Fixed Income

Jay Powell won’t be removed as Fed Chair before the expiry of his term next May, but we will learn the identity of his replacement this year, setting up a potentially awkward “shadow Fed Chair” situation.

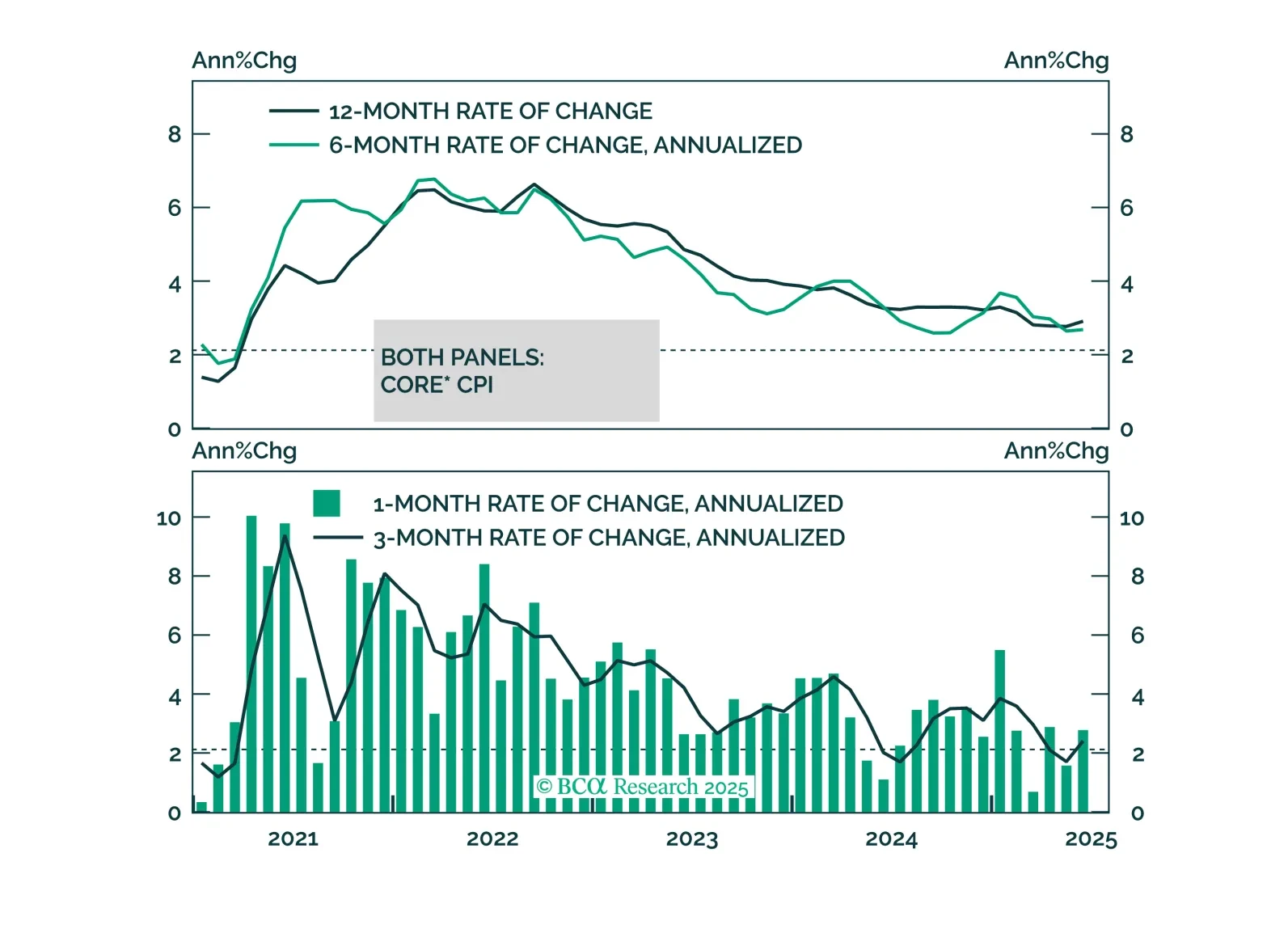

We discuss the implications of this morning’s CPI report and the relative attractiveness of 2/5 Treasury curve steepeners.

