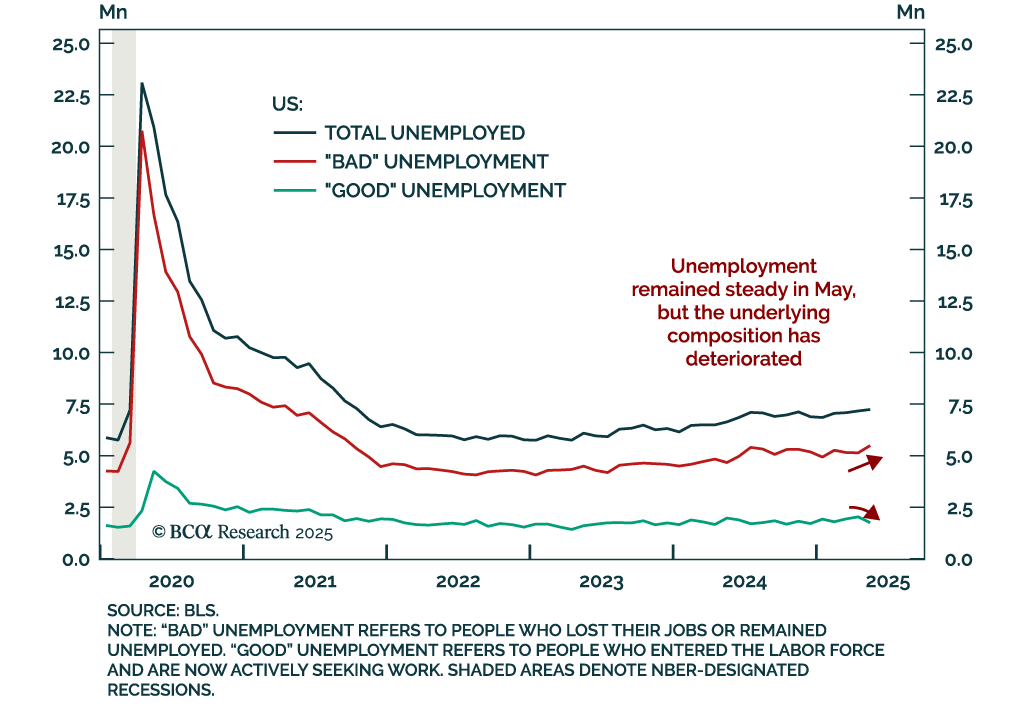

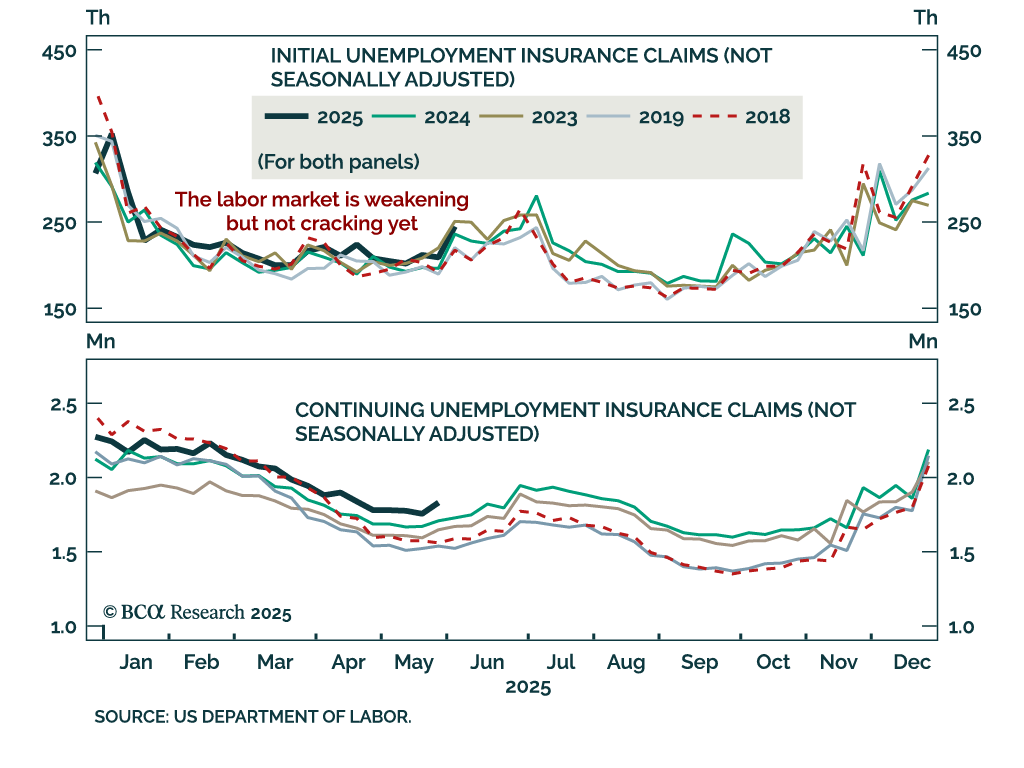

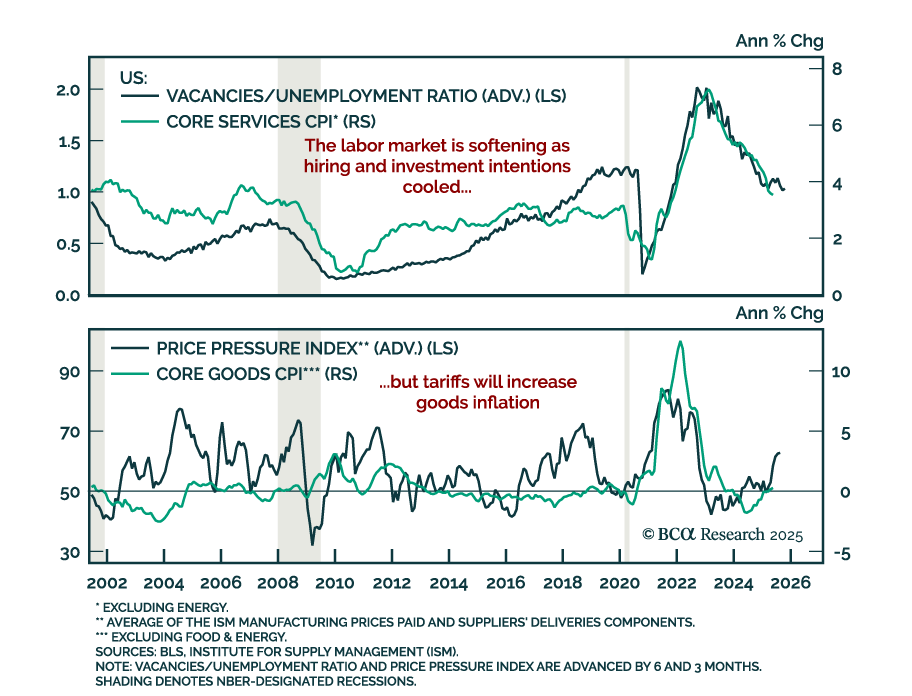

Labor Market

Provided that humanity can overcome the existential risks posed by AI, real incomes will rise. Although most workers will ultimately gain from the transition to an AI-dominated economy, the biggest winners will be those who control the land and the natural resources beneath it.

