Fixed Income

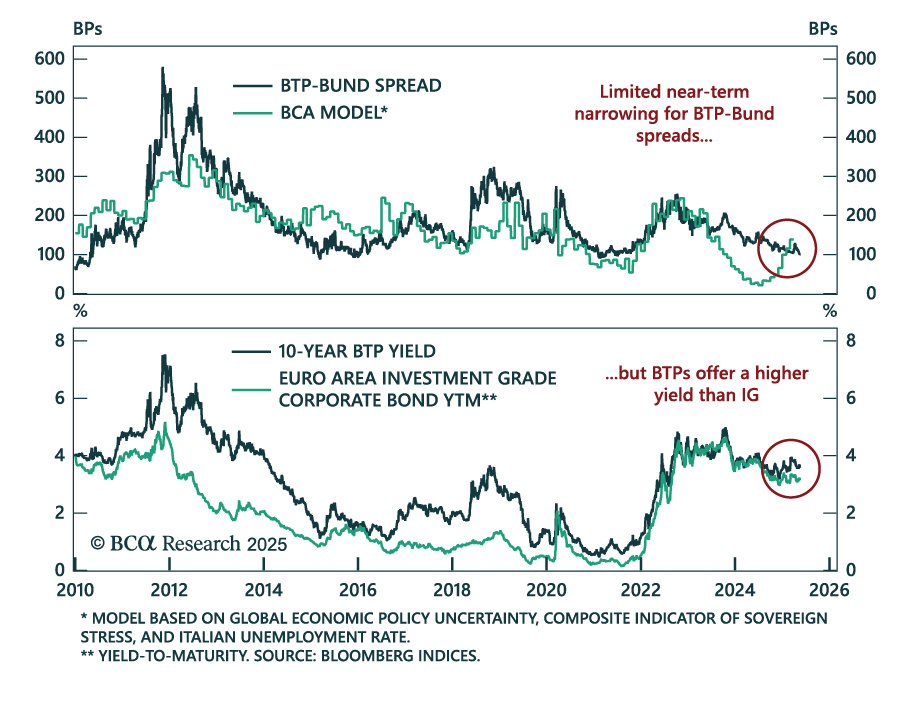

The European bond market is pricing in a more optimistic outlook. The BTP-Bund spreads have narrowed 30bps since April 9 and are now within reach of their pre-Ukraine war level. BCA’s European strategists do not share this optimism, at least not in the…

