Hotels, Resorts & Cruise Lines

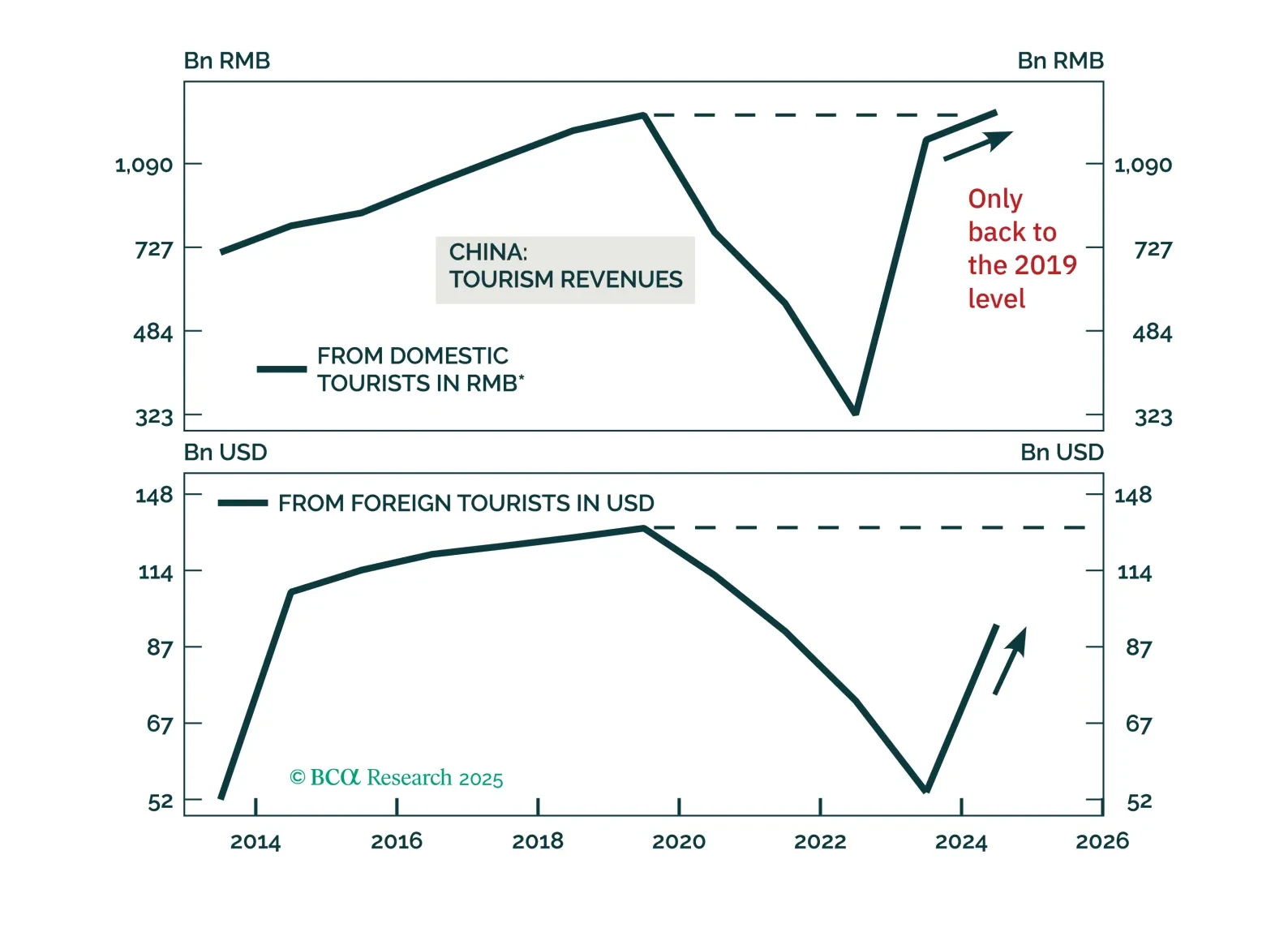

Chinese tourism will continue growing, but investors should be mindful not to overpay for Chinese tourism stocks by extrapolating their past double-digit revenue growth into the future.

In this week’s report “Adaptive Expectations: Revisiting Our Views”, we concluded that the S&P 500 is unlikely to find a bottom until inflation turns and monetary conditions stabilize, and US equities will follow a “fat and down” trajectory. We recommended that investors should overweight defensives vs. cyclicals. Accordingly, today we downgrade our overweight in Travel complex (Hotels, Cruises, and Airlines) to underweight. As a reminder, we recently moved retailing and durables categories to below benchmark. The key reason for this call is the effect of persistently high inflation on discretionary spending. In the past, we have written about the bifurcation of the US consumer, and that, while lower-income Americans are struggling with soaring prices of food, gas, and shelter, wealthier Americans are more comfortable and just shift their spending away from goods to services, such as eating out and travel. We expect strong profits for the travel sector this summer on the back of strong consumer demand and return of the business and international travel. We have discussed the drivers of the industry in these reports (here and here). Yet, markets are forward-looking, and the outlook for the industry beyond the summer months is dimming. With inflation entrenched, now even middle- and upper-class Americans as well as retirees are also starting to feel the pain. The US equity and bond market selloffs of the past 12 months have wiped out about $12 trillion and $3.5 trillion off their respective market value. This adds up to a combined $15.5 trillion or about 60% of US GDP (Chart 1). These are nest eggs and pensions shrinking by the day, diminishing future spending, and causing anxiety about the future. And while the S&P 500 is still at a level above the pandemic lows, adjusted for inflation, most of the gains are gone. On top of the reduced value of investments, negative real wage growth dampens consumer confidence (Chart 2). To make things worse, fears of recession and impending layoffs are pervasive in media stories, stoking fear of the future, and perhaps, making an economic downturn a self-fulfilling prophecy. Therefore, even wealthier Americans may have to tighten their belts and reduce their discretionary spending, with travel and leisure categories being on top of their list. Chart 1 Chart 2 Therefore, after the summer vacation surge is over, hotels and airlines are likely to experience slower demand which will weigh on their sales and pricing power. At the same time, these are industries most affected by the rising cost of fuel (airlines and cruise lines) and rising wages (hotels). As a result, we expect profitability to diminish and earnings growth recovery to stall. We have a negative outlook on the travel industry on a tactical time horizon. Bottom Line: Entrenched inflation is weighing on discretionary spending, and travel is likely to be the next victim of curtailed spending. We downgrade the S&P Hotels and the S&P Airlines indexes from overweight to underweight.

