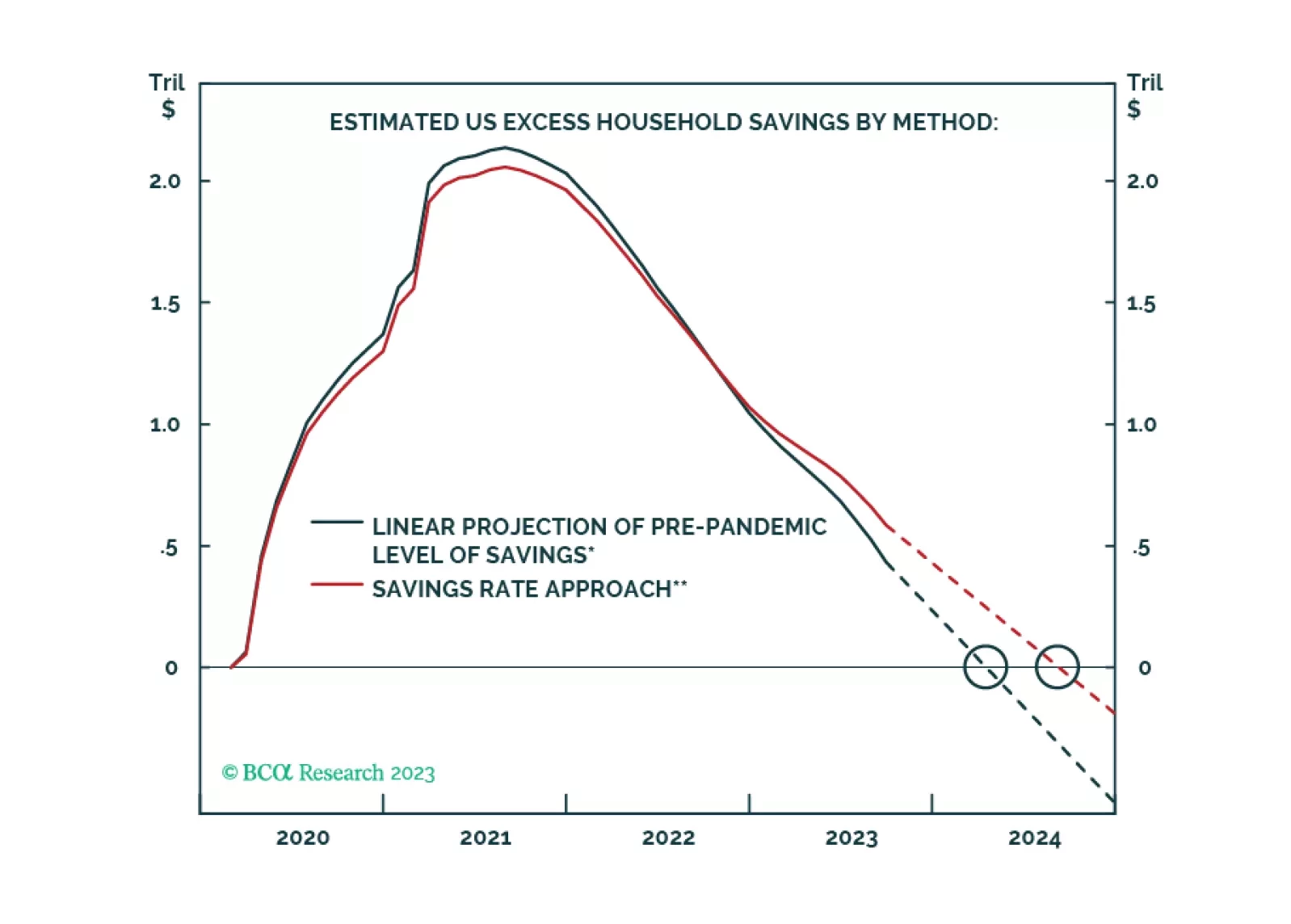

Global

BCA’s Commodity & Energy Strategy service does not expect a global recession next year. In practical terms, this means they are more bullish on their oil-price outlook for 2024 than the consensus and also differ with the BCA House view. In…

The Baltic Dry index, which measures the average price paid for the transport of dry bulk materials across more than 20 shipping lanes, has rebounded 63% this month and 130% since the middle of the year. The latest leg of the rally is not happening in…