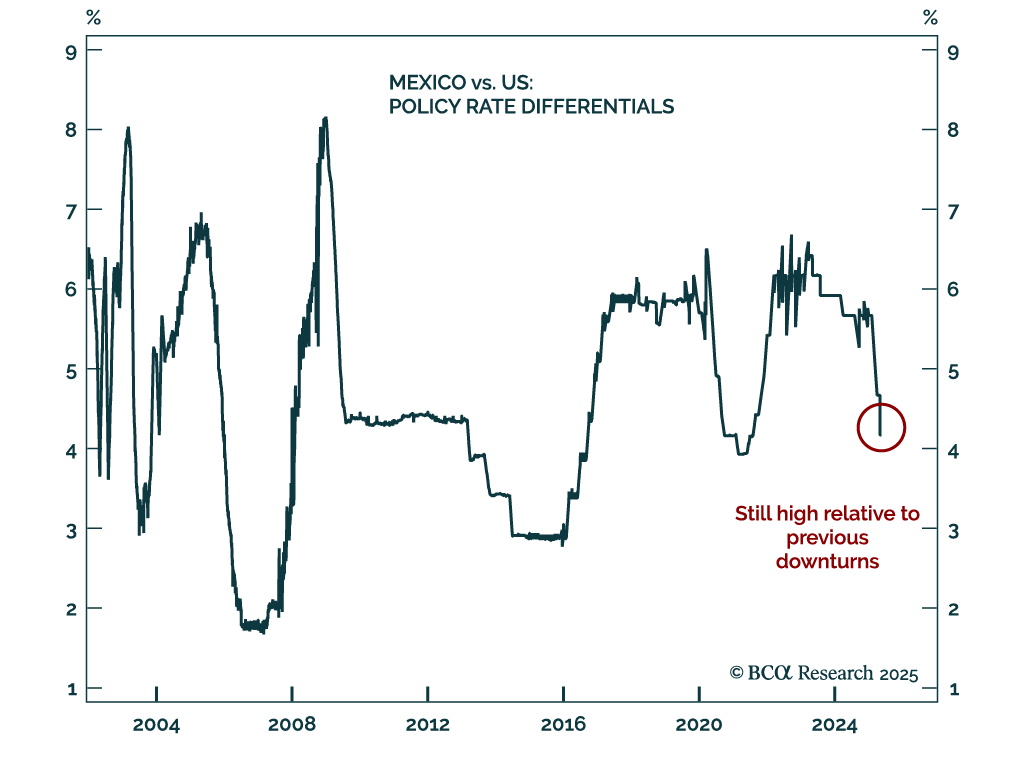

Banxico’s 50 bps rate cut reinforces our bullish view on Mexican bonds, with easing likely to continue as inflation falls and growth slows. The central bank unanimously lowered its policy rate to 8.5%, and we expect further cuts ahead as Mexico heads toward a…

