Fixed Income

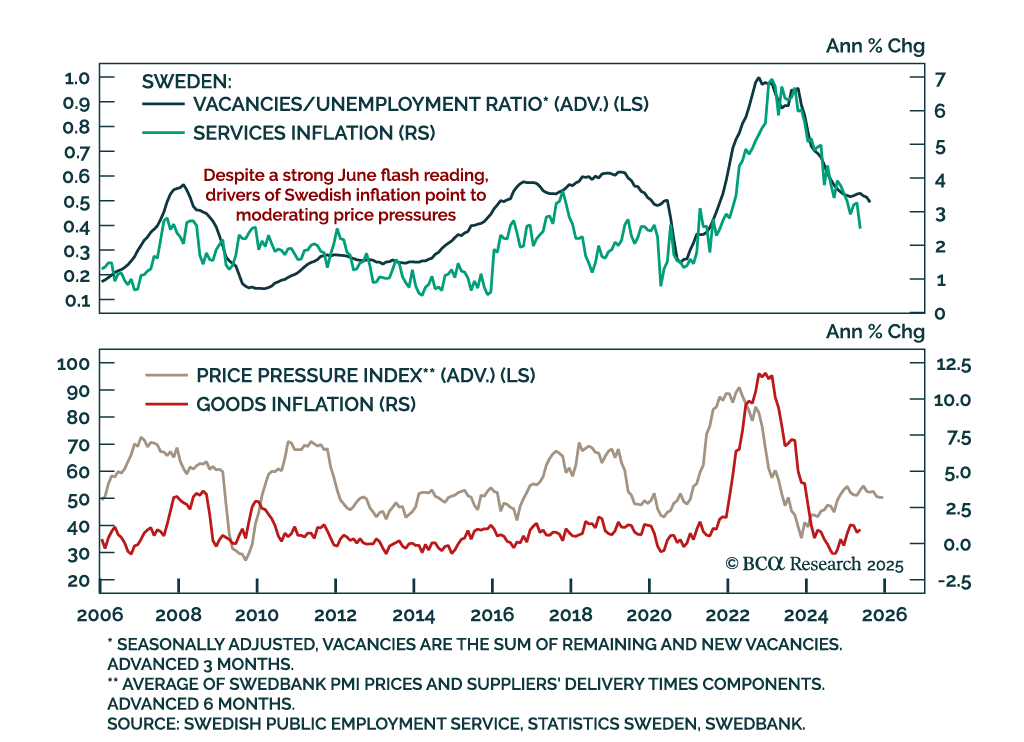

Stronger-than-expected June inflation will likely keep the Riksbank on hold in August, despite soft underlying trends. Headline inflation accelerated more than expected to 0.5% m/m (0.8% y/y), while CPI ex-housing rose to 2.9% y/y and core inflation to 3.3%…

