Fixed Income

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

Markets are increasingly pricing an end to the global easing cycle, with many central banks expected to remain on hold. But uncertainty remains high, and policy surprises are likely going into 2026. This Strategy Report breaks down the current drivers behind G10 central bank policies, and how to position for the next moves across FX and fixed income.

Asset allocators must pay attention not only to the magnitude of an asset’s expected returns but also to its shape, a concept technically known as skew. Adding skew into our analysis moves our equity allocation up to neutral while bonds remain at underweight. Plus: a new tactical trade is to buy sugar.

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.

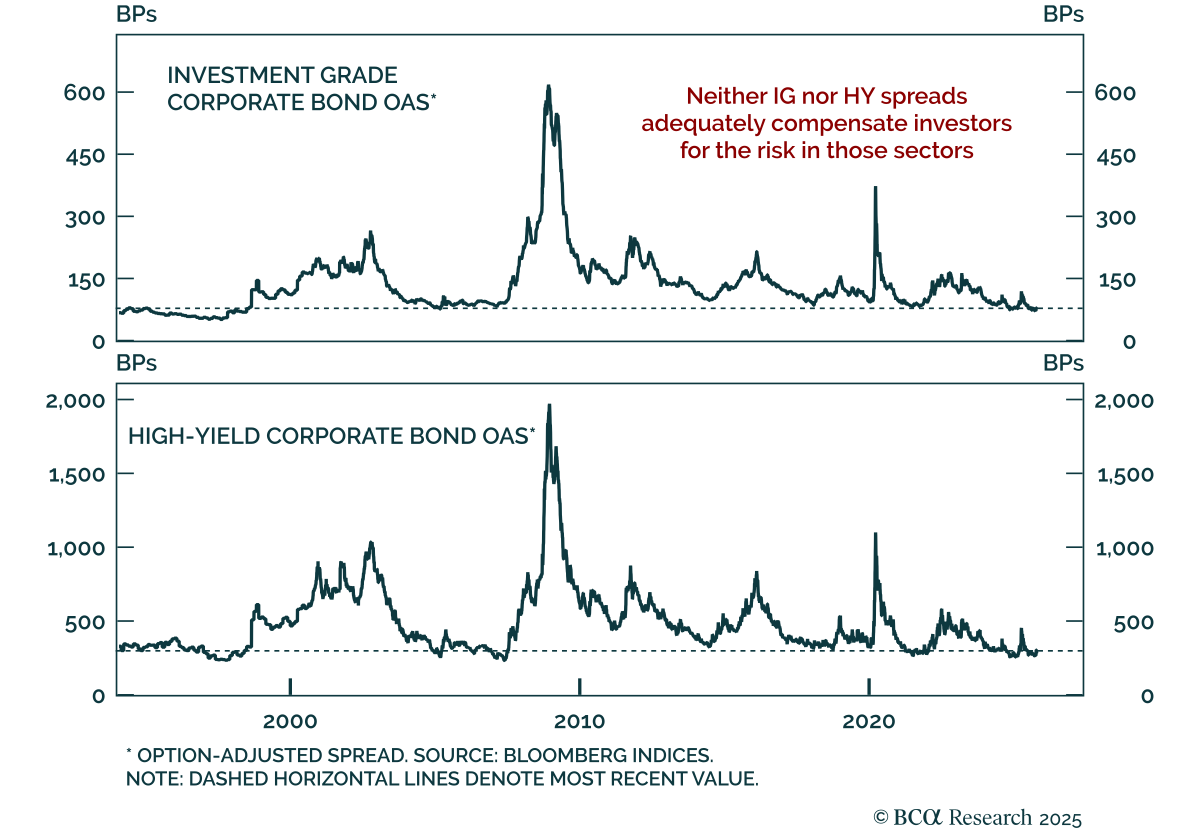

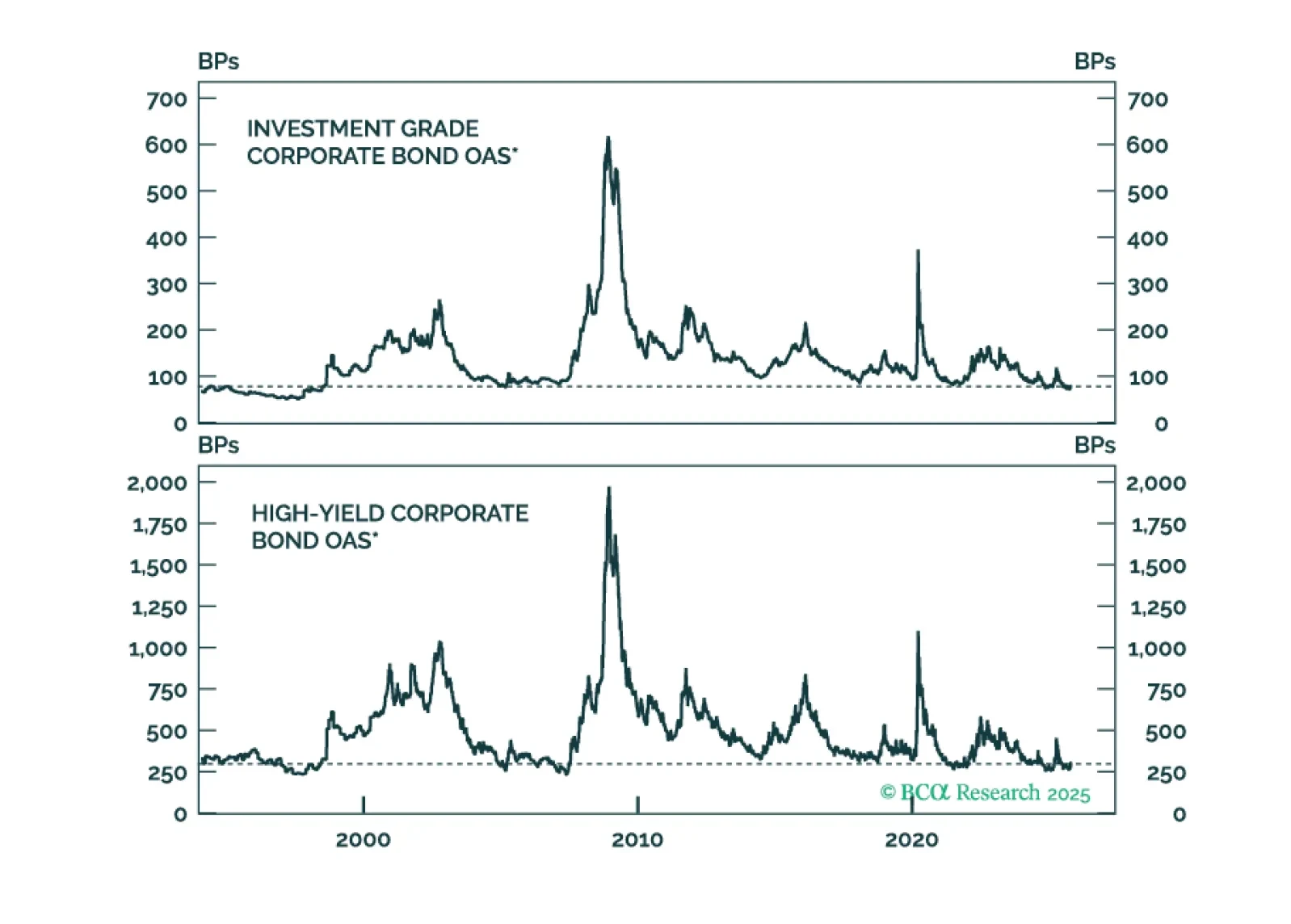

This week’s Special Report evaluates the reward and risk in corporate bonds. We address the question of whether low expected excess returns today are justified by low risk or an example of overvaluation.