Highlights This is the second part of the publication, in which we provide an in-depth overview of Hotels, Restaurants, and Airlines, or the “travel complex” as we dubbed it. In last week’s report, we provided an overview of the macroeconomic backdrop, the Delta variant trajectory, and a “deep dive” into the hotel industry. We concluded Hotels is a sound tactical and cyclical investment, and we recommended an overweight. Airlines Less profitable trip mix and excess capacity: Domestic travel has rebounded to 2019 levels, while international and corporate travel are still lagging due to government and corporate restrictions (Chart 1). Some of the excess capacity is being redirected to domestic leisure travel, which has higher volume but is far less profitable. Airline cargo growth is a saving grace. The cost side of the airline business has its own challenges. Airlines have high fixed costs as they own or lease aircraft fleets. This creates a heavy financial burden during downturns. The price of jet fuel has increased to pre-pandemic levels. Labor costs are high due to the unionized work force and rising wages. Profitability is elusive: With airline revenues down 27% YoY in August 2021, and costs on the rise, it is hard to envision profitability without a return of international and business travel. Too much debt: Airlines’ net debt has risen significantly since the pandemic. Without positive cash flow generation, it will become harder and harder for them to meet their debt obligations. We have a negative outlook for airlines and are underweight the S&P Airlines index. Restaurants Defensive: Although the S&P Restaurant Industry resides within the pro-cyclical S&P Consumer Discretionary Index, its composition is nothing but defensive as it is dominated by fast-food chains. Profitable and resilient: Despite the havoc wreaked by Covid, the restaurant industry has not stopped being profitable (Chart 2). With any new Covid variant scare, restaurants will just go back to their “drive-throughs” playbook. Over the course of 2021, restaurant spending has risen by more than 40%. We have a positive outlook for fast-food chains and are overweight the S&P Restaurant index. Feature This is the second part of the publication, in which we provide an in-depth overview of Hotels, Restaurants, and Airlines, or the “travel complex” as we dubbed it. These industries share many drivers of profitability as each provides in-person experiences. They are also highly dependent upon public sentiment regarding the potential dangers and likelihood of Covid infections. Further, consumer confidence and financial wellbeing are at the core of this group’s profitability, as the travel complex is a quintessential discretionary spending category. The recovery of the group was coming along quite well until the Delta variant derailed it in late summer, with reports pouring in about dining rooms closing, airline bookings flagging, and hotel occupancy dipping. What is next? In last week’s report, we provided an overview of the macroeconomic backdrop, the Delta variant trajectory, and a “deep dive” into the hotel industry. We concluded that the Hotels, Resorts, and Cruise Lines industry has significant potential to return to its former “glory”: Delta is cresting, financially healthy US consumers are choosing to spend their money on services and experiences, sell-side forecasts are pointing to surging sales, and hotels have substantial pricing power. The industry is a sound tactical and cyclical investment, and we recommend an overweight. This week we will continue with a deep dive into the Restaurant and Airline industries. Sneak Preview: We like restaurants (overweight) but airlines, not so much (underweight). Chart 1Airline Majors' Traffic Still Has Not Recovered To 2019 Level Chart 2Profitability Is Resilient To Downturns Airlines “To suggest that the airlines should have better prepared for this environment seems akin to suggesting Pompeii should have invested more heavily in firefighting technology.” (JP Morgan, Mar. 22, 2020) Having avoided bankruptcy in 2020 thanks to federal payout support, US passenger airlines recorded $4.3 billion more in pre-tax losses in the first half of 2021. Clearly, this industry’s woes are far from over. Unsurprisingly, airlines have had the worst performance of any industry in the travel complex, underperforming the S&P 500 by 5% over the past year (Chart 3 & Table 1). Importantly, the performance of the industry slumped at the end of the summer, triggered by the Delta variant scare: After several months of steady increases, new ticket sales have dipped. As we noted last week, several major airlines have warned in regulatory filings that their third quarter may not look as rosy as was hoped. American Airlines, Southwest Airlines, and United all noted a deceleration in near-term customer bookings in August and elevated trip cancellations, even in leisure.1 All three have suggested that the Delta variant is having a dampening effect on business. We believe that the Delta variant is cresting. Our base case is that herd immunity is not far off. Of course, the travel complex is vulnerable to any new virus scare (Table 2), and this is a risk that investors need to keep in mind. However, unlike hotels, airlines face multiple other challenges. Chart 3The S&P Airline Industry Index Is Still Under the Pre-pandemic Level Table 1PerformanceTable 2Airline Industry Composition Competitive Landscape The US airline industry generated total operating revenues of $92.7 billion in 2020, down 48.3% from $179.4 billion in 2019. The industry is dominated by five majors, that are included in the S&P 500 index). Macroeconomic Backdrop For Airlines The airline industry is highly cyclical, and its wellbeing is tightly tied to economic growth. As economic activity improves, business travel tends to increase (except when Covid-related restrictions change the normal course of things). As economic growth translates into higher wages and stronger employment gains, leisure travel also takes off. So does the transportation of goods. As we discussed in Part 1 of the report, the economy is currently in a slowdown stage of the business cycle: Growth is slowing but off high levels. As such, even in the absence of Covid-19 or the Delta variant, Airline sales would continue to grow but at a slow pace. US consumers are financially healthy, and while most of the stimulus money has been spent, more and more people are returning to work. Recently, consumer confidence has soured on the back of a resurgence in Covid infections and rising prices (Chart 4, panel 2). However, domestic airline tickets are still cheap, and only fear of infection is keeping Americans grounded. With Delta cresting, people will go back to flying. Chart 4Airlines Are Highly Cyclical Key Drivers Of Profitability: Revenue Vs Expenses Revenue While many industries have been hit hard by the pandemic (brick-and-mortar retail, hotels, restaurants) most have turned the corner and are now profitable. Airlines, however, are still struggling (Chart 5). The good news is that losses have been declining, but the bad news is that the financial situation of most airlines is still precarious. Airlines rely on diverse sources of revenue, and thanks to that, business is starting to recover. The following are the key streams: Fares charged to customers In-flight entertainment, food, and beverages Sales of frequent-flyer credits to hotels, auto rental agencies, credit card issuers Auxiliary charges: Baggage checks, choice of seat, extra leg room Cargo and mail Chart 5Airlines' Revenue Remain