Fixed Income

A reaction to this morning’s employment report and a preview of the potential bond market implications of next week’s US election and FOMC meeting.

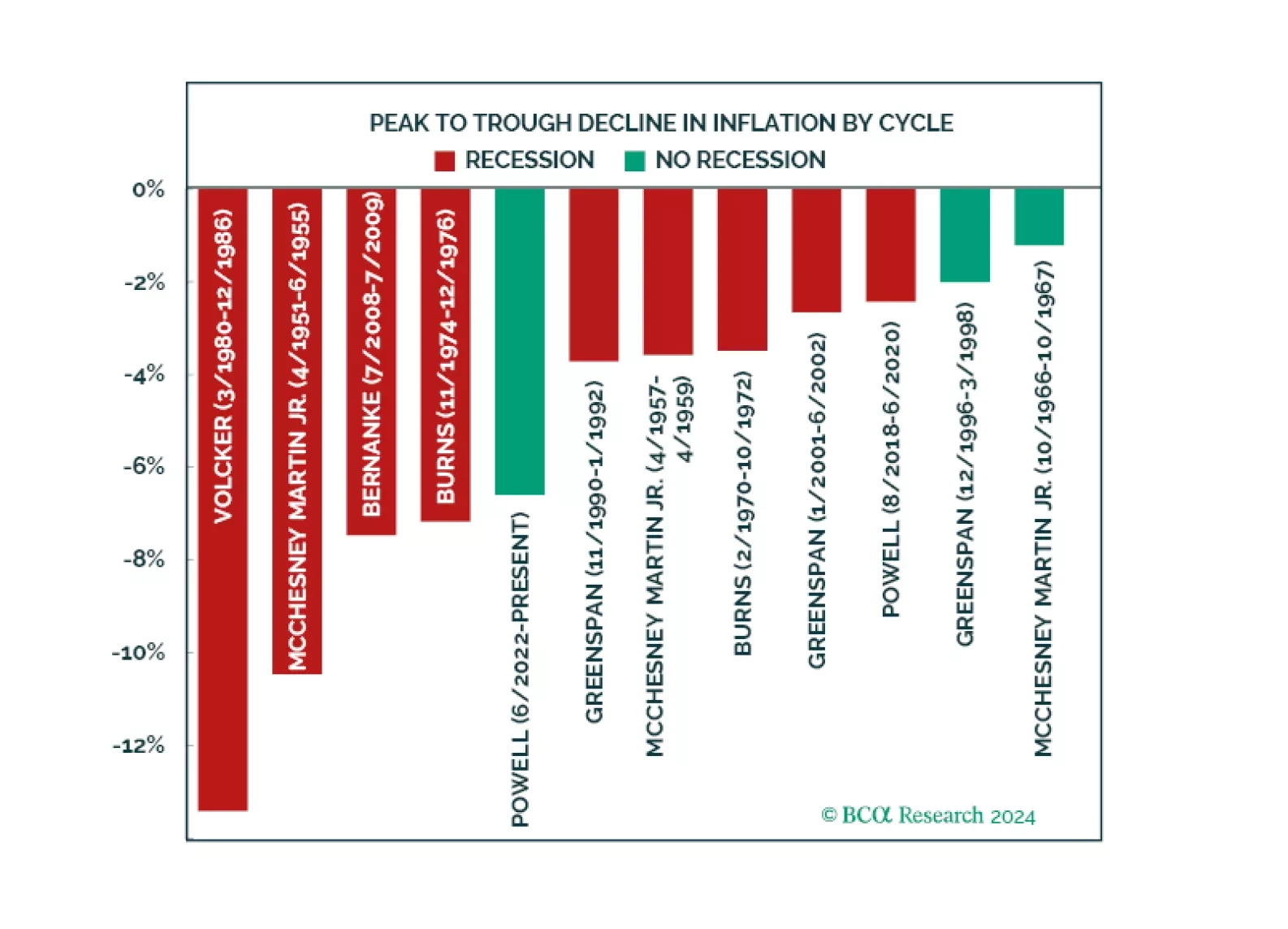

Can Powell achieve a soft landing? There are some indications he is doing it. We examine why our negative stance was wrong and analyze the four growth engines that kept recession at bay. Half of these forces remain while the other half have run out of juice. While this might be enough to keep the economy going, we maintain our defensive positioning. Equities have priced a very benign outcome. Meanwhile, rising rates in anticipation of a Trump win are pushing the economy away from the soft-landing path. We hedge the possibility of further upside in yields in case Trump gets elected by downgrading duration to neutral.

