AI

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

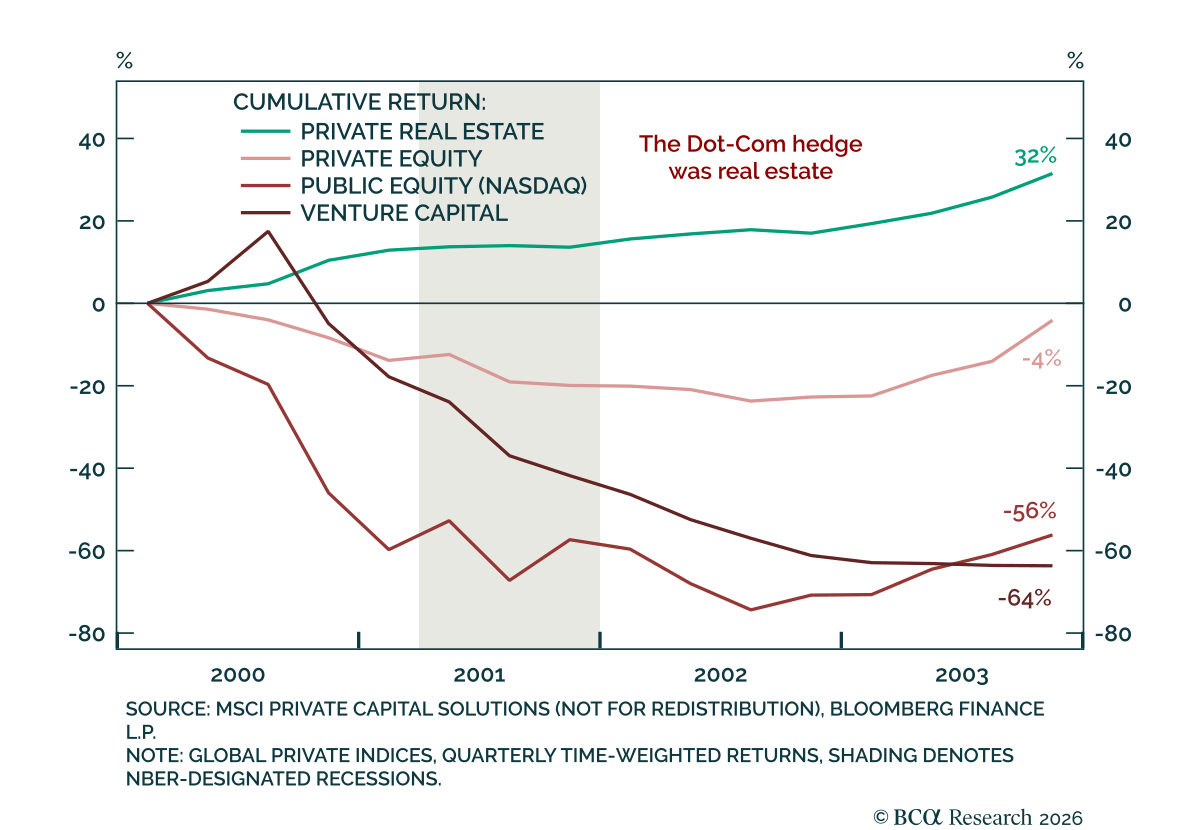

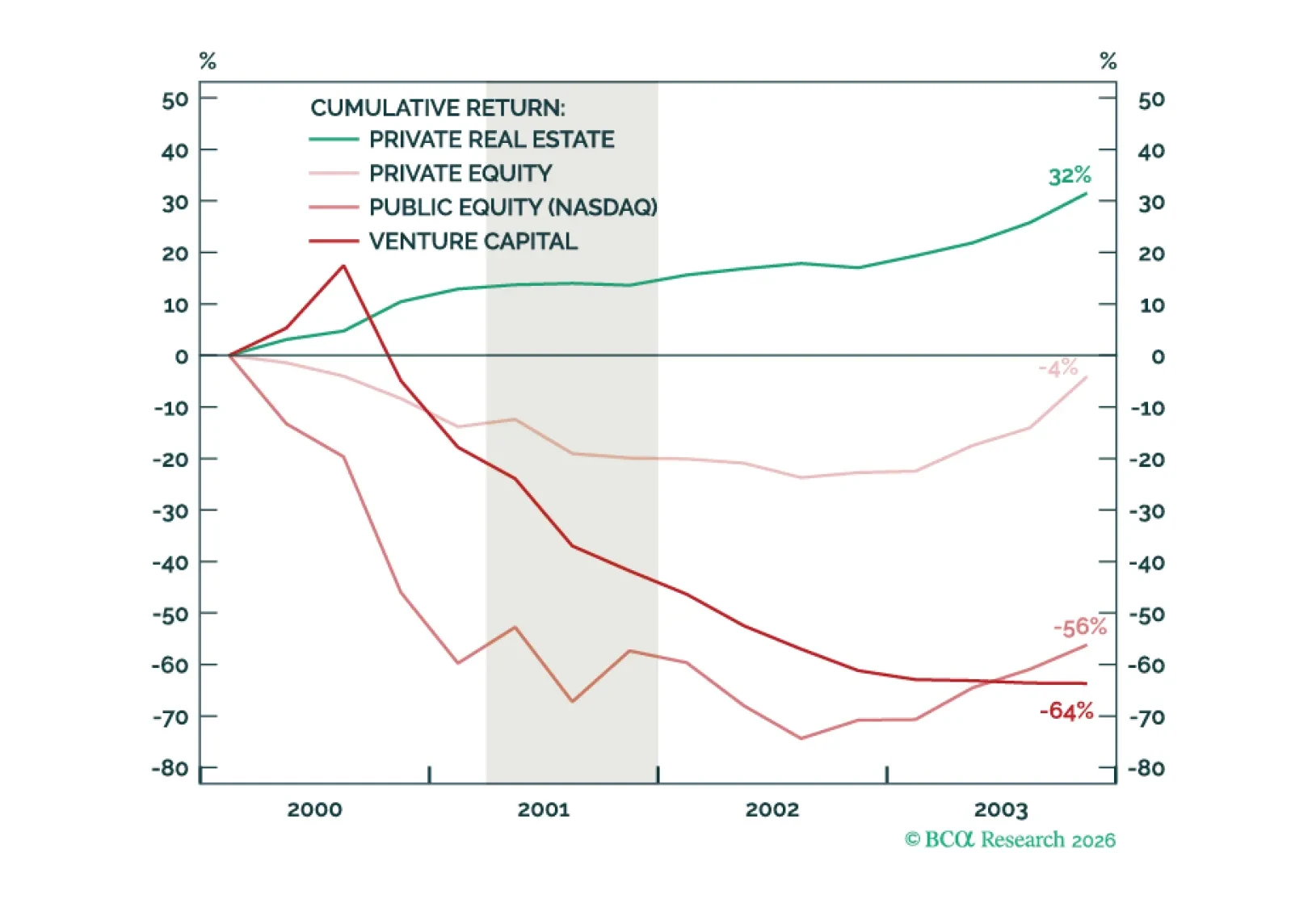

AI dominates markets, but concentration is risk. Real Estate is the diversifier. It outperformed during the Dot-Com bust and will do so again if the AI trade unwinds. Even Office, the sector arguably most exposed to AI disruption, will prove more resilient than bears expect.

