Monetary

Chinese equities are extending their gains following the end of the Lunar New Year holiday. Onshore stocks have gained 9.0% since February 5, outperforming the global benchmark by 7.5 percentage points over this period. Similarly, the MSCI Investable index –…

We rank the US spread sectors in terms of risk versus reward.

The US Conference Board’s Leading Economic Index (LEI) fell by 0.4% m/m in January, following a 0.1% m/m drop in December – disappointing expectations of a milder decline. This marks the 23rd consecutive monthly decrease and has pushed down the index to its…

Chinese policymakers surprised on Tuesday with greater-than-anticipated easing for the troubled property market. Although the 1-year loan prime rate (LPR) – the benchmark for most household and corporate loans – was kept unchanged at 3.45%, the 5-year LPR –…

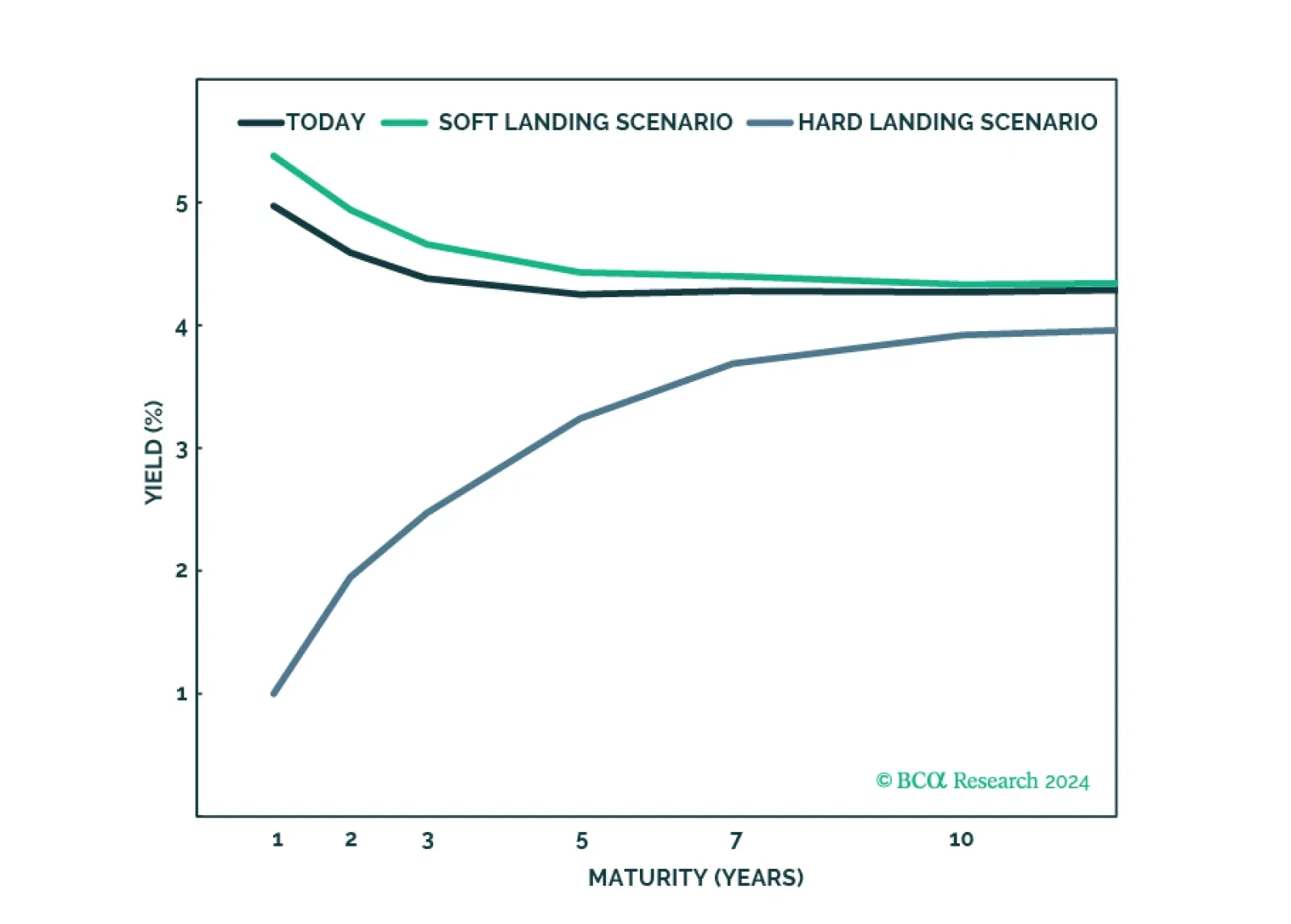

US Treasuries have been selling off over the past two months as investors downgrade the odds of an imminent start to the Fed’s easing cycle. Naturally, a question facing investors is whether current levels constitute a good opportunity to increase duration…

