AI

Artificial intelligence will destabilize domestic politics and international security. States will try to adopt more creative fiscal policy, including by raising taxes on Big Tech.

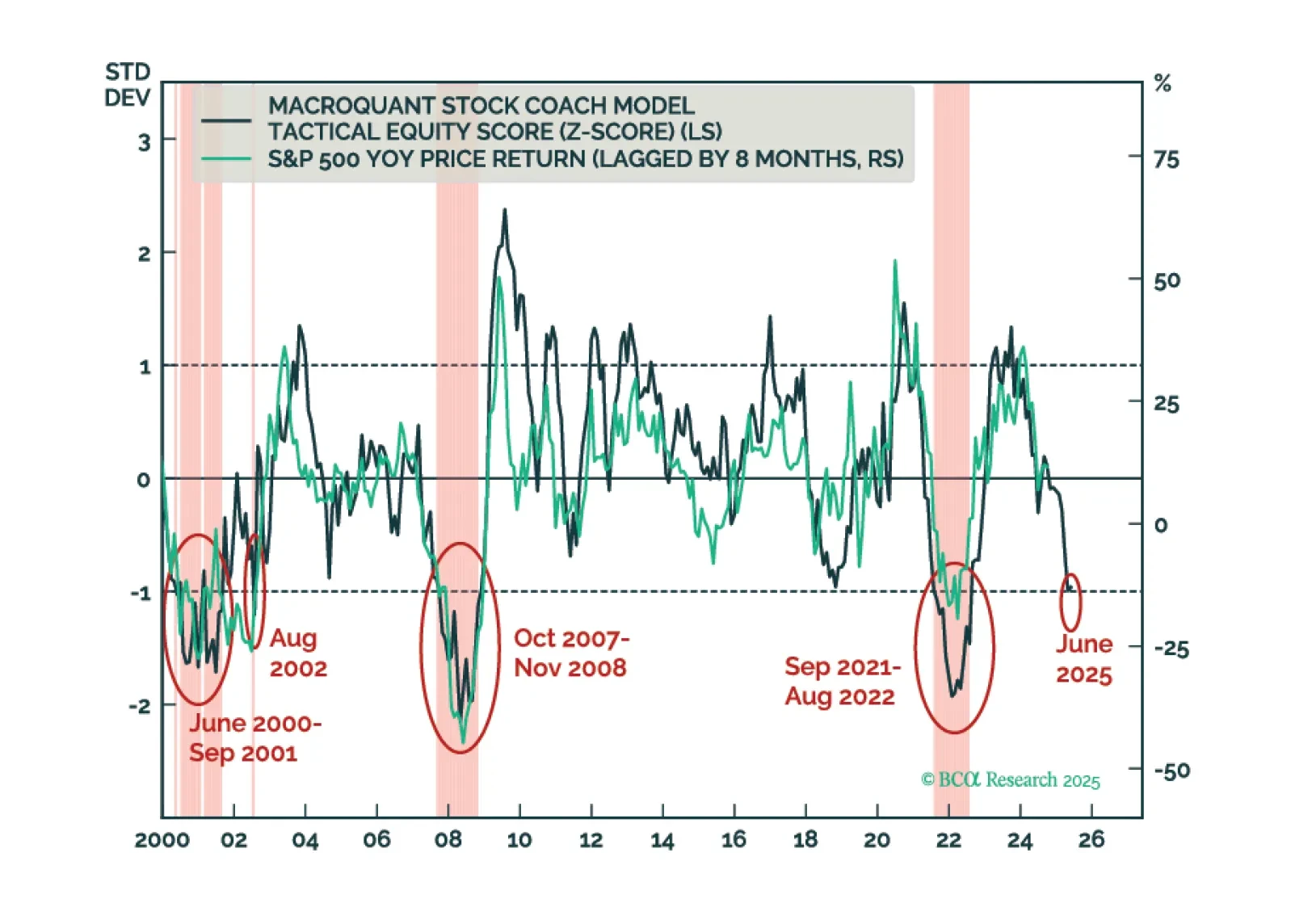

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

Provided that humanity can overcome the existential risks posed by AI, real incomes will rise. Although most workers will ultimately gain from the transition to an AI-dominated economy, the biggest winners will be those who control the land and the natural resources beneath it.