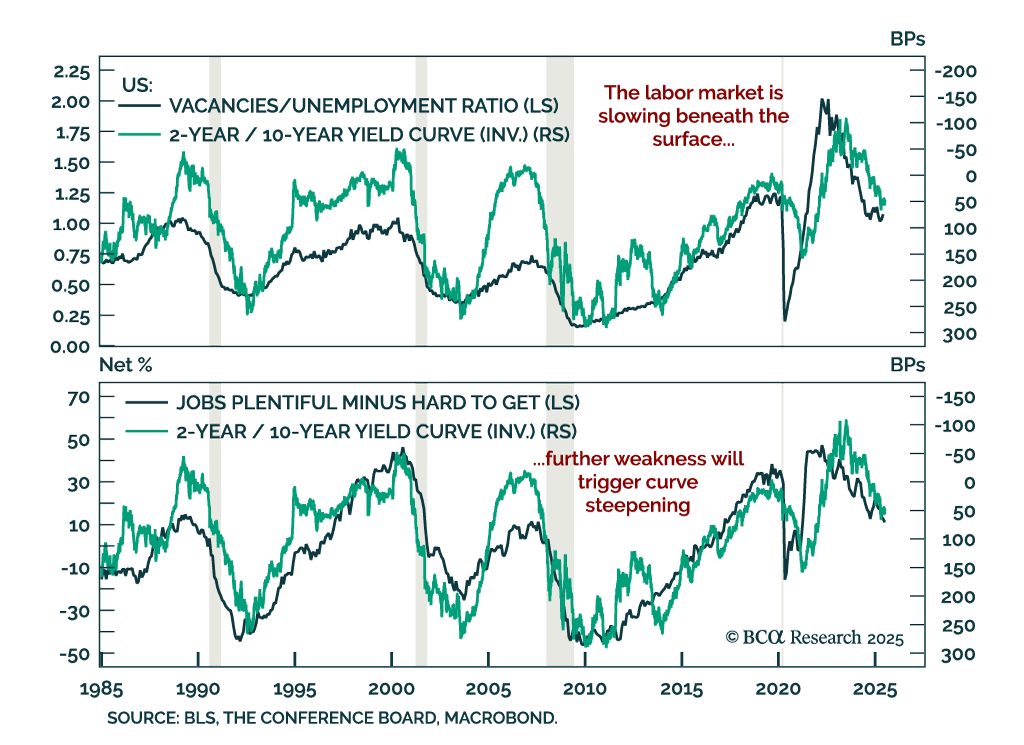

Labor market cracks reinforce long duration and steepener positioning as growth risks mount. Job market data has looked strong on the surface, but the details of the June employment and JOLTS reports confirm a slowing trend within the “low hiring, low firing”…

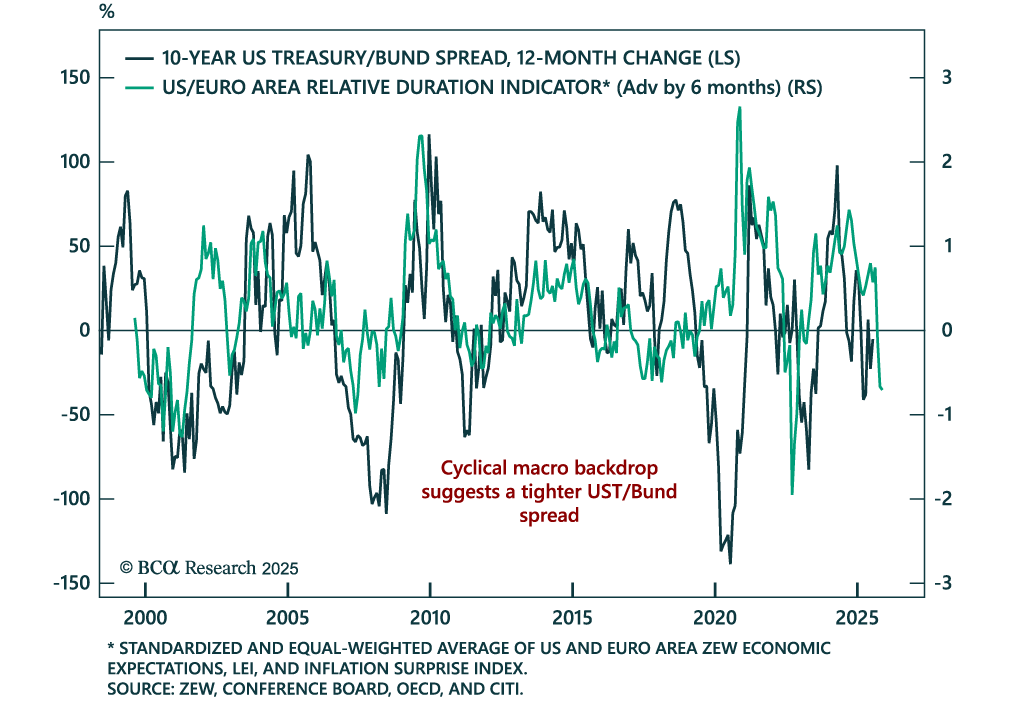

Relative growth and inflation trends point to a narrower UST/Bund spread. Our Chart Of The Week comes from Robert Timper, Global Fixed Income Strategist. This week, our rates strategists introduced a new US/Euro Area Relative Duration Indicator, designed to…

