Fixed Income

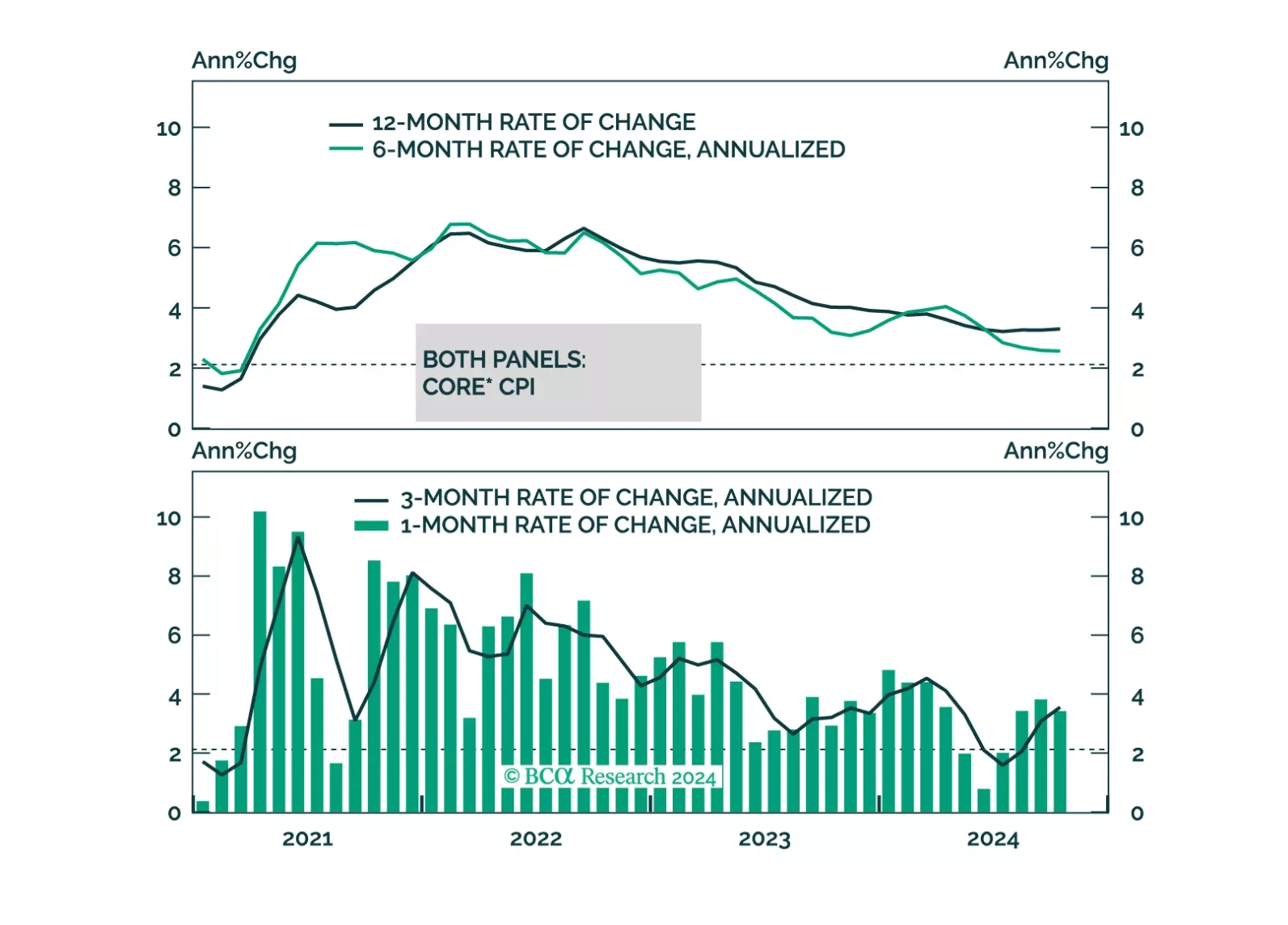

We update our inflation forecast following this morning’s CPI release, concluding that TIPS breakeven inflation rates have room to fall.

Our Portfolio Allocation Summary for November 2024.