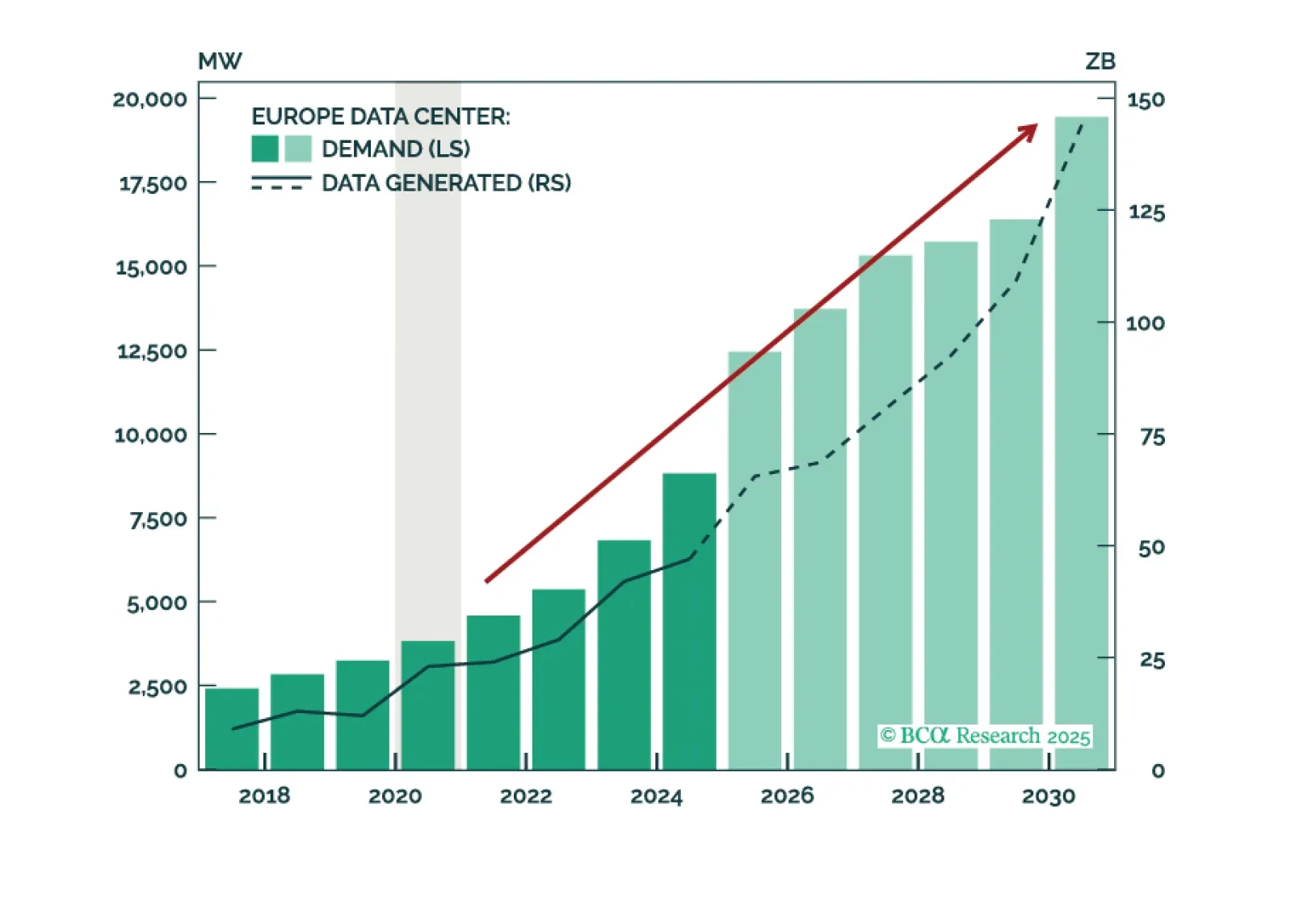

While the US is the pioneer, Europe will follow suit—more rapidly than expected. It is not a question of if GenAI will boom in Europe, but when. Europe’s Data Center growth is already strong today, but a US-style boom is just around the corner.

