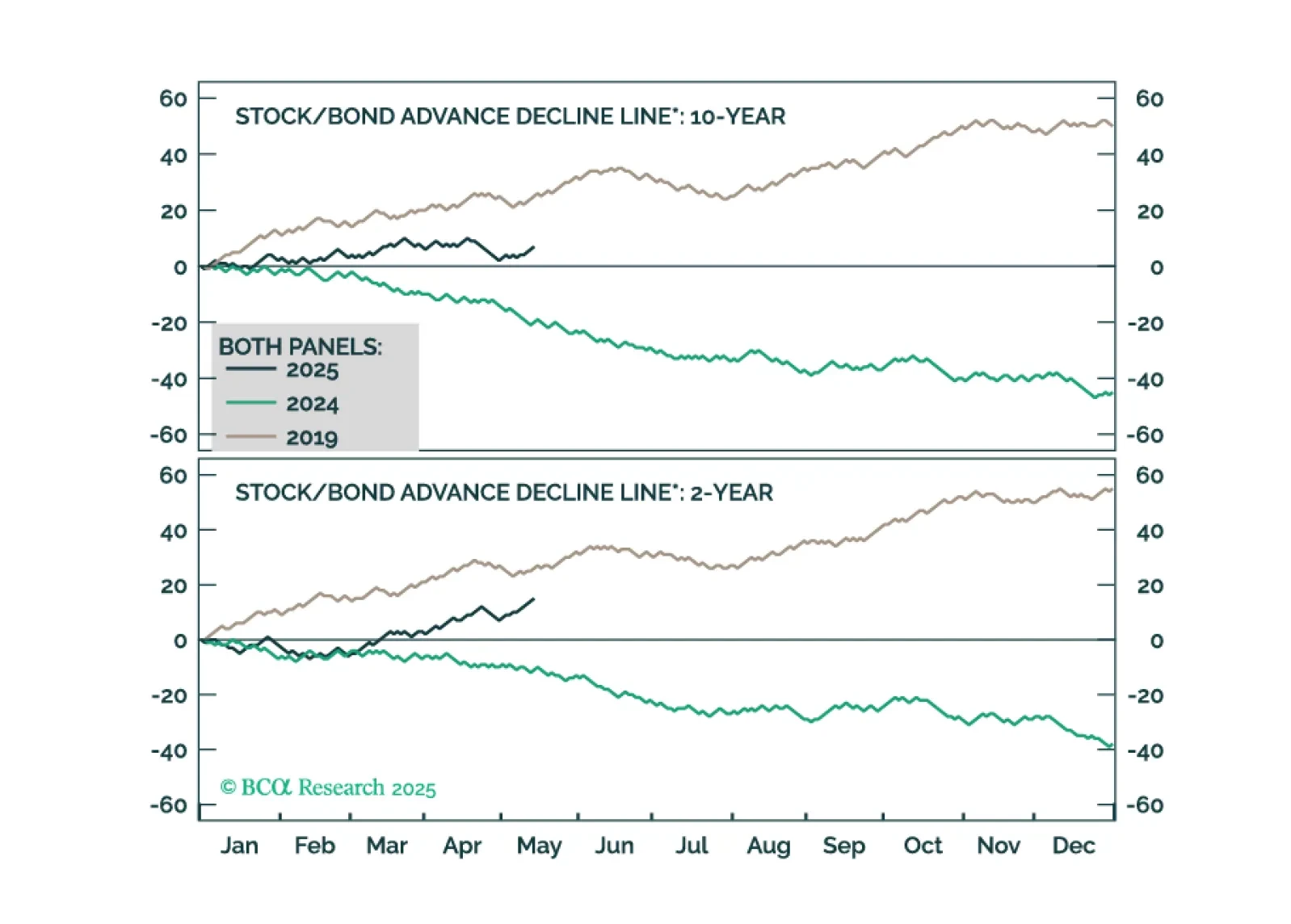

Our Global Asset Allocation strategists remain underweight US equities and the dollar, as fiscal policy overtakes tariffs as the key market driver. The “One Big Beautiful Bill” may avoid worst-case scenarios, but rising US yields are already weighing on…

