US Dollar

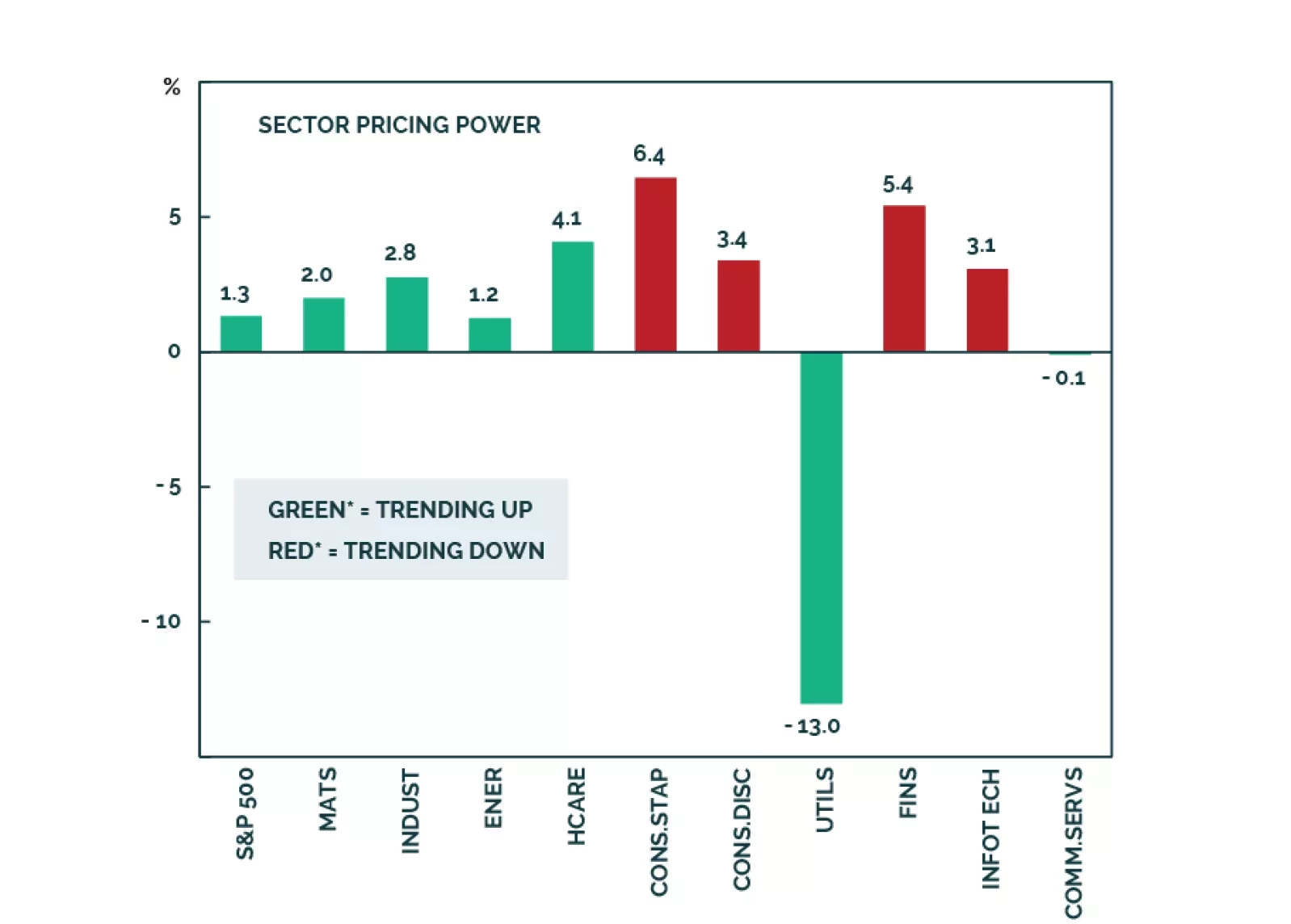

Q3 earnings commentary has been broadly positive, despite intensifying macro headwinds. Going forward, a negative growth outlook and geopolitical risks, are a threat to buoyant earnings expectations. We project that earnings growth for 2024 will move lower than currently projected - a negative for equities. This Santa Claus rally is unlikely to be the start of a new bull market.