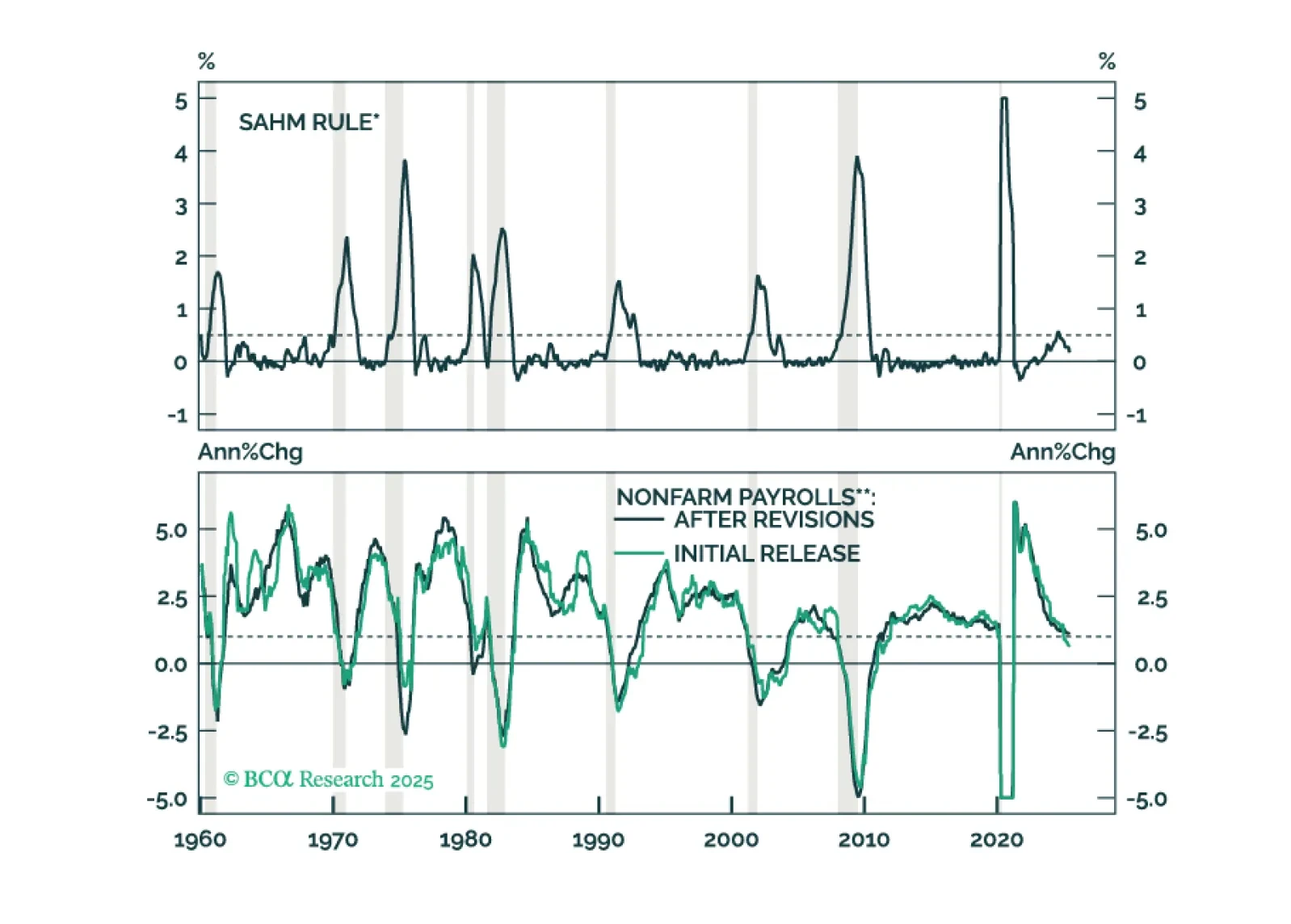

June’s employment report showed a tick down in the unemployment rate, an improvement that rules out a Fed rate cut later this month.

