Fixed Income

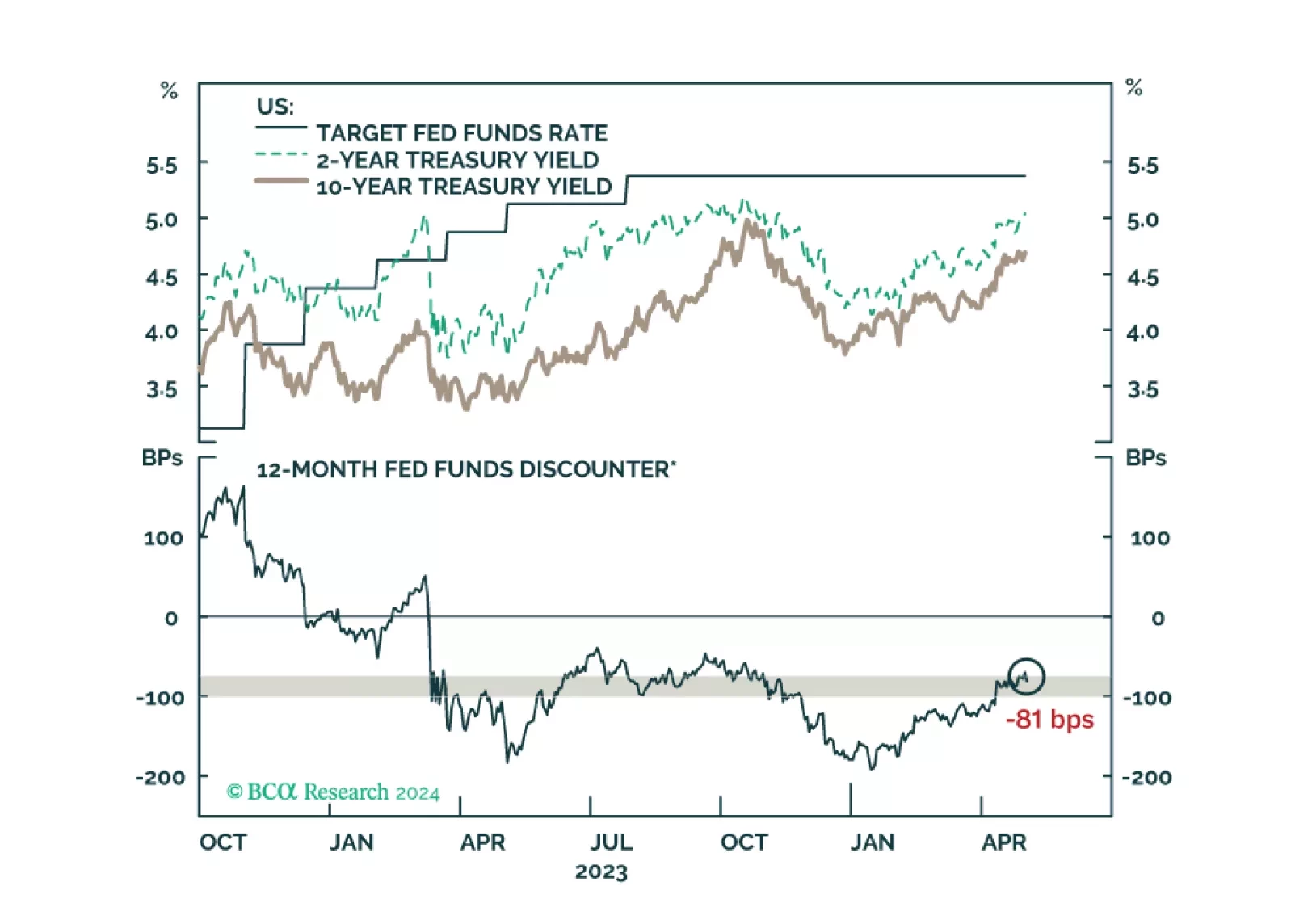

Updated views on US Treasury yields and the dollar following today’s FOMC meeting.