Chart 6Airline Majors' Traffic Still Has Not Recovered To 2019 Level Traffic Recovery: Domestic Travel Has Rebounded, While International And Corporate Travel Are Still Lagging Budget airlines are pandemic winners: As of October 2021 compared to October 2019, scheduled available seat miles are down for all the airlines in the S&P 500 index (AAL, LUV, DAL, UAL, and ALK) (Chart 6). Only the budget airlines such as Allegiant, Spirit, and Frontier have a scheduled number of flights above the 2019 watermark. The underlying reason for such a dichotomy is easy to explain. The successful rollout of Covid-19 vaccines in the US has unleashed material pent-up demand for domestic leisure travel, benefiting domestic budget airlines. US domestic seat miles and load factors have recovered to pre-pandemic levels (Chart 7) as consumers have eagerly spent their stimulus checks on travel within the US. Chart 7Domestic Load Factor Has Fallen Below Pre-Pandemic Levels Major airlines are bleeding cash due to high exposure to international and business travel segments: In the meantime, many government and company-imposed restrictions on international and business flights are still in place. Companies are taking a very cautious approach to office re-openings and employee travel, and Zoom has become embedded as a viable corporate communications alternative and a cost-saving tool. As a result, the airline traffic of the majors with high exposure to international (Chart 8) and business travel (Chart 9), is still below the pre-pandemic level. Some of that capacity is being redirected to domestic leisure travel, which has higher volume but is far less profitable. Chart 8In August 2021, US-International Air Travel* Fell 54% Below 2019 Levels Chart 9Since Mid-July, Growth Of Overall And Corporate Ticket Sales Has Slowed Corporate and international travel are the most lucrative revenue segments and are significant in size: Before the pandemic, business travel constituted 30% of all trips. The industry can hardly recover without these segments rebounding. Until that happens, companies will stay unprofitable, and cash burn will continue. Business travel is projected to recover in 2022 at best and 2024 at worst: The US Travel Association projects US business travel to return to the 2019 level in 2024. The Airlines for America Association (A4A) concurs. It projects that airline passenger volumes will return to the 2019 level in 2022 in the best-case scenario and in 2024 in the worst. Airline cargo is a saving grace: With passenger revenues still lagging 2019 levels, many airlines are focusing on the capacity of their cargo units. With global supply chains clogged and shipping costs increasing five-fold over the past few months, this is a profitable niche. Air cargo demand reached its all-time high in 2020 and continues to grow in 2021: US airlines posted a 20.5% increase in demand for international air cargo in July 2021 from the July 2019 actuals (Chart 10). Chart 10For US Airlines, Growth In Air Cargo Continues To Outpace Air Travel By A Large Margin Airlines Compete On Volume: Airfares Are Low Despite the inflationary environment, the price of airfares is still 18% below its 2019 level (-10% annualized), and that is after 7% YoY price increases in 2021 (Chart 11). These are price levels not seen since the 1990s. With all the spare capacity, former international and business travel is now competing to attract domestic leisure passengers. Making things worse, due to prior commitments, airlines continued to grow their fleets throughout the pandemic closures (Chart 12), further increasing capacity and exacerbating competition for passengers as business and international travel are likely to lag, making peak ticket prices and peak revenue elusive (Chart 13). There is also another matter to consider, which is hardly minor. Airline taxes and fees constitute about a quarter of the price of a ticket. According to an example put together by A4A, the base airline fare of $236 has $64 in multiple taxes and fees, making tickets less affordable. Chart 11Airfares Have Fallen by 10% A Year Since The Beginning Of The Pandemic Chart 12Capacity Continues To Increase Chart 13Airfares Are Down 18% From 2019 And 29% From 2014 Sales Growth Analysts expect airline sales growth to stabilize at 60% over the next 12 months. The base effect certainly plays a significant role, but this rate will help the industry to recover. Expenses Airlines have high fixed costs as they own or lease aircraft fleets. This creates a heavy financial burden during downturns, as costs can hardly be cut. Other expenses such as labor and fuel are also sticky. Price Of Jet Fuel Has Increased To Pre-pandemic Levels The cost of jet fuel is one of the most significant input costs for airlines, constituting anywhere between 10% and 30% of revenue (Chart 14). The price of fuel can make a significant difference for an airline’s razor-thin margins. Airlines therefore tend to hedge their fuel exposure. Jet-fuel prices have rebounded to their pre-pandemic level and are up 49% from January 2021 (Chart 14), no longer giving the airline any slack on the cost side. According to Zach Research, at United Airlines the average aircraft fuel price per gallon increased by 66.9% year-over-year to $1.97 in the June quarter. Owing to the uptick in air travel demand witnessed in the June quarter following increased vaccinations, fuel gallons consumed were up 206.4%. Chart 14Price Of Jet Fuel Has Increased To The Pre-pandemic Levels Chart 15Labor Costs Increased Again Labor Costs Are Fixed Due To The Unionized Work Force Labor is another significant line item on the expense side of the airline’s income statement. Normally labor costs constitute 30-40% of sales. During the darkest days of the lockdowns, labor expense soared to 60% of sales (Chart 15). With a highly unionized labor force, layoffs and furloughs require significant payouts. There are also many other conditions in the labor contract that must be met. As a result, as sales tanked, labor costs did not change in the same proportion. Even so, airlines reduced their workforce from 458,000 people in 2019 to 363,000 in November 2020 (Chart 15). Now, with sales growing again, airlines have started rehiring. However, with recent wage rises, new employees are more expensive. Profitability With revenue challenged by a less profitable trip mix, excess capacity, and rising fuel and labor costs, airlines have been losing money for over a year now (Chart 16). While the increase in leisure travel and cargo units is helping, it is hard to envision profitability without a return of international and business travel. With airline revenue down 27% YoY in August 2021, and costs on the rise, profitability is still a long way off (Chart 17). Chart 16Airlines Are Unprofitable… Chart 17…And Are Burning Cash Net Debt Airlines’ net debt has risen significantly since the pandemic, driven by their need to support fixed costs (Chart 18). The increase in net debt was also stimulated by large government support and a low interest-rate environment. The problem is that since airlines are unprofitable, and are burning cash, it is becoming harder and harder for them to meet their debt obligations (Chart 19). While there have not been any high-profile bankruptcies in the US, some European and Asian carriers, such as Norwegian Air and AirAsia Japan Co., had to file for bankruptcy protection. As airlines are expected to continue to burn cash through 2022 their credit ratings have been downgraded (Table 3). We would not be surprised if more bankruptcies or industry consolidations