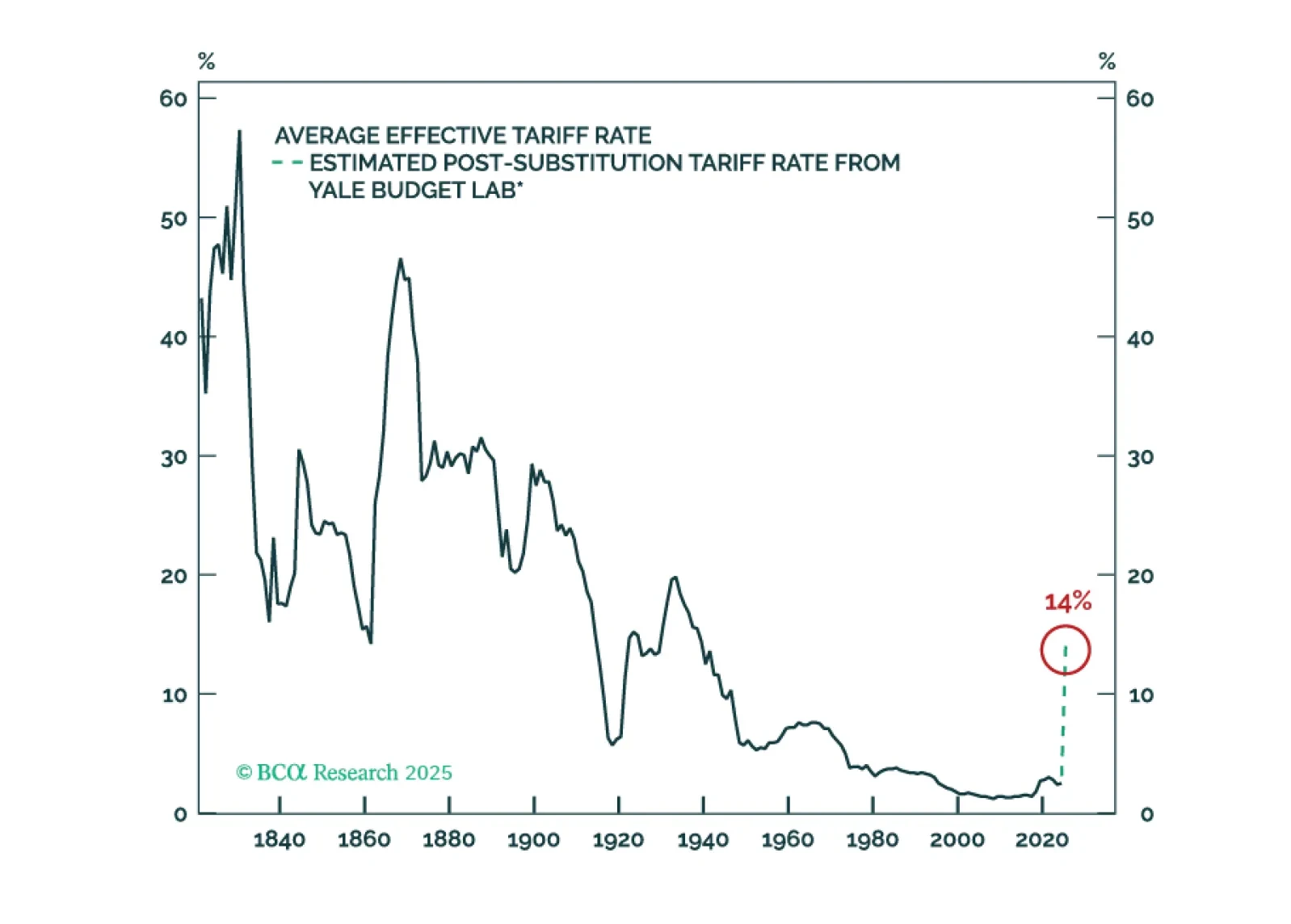

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.