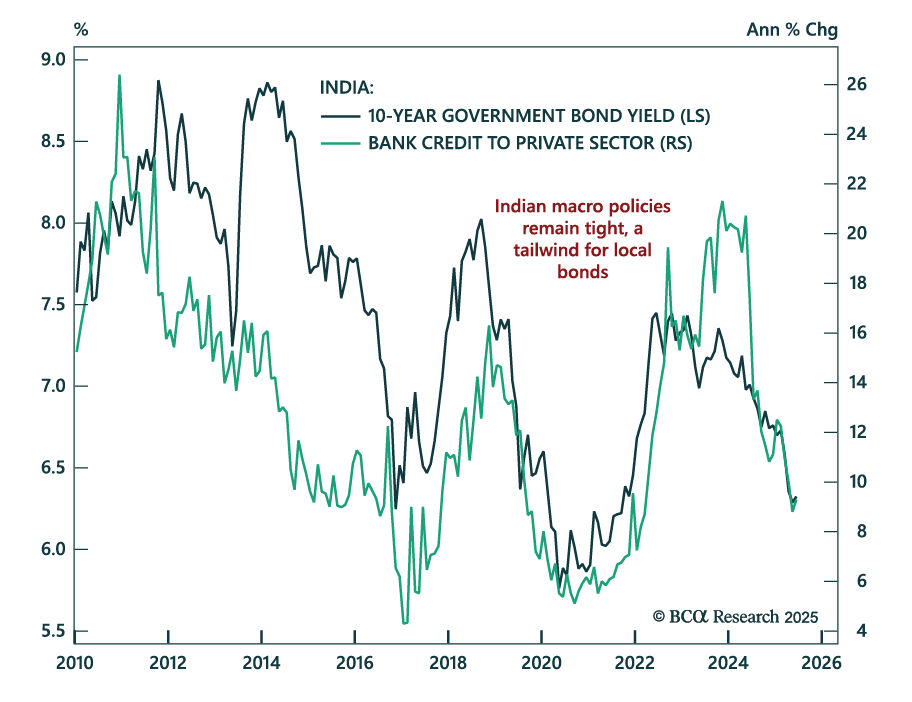

With inflation at a six-year low and restrictive policy weighing on growth, our EM strategists remain long Indian bonds and underweight equities. Headline CPI fell to 2.1% y/y, largely driven by lower food prices, bringing inflation to the lower bound of the…

