AI

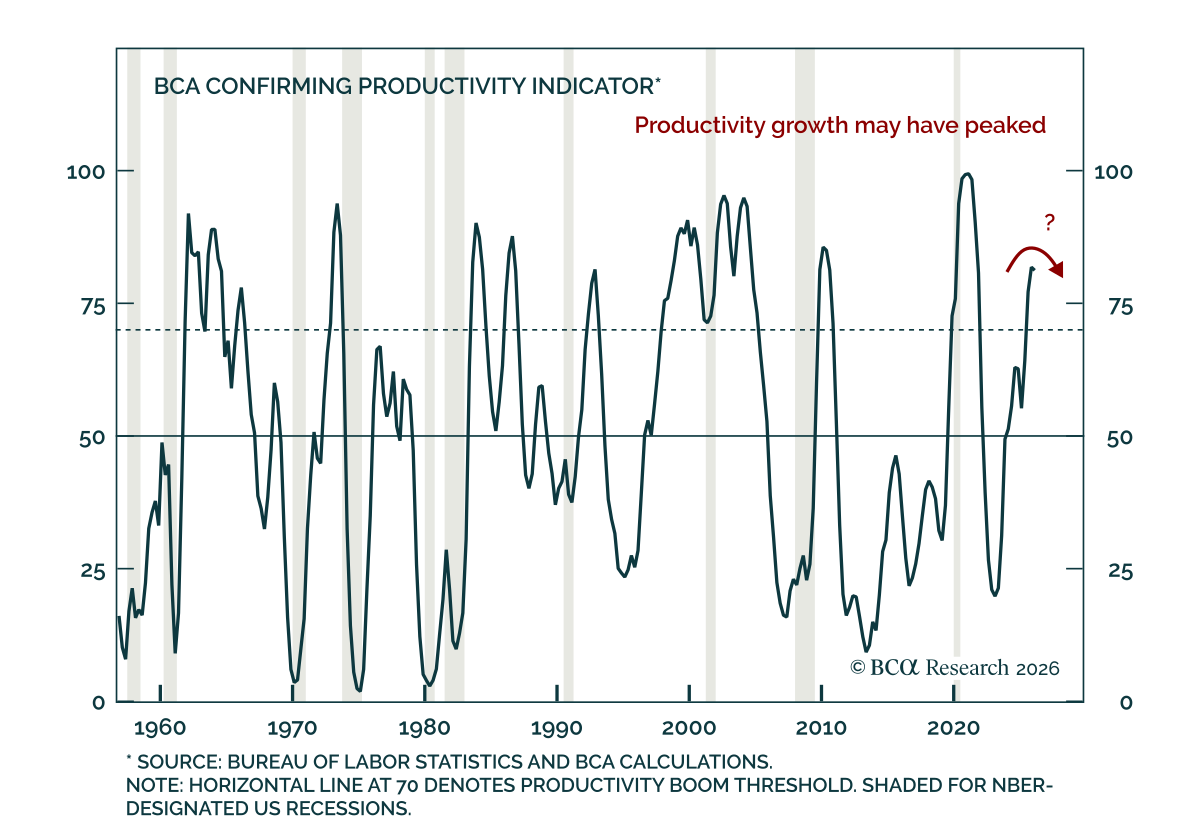

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.