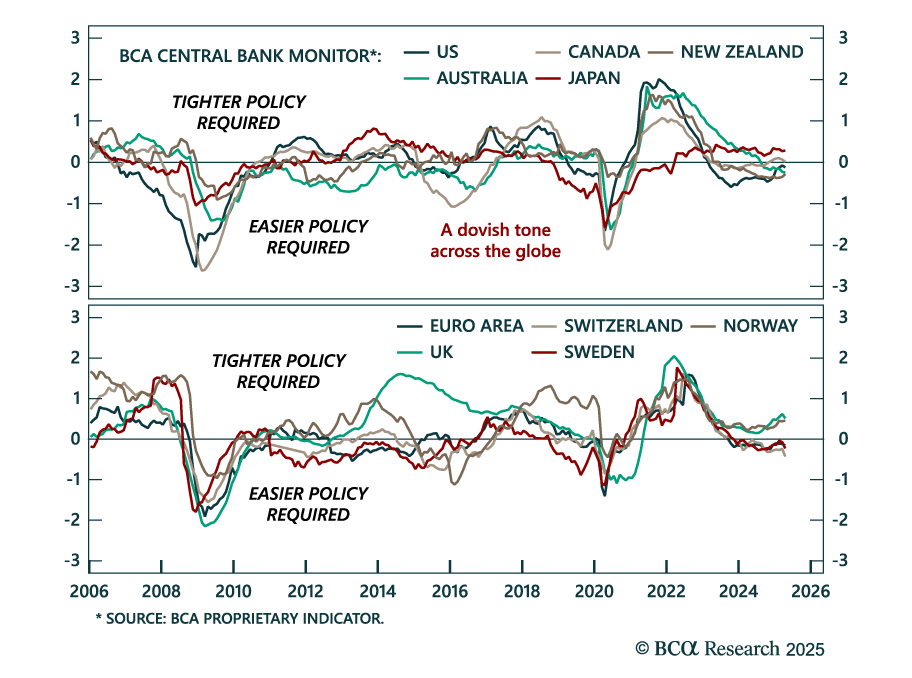

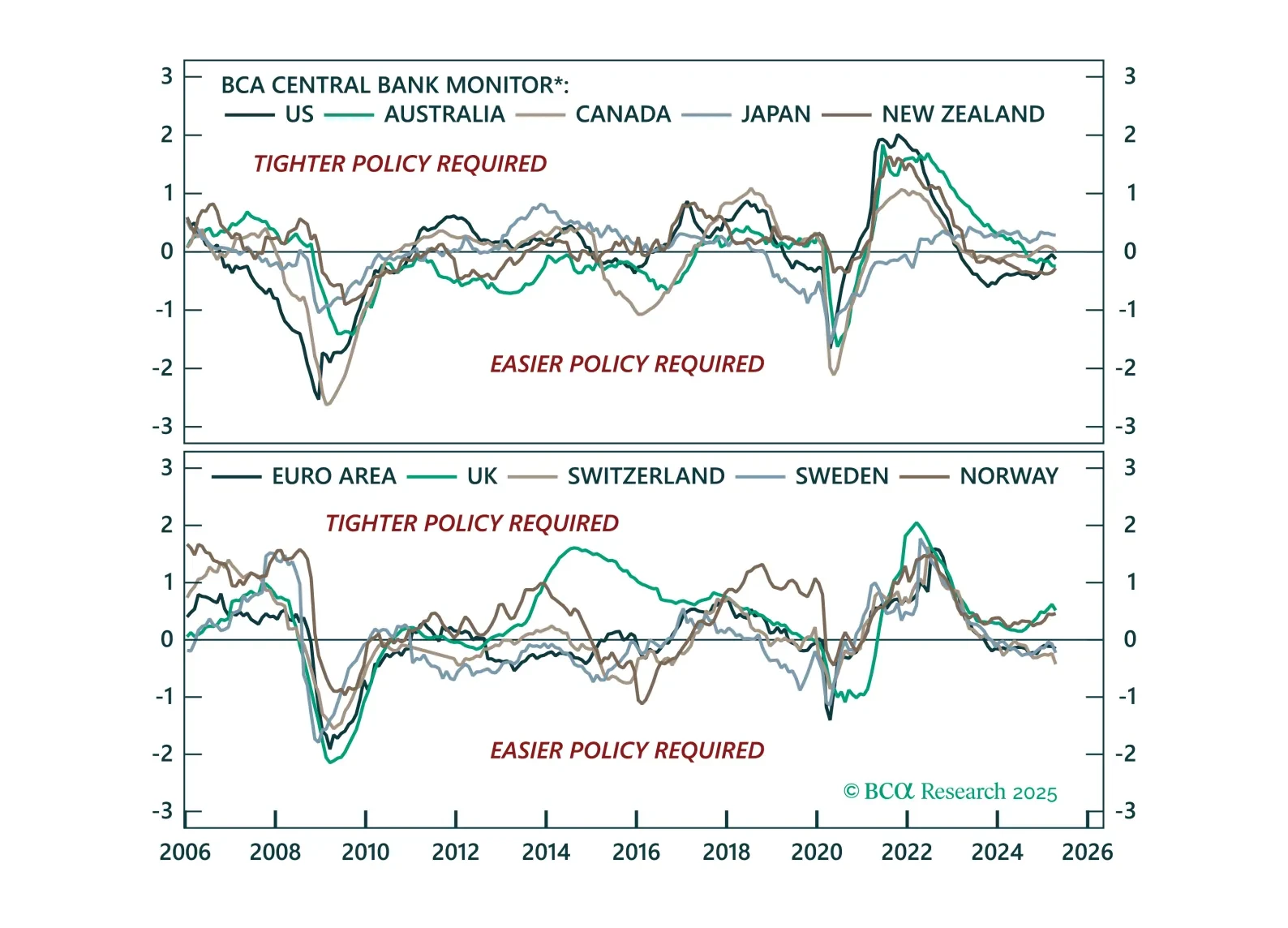

Expect broad-based dovish surprises from major central banks, and stay overweight UK and euro area government bonds. Our Global Fixed Income, European, and FX strategists published a joint update of BCA’s Central Bank Monitors. They expect the Bank of…