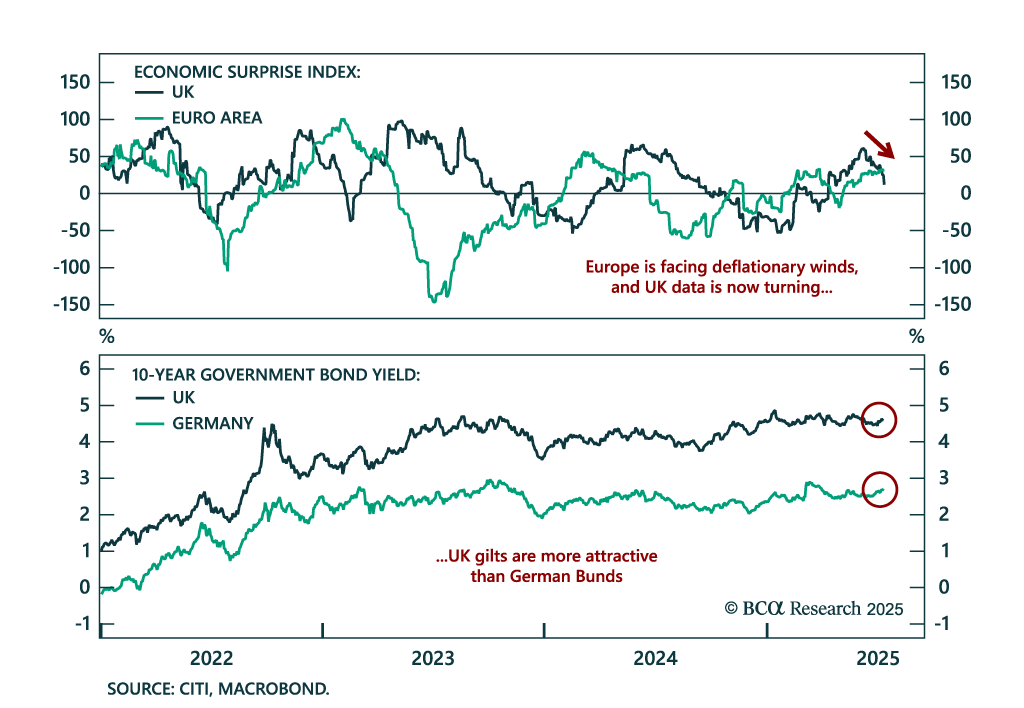

UK growth data continues to disappoint, making the case for a Gilts overweight and a dovish BoE. May GDP fell 0.1% m/m, missing estimates and marking a consecutive monthly contraction after April’s 0.3% decline. Industrial and manufacturing output both…

Our Portfolio Allocation Summary for July 2025.