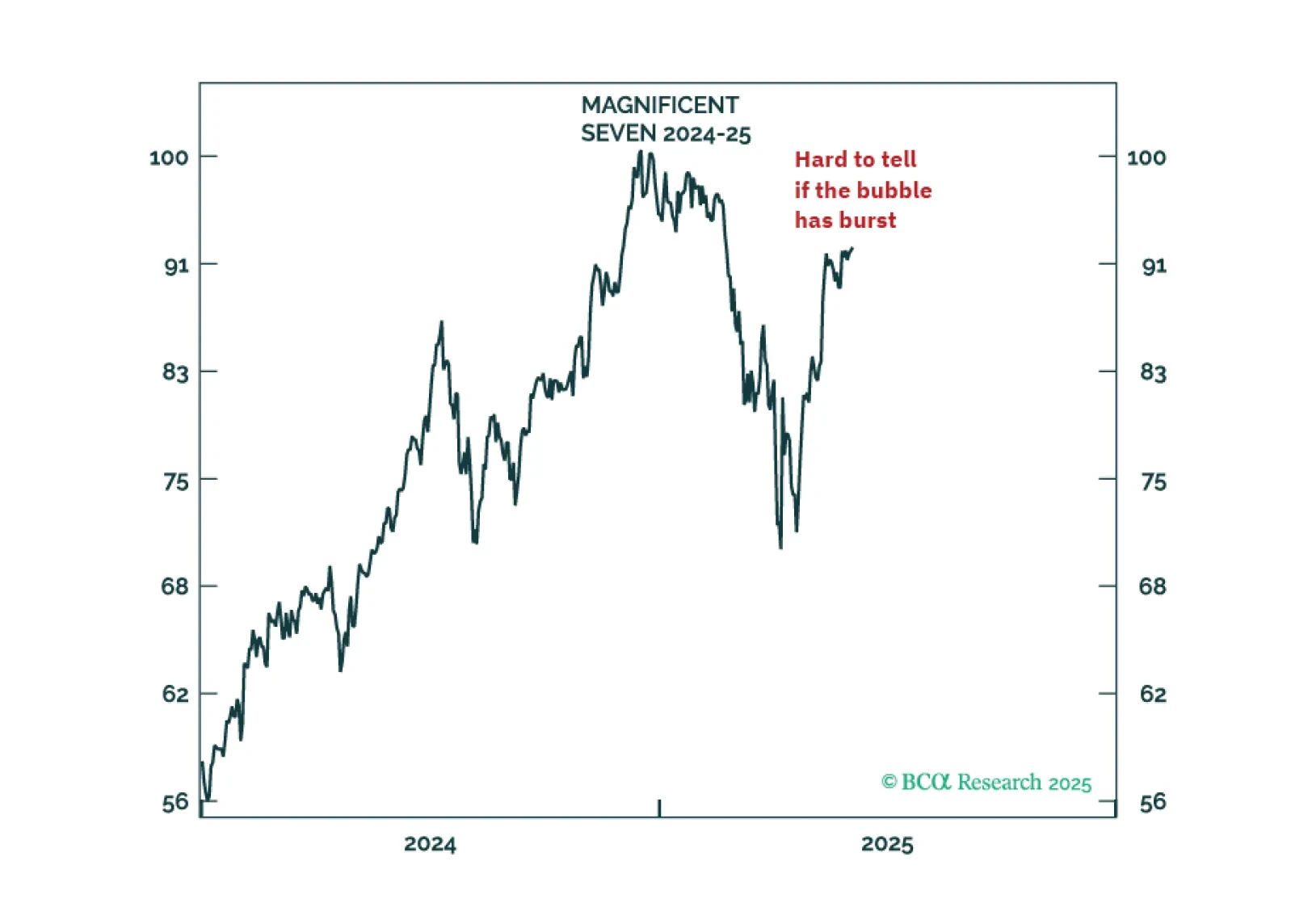

I am a structural disbeliever in the US superstar stocks because these winners of the previous technology, Web 2.0, are unlikely all to be the winners of the latest technology, AI. But I would suspend my disbelief if the Magnificent-7 index reaches a new high and the bursting AI-bubble configuration is broken. Plus, a new recommendation is to overweight Global Healthcare (IXJ).