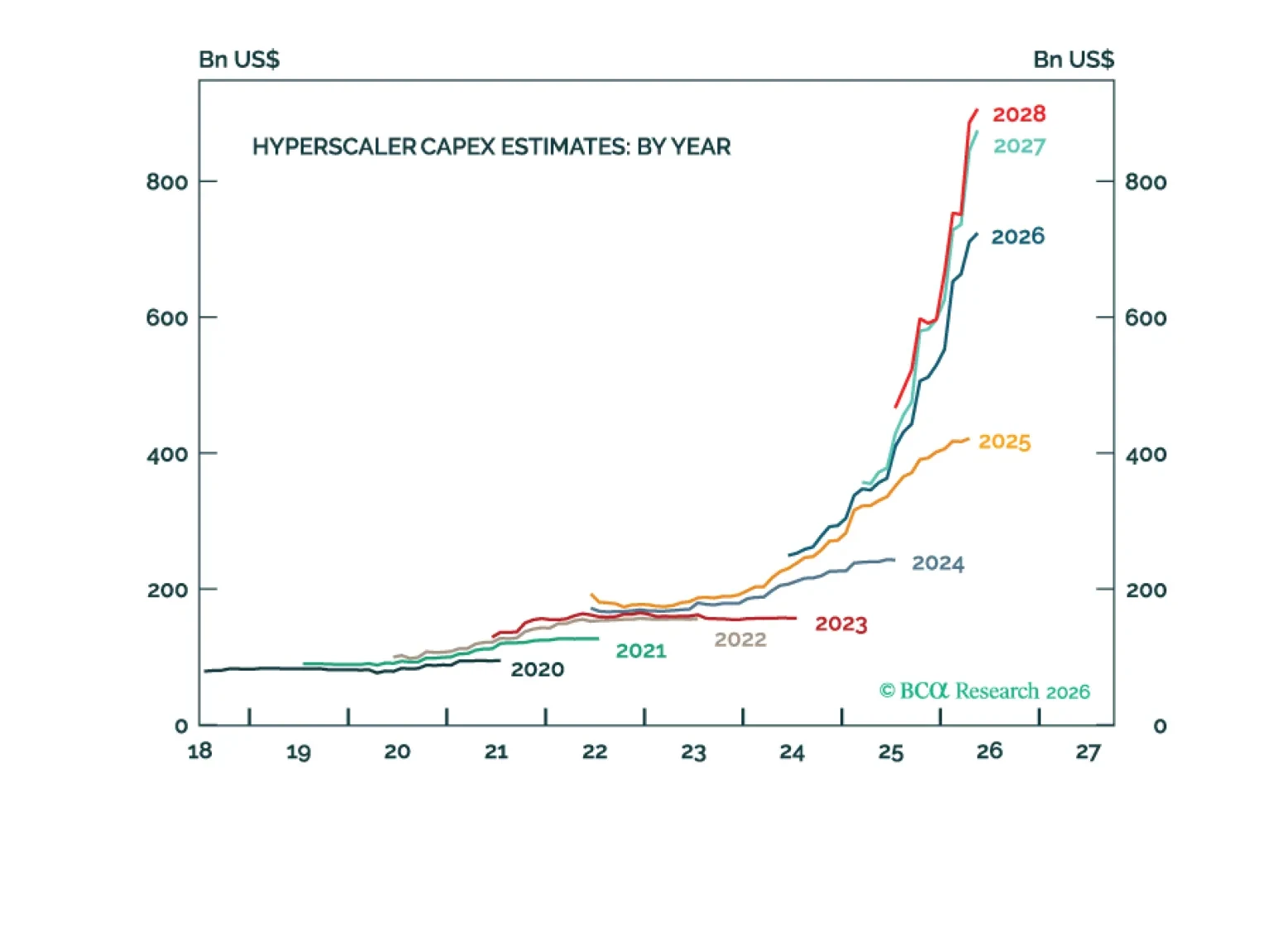

A surefire way to make money is to buy stocks in industries experiencing shortages. AI supply-chain bottlenecks will persist for the next few years but markets will price in relief before then.