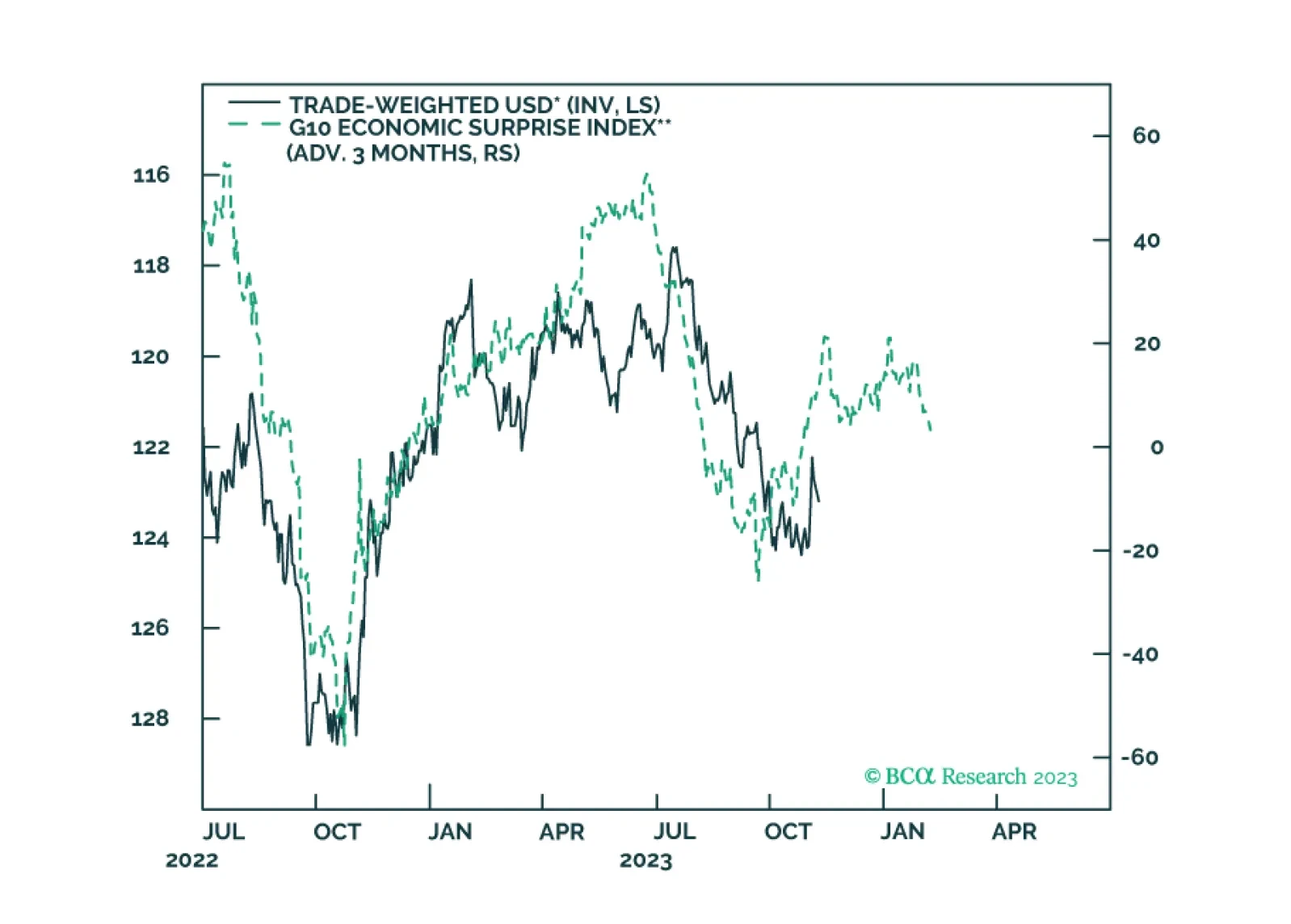

In this report, we go around the globe and survey the near-term outlook for G10 currencies. Our longer-term view on the dollar has been clear, we are sellers. In this report, we review if a tactical sell is also warranted given incoming data and the message from our models.