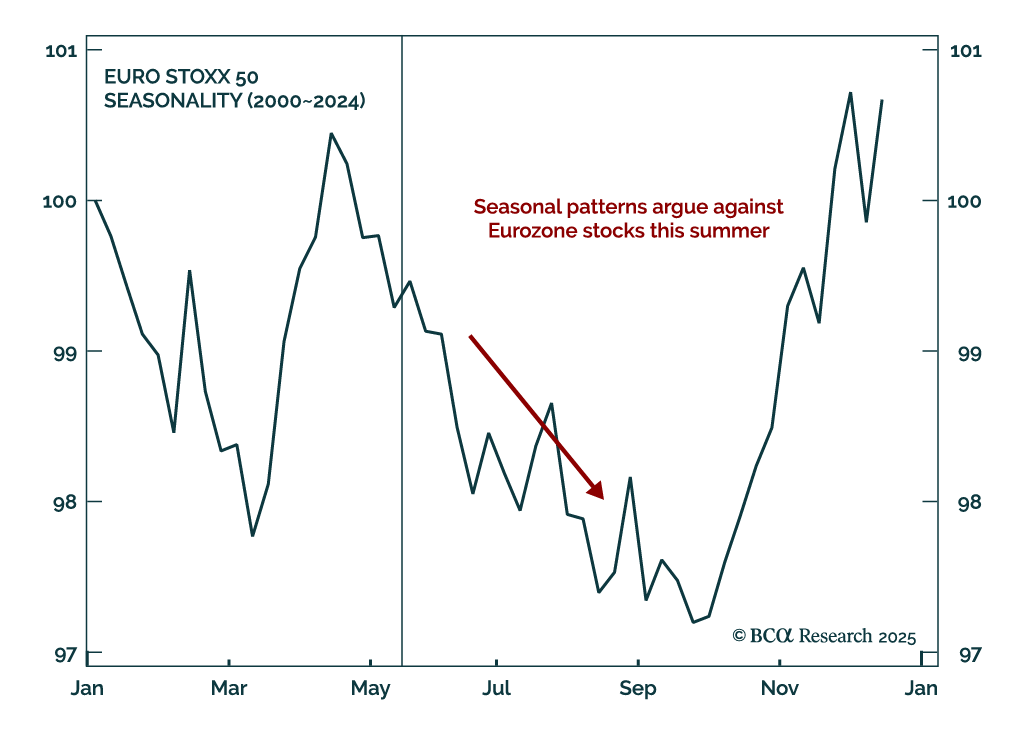

Our European strategists expect the EURO STOXX 50 to remain rangebound between 4750 and 5500 this summer, creating a punishing environment for buy-and-hold investors. With the index near the top of its range, they recommend trimming outright exposure and…