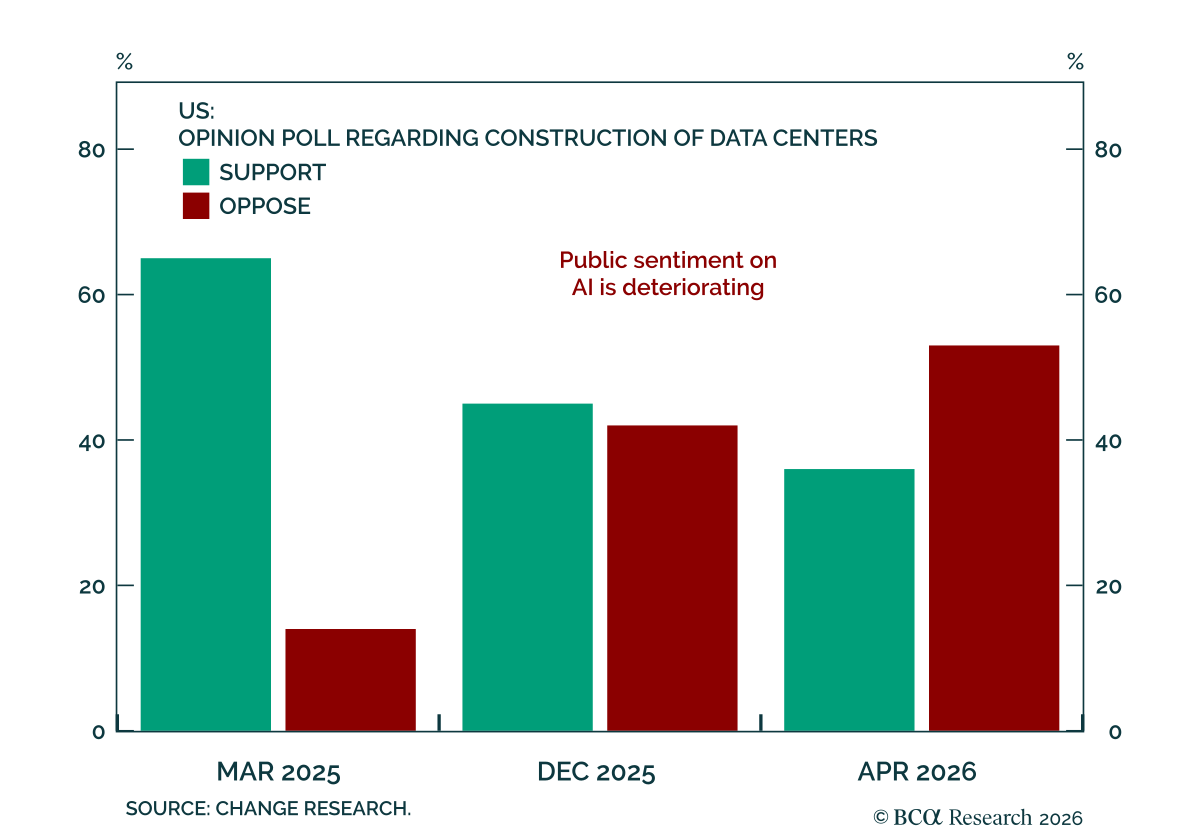

The populist backlash against AI could result in bipartisan regulation in 2027, but is especially likely to prompt tax hikes from 2029.