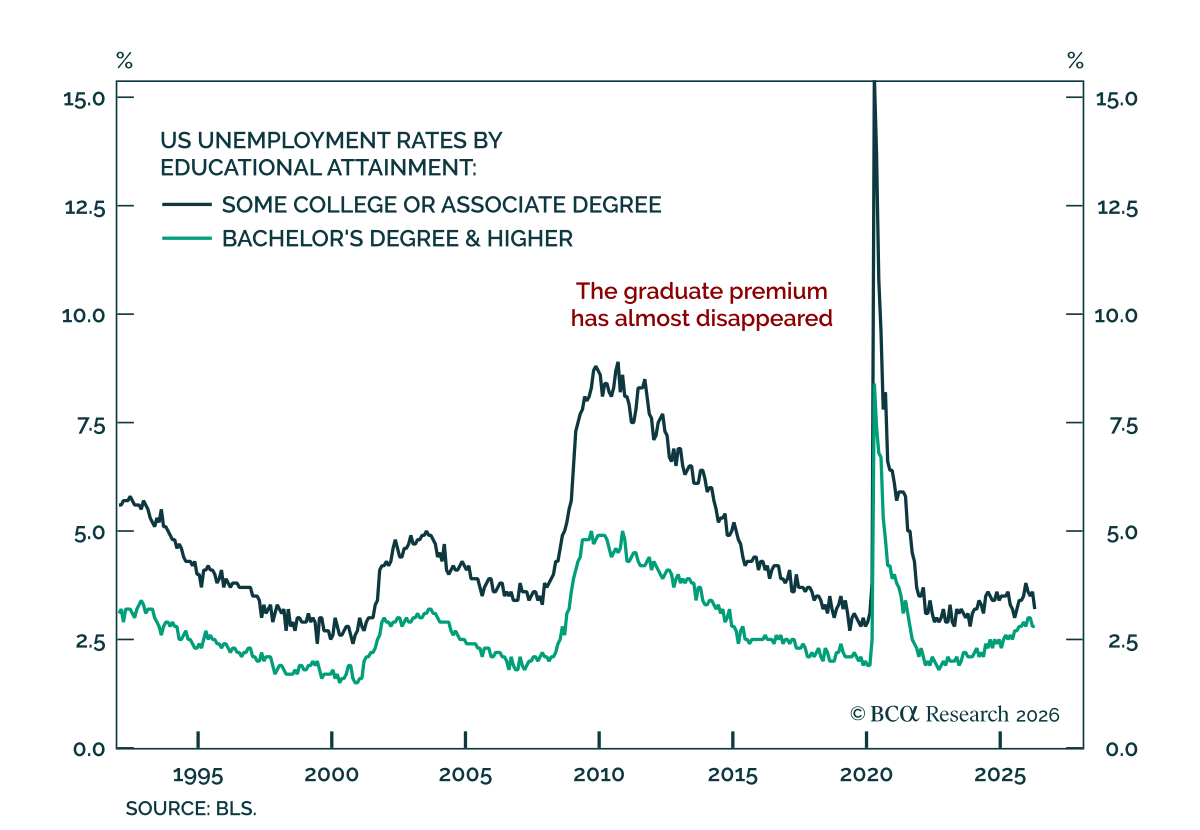

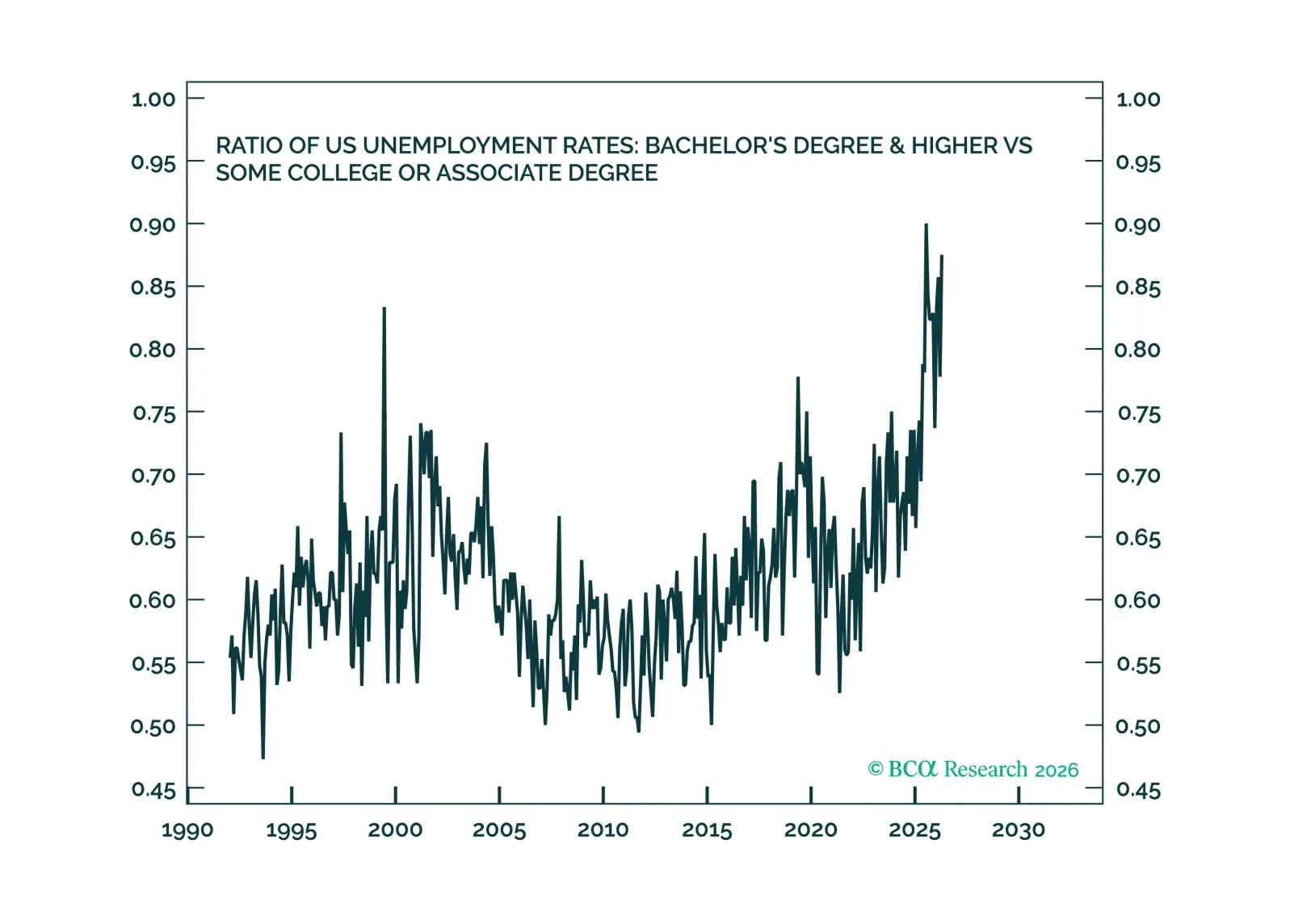

AI excels at IQ but fails miserably at EQ. Hence, AI will obsolete any job that relies on IQ, including many graduate-level jobs. But high-EQ humans will be in high demand to pair up with AI, and many of these jobs will be middle income jobs. We discuss the implication for the economy and markets. Plus, a new tactical trade is underweight global tech versus healthcare.