The latest Bank of Japan meeting did not alter our high-conviction views of being long the yen and underweight JGBs.

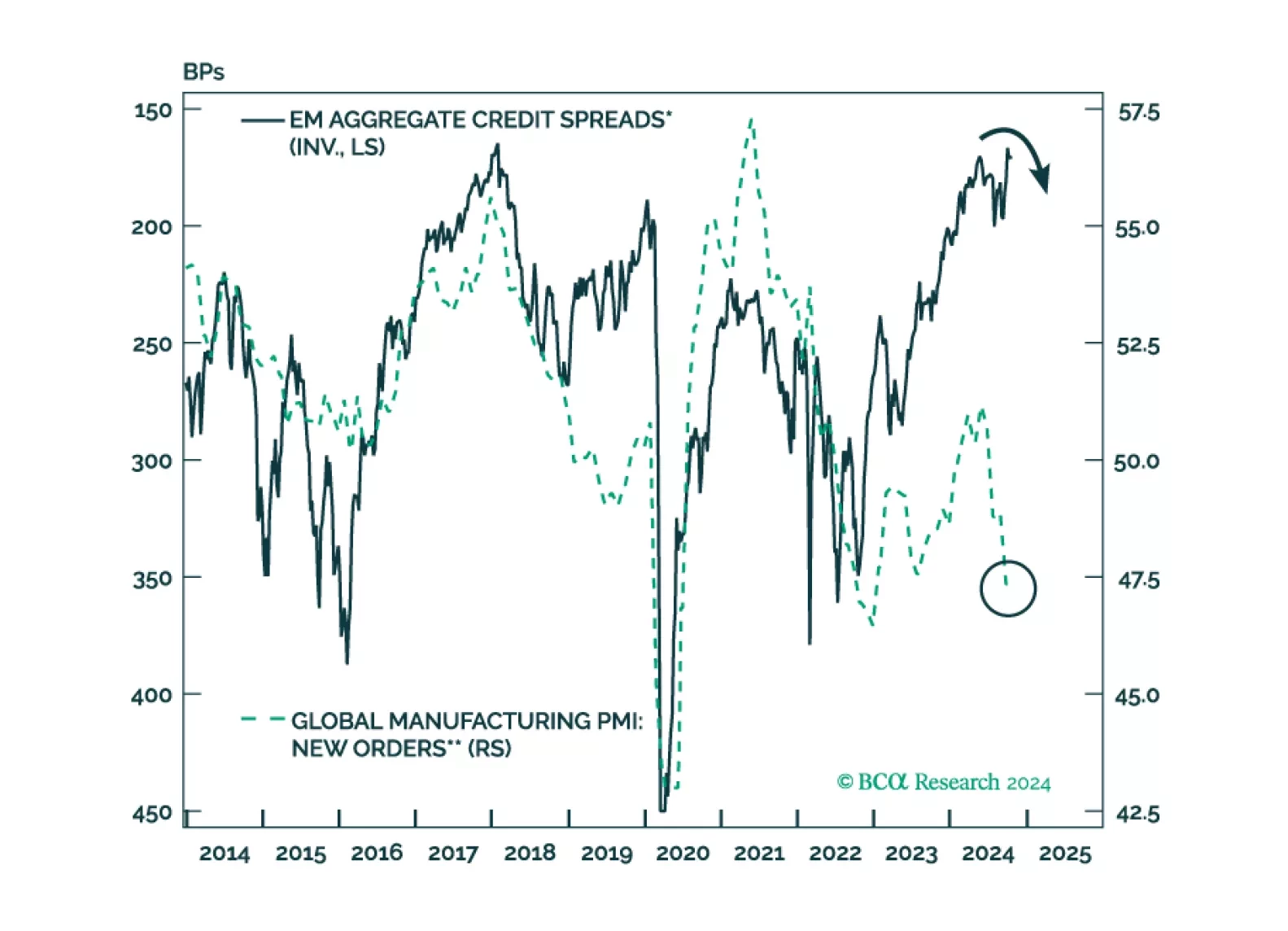

EM credit markets have recently defied the selloffs in EM equities, currencies, local currency bonds, and commodity prices. Such a decoupling is unusual. Resilient US growth and Fed easing are not sufficient to justify very low EM credit spreads.