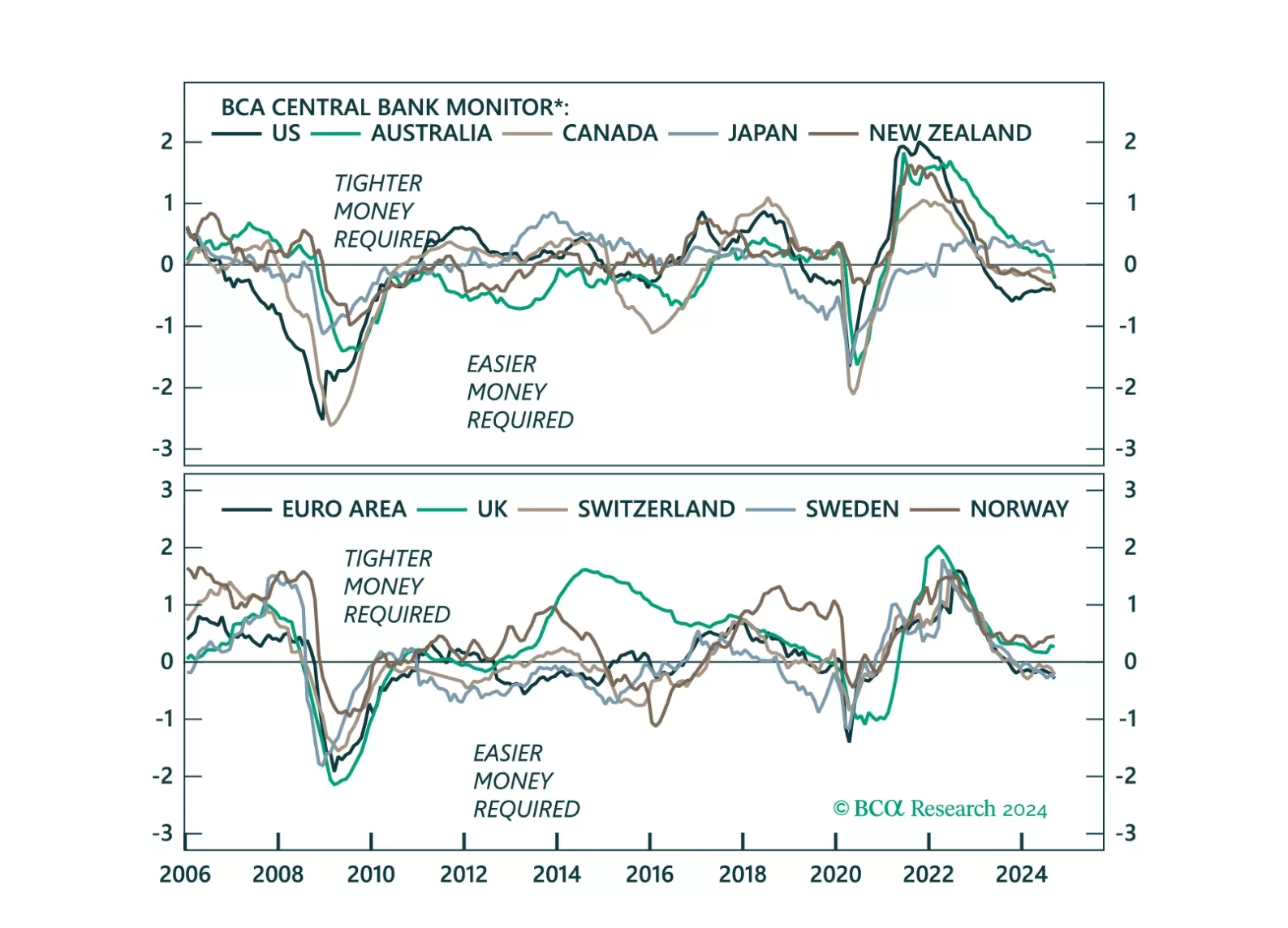

This week, we update our Central Bank Monitors (CBMs), that help us calibrate how monetary policy should be adjusted in developed-market economies. Our conclusion is that while overall, easier monetary settings are required, there a few trade ideas that arise from the divergences in signals amongst G10 countries.