take place in the near term. Chart 18Debt Levels Have Increased Significantly Chart 19Airlines Have Difficulty With Interest Payments Table 3All Airlines Credit Ratings Have Been Downgraded When Will Airlines Thrive Again While revenue lags, the industry will remain vulnerable to shocks and cost headwinds. However, once international and business travel recovers, sales will pick up, and companies will generate positive cash flow. Cash generation is a necessary condition for financial recovery – once airlines arrest the cash burn, they can shift their efforts towards rebuilding profitability and, eventually, repairing their balance sheets. Valuations And Technicals Airlines are trading at 36x forward earnings, which is optically high. However, the Valuations Indicator suggests that airlines are not expensive relative to their own history (Chart 20). The industry is also modestly oversold (Chart 21). Chart 20Airline Are Not Expensive Relative To Own History… Chart 21…And Are Oversold Investment Implications Airlines are slowly recovering from a malaise induced by the pandemic lockdowns. However, the road to recovery will be long. While domestic leisure and cargo traffic has picked up, it will be another couple of years before international and business travel rebounds to the pre-pandemic levels. With fuel and labor costs on the rise, profitability is elusive without those segments. And, even when airlines return to profitability, it will take them years to repair their indebted balance sheets. What is worse, with current levels of debt burden and negative interest coverage, bankruptcies may not be out of the question for some. While airlines may rally with rates rising and cyclicals outperforming, we are negative on the industry on both a cyclical and structural basis. However, if any of our clients wish to trade this industry, there are several liquid ETFs that represent this space (Table 4). If investors chose to be granular and pick individual stocks in this space, they need to be aware of the individual challenges of each airline and their levels of indebtedness vs cash burn. In short, we have a negative outlook for airlines and are underweighting the industry. Table 4Airline ETFs Are Readily Available Restaurants: Defensive Cyclicals Industry Composition Although the S&P Restaurant Industry resides within the pro-cyclical S&P Consumer Discretionary Index, its composition is nothing but defensive. In fact, a more appropriate name would have been the S&P Fast-Food Industry, with MCD and SBUX accounting for 70%+ of the industry market cap (Table 5). Table 5Industry Composition Performance Restaurant Industry performance has been tracking the performance of the S&P 500, lagging the benchmark by only 8% since January 2020 (Chart 22) Chart 22Restaurant Performed Almost In Line With The S&P 500 Restaurants Are “Defensive Cyclicals” Since fast-food prices are generally low, fast-food restaurants tend to be what economists call “inferior” goods, i.e., goods whose sales rise when the economy is in a downward spiral. Restaurants tend to outperform in the slowdown stage of the business cycle (Chart 23), are flat during contraction, and underperform during expansions. Consistent with these expectations, fast-food restaurants also came out as winners of Covid lockdowns: Although sales initially dipped, they quickly recovered as fast-food chains reoriented their business toward drive-throughs and other forms of take-out (Chart 24). Chart 23Fast-Food Restaurants Are Defensive Chart 24Sales Growth Is Recovering Covid While the restaurant business was coming along quite well, concerns emerged at summer’s end that the Delta variant would further delay industry recovery. Chains like McDonald’s and Chick-fil-A announced that they are slowing their dining room re-openings. As data from restaurant analytics firm Black Box Intelligence demonstrates, sales that had grown steadily earlier this summer have fallen.2 We believe that the reaction to the Delta variant is transitory as new infections are cresting. And, in the worst-case scenario, fast-food restaurants in the index will just switch back to their Covid “drive-through playbook,” and will maintain their level of profitability. Restaurant Spending And Profitability Over the course of 2021, US retail sales releases reveal that restaurant spending rose by more than 40%, outpacing the headline number (13%) by a wide margin (Chart 25). While restaurant spending is likely to decelerate over the coming months as pent-up demand for services is satisfied, earnings will continue to improve. This is in line with analyst expectations (Chart 26). Chart 25Restaurant Sales Skyrocketed In 2021 Chart 26Earnings Will Continue to Grow But At A Slower Pace Despite the havoc wreaked by Covid, the restaurant industry has not stopped being profitable, and although margins dipped in the midst of the lockdown, they swiftly rebounded. The 83% YoY print in restaurants FCF is nearly an all-time high reading since the history of the data going back to the 1990s (Chart 27). Debt Is Low Net debt to total assets also echoes the upbeat message highlighting that US dining stocks remain in good financial health (Chart 28). Chart 27Free Cash Flow Is At All-Time High Chart 28Debt Is Low Valuations And Technicals Valuations are not demanding while technicals suggest that the industry is oversold (Chart 29). Chart 29Restaurants Are Oversold & Undervalued Investment Implications The current slowdown stage of the business cycle is favorable for the fast-food industry. This industry is profitable and resilient in downturns. It is also attractively valued. The industry is oversold, which represents a favorable entry point for an overweight position. In short, fast-food restaurants are a sound “cyclical defensive”: They are resilient to downturns, highly profitable, and have healthy balance sheets. We have a positive outlook on the industry and are overweight. A Quick Aside: Toast IPO Before we conclude, a brief note on the new Toast (TOST) IPO is in order. While the stock became public only last week and is not a part of the S&P 500, it is an important newcomer to the stock market. The company is a market leader in cloud-based restaurant management software. Toast’s performance is tied to the health of the overall US restaurant industry. Many of the popular restaurants and fast-food chains are among Toast’s clients. Bottom Line We have a negative outlook for Airlines: This highly cyclical industry is on a long-winding path towards recovery, profitability, and deleveraging. Airlines face multiple challenges and headwinds: Fuel and labor costs are rising, while their most profitable revenue segments, international and business travel, are missing in action. Cash burn is still acute, and profitability is elusive despite all the progress made. We are much more positive on the outlook for the Restaurant Index, which represents some of the largest fast-food chains in the nation. This industry thrives during economic slowdown, is resilient to shocks, and is highly profitable. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Footnotes 1 Travel Investors Need More Drive, WSJ, Sep 12, 2021 2 Restaurants Close Dining Rooms Again as Delta-Driven Infections Spread, WSJ, Sep 13, 2021. Recommended Allocation

BCA Research’s US Equity Strategy service recommends overweighting the Hotels, Resorts, and Cruise Lines industry. The team summarizes this view as follows: The Delta variant is cresting. Their base case is that herd immunity is not far off. Of…