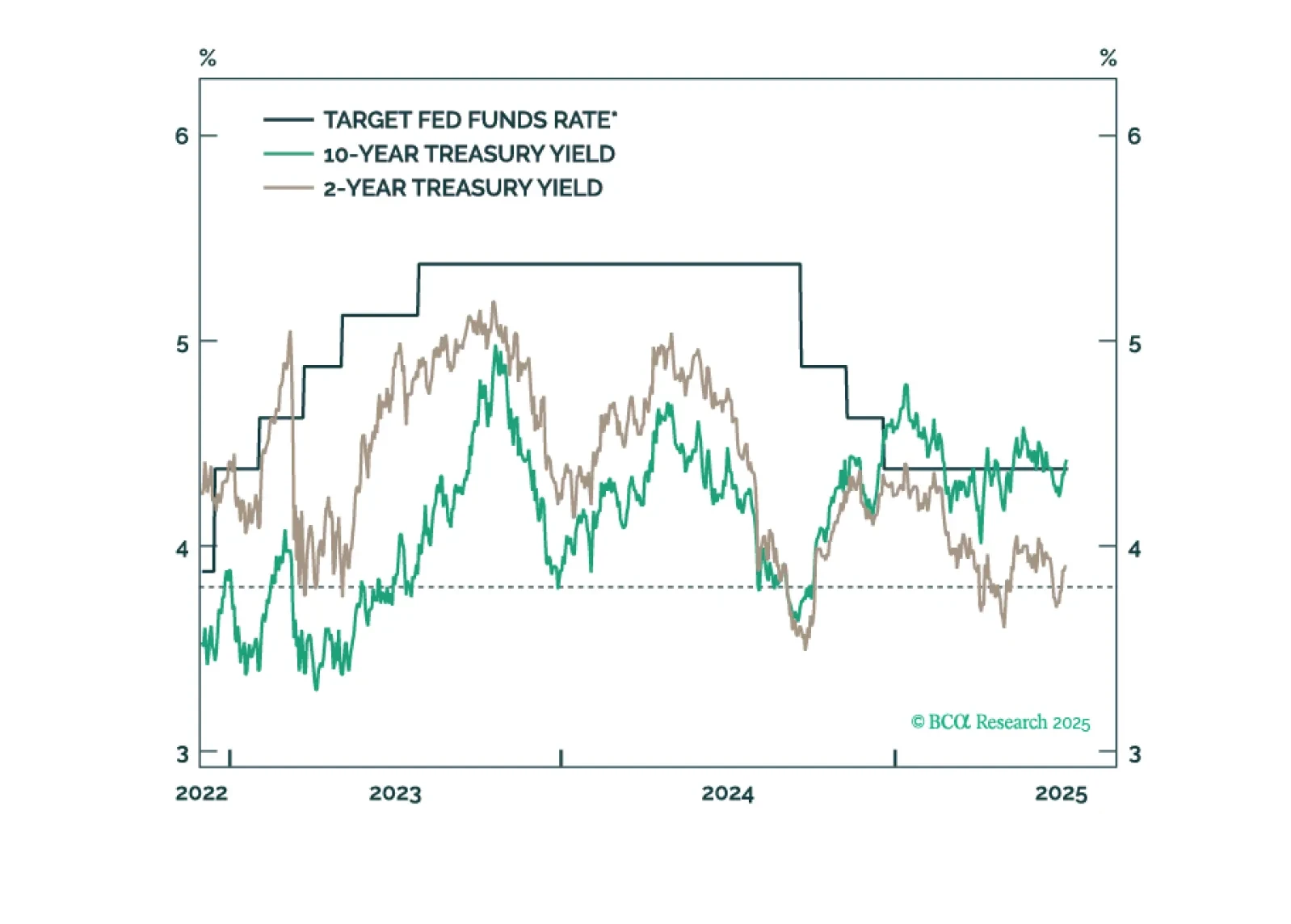

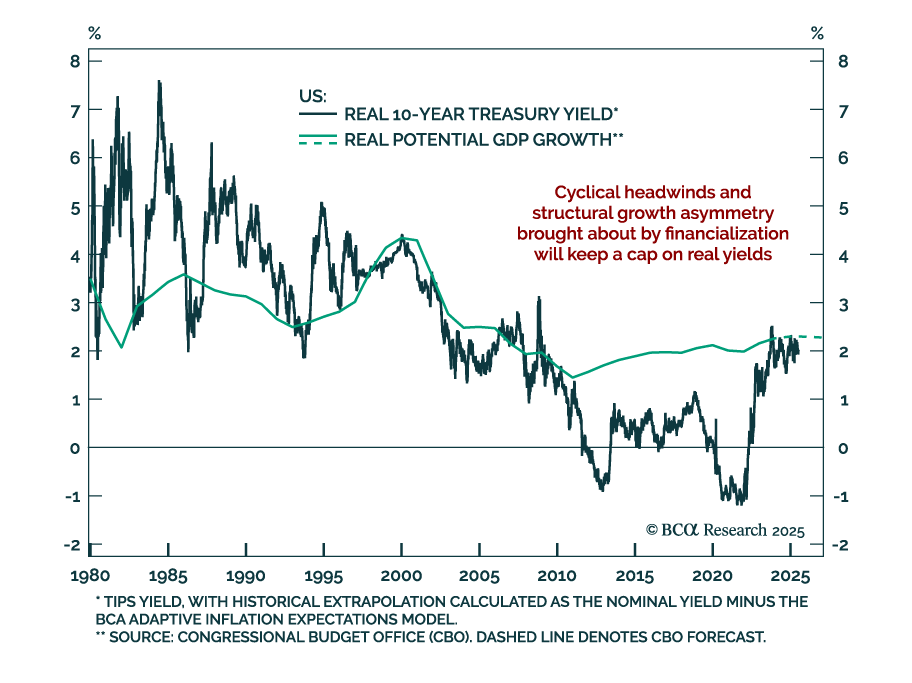

Real yields remain near 2%, but structural asymmetries justify a duration overweight as inflation expectations stay anchored. US 10-year yields have been volatile, testing 4.80% in January and dropping below 4.0% after April’s Liberation Day. Meanwhile,…