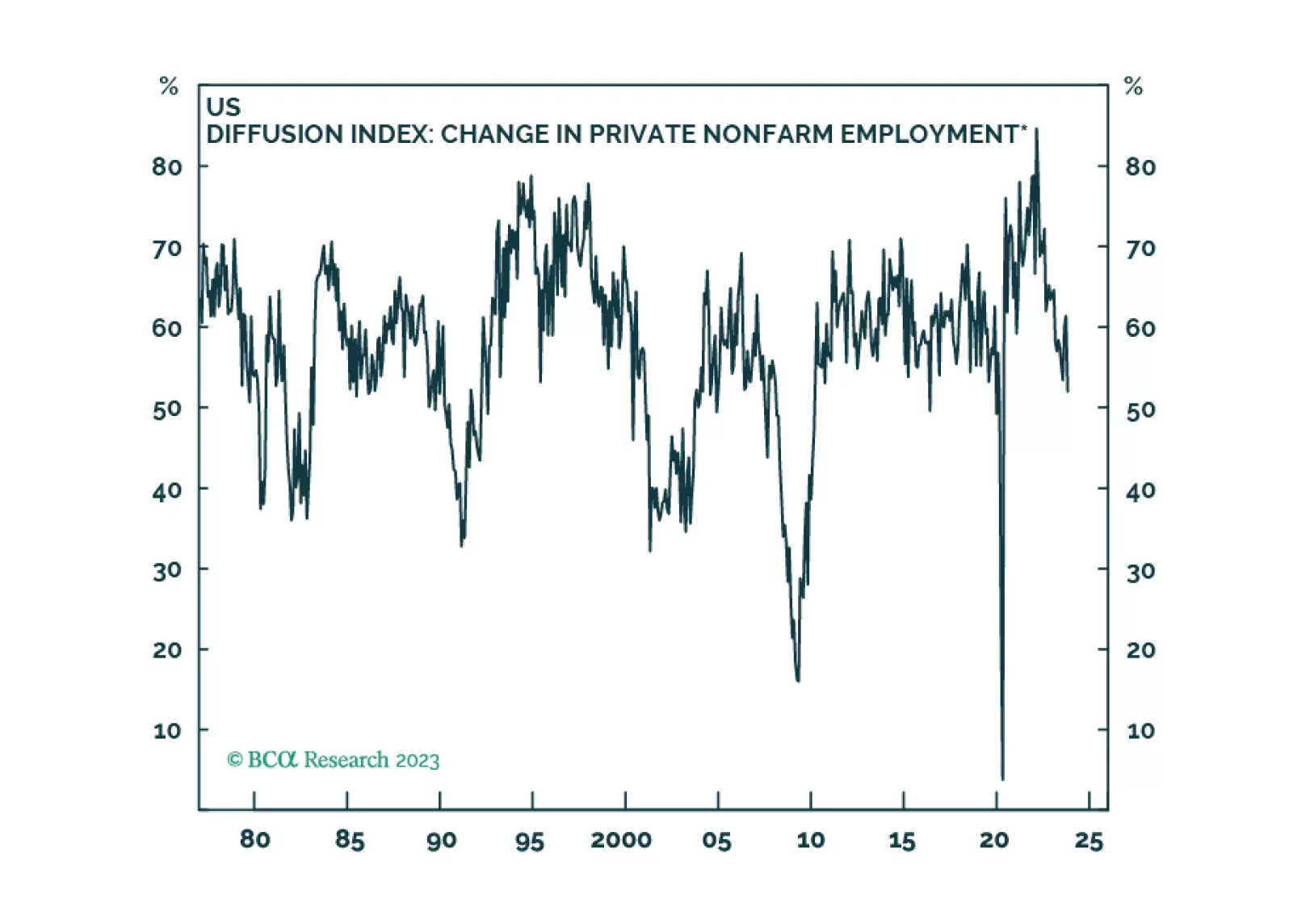

Labor markets are softening in most developed economies, as is usually the case in the lead-up to recessions. Our base case is that the global recession will begin in the second half of 2024, but we will be monitoring our MacroQuant model on a daily basis for confirmation.