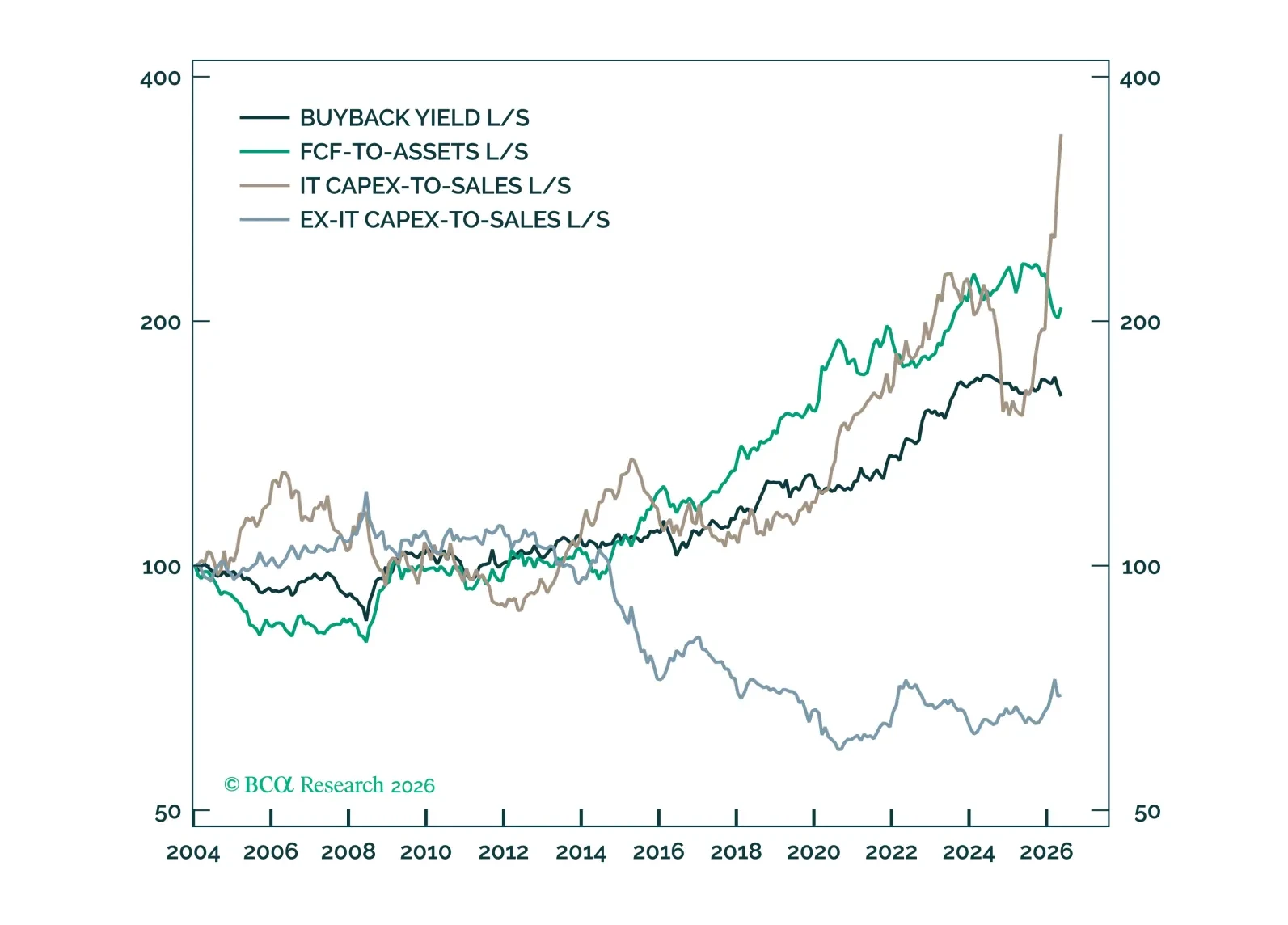

Tech, and increasingly the market, is moving from a cash-return regime to a reinvestment regime. After the GFC, investors rewarded companies that returned cash to investors. In the AI cycle, they are rewarding companies that put that cash back to work. This is not just a story of falling free cash flow; it is the mirror image of a market rewarding reinvestment. Tech has defined both regimes, revealing the old cash-flow “stars” as sector bets masquerading as alpha.