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

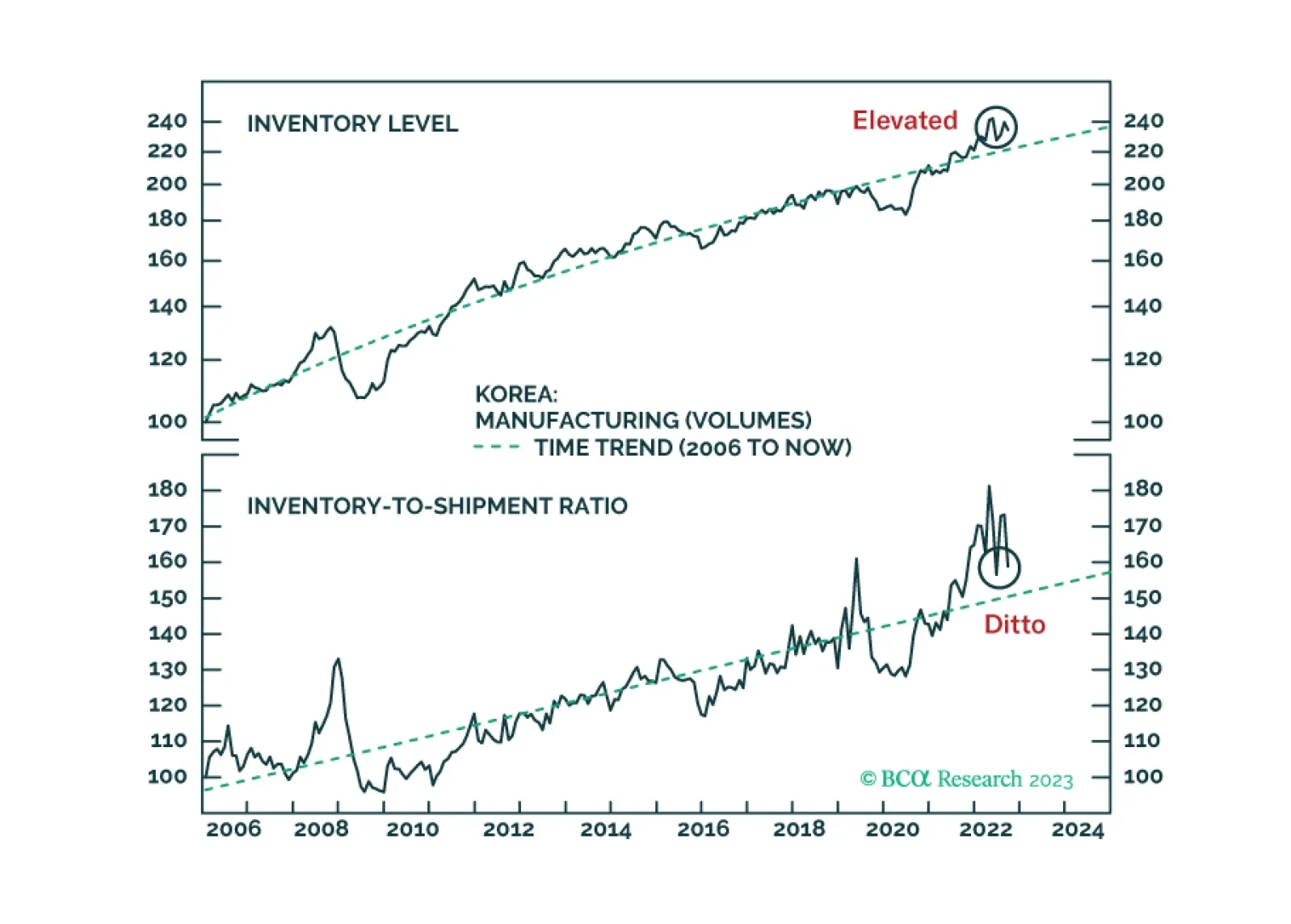

According to BCA Research's Emerging Markets Strategy service, investors should focus on fluctuations in final demand rather than inventories. A common narrative endorsed by many market participants is that inventory restocking worldwide will support the…

Most developed market central banks have paused hiking interest rates. With interest-rate differentials having been the most important driver of currencies over the last two years or so, the focus might now shift to other factors. One such factor could be…

Global cyclical sectors are outperforming defensive sectors on a year-to-date basis. The bulk of this outperformance occurred in the first seven months of the year. Relative valuations contributed to this dynamic as last year's selloff was more pronounced…

BCA Research's Commodity & Energy Strategy service concludes that lithium demand will rise over the long run. Lithium prices are continuing the selloff that began earlier this year, which was caused by strong production and mining capex increases. …

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.

Global equities have had a stellar 2023, rising by 16% year-to-date and outperforming global bonds by roughly the same amount. However, the large concentration of US stocks in the Magnificent Seven has called into question the legitimacy of this rally. There…

After dipping into negative territory between June and early August, the Global Economic Surprise Index has since rebounded, signalling an improvement in economic momentum. Initially, this rebound was isolated to the US. However, the trend has been broadening…