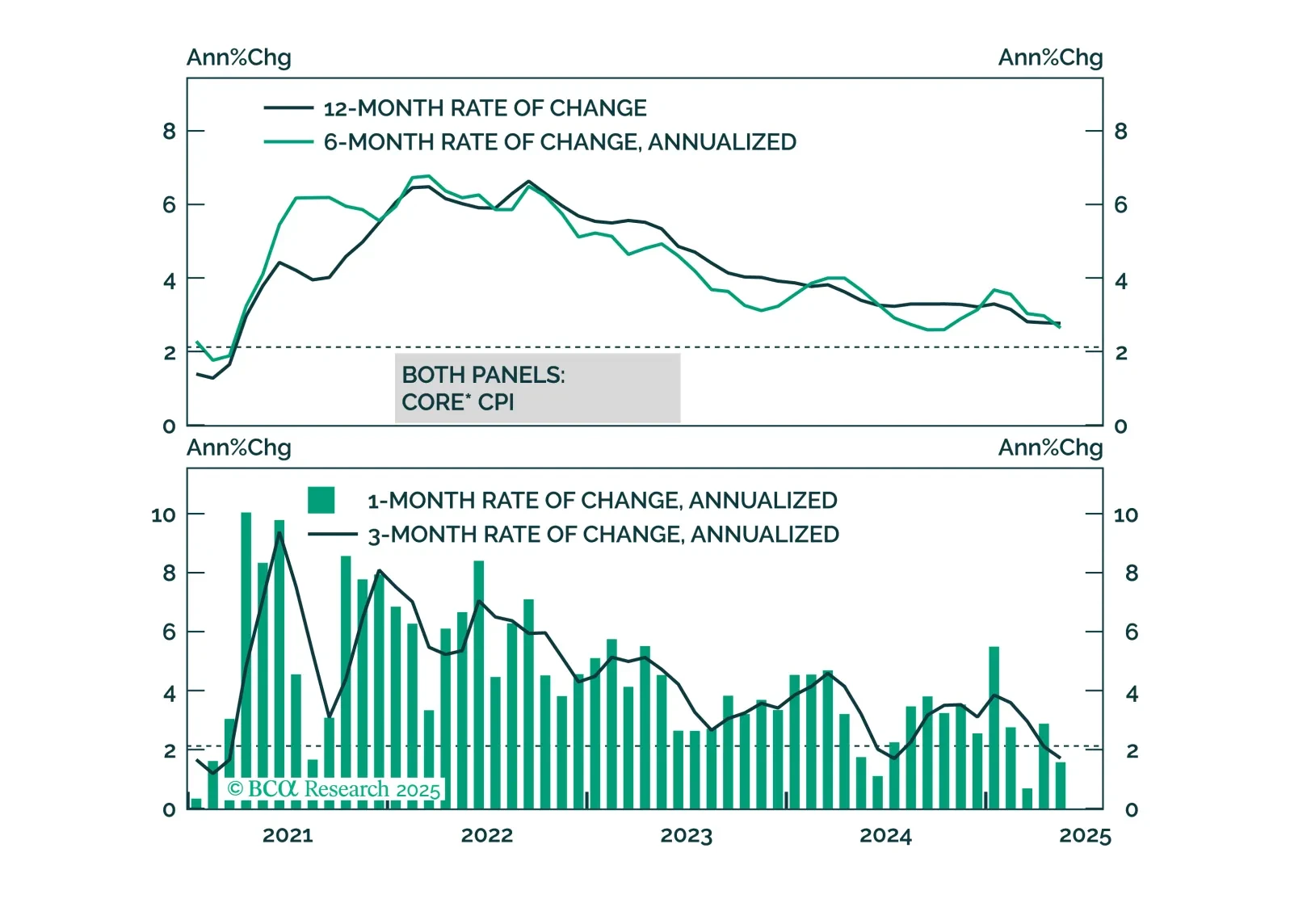

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

The US economy has held up better so far this year than we had expected. For the time being, investors should remain modestly underweight equities. A more aggressive underweight would be justified only once the “whites of the recession’s eyes” are visible.