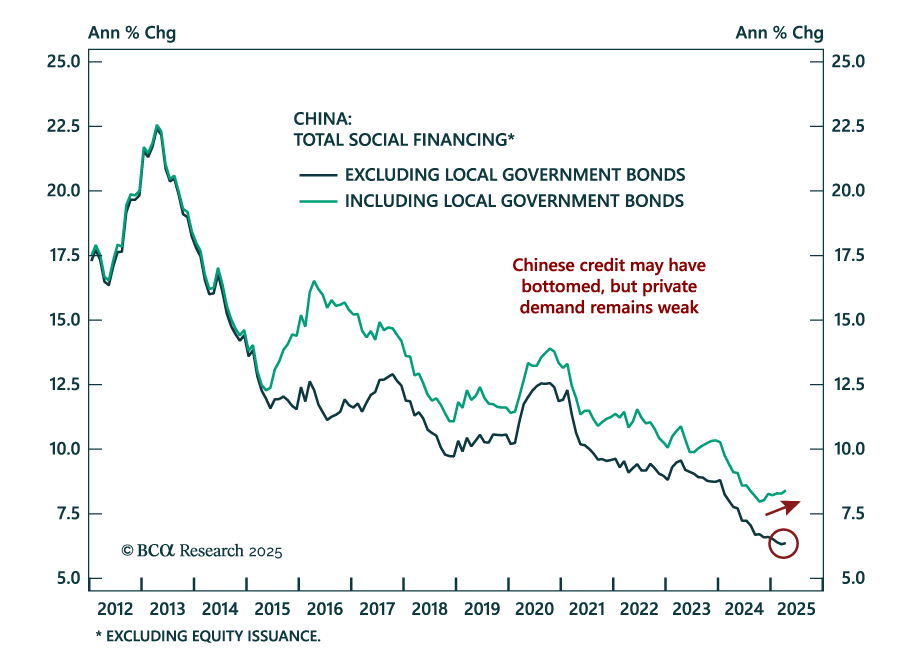

China’s weak April credit data reinforces the case for defensive positioning, with policy aimed at stability, not recovery. New yuan loans and aggregate financing both rose less than expected. While credit growth may have bottomed, it remains public-sector…