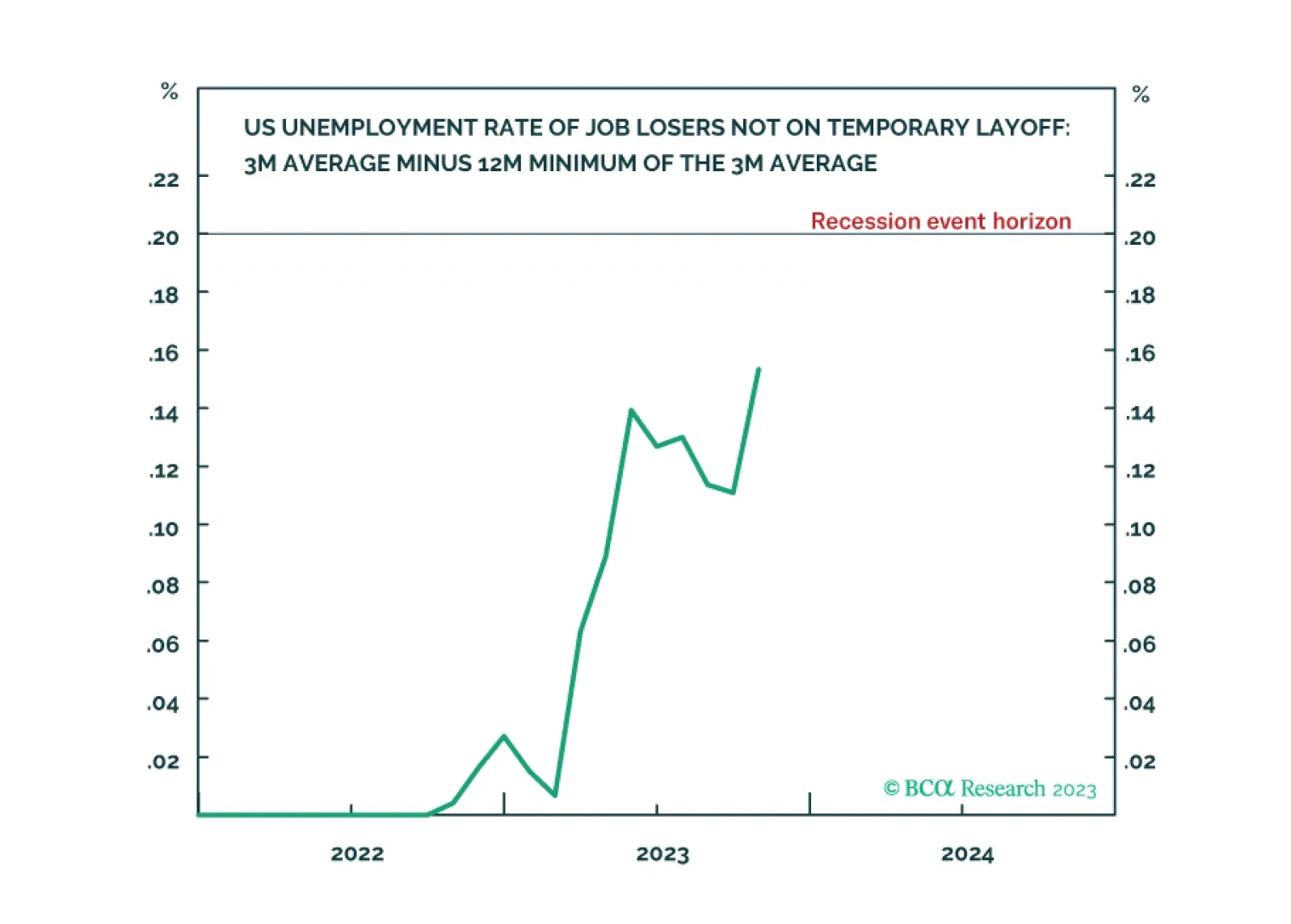

Following the October US jobs data, the ‘Joshi rule’ real-time US recession indicator increased from 0.11 to 0.15, meaning that it is fast approaching its event horizon of 0.20. We go through the investment implications. We also highlight a new long-term recommendation. Plus, the Norwegian krone is close to a potential rebound.