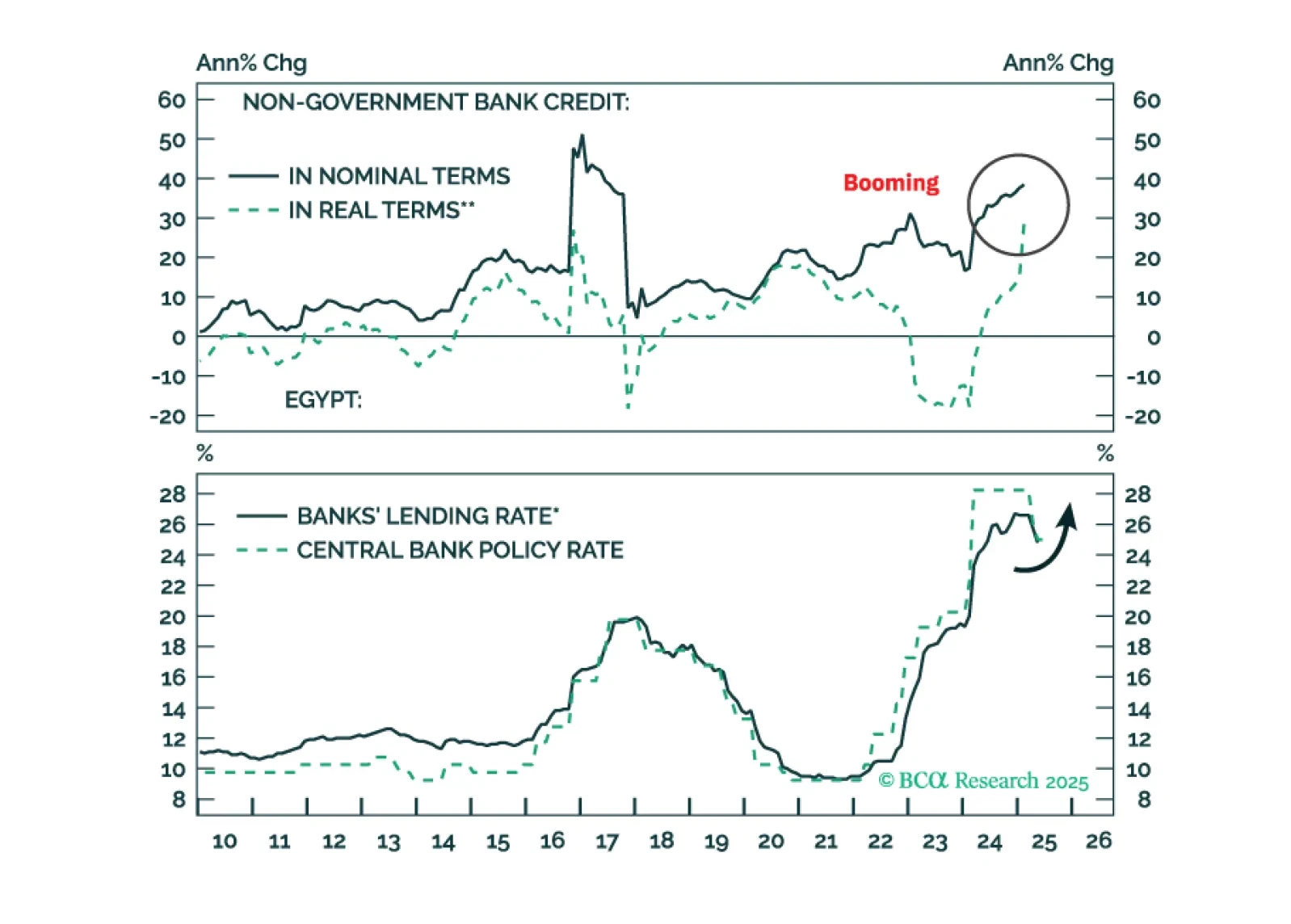

Downward pressure on the pound will rise in the coming months. Inflation will go up, so will bond yields. It’s time to book profits on Egyptian domestic bonds.