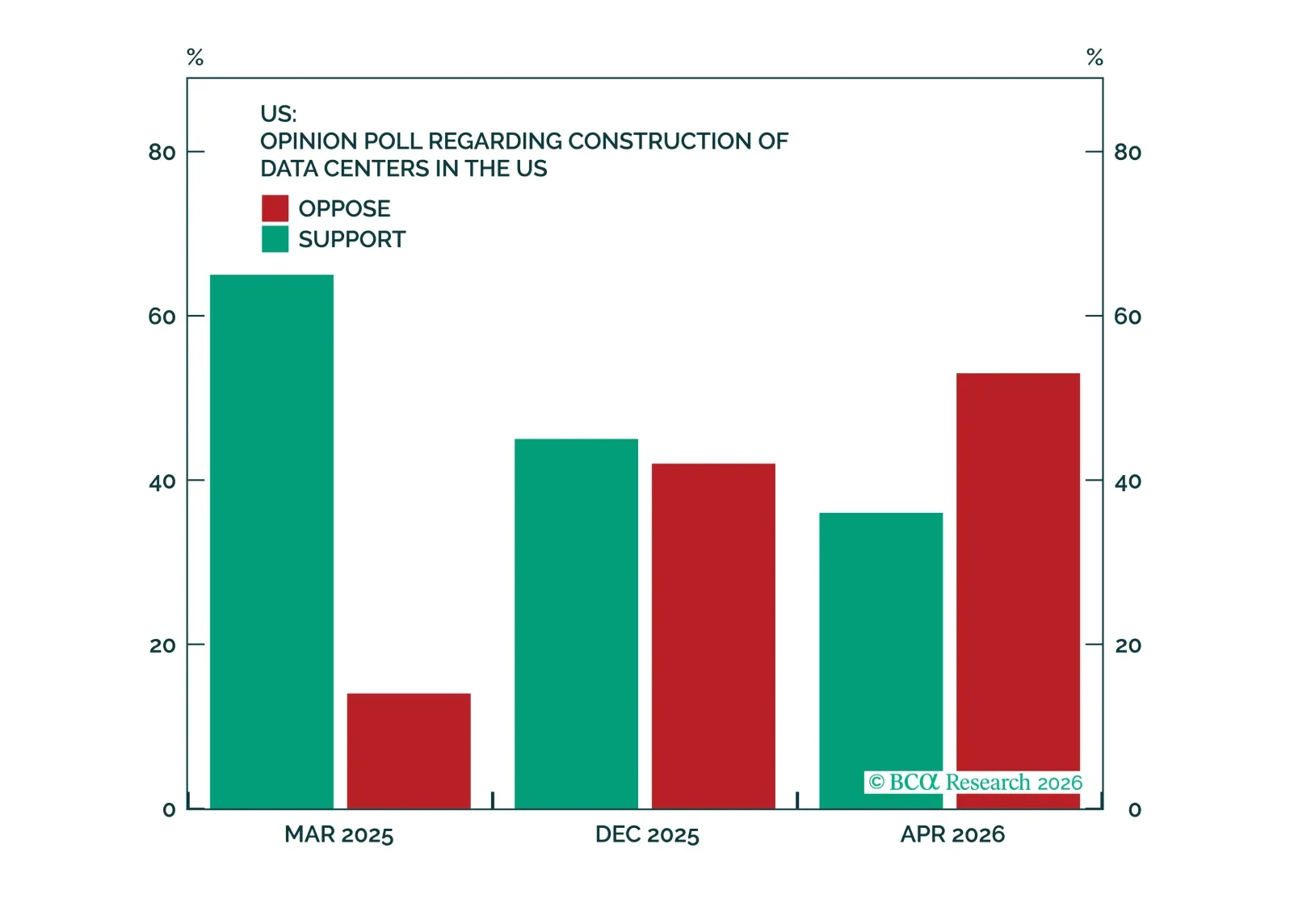

Based on 40 years of history and some 12,000 IPOs, the evidence suggests that the coming IPO wave may dampen forward market returns, mute further multiple expansion, and possibly interrupt sector trends. That said, even monster-sized IPOs are unlikely to trigger a sustained bear market: only about 20% of mega-IPOs coincide with market peaks. The bigger risk is AI leadership rotation as new listings dilute scarcity premia in existing winners.