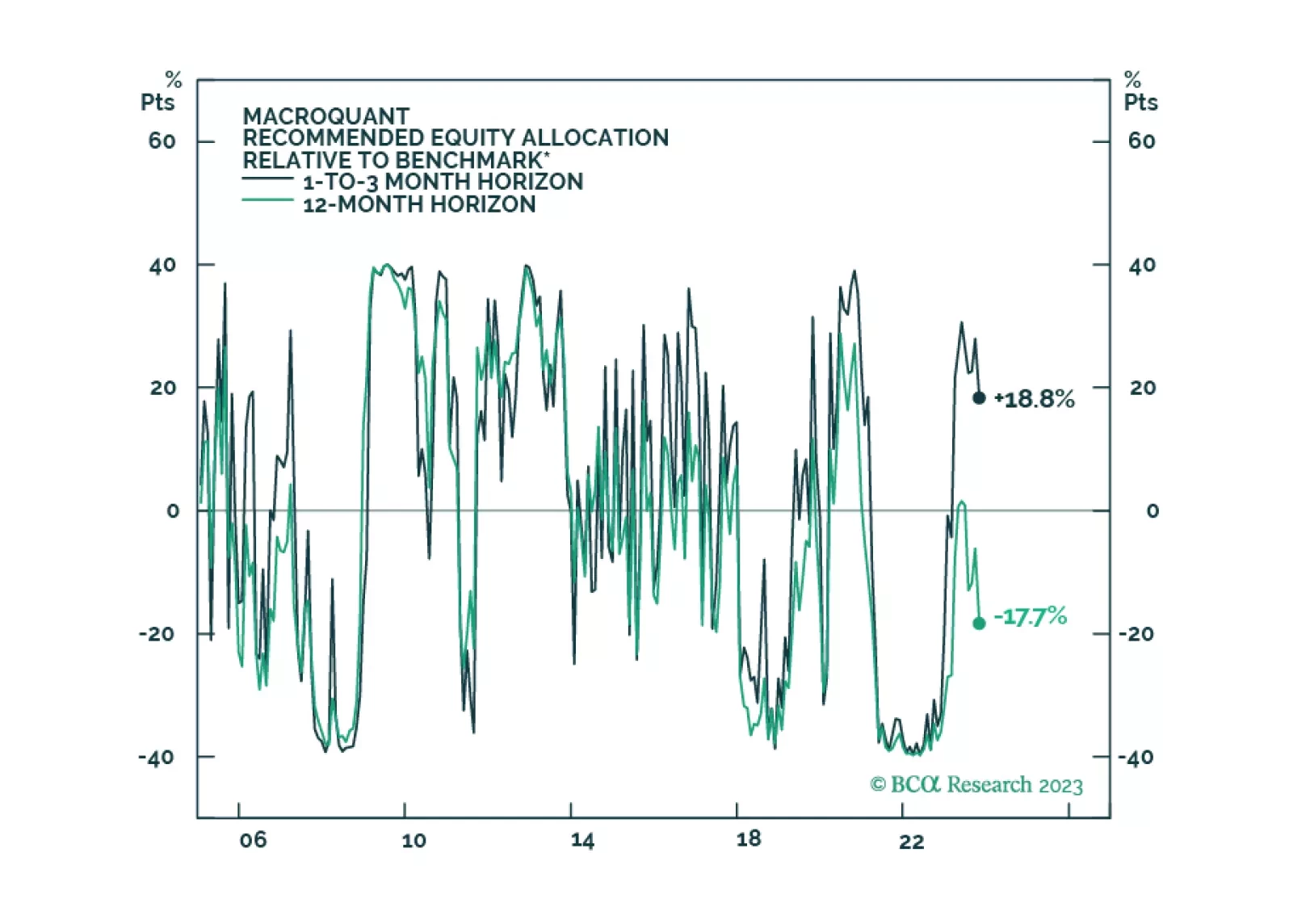

We are approaching another phase transition from boom to bust. Stocks should rally into year-end, but investors should look to reduce equity exposure early next year while increasing bond exposure.