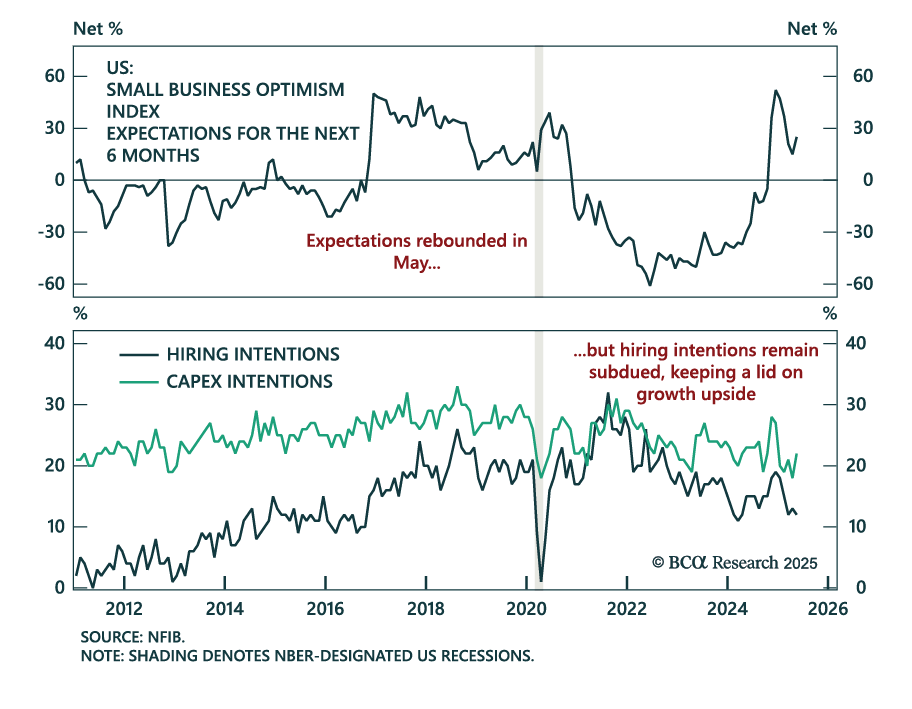

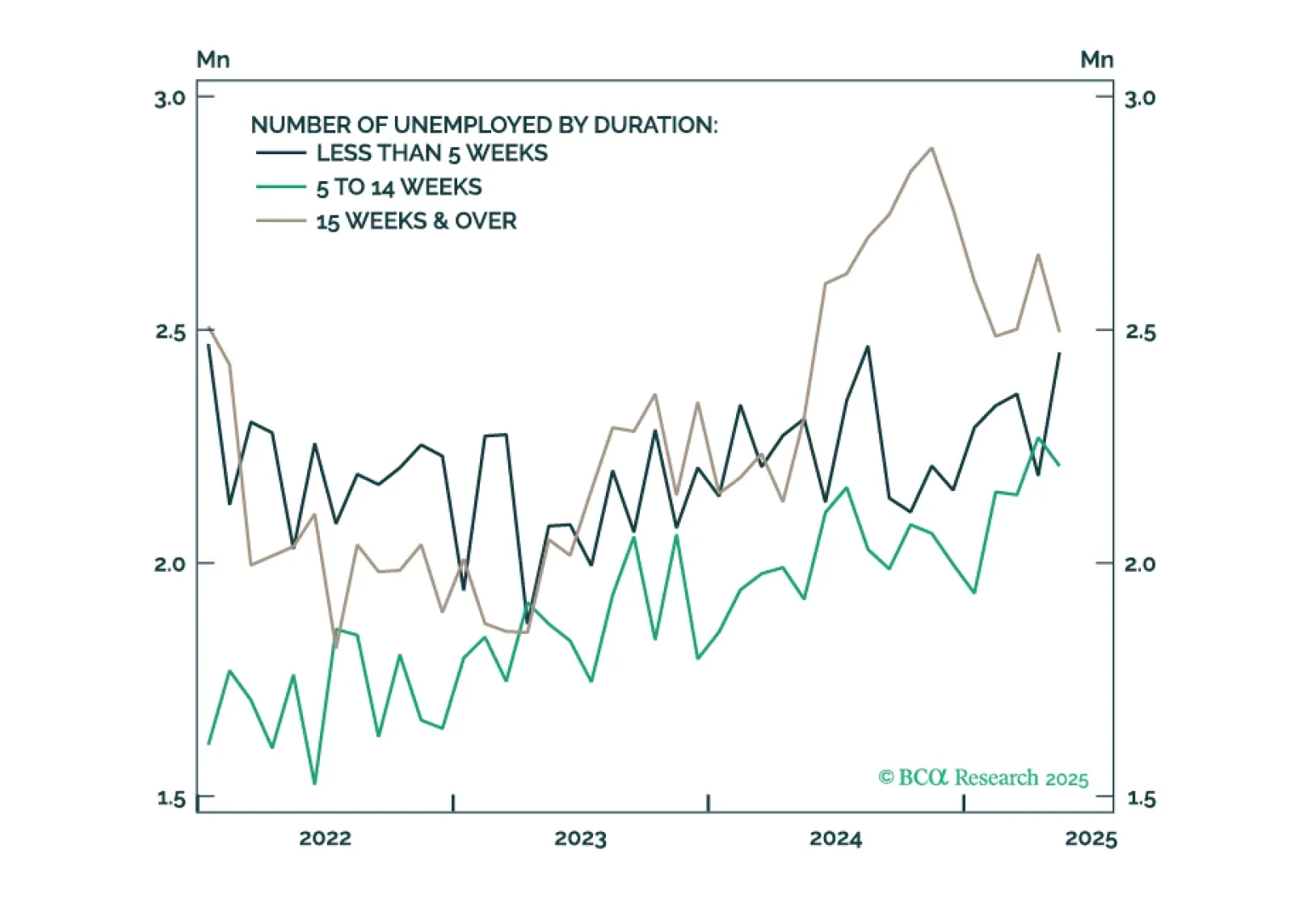

For now, measures of labor market utilization (like the unemployment rate) are only gradually weakening. But we know from history that these trends have a habit of quickly accelerating in advance of recession.