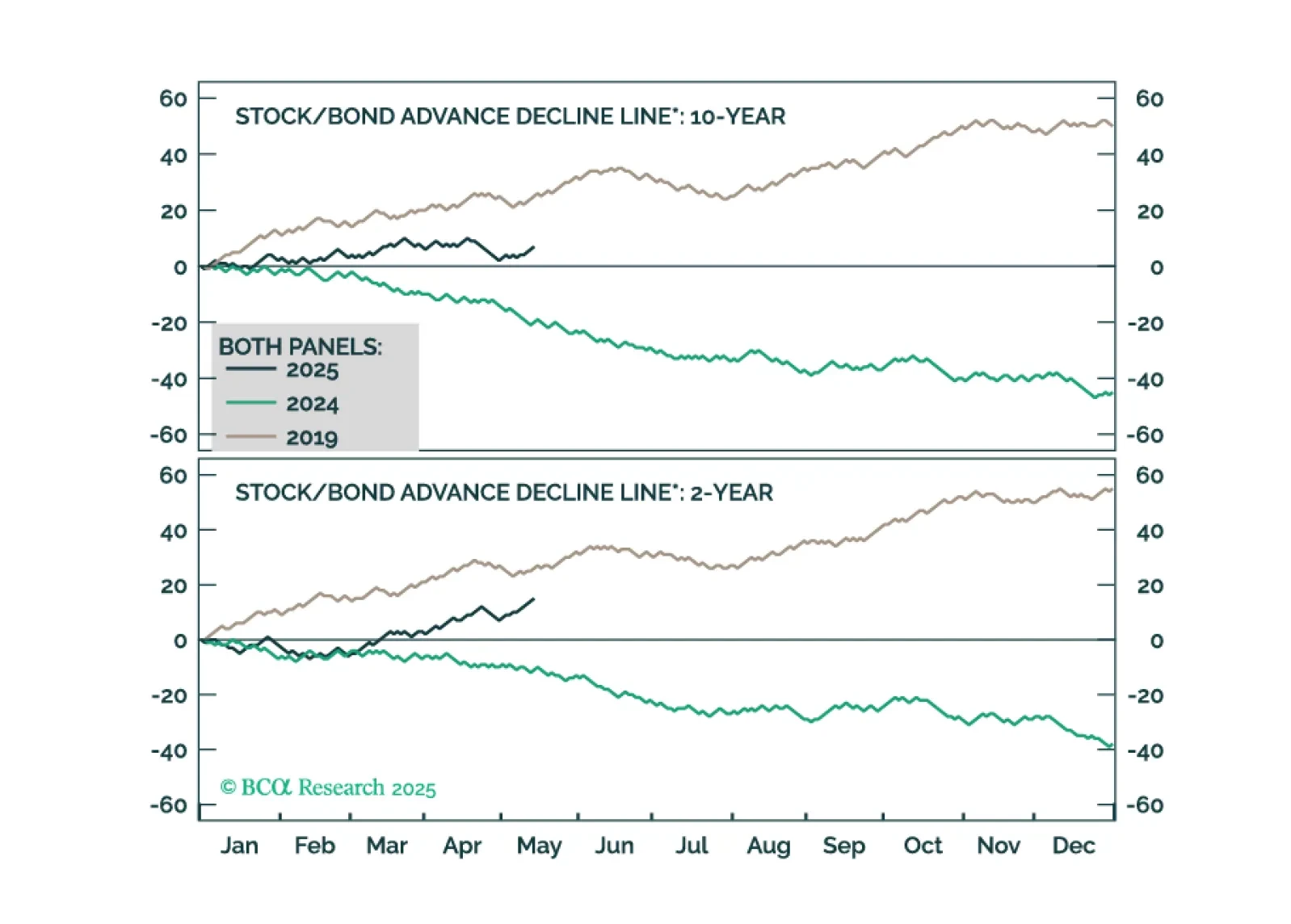

The stock-bond yield correlation is stabilizing after months of jitters, setting the stage for renewed Treasury demand as recession risks build. A negative correlation typically points to inflation concerns, while a positive one reflects growth optimism. In…

A weakening economy will apply downward pressure to Treasury yields, but the Trump term premium will keep long-dated yields higher than they would otherwise be. This makes Treasury curve steepeners the most attractive trade in US fixed income.

The easing bias remains, but not all central banks are equal. This Central Bank Monitor update reveals who is ready to cut more and who is still pretending not to.

Our Portfolio Allocation Summary for May 2025.

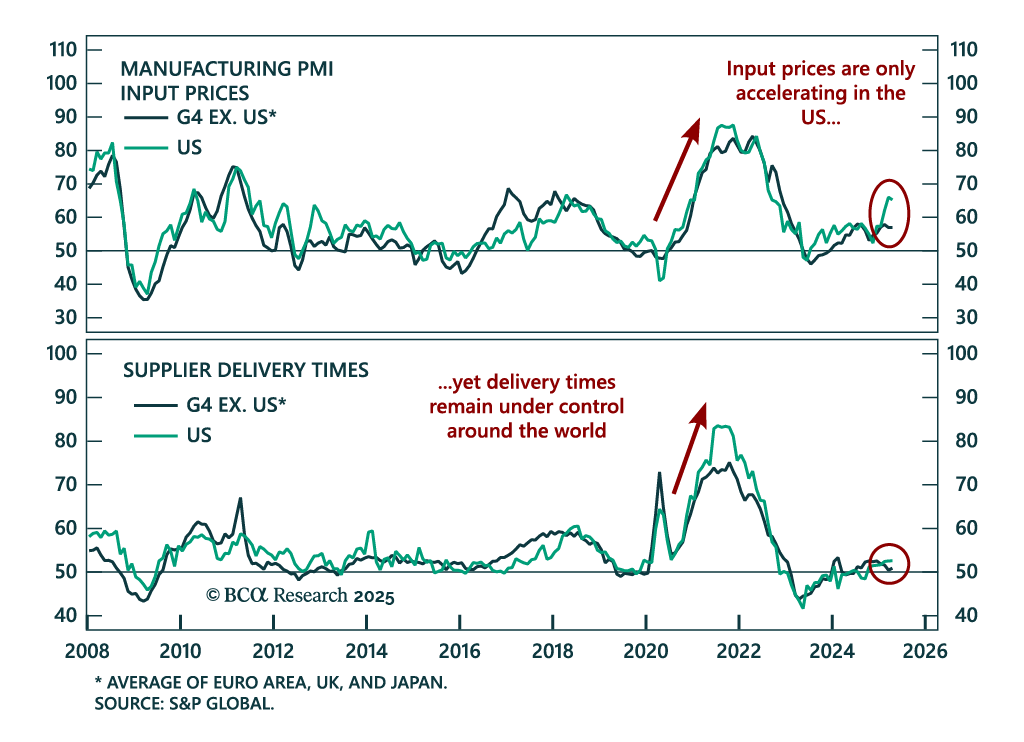

The inflation divergence between the US and Eurozone drives our call to stay long US duration. Inflation, typically a lagging indicator, blends slow-moving labor pressures with fast-moving supply drivers. The COVID inflation spike was a rare fusion of both,…