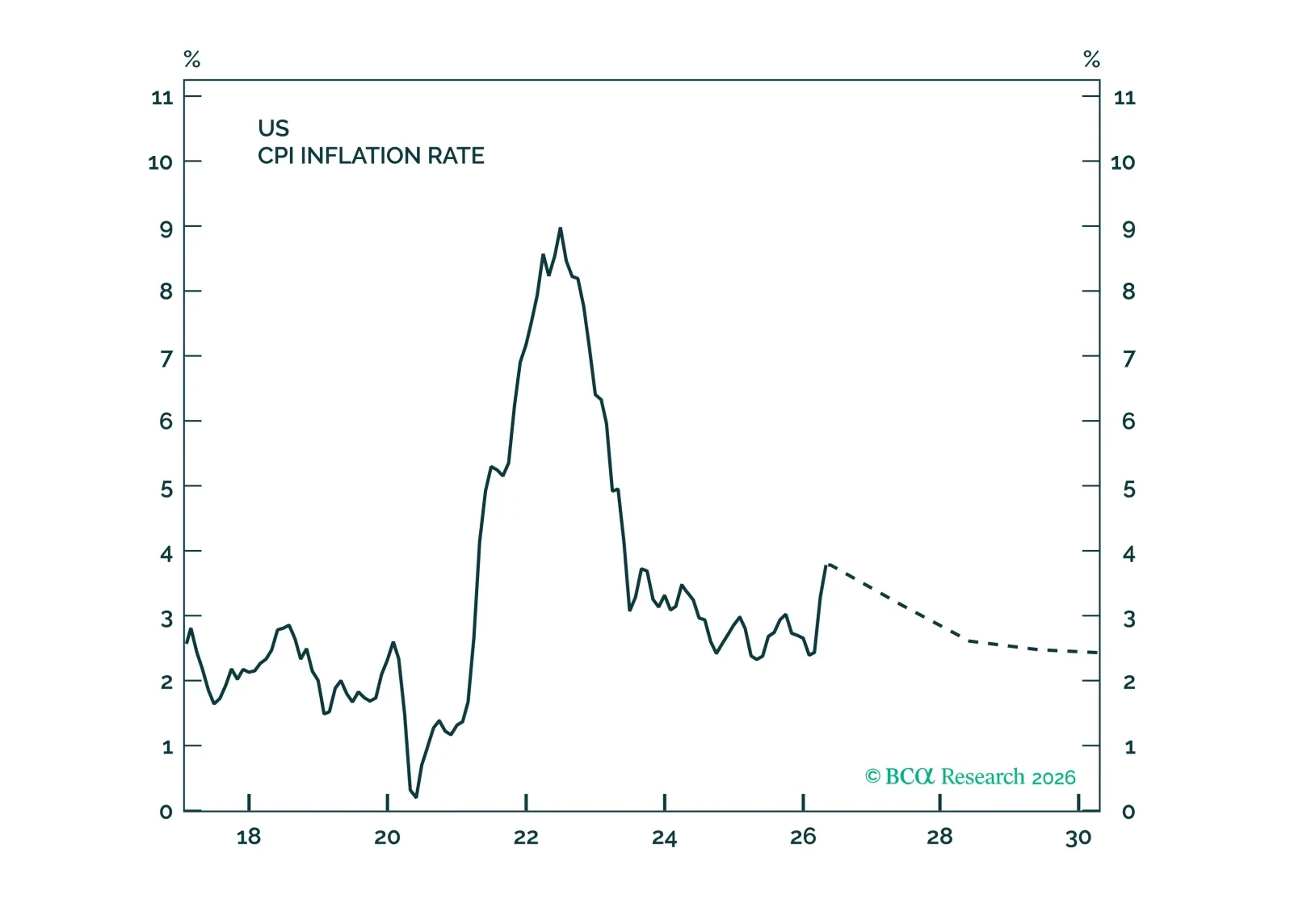

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

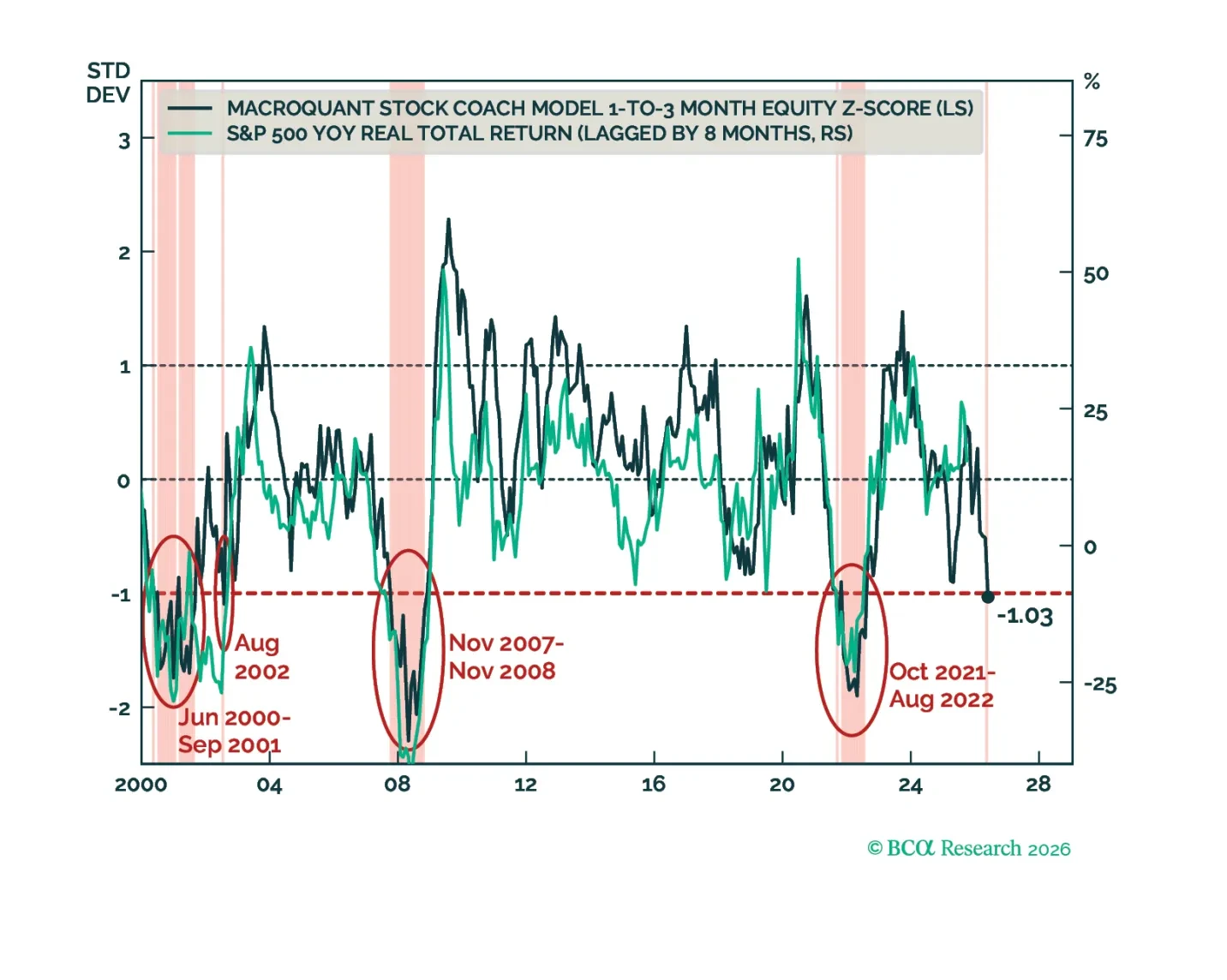

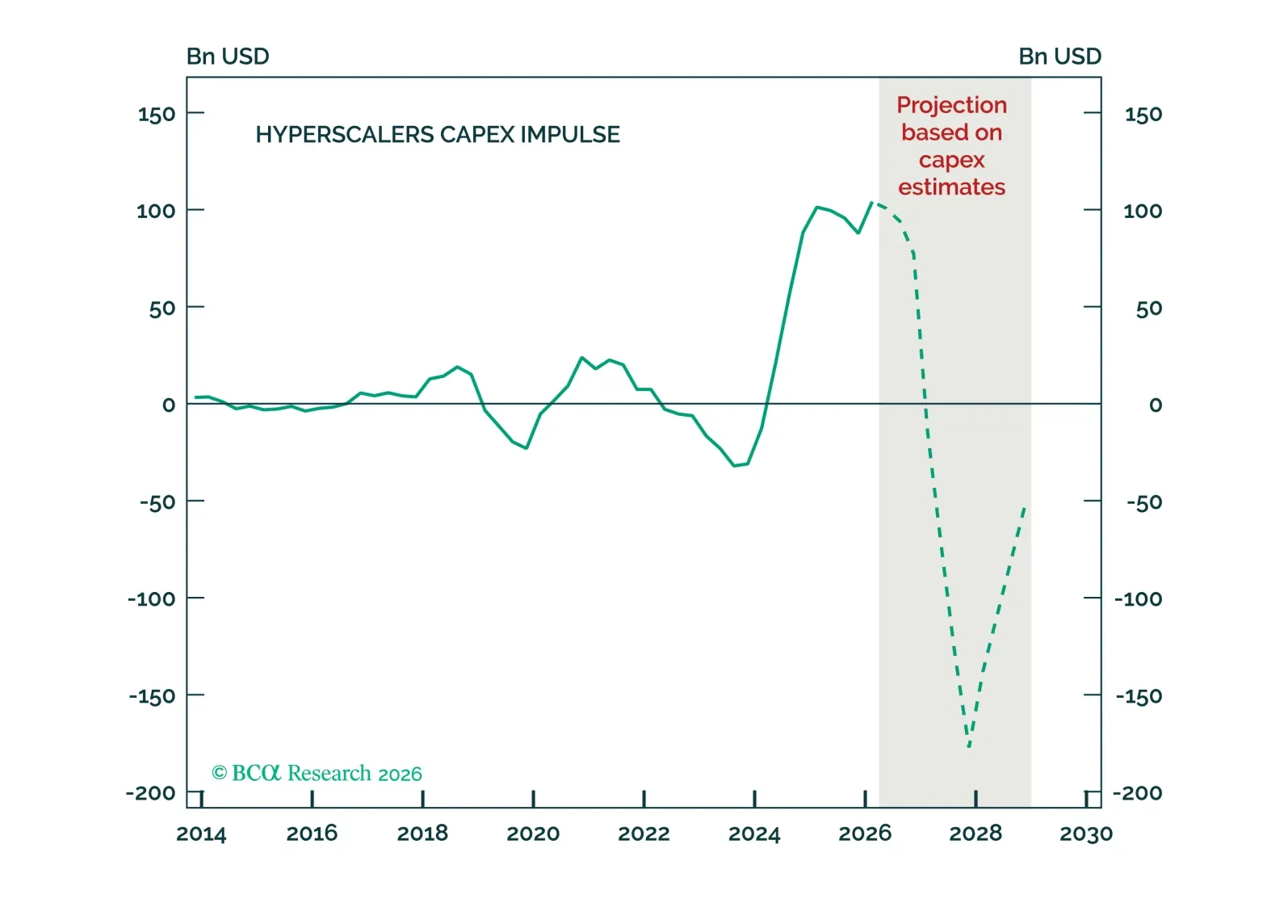

Bears will fold like lawn chairs this summer as traffic returns to Hormuz, allowing markets to overcome seasonal malaise. But we are starting to see how the expansion ends. A macro brew of global central bank tightening due to stickier-than-expected inflation, negative second derivative in AI capex, and surging supply of equities due to Monster IPOs. Expect a blow-off rally until midterms, uncertainty after, calamity in 2027.