Highlights Covid-19 has wreaked havoc in the markets, but the Hotels, Restaurants & Leisure, and Airline industries have been most affected. These industries constitute what we call the “travel complex” as they share common drivers of profitability: First, they have been significantly affected by restrictions imposed on individuals and businesses in response to Covid-19 and, second, they rely on discretionary spending. Recovery of the group was proceeding swimmingly until the Delta variant derailed it in late summer, with reports pouring in about dining rooms closing, airline bookings flagging, and hotel occupancy dipping. What is next? The Delta variant is cresting. Our base case is that herd immunity is not far off. Of course, the travel complex is vulnerable to any new virus scare, and this is a risk investors need to keep in mind. Rising rates will be a mild tailwind for the group, as it tends to outperform in that regime. But this is not a key driver of its performance. Consumer confidence and financial wellbeing are at the core of this group’s profitability. So far, Americans still have money to spare and generally prefer to spend it on services. It is disconcerting that the Consumer Confidence Indicator has turned, but we are not too alarmed just yet: Jobs are still plentiful, and Americans are going back to work. August retail sales surprised on the upside. In Part 1 of the report this week, we take a deep dive into the Hotel, Resort, and Cruise Lines industry. We find the industry attractive for the following reasons: Hotel occupancy has increased, and the amount of money consumers are prepared to spend in hotel stays has surged. Sales are expected to increase by 75%, albeit from low levels, over the next 12 months. Hotels have also discovered many new sources of revenue. Earnings growth is impossible to estimate since last year the industry was losing money; however, margins have just turned positive. Companies also have significant pricing power to pass on expenses to their guests, and have the ability to mend their margins, eventually going back to the historical 20%. Lastly, the industry is cheap relative to its own history on a forward PE basis. According to our Technical Indicator, it is also oversold. The Hotels, Resorts, and Cruise Lines industry has a significant potential to return to its former “glory”, and we believe that it is a sound tactical and cyclical investment. We recommend overweighing this industry. NB: Please stay tuned for Part 2 of the report, on Restaurants and Airlines, next week. Feature Part 1: Hotels, Resorts And Cruise Lines In this two-part publication, we will provide an in-depth overview of Hotels, Restaurants, and Airlines. These industries constitute what we call the “travel complex” as they share many common drivers of profitability: First, they are the industries most exposed to Covid-related fears as well as corresponding government health directives, and, second, they rely on the discretionary spending of both consumers and businesses. In this publication, we will examine the macroeconomic backdrop for the entire travel complex, and then zoom into the Hotels, Resorts, and Cruise Lines industry (“Hotels”). Next week, we will provide an in-depth overview of Restaurants and Airlines. Sneak preview: We are bullish on Hotels and are overweight this industry in our portfolio. Hotels, Restaurant And Leisure, Along With Airlines, Were The Poster Child For Post-Covid Recovery… Covid-19 has wreaked havoc in the markets, but the travel complex was most affected. Airlines, hotels, and restaurants have suffered tremendous losses, and all have required government bailouts either directly, or indirectly through the Paycheck Protection Program (PPP). The travel complex rebounded mightily as the vaccine became widely available in February, and Americans suffering from cabin fever boarded planes, traveled, and ate out (Chart 1). Chart 1Hotels And Airlines Are Still Trading Below Their Pre-Covid Levels Table 1Travel Complex Is Lagging S&P 500 …Everything Changed This Summer All these positive developments began to reverse over the summer as Delta made its appearance in the US, and even the vaccinated succumbed to fears of infection. Airlines were one of the worst performers in the index. Hotels and restaurants were doing better, but their performance did not shoot the lights out either (Table 1). Restaurants: According to a National Restaurant Association survey of 1,000 adults, in recent weeks nearly one in five Americans say they are no longer going out to restaurants, 9% have canceled existing plans to eat out, and 37% of adults said they ordered delivery or takeout instead of dining in a restaurant. Chains like McDonald’s and Chick-fil-A are slowing their dining room reopenings. As data from restaurant analytics firm Black Box Intelligence demonstrate, sales that had grown steadily earlier this summer have fallen.1 Airlines: Several major airlines have warned in regulatory filings that their third quarter may not look as rosy as hoped. United Airlines has noted a deceleration in customer bookings, while Southwest Airlines reported a continued softness in bookings—even in leisure—and elevated trip cancelations. Similarly, American Airlines has said that, after a strong July, it saw a softness in near-term bookings in August and an increase in near-term cancelations. All three have suggested that the Delta variant is having a dampening effect on business.2 Hotels: Marriott International said that revenue per available room in August of 2021 was down 27% from the 2019 level – a drop from the 23% decline seen in July. However, the CEO of the company sounded sanguine: “The trends seem to be stabilizing as we get into the early days of September”. Most of the decline came from lockdowns in China. The most recent data shows revenue per available room was down 44 percent off 2019 levels — not ideal but an improvement from the 57 percent decline seen a week prior.3 With bad news abundant, the natural question is whether these industries are still a good tactical and cyclical investment. Delta Variant Clearly, a resurgence in infections has had an adverse effect on the travel complex. However, there are early signs that the Covid-19 Delta variant is cresting (Chart 2). Around 75% of the U.S. population has had at least one vaccine shot. Globally, 31.5 million doses/day are being administered. At this rate, it will take just eight months to vaccinate 75% of the global population. Herd immunity is not far off. Our base case is that Covid-19 and its multiple variants are unlikely to disappear, but consumers and businesses are learning how to live with it. We believe that the surge of Delta infections will subside over the fall, and the entire travel complex will continue to recuperate from the Covid-inflicted damage. Of course, the resurgence of Covid-19 cases and newer variants could undermine a recovery. This is a risk investors need to monitor. Chart 2The Covid-19 Delta Variant Is Cresting Macroeconomic Backdrop Rising Rates Are A Tailwind For The Travel Complex Direction and rate of change in yields dictate which US equity sectors and industries will do well. There are many crosscurrents in both economic data and Fed speak currently that obscure the answer to this question. Analysis of the performance of travel industries by rates regime suggests that all of them tend to do better when rates are rising, as higher rates indicate stronger economic growth (Chart 3). Airlines are most sensitive to an economic slowdown and will underperform most if rates stay “lower for longer”. Consumers Still Have Money To Spend On Services But Less