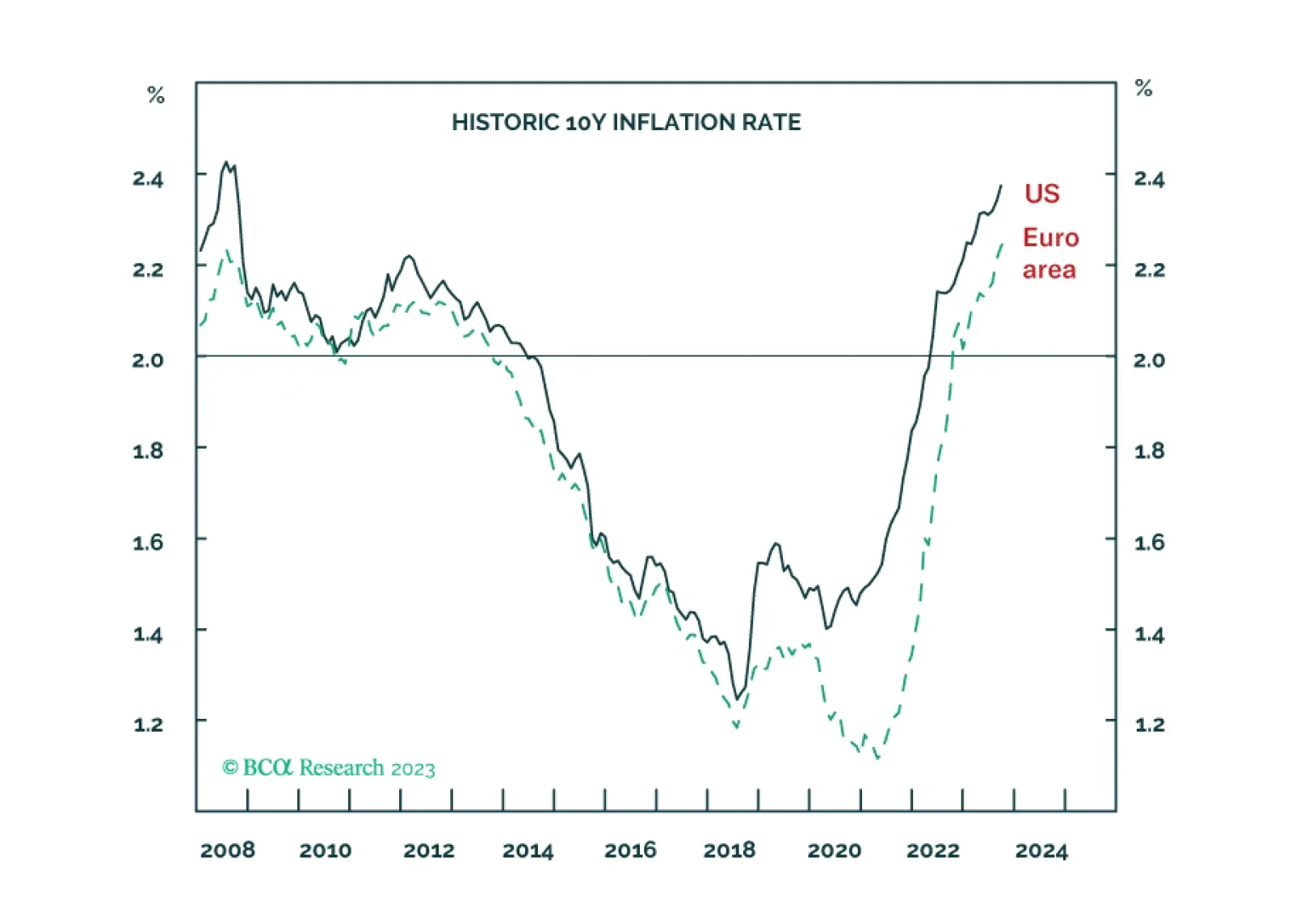

The fundamental component of long-term inflation expectations has climbed to its highest level since 2008 in both the US and the euro area. This means that both the Fed and the ECB will need to engineer inflation to undershoot 2 percent for an extended period if they are to maintain their 2 percent inflation targets. We explain what this means for investment strategy over the coming 6-12 months. Plus, we pinpoint what to focus on in this Friday’s US jobs report. And we identify food and beverages (PBJ) and the Indonesian rupiah (IDR/USD) as excellent rebound candidates.