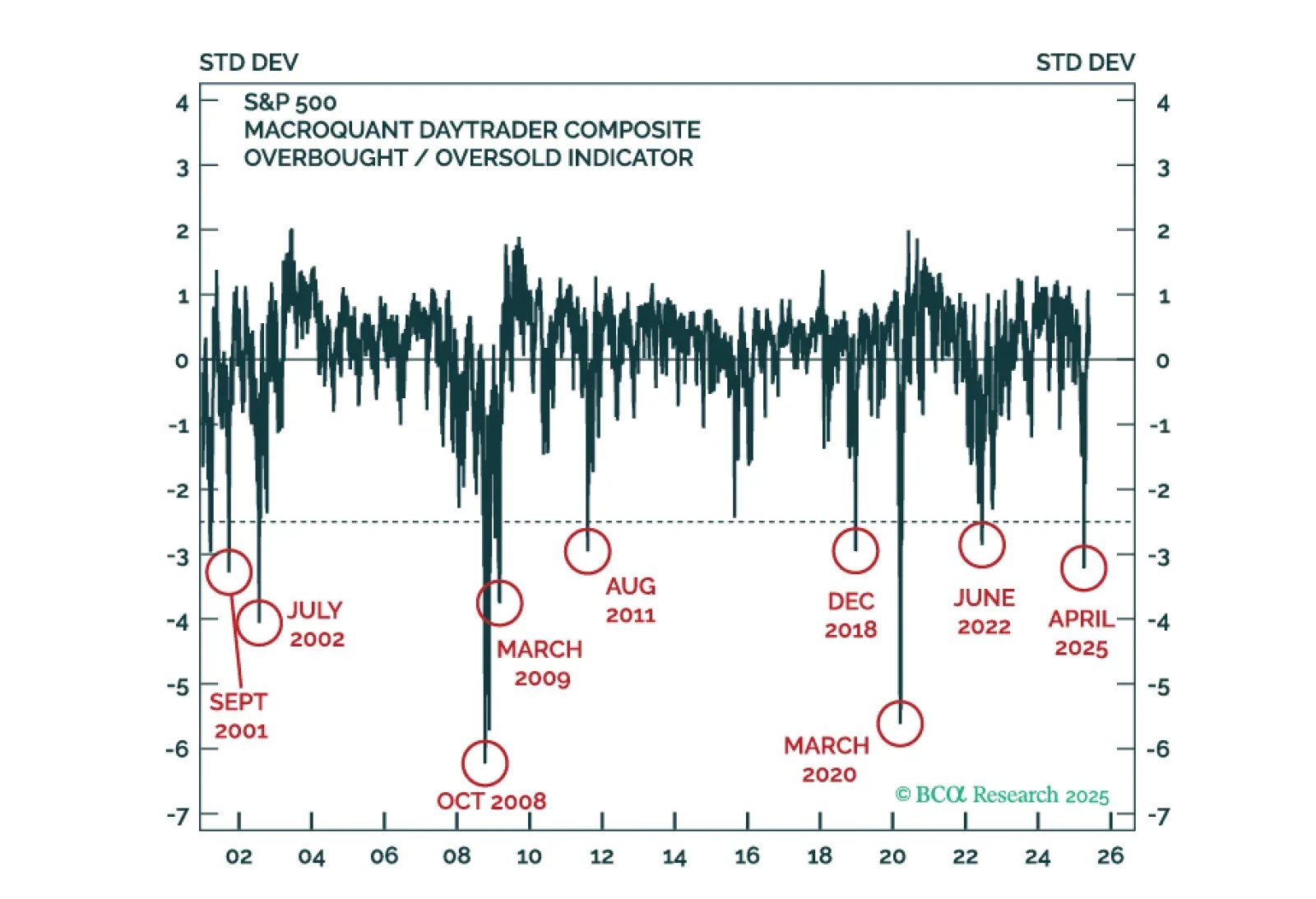

MacroQuant warns that US equities are pricing in very little economic risk. The model is shunning equities and recommends a large overweight to cash.

MacroQuant warns that US equities are pricing in very little economic risk. The model is shunning equities and recommends a large overweight to cash.