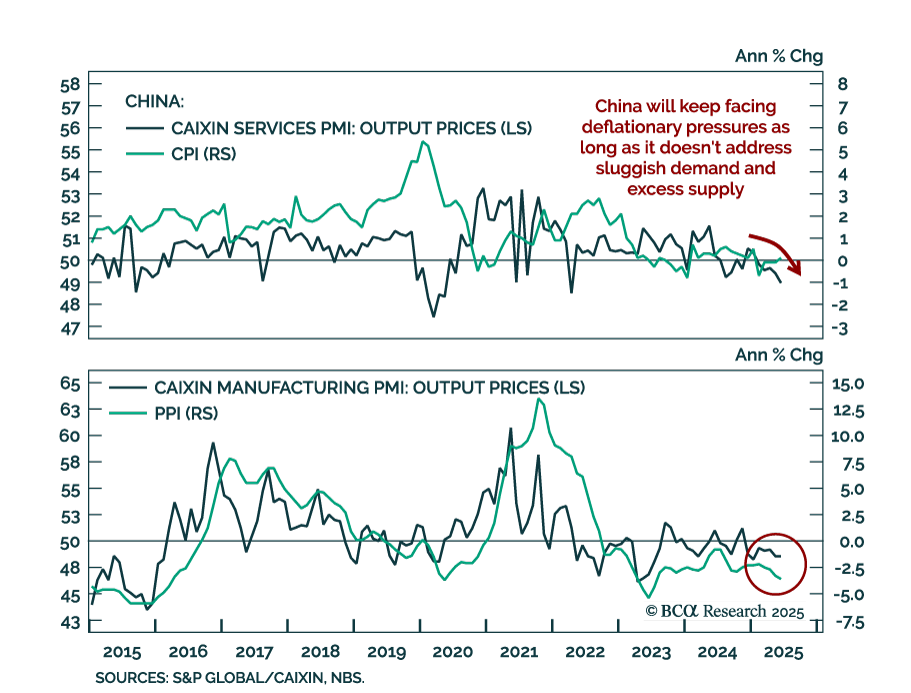

Persistent deflation and constrained policy options support a defensive stance on China, favoring bonds and high-dividend equities. Consumer prices were roughly flat in June, rising just 0.1% y/y after a 0.1% decline in May. Producer prices fell 3.6%,…

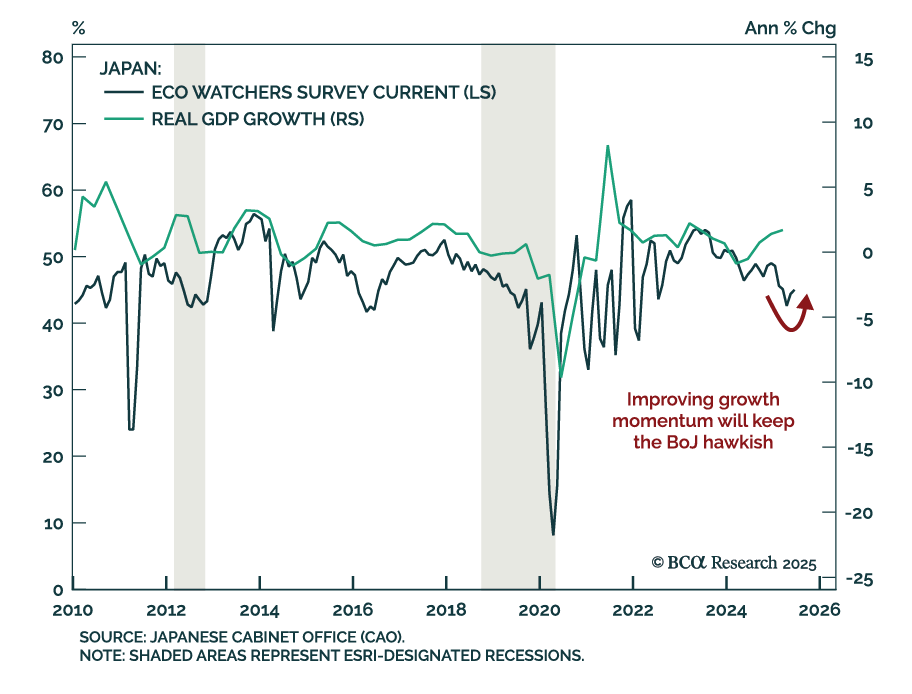

Japan’s improving growth momentum and structural inflation shift support an underweight in JGBs and long JPY positioning. The June Eco Watchers Survey was broadly in line with expectations, with current conditions ticking up to 45.0 and expectations modestly…