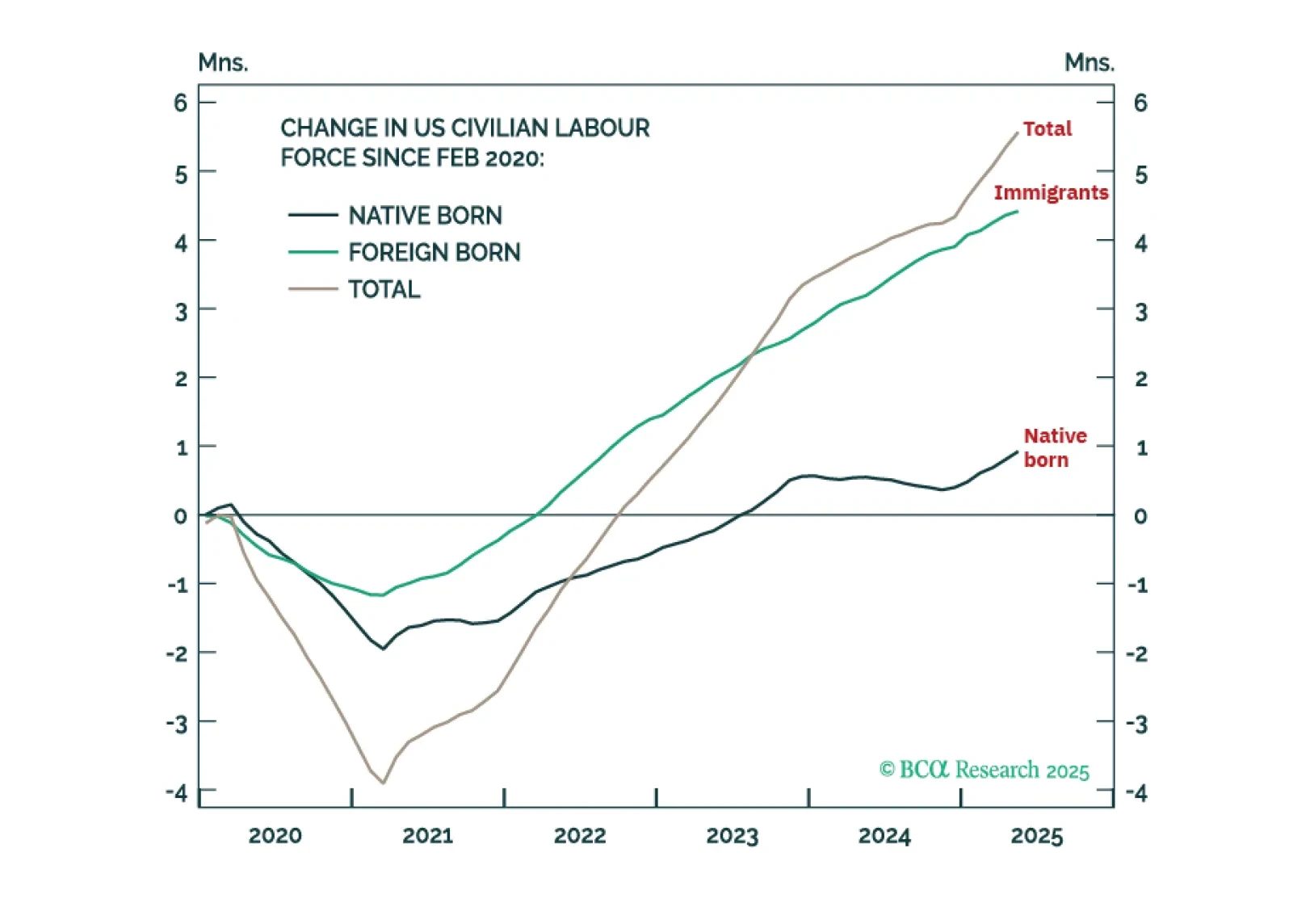

Trump’s immigration policies are protecting the US economy from a sharp rise in unemployment but steering it into a ‘mini stagflation’. Plus: a new tactical trade is to underweight global technology (IXN).