Than Before Chart 3Travel Outperforms When Rates Are Rising Travel is a quintessential representation of discretionary spending on services. Consumers travel and eat out when they are confident about the future and have a healthy income and excess savings. Chart 4Disposable Income And Savings Are Returning To Trend The helicopter money drop has increased consumer income and padded their savings. However, income gains were not permanent and, recently, disposable income has returned to trend (Chart 4, Panel 1). Further, much of the excess savings has been spent (Chart 4, Panel 2). In another unpleasant twist, over the past few months, wage gains (4.8%) have lagged price increases (5.2%), reducing the purchasing power of American consumers. In response to these developments, the consumer mood has soured: The Consumer Confidence Indicator has slumped to a six-month low of 114 from 125 a month earlier. The next 12-month inflation expectations have surged to 6.5%. While it is disconcerting that consumer confidence has turned, we are not too alarmed just yet: Jobs are still plentiful, and Americans are likely to go back to work as the majority of children are now attending schools in person. In short, Americans are not destitute, but the pattern of spending is normalizing and returning to the pre-pandemic trend. The August retail sales print at 0.7% surprised on the upside and proves that US consumers have not tightened their belts. It is also a positive for the travel complex that demand for services exceeds demand for goods: Consumer expenditure on goods is above trend and has recently turned, while spending on services is below pre-pandemic levels, and the rebound is running its course (Chart 5). Inflation Is Not A Concern For The Travel Complex CPI readings for the travel complex this summer looked outright scary: In July, airfares were up 19% YoY and the price of hotel stays was up 24% YoY. These numbers have come down to 6.7% and 19.6% in August. Indeed, these readings make us wonder whether travel is still affordable to consumers. The answer is a resounding “yes” – reported surges in prices are a function of a base effect and, compared to the same time two years ago, the two-year CAGR of prices looks reasonable for all the industries (Chart 6). Chart 6Price Increases For The Travel Complex Are Moderate Chart 5Real Spending On Services Is At Pre-Pandemic Levels: Room For Further Rebound Analysis By Industry: Hotels, Resorts, And Cruise Lines Hotels is a $55B industry4 which is forecast to produce 31.4% growth in 2021 (Table 2). Its market cap is $239Bn and it constitutes 0.6% of the S&P 500 index. The US Hotel industry suffered about $125 billion5 in aggregate lost revenues due to the pandemic in 2020. Hotel operators were in total cash-conservation mode – slashing capex budgets by 75%, suspending dividends, and raising capital. Some 670,000 workers lost their jobs or were furloughed – only half of these workers have returned so far (Chart 7). Table 2Hotels (GICS 4) Constituents After a tough year, Hotels have now mostly reopened. Demand is expected to surge by 31.4% YoY in 2021, and per room revenue has reached $94, higher than the pre-Covid-19 level. Many hotels have returned to profitability. However, hotel occupancy in the US is yet to return to the pre-pandemic level: It currently stands at around 50% compared to 70% plus pre-Covid (Chart 8). Chart 7Industry Was Decimated By Covid And Is Recovering Slowly Chart 8Occupancy Rates Are Returning Back To Normal Sources Of Revenue Hotels started to recover during the first half of 2021 and revenues are expected to continue to surge to well above the pre-pandemic level in 2022. Analysts expect hotel sales to rebound by 75% over the next 12 months (Chart 9). There are multiple sources of revenue, and a reduction in business travel and international tourism is likely to be replaced by other creative options. Leisure Travel: Significant pent-up demand has been driving a recovery in hotel stays, but it is mostly in leisure travel. According to AHLA, 56% of consumers say they expect to travel for leisure, roughly the same amount as in an average year. Consumer spending on hotels has rebounded and is close to the pre-pandemic normal (Chart 10). Chart 9Blockbuster Sales Growth Is Expected (Off Low Base) Chart 10Consumers Eagerly Spend On Hotels Business travel is still lagging. According to AHLA, business travel was down by 85% compared to 2019 through April 2021, and since then has only begun ticking up slightly. However, going forward, this trend may turn as companies start positioning their in-person visits as a competitive advantage. Bleisure travel: A new post-Covid trend has developed: Workers combine business travel with leisure, prolonging hotel stays. Another creative idea is “working from a hotel” packages to appeal to remote workers tired of being cooped up at home. International tourism: Covid-related restrictions in the rest of the world, and especially cessation of travel from China, is still denting hotel revenue. With global vaccination rates improving by the day, this segment won’t take long to rebound. Profitability While there is forecast to be a pronounced rebound in hotel sales growth over the next 12 months, it is less obvious whether and when the industry will return to its former levels of profitability (Chart 11). After all, not only was the travel complex damaged by the pandemic, but now hotel operators also incur additional Covid-related cleaning expenses. Currently, analysts expect the next 12 months EPS to rebound to about a quarter of January 2020 trailing EPS ($10 vs $34). While this looks measly, from an investment standpoint it presents an opportunity as eventually, albeit slowly, earnings will return to trend. Historical earnings growth is not calculable as the industry was losing money until very recently. Chart 11Earnings Are Expected To Grow Again Margins And Pricing Power Margins crossed the zero threshold in Q2-2021, but are still almost 20 percentage points below the long-term average (Chart 12). While hotel costs have increased with the pandemic, this industry has significant pricing power to pass on its costs to consumers (Chart 13). Chart 12The Hotel Industry Has Returned To Profitability Chart 13Hotels Have Significant Pricing Power And Can Pass Extra Costs To Guests Valuations And Technicals The Hotels industry is trading at 30x forward PE and on a 5-year normalized basis, it is trading with a discount to the S&P 500, which is unusual (Chart 14). In terms of our Technical Indicator, the industry is somewhat oversold, and now looks more attractive than it did earlier this year (Chart 15). Chart 14Hotels Are Trading With A Discount To S&P 500 Which Is Unusual Chart 15Hotels Are Slightly Oversold Cruise Lines Cruise Lines were the worst-hit and the slowest to recover among the sub-industries, but they are expected to make a comeback in 2022 with a significant surge in revenue growth. Most of the drivers for these companies are similar to Hotels and Resorts – but recovery is delayed due to restrictions that kept cruise ships anchored much longer than initially expected. Investment Implications We stay with our overweight in Hotels, Resorts, and Cruise Lines. We will summarize the reasons: The Delta variant is cresting. Our base case is that herd immunity is not far off. Of course, the industry is also vulnerable to any new virus scare, and this is a risk that investors need to keep in mind. Rising rates will be a mild tailwind for the industry, as it tends to outperform in that regime. But this is not a key driver of