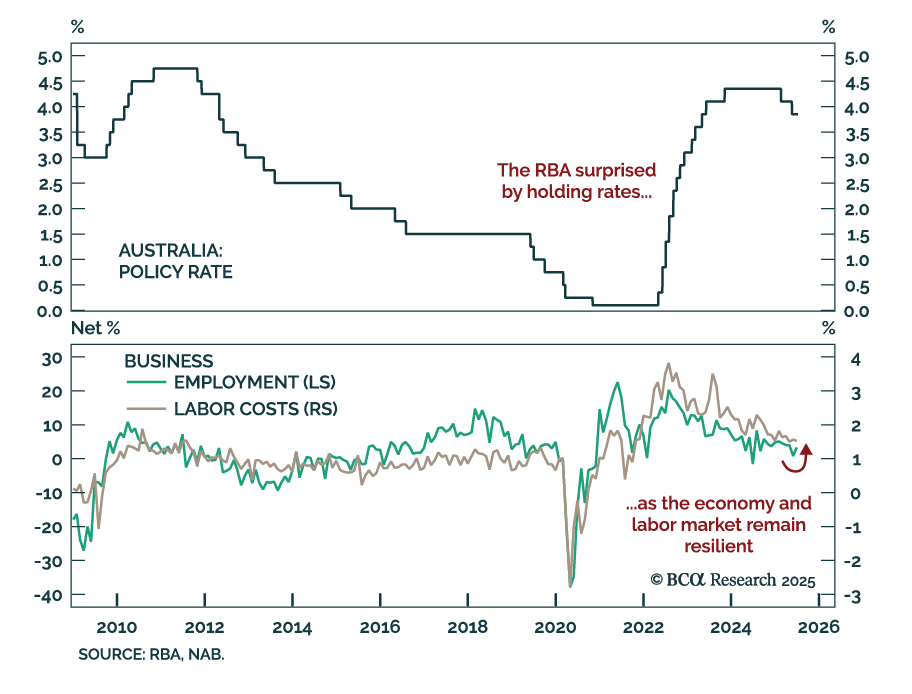

The RBA’s surprise hold reinforces a slower easing path, warranting an underweight on Australian bonds. Markets had priced in a 25 bps cut, but the central bank opted to keep rates at 3.85%. Governor Bullock characterized the decision as a matter of timing,…

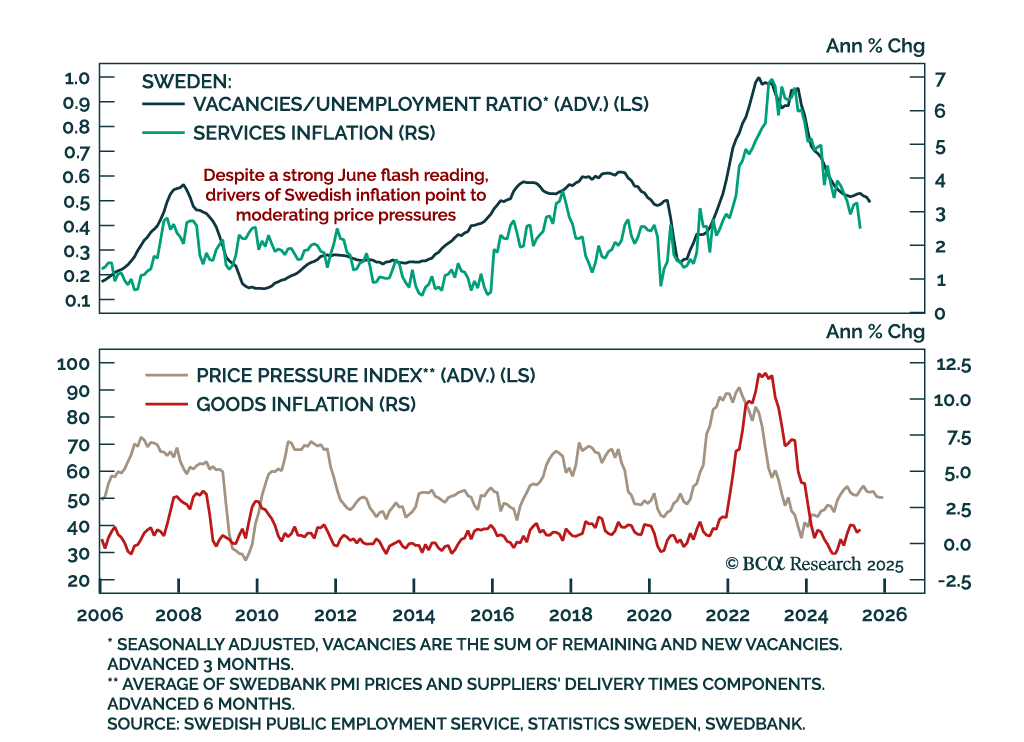

Stronger-than-expected June inflation will likely keep the Riksbank on hold in August, despite soft underlying trends. Headline inflation accelerated more than expected to 0.5% m/m (0.8% y/y), while CPI ex-housing rose to 2.9% y/y and core inflation to 3.3%…