Wild hopes for US rate cuts got shattered, exactly as we predicted. But given the different incentives that the Fed and ECB now face, the relative pricing between the Fed and the ECB could widen further in the coming months. We discuss the implications for rates, the dollar, and the relative positioning in US versus European equities.

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

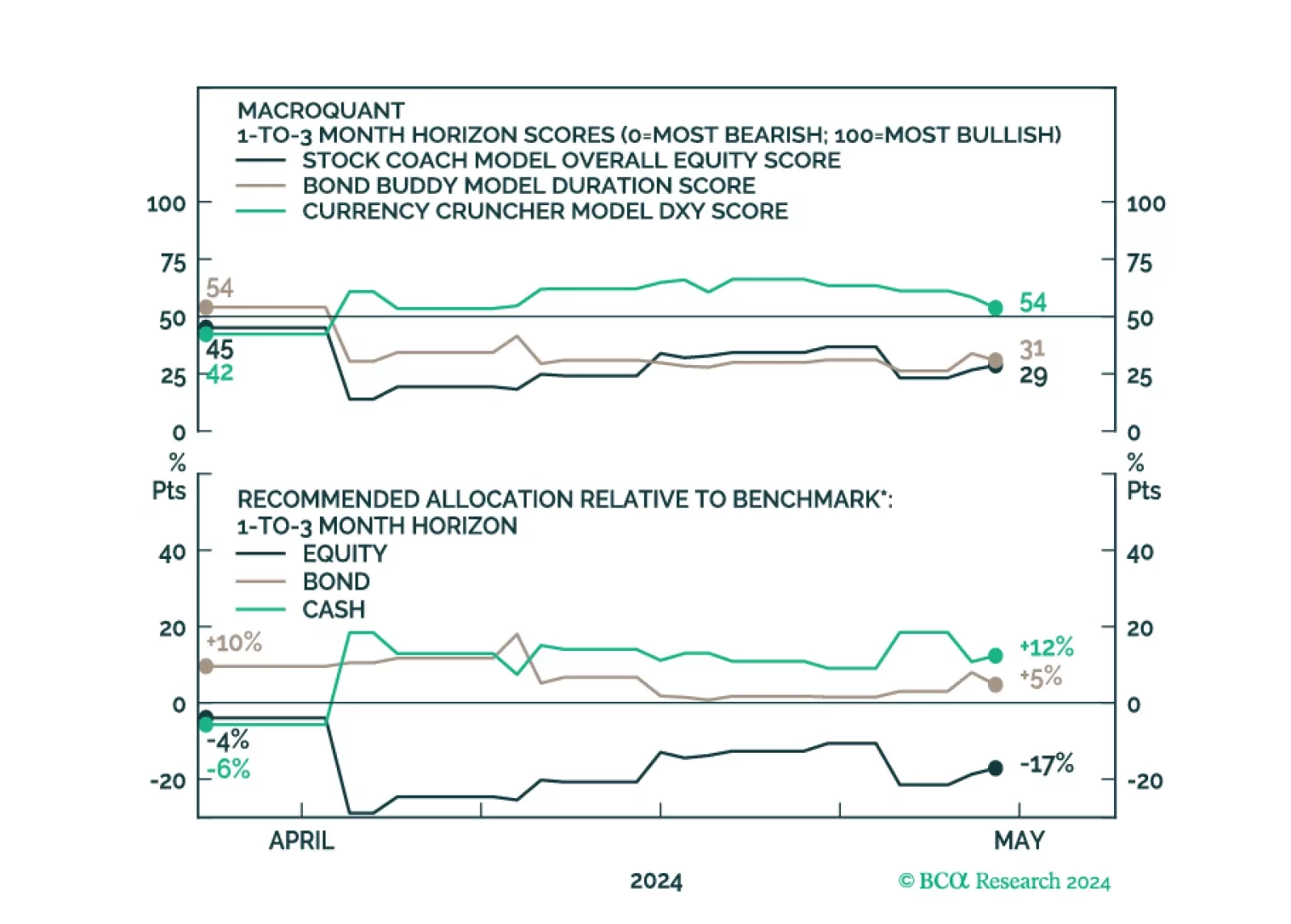

MacroQuant downgraded equities from neutral to underweight on a 1-to-3 month horizon. The model suggests increasing exposure to cash.