its performance. Consumer confidence and financial wellbeing are at the core of Hotel profitability. So far, Americans still have money to spare and prefer to spend it on services. It is disconcerting that the Consumer Confidence Indicator has turned, but we are not too alarmed just yet: Jobs are still plentiful, and Americans are going back to work. Hotel occupancy has increased, and the amount of money consumers are prepared to spend on hotel stays has surged. Sales are expected to increase by 75%, albeit from lower levels, over the next 12 months. Hotels have also discovered many new sources of revenue. Historical earnings growth is not available as until recently the industry was losing money; however, margins have just turned positive. Companies also have the significant pricing power to pass on expenses to their guests and have the ability to mend their margins, eventually going back to the historical 20%. Lastly, the industry is cheap relative to its own history on a forward PE basis. According to our Technical indicator, it is also oversold. The Hotels, Resorts, and Cruise Lines industry has significant potential to return to its former “glory”, and we believe that it is a sound tactical and cyclical investment. We recommend overweighing this industry. Bottom Line The Hotels, Resorts, and Cruise Lines industry has been severely damaged by the pandemic, and the road to recovery may be long. It is also vulnerable to any new virus scare. However, with Delta cresting, financially healthy US consumers choosing to spend their money on services and experiences, sell-side forecasts pointing to surging sales, and companies possessing substantial pricing power mean that we are bullish on the industry. Irene Tunkel Chief Strategist, US Equity Strategy irene.tunkel@bcaresearch.com Footnotes 1 Restaurants Close Dining Rooms Again as Delta-Driven Infections Spread, WSJ, September 13, 2021. 2 Travel Investors Need More Drive, WSJ, September 12, 2021. 3 Hotel Industry News: Marriott CEO Sees Hotels Bouncing Back Quickly After Delta Variant Slump, Skift, September 9, 2021. 4 IBISWorld, August 23, 2021. 5 Oxford Economics. Recommended Allocation

Highlights Portfolio Strategy Firming leading rail freight indicators signal that intermodal, coal and commodity (ex-coal) carloads are in high demand. Tack on the global economic reopening in the back half of the year and rising commodity prices, and factors are falling into place for a durable outperformance phase in rails. Boost exposure in the S&P rails index to overweight. Recovering lodging demand coupled with restrained industry capacity should restore hoteliers’ pricing power and boost profitability. The S&P hotels, resorts and cruises index remains a high-conviction overweight. Recent Changes Boost the S&P railroads index to overweight, today. On March 9, our 5% rolling stop on the S&P autos & components index was triggered and we lifted exposure to neutral that netted our portfolio 29% in relative gains since the January 25, 2021 inception. This move also augmented the S&P consumer discretionary sector back to a benchmark allocation resulting in a 7.5% gain. Table 1 Feature While President Biden signed a new $1.9tn fiscal package into law last week, valid concerns surrounding the path of the 10-year US Treasury yield added choppiness to the stock market’s consolidation phase (Chart 1). Junk bond spreads stayed calm despite the ongoing Treasury bond market selloff and related MOVE index (bond market volatility) jump and remain a key indicator to monitor in order to gauge if a garden variety equity market pullback can morph into something more significant. Recent empirical evidence suggests that the deviation between the MOVE index and junk spreads will likely return to equilibrium via a settling down of the former, as occurred in the May 2013 taper tantrum episode (Chart 2). Chart 1Choppiness Galore Chart 2A Taper Tantrum Repeat? Importantly, delving deeper in the relationship between bonds and stocks and putting it in historical context is instructive. Our sister Emerging Markets Strategy service recently posited that in the coming years the current negative correlation between stock and bond prices will revert to positive as it prevailed prior to the Asian Crisis (Chart 3). The post-1997 era is largely characterized as disinflationary, while the period from the 1960s to the mid-1990s as primarily inflationary. As a reminder core PCE price inflation was last above the Fed’s 2.5% target in the early 1990s (please see grey zone, top panel, Chart 3). Chart 3From Inflation To Disinflation And Back To Inflation? Importantly, what will cement the correlation between stock prices and bond prices becoming definitively positive anew will be a shift upward of core PCE price inflation. Chart 4 shows that core PCE inflation leads the stock-to-bond correlation by 45 months and can serve as a confirming signpost that bonds will no longer offer downward protection to stocks and likely render risk parity useless. Chart 4Joined At The Hip, Albeit With A Lag If this paradigm shift is indeed taking root, this raises two questions: First, how will the broad equity market perform during a more persistent bond market selloff phase? Second, what equity sectors will likely outperform under such a scenario and which ones should equity investors avoid/underweight in their portfolios? Our analysis centered on historically significant bond market selloffs, which we clearly depict in the shaded areas in Chart 5. Chart 5Don’t Fear The Bond Bear Table 2 shows the results of our analysis broken down in two separate eras. Between the 1960s and the early-1990s, “the inflation era”, we use monthly data, whereas from the early-1990s onward, “the disinflation era”, we use high quality daily data. In the seven inflationary iterations the SPX median fall was 3%,1 whereas in the nine disinflationary episodes the SPX median rise was 18%.2 Impressively, since the LTCM debacle every single bond market selloff has been cheered by the stock market (Table 2). Table 2SPX Returns During Bond Bear Markets Table 3 delves deeper into GICS1 sectors and compares relative returns to the SPX during sizable bond market selloffs. Table 3US Equity Sector Returns During Bond Bear Markets During “the inflationary era” deep cyclicals outperformed the broad market, whereas early cyclicals trailed the SPX. The defensives’ performance is split down the middle with telecom and utilities faring poorly, while health care and staples outshining the SPX. One surprising result is that during “the inflationary era” relative tech performance was very resilient compared with what one would expect. There is an accentuation of relative returns in “the disinflationary era”, with all the defensives significantly underperforming and the deep cyclicals broadly outshining the SPX. Early cyclicals make a U-turn and are clear outperformers. One surprising result is the energy sector’s negative median return. Finally, the real estate sector’s significant underperformance really stands out in “the disinflationary era”. Netting it all out, the broad equity market has historically risen consistently in tandem with a bond market sell off primarily in “the disinflationary era”. Impressively, the SPX has been resilient on average even in “the inflationary era”; granted there have also been some notable drawdowns (Table 2). The implication is that at the current juncture the SPX may have some trouble digesting the bond market’s rapid selloff, but will recover smartly especially as the bond market selloff eventually proves more reflective of