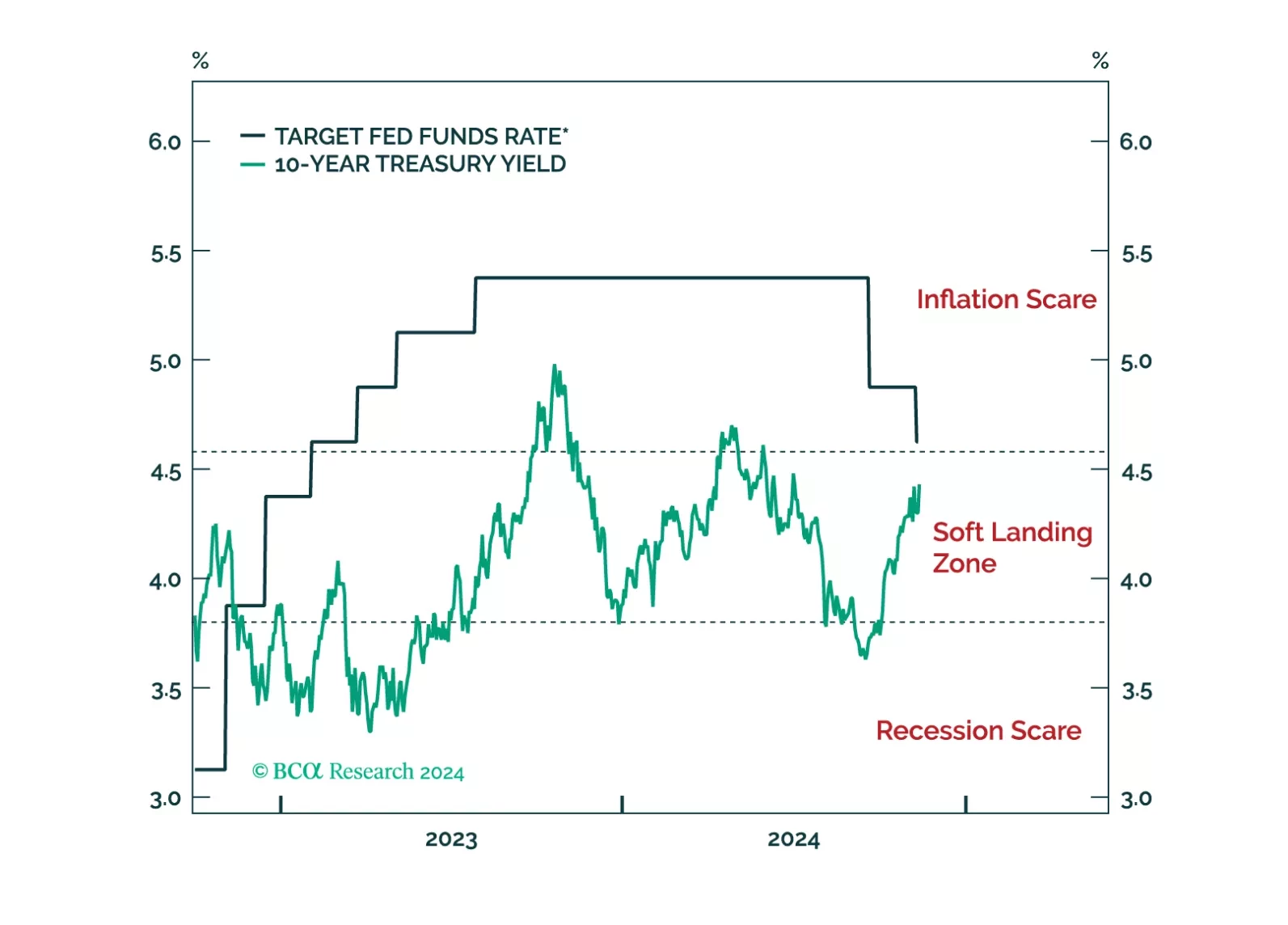

The force of the post-election momentum leads us to believe we could be stopped out of our defensive positioning before the week is out, but we still believe in our recession call. If we are eventually stopped out, we will seek a more opportune entry point to bet against risk assets once the election fever runs its course.