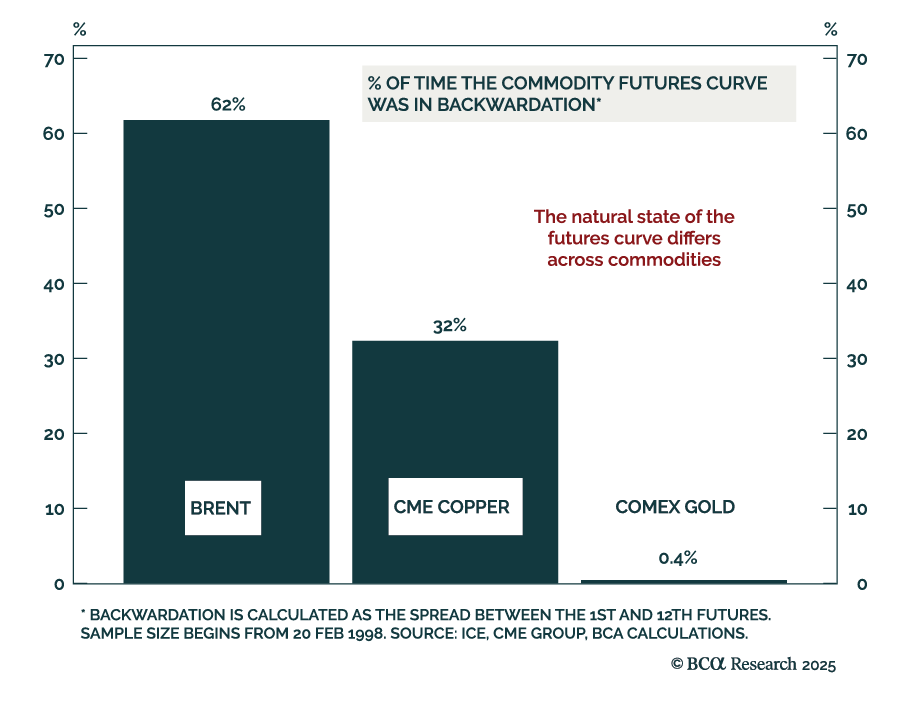

Oil, copper, and gold futures curves have experienced abnormal changes in the past few months, but a bearish global outlook will steepen contango structures across all three. Oil’s curve structure has flipped from backwardation (higher short-term than…

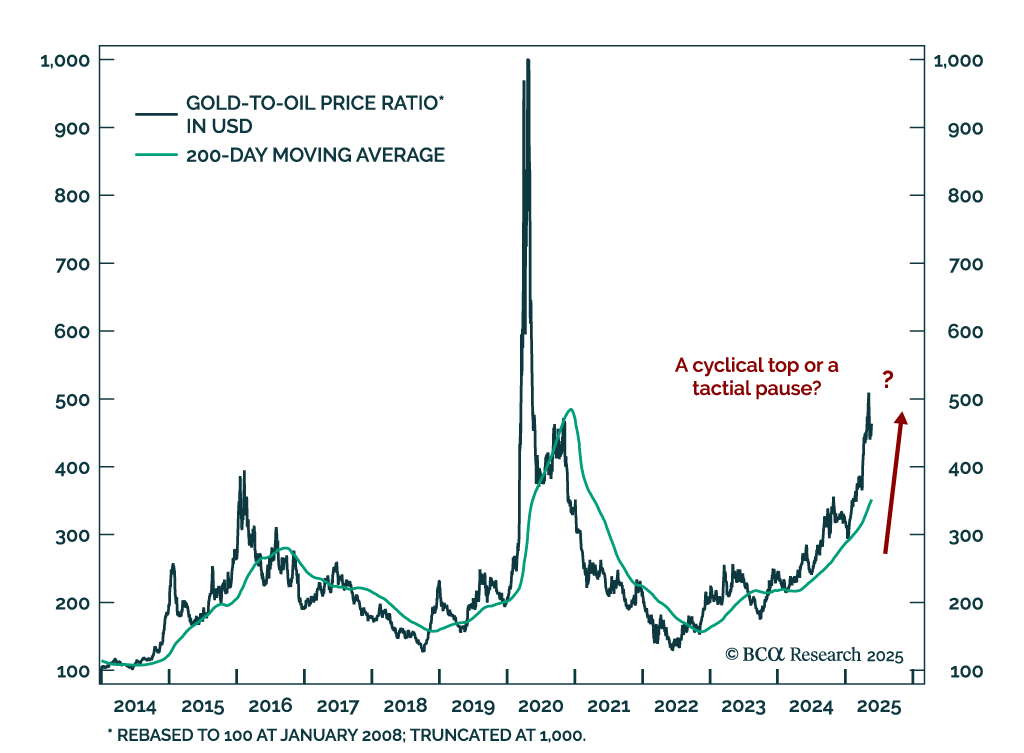

The gold-to-oil price ratio seems tactically overextended, but global macro drivers suggest it will rise further. The gold bull run is still relatively young and not yet stretched compared to rallies from the past 50 years. Importantly, ongoing…