growth rather than restrictive. (For inclusion purposes, the appendix on page 16 shows the GICS1 sector performance since the 1960s with shaded areas depicting periods of significant bond market selloffs, and similar to Chart 3 the appendix on page 19 plots the relative share price monthly returns correlation to bond price monthly returns.) This week, we update our high-conviction overweight view on an early-cyclical sub-group with a reopening tailwind, and lift a deep cyclical transportation index to an above benchmark allocation. Hop Back On The Rails The Dow Theory is in full force and serves as a confirmation of the breakout in the Dow Industrials recently, as transports have been firing on all cylinders of late, and is also a harbinger of new all-time relative share price highs in railroads (Chart 6). Today we recommend investors get back on board the rails, a key transportation sub group, and lift exposure from neutral to overweight. Chart 6Dow Theory Green Light Leading indicators in all three key rail freight categories suggests that the railroad rebound is still in the early innings. The V-shaped recovery in the ISM manufacturing and services surveys is underpinning total rail shipments and signals that our rail diffusion indicator has more upside (Chart 7). Chart 7All Aboard… The Cass Freight Index shipments and expenditures components are also on a tear and corroborate that demand for rail freight services is robust. The upshot is that still beaten down sell-side analysts’ relative revenue growth estimates will likely surprise to the upside (Chart 8). Importantly, our Railroad Indicator does an excellent job in capturing this firming rail demand backdrop and signals that relative share price momentum has more room to rise (second panel, Chart 9). Chart 8...The Rails Chart 9Intermodal Is On Fire On the intermodal front, the back half of the year economic reopening due to the population’s inoculation along with President Biden's freshly signed fiscal spending bill suggest that retail related hauling services will pick up steam. The overall business sales-to-inventories (S/I) ratio in general and the retail S/I ratio in particular corroborate the upbeat demand outlook for intermodal carloads (third panel, Chart 9). Similarly, the LA port is as busy as ever as containerships are arriving non-stop full of cargo from China (bottom panel, Chart 9). On the commodity front, coal shipments are staging a comeback from extremely depressed levels and there is scope for a jump to expansionary territory especially given the soaring natural gas prices (second & middle panels, Chart 10). With regard to the broad commodity complex (excluding the historically large coal carload category) the demand profile for rail services is as upbeat as ever. Not only are commodity prices galloping higher, but also BCA’s Global Leading Economic Indicator is steeply accelerating painting a bright picture for rail hauling (fourth & bottom panels, Chart 10). Moreover, the surging global PMI signals that the global economic recovery is also on the ascent, which bodes well for relative profit growth (middle panel, Chart 11). Chart 10Commodity Carloads Set To Surge Chart 11Global Recovery Is A Tailwind Importantly, on the operating front our railroad industry profit margin proxy is at an historically wide level and underscores that the path of least resistance is higher for margins (Chart 11). Thus, rail profits are highly levered to industry pricing power that is on the cusp of spiking higher, especially if our thesis of the firming rail demand backdrop is accurate. The implication is that a rerating phase is in the cards for the S&P railroads index (middle panel, Chart 12). Finally, our EPS macro model has slingshot higher and suggests that rail earnings have a long runway ahead (bottom panel, Chart 12). Netting it all out, firming leading rail freight indicators signal that intermodal, coal and commodity (ex-coal) carloads are in high demand. Tack on the global economic reopening and rising commodity prices, and factors are falling into place for a durable outperformance phase in rails. Bottom Line: Boost the S&P rails index to overweight, today. The ticker symbols for the stocks in this index are: BLBG: S5RAIL – CSX, KSU, NSC, UNP. Chart 12Pricing Power Holds The Key Stay Checked In To Hotels In late-November we boosted the S&P hotels, resorts & cruises index to overweight and got some eyebrows raised from our diverse client base. Subsequently, we added this niche consumer discretionary sub-group to our high-conviction overweight list for 2021 and the client pushback intensified. Today, we reiterate our high-conviction call on the S&P hotels, resorts & cruises index that has already added alpha to our portfolio to the tune of 17% since inception. While relative share price momentum has climbed of late and relative valuations have troughed, our sense is that the re-rating phase is just getting under way (Chart 13). As the global push for COVID-19 vaccinations heats up, the semblance of normality will serve as a catalyst to unlock excellent value in hotels. True, lodging services demand is as downbeat as ever, but this index is a prime beneficiary of the reopening trade. Pent-up services demand will get unleashed with consumers likely indulging on more lavish vacationing starting this Memorial Day. Rising government transfers, a soaring savings rate and increasing incomes all augur well for lodging demand and is also corroborated by our hotels demand indicator (Chart 14). Tack on firming consumer sentiment and the ISM services index staying squarely above the 50 expansion line, and the industry’s demand outlook lifts further. Chart 13A Valuation Re-rating Phase Looms Chart 14Leading Demand Indicators Give The All-clear Given that hotel capacity has been restrained, there are high odds that upbeat demand will likely catch hoteliers unprepared to fulfil it, and thus causing a jump in selling prices (Chart 15). Business travel is also slated to return as a flexible work place environment becomes the norm and the need to meet clients and prospects in order to conduct business will come back with a vengeance. The implication is that beaten down industry profit margins will recover smartly and boost lodging profitability especially given the collapse in the industry’s wage bill (Chart 15). Finally, our S&P hotels, resorts & cruises macro sales model encapsulates all these moving parts and signals that the budding recovery in revenue growth will gain momentum in the back half of the year (Chart 16). Chart 15Widening Margins Will Restore Profitability Chart 16Macro-based Revenue Growth Model Points To A V-shaped RecoveryAdding it all up, recovering lodging demand coupled with restrained industry capacity should restore hoteliers’ pricing power and boost profitability. Bottom Line: We reiterate the high-conviction overweight status in the S&P hotels, resorts and cruises index. The ticker symbols for the stocks in this index are: BLBG: S5HOTL – MAR, HLT, CCL, RCL, NCLH. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Appendix Chart A1 Chart A2 Chart A3 Chart A4 Chart A5 Chart A6 Footnotes 1 Given the different time frames of the bond market selloffs we decided to show annualized equity returns. 2 Ibid. Current Recommendations Current Trades Strategic (10-Year) Trade Recommendations Size And Style Views February 24, 2021 Stay neutral cyclicals over defensives January 12, 2021 Stay neutral small over large caps June 11, 2018 Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, ABNB, V). January 22, 2018 Favor value over growth