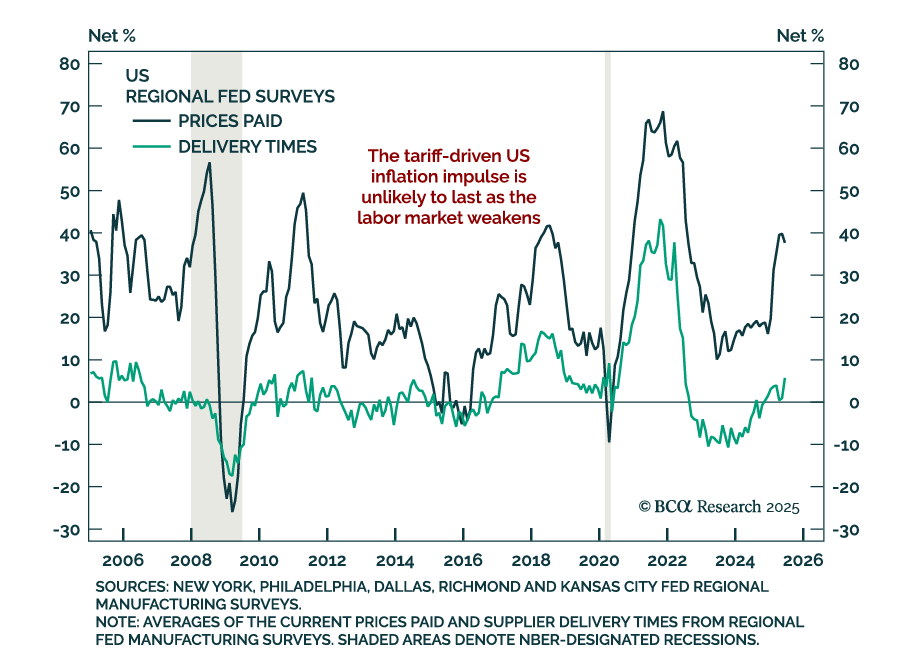

Regional Fed surveys confirm sluggish US manufacturing and tame inflation, supporting long duration positioning outside the US. The June Dallas Fed Manufacturing survey missed expectations, rising to -12.7 from -15.3, still deep in contraction. New orders…