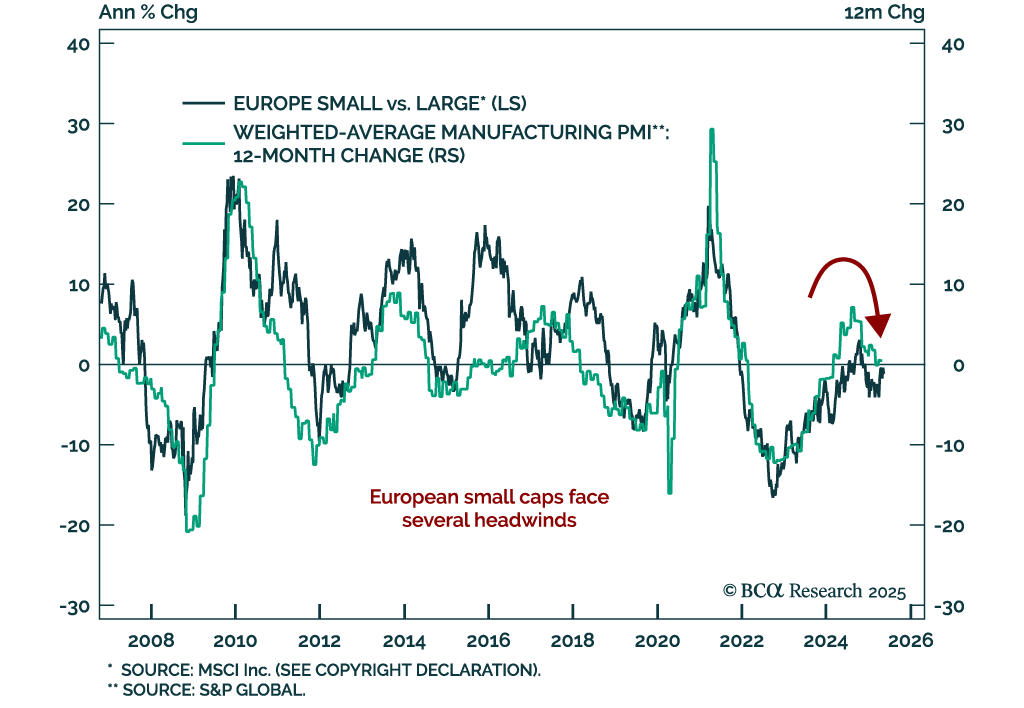

The outperformance of European small caps is coming to an end. Our Chart Of The Week comes from our European Investment Strategy team.The team identifies several headwinds for small caps in Europe in the near term. Small caps’ performance is primarily…

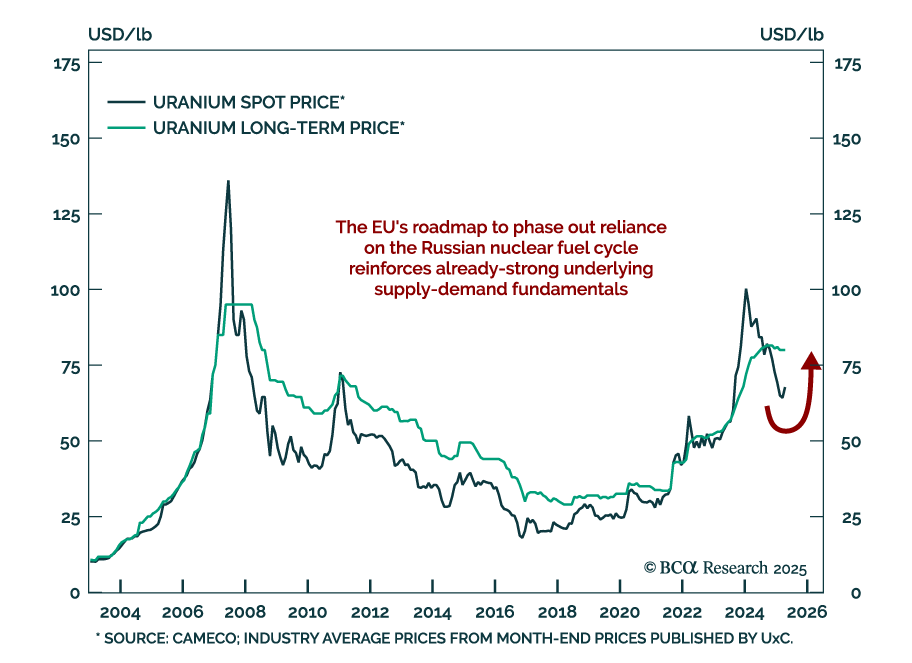

Uranium spot prices may have found a floor after falling to $64/lb from a $107/lb peak in February last year. This drawdown has been unexpected considering the strength of the underlying supply-demand fundamentals for uranium. The momentum remains…

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.