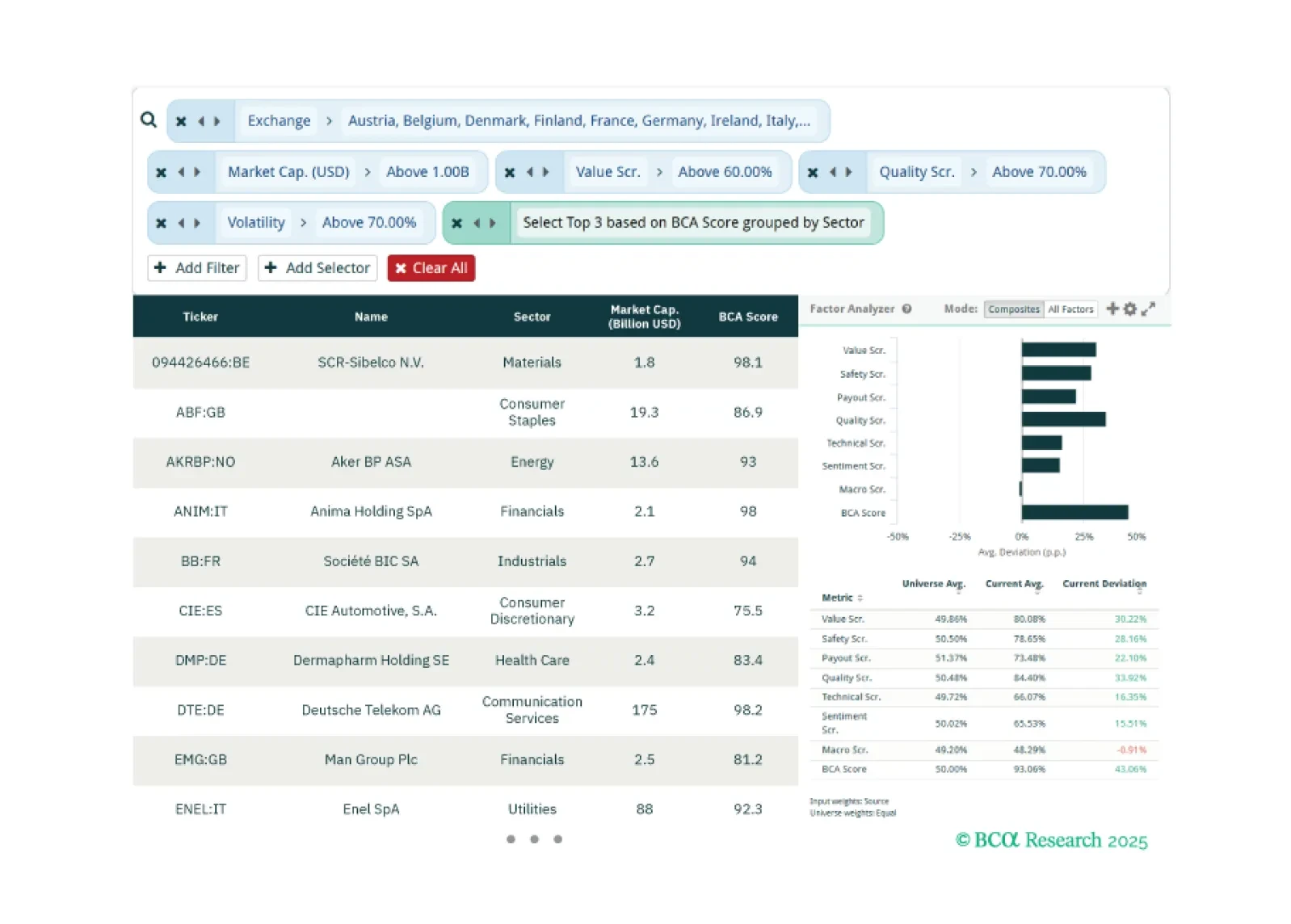

This week, our three screeners cover: Favoring European equities over US equities, cybersecurity stocks, and large caps with large moves in their BCA Score.

Despite our bearish predisposition towards stocks, we are open-minded to anything that could challenge our thesis. As such, in this report, we review five upside scenarios for equities.