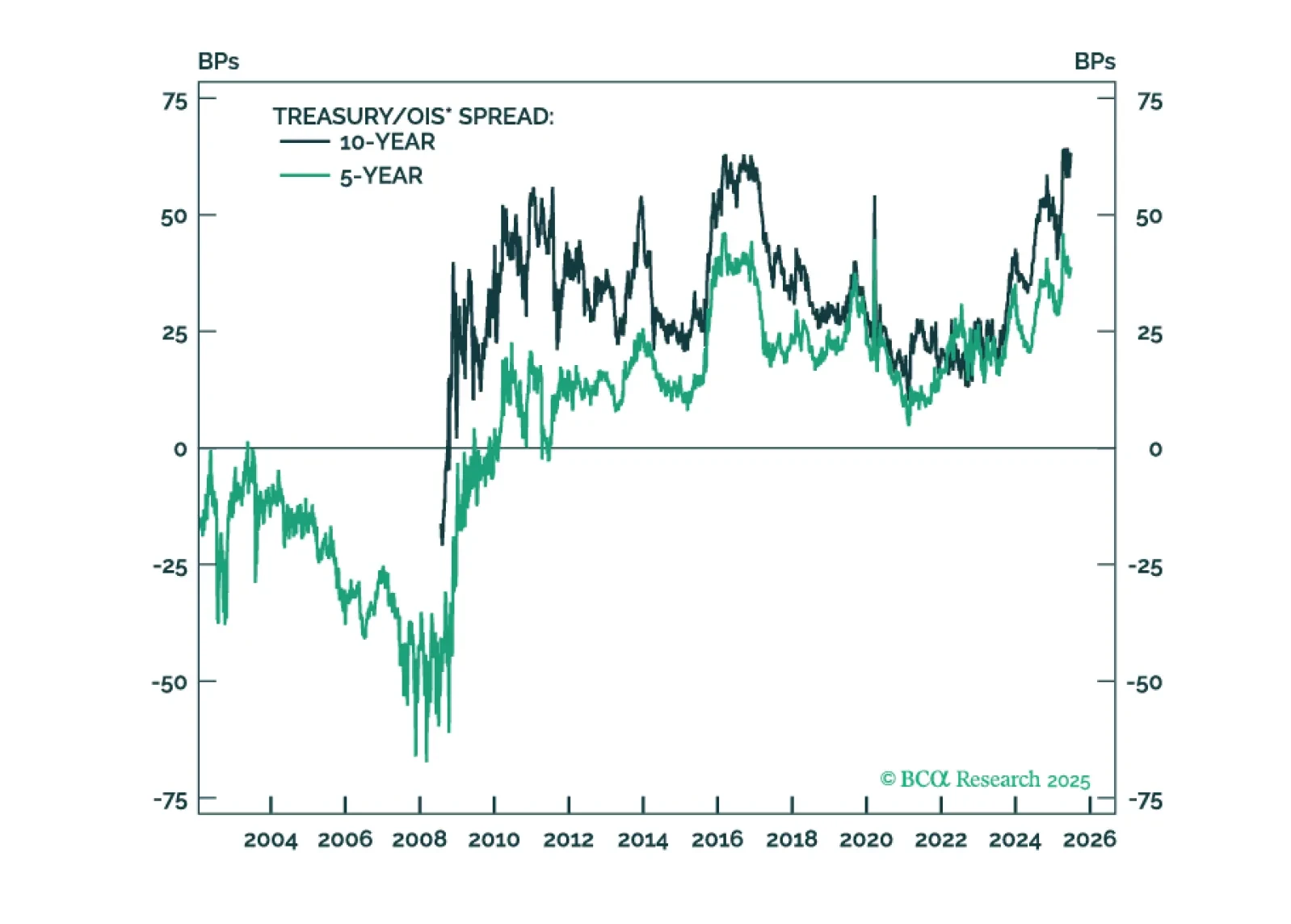

Our US Bond strategists expect a modest narrowing of the Treasury/OIS spread, supporting a cyclical long-duration stance and 2s10s steepeners. Over the past year, the spread has added roughly 30 bps to the 10-year Treasury yield, driven by factors such as…

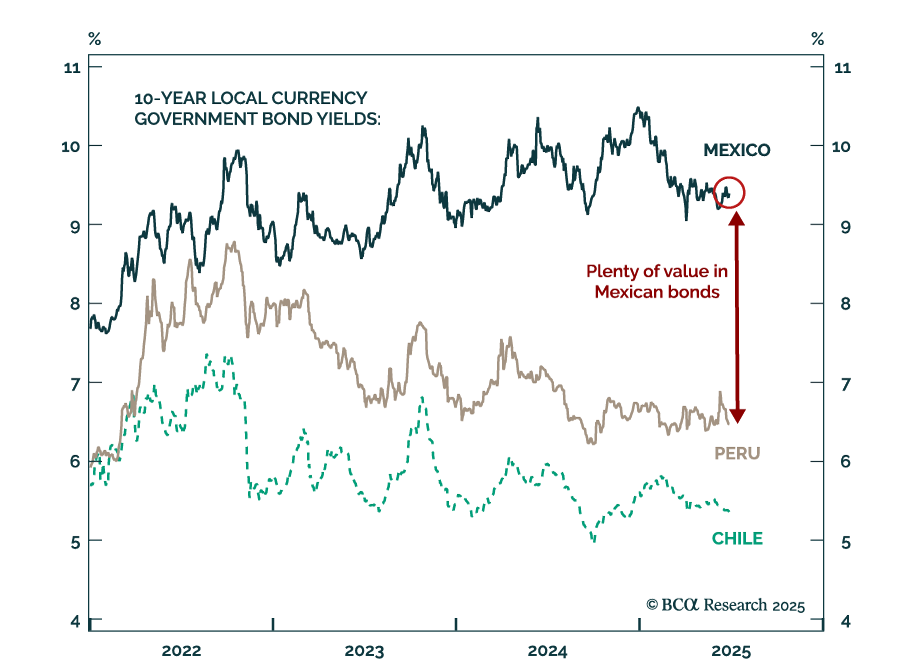

Banxico’s dovish stance reinforces our bullish view on Mexican local currency debt. The Mexican central bank cut interest rates by another 50 basis points to 8%. The central bank will continue easing monetary policy well into next year. Slower US…

The Treasury/OIS spread has exerted notable upward pressure on Treasury yields during the past year, but the factors driving the spread are now turning more favorable.