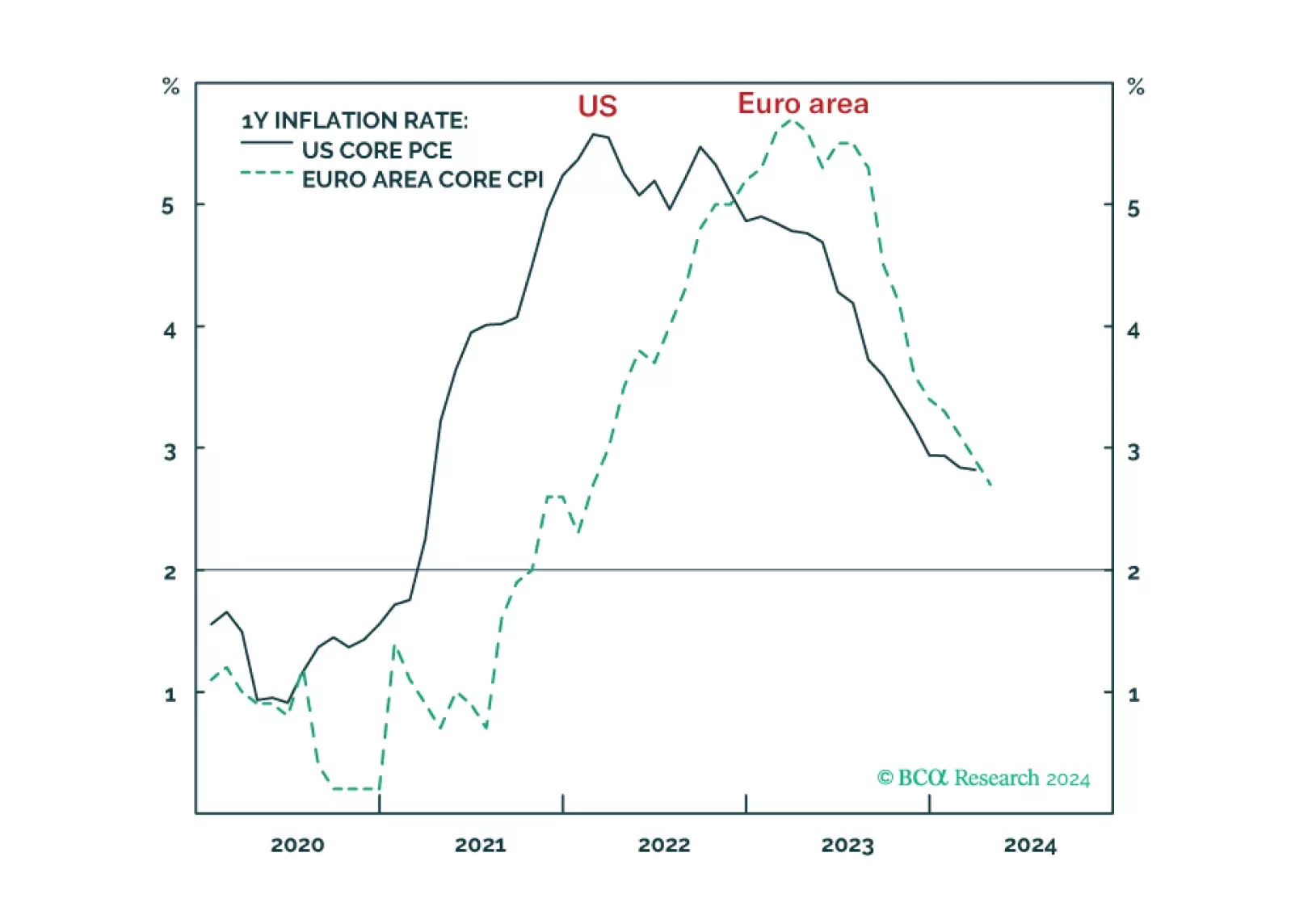

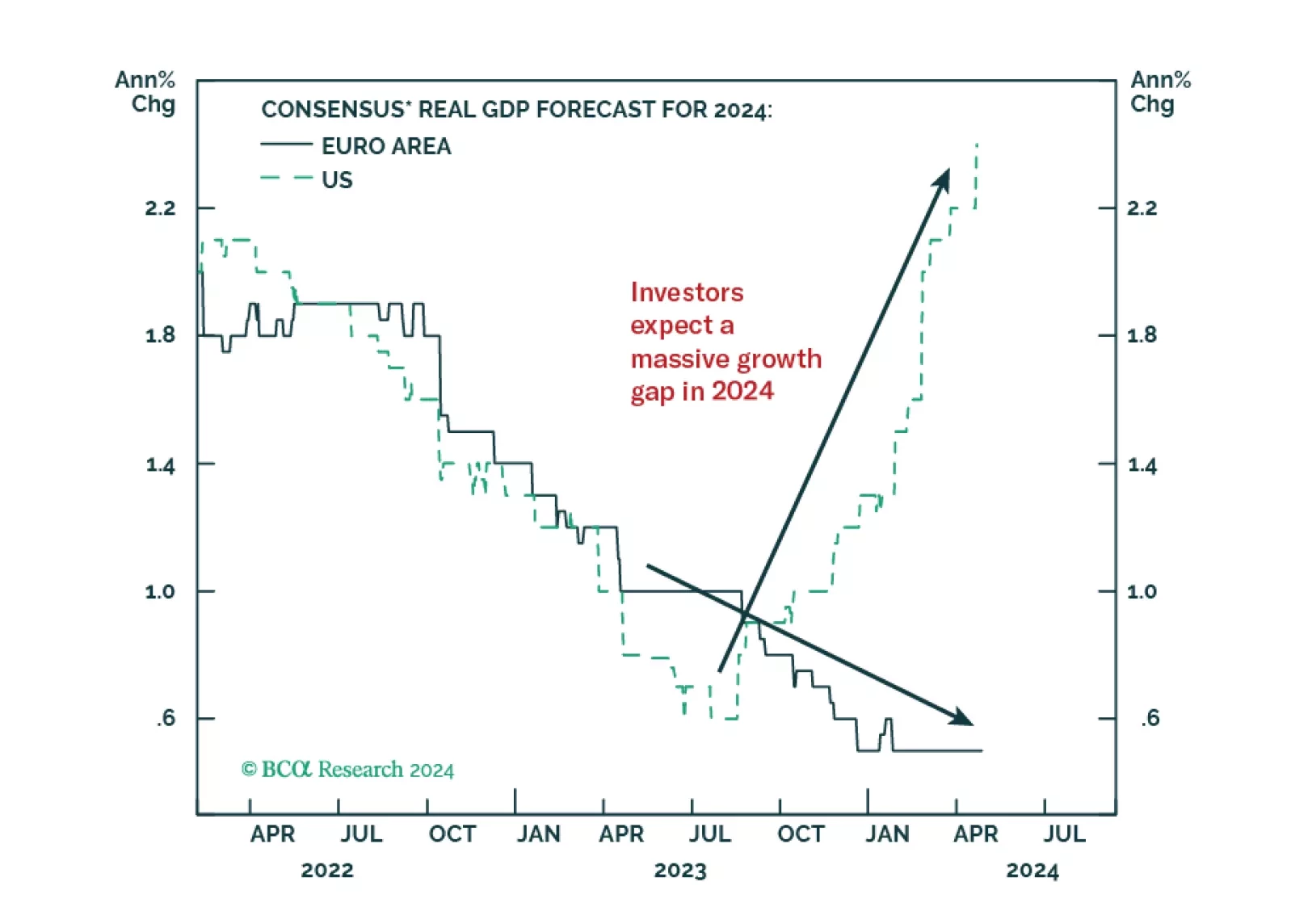

Investors anticipate a record growth gap between the US and the Eurozone in 2024. Does this skewed expectation create market opportunities?