The stronger-than-anticipated acceleration in Sweden’s headline CPI inflation is unlikely to derail the Riksbank’s plan to pivot to policy easing this year. In particular, base effects from lower energy prices a year ago are behind the 1-point increase in…

The S&P 500 forged a new all-time high last Thursday and ended the week with a 4.9% year-to-date gain, extending the rally that started in late-October. Interestingly, the recent increase comes even though investors have priced out a Fed rate cut in March…

Much of the focus of investors concerned about lingering price pressures has been on services prices. There is good reason for that. Even though core CPI inflation remains relatively elevated at 3.9% y/y in January, core goods prices fell by 0.3% y/y and are…

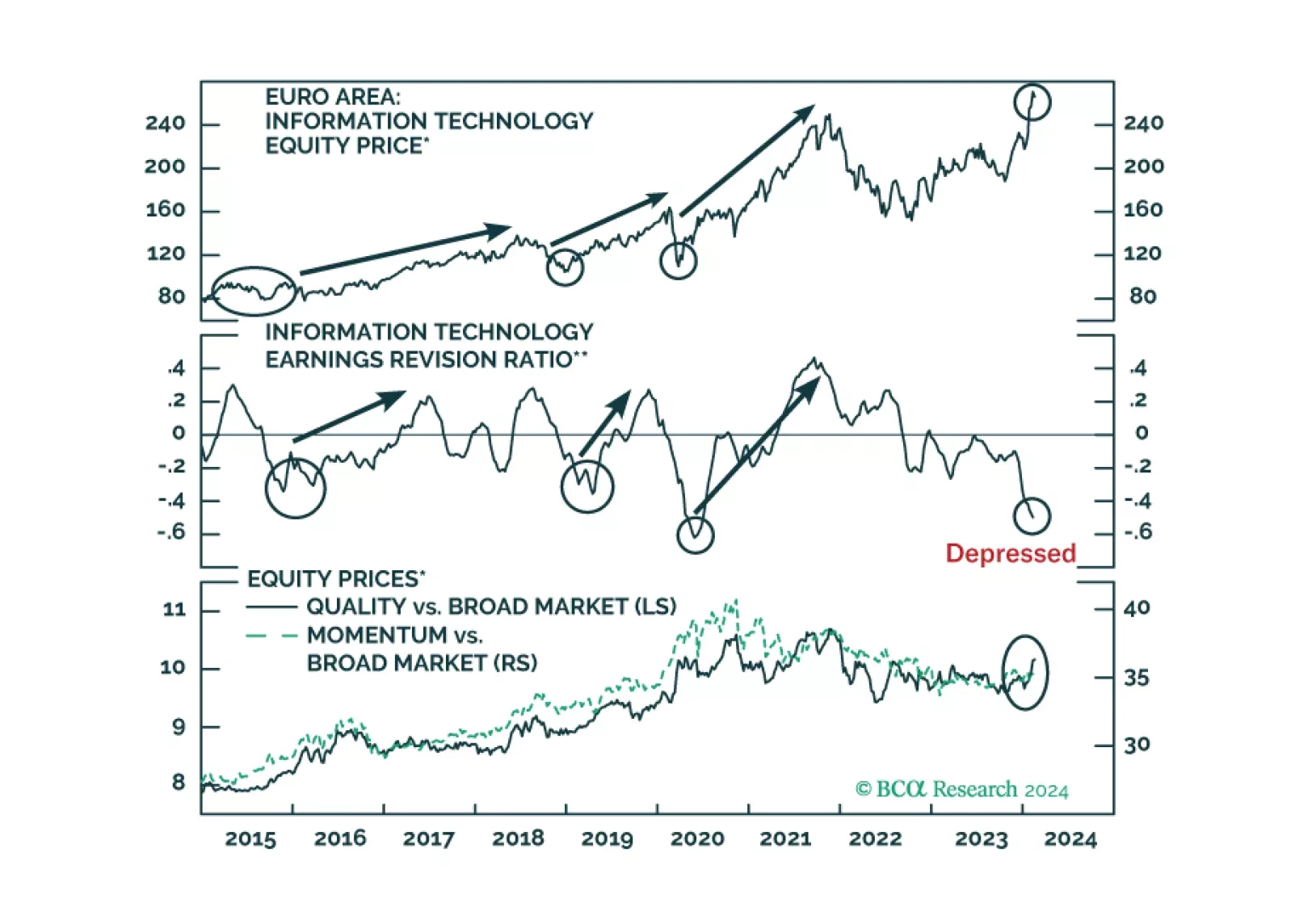

Signs that we are entering the last phase of a bubble are building up. Can European equities benefit from a new tech mania?

Households have ramped up their cash holdings since the end of 2019, but the absence of an empirical link between cash and consumption leads us to believe that we’ve modestly overestimated the risk of consumer-driven overheating.