High interest rates will eventually cause growth to slow. Signs of stress are already starting to show. Stay cautiously positioned.

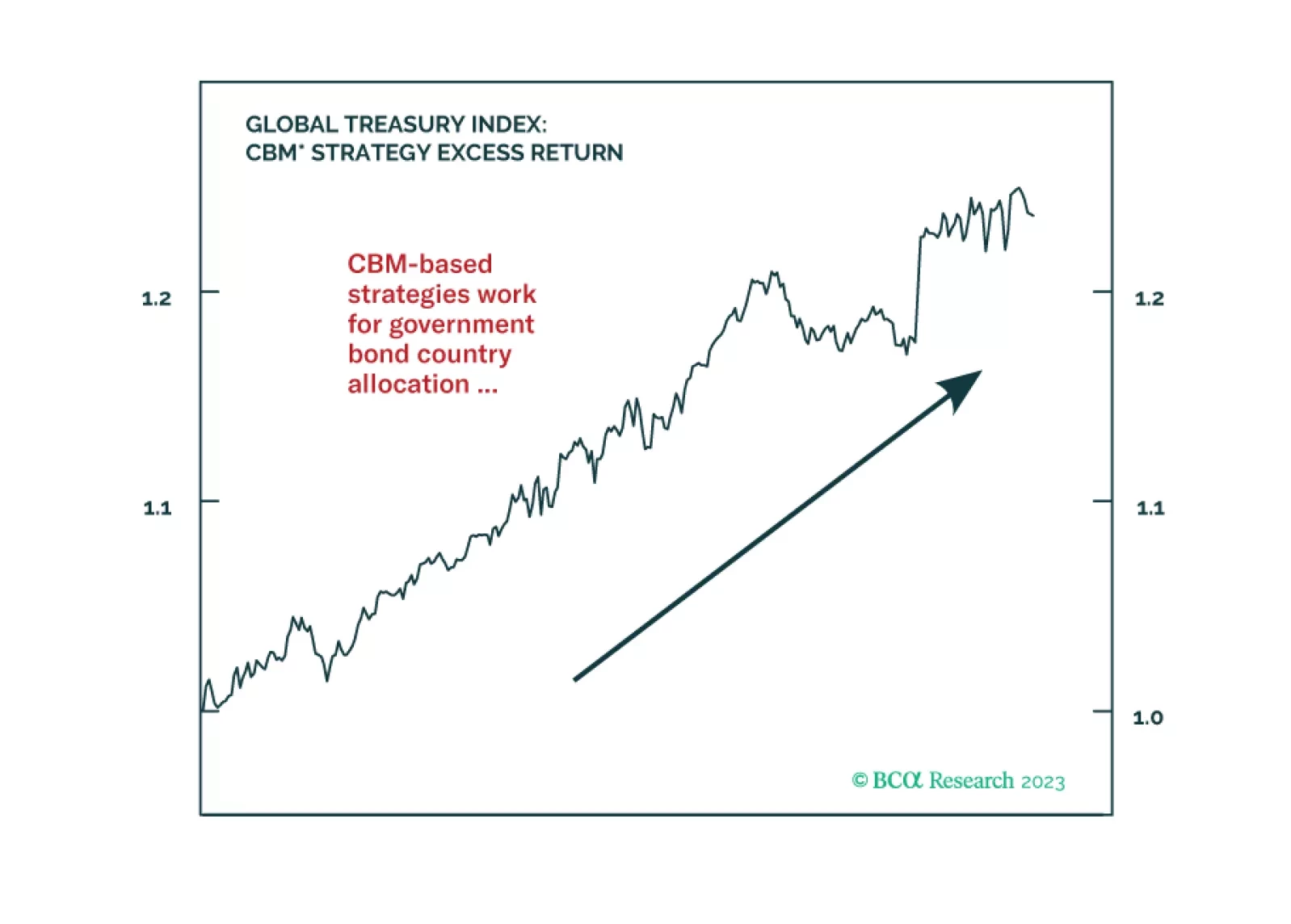

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.