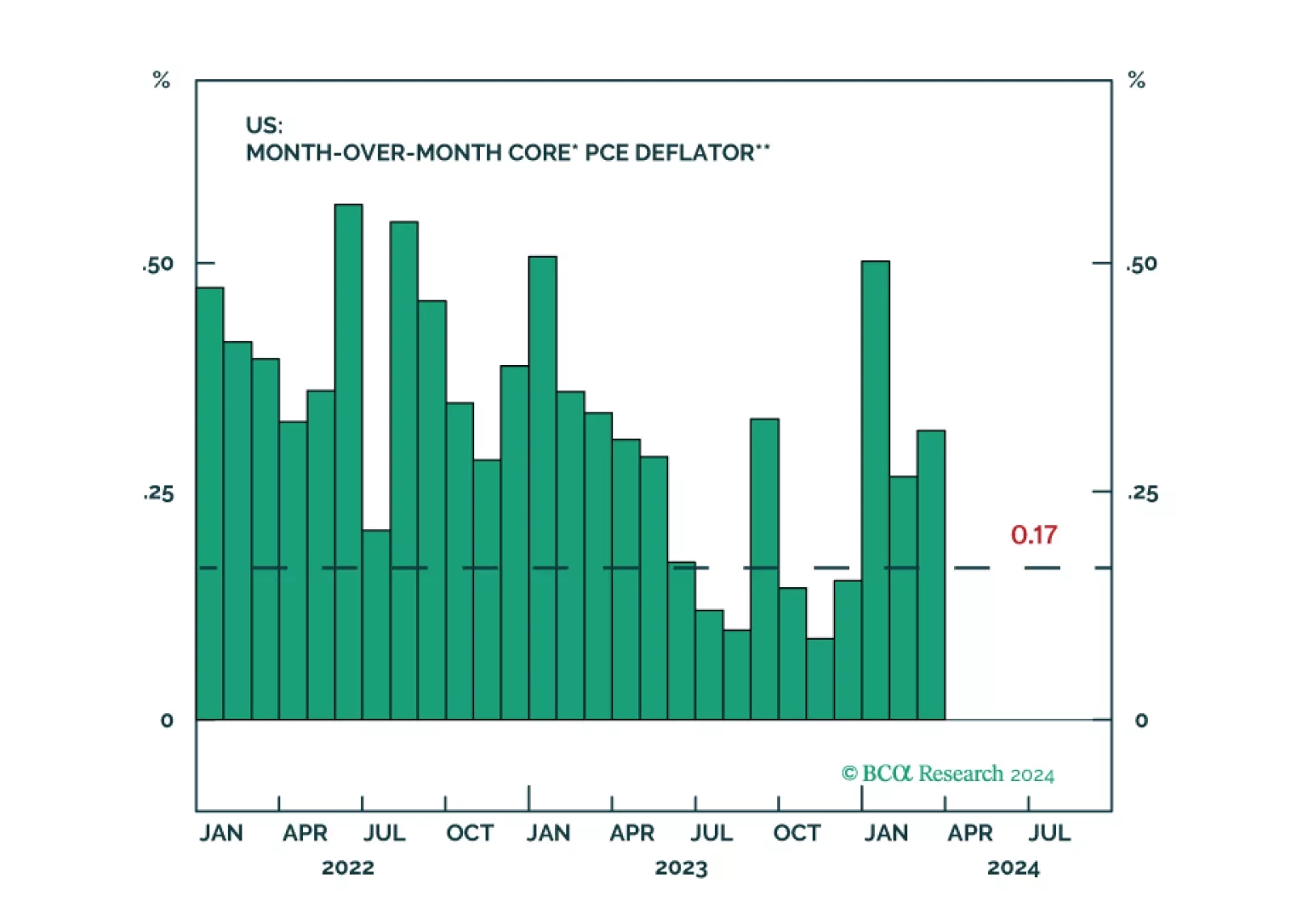

The latest edition of our Big Bank Beige Book suggests the expansion remains intact, though weakness in C’s private-label credit card portfolio could be a harbinger of distress among lower-income consumers. We remain tactically neutral with a bias to turn defensive once clearer signs of a recession emerge.