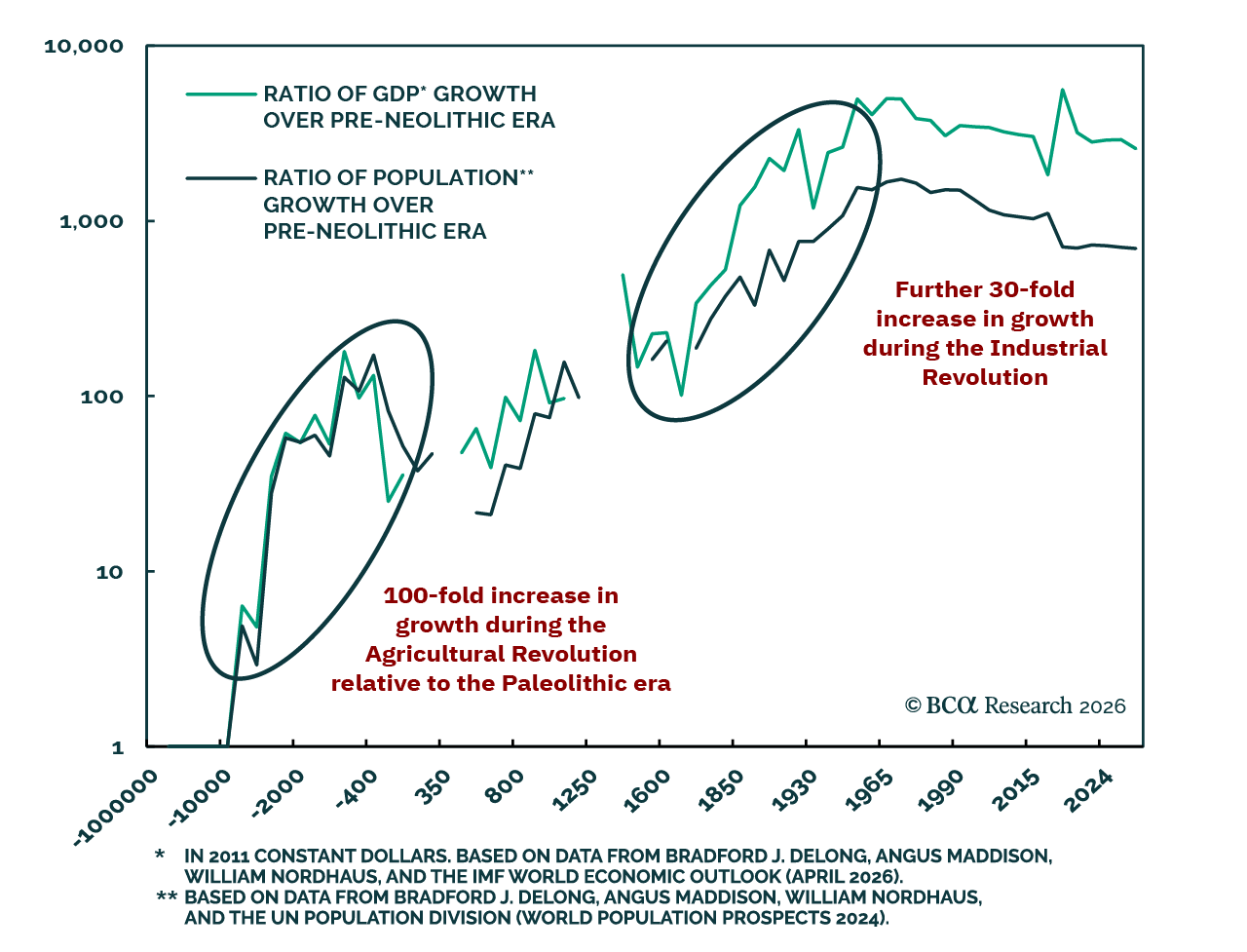

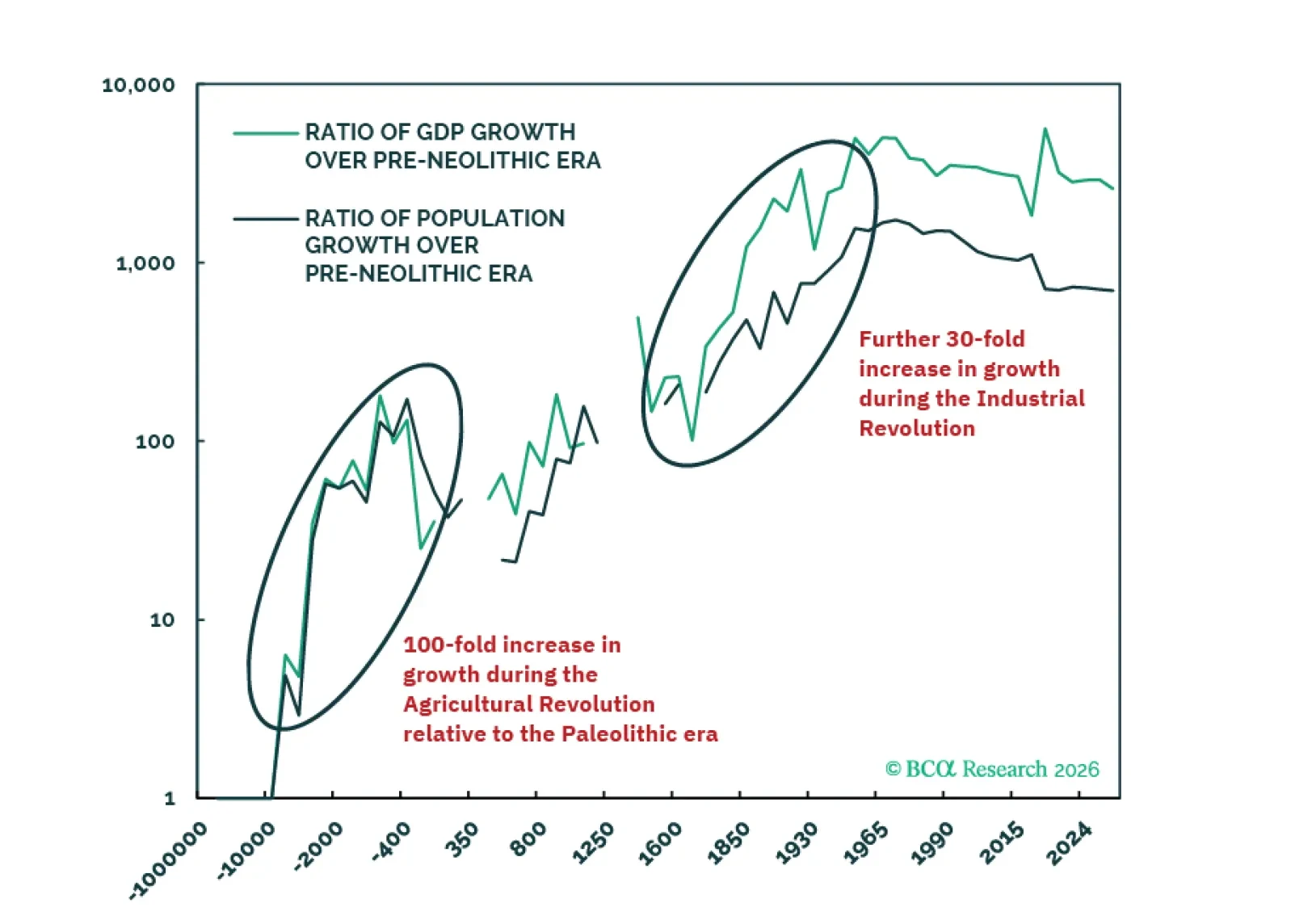

AI could be as transformative as the Agricultural or Industrial Revolutions. However, the fact that you are reading these words at the dawn of the AI age hints at a darker possibility, which is that AI will lead to humanity's demise. Fortunately, the most straightforward interpretation of quantum mechanics suggest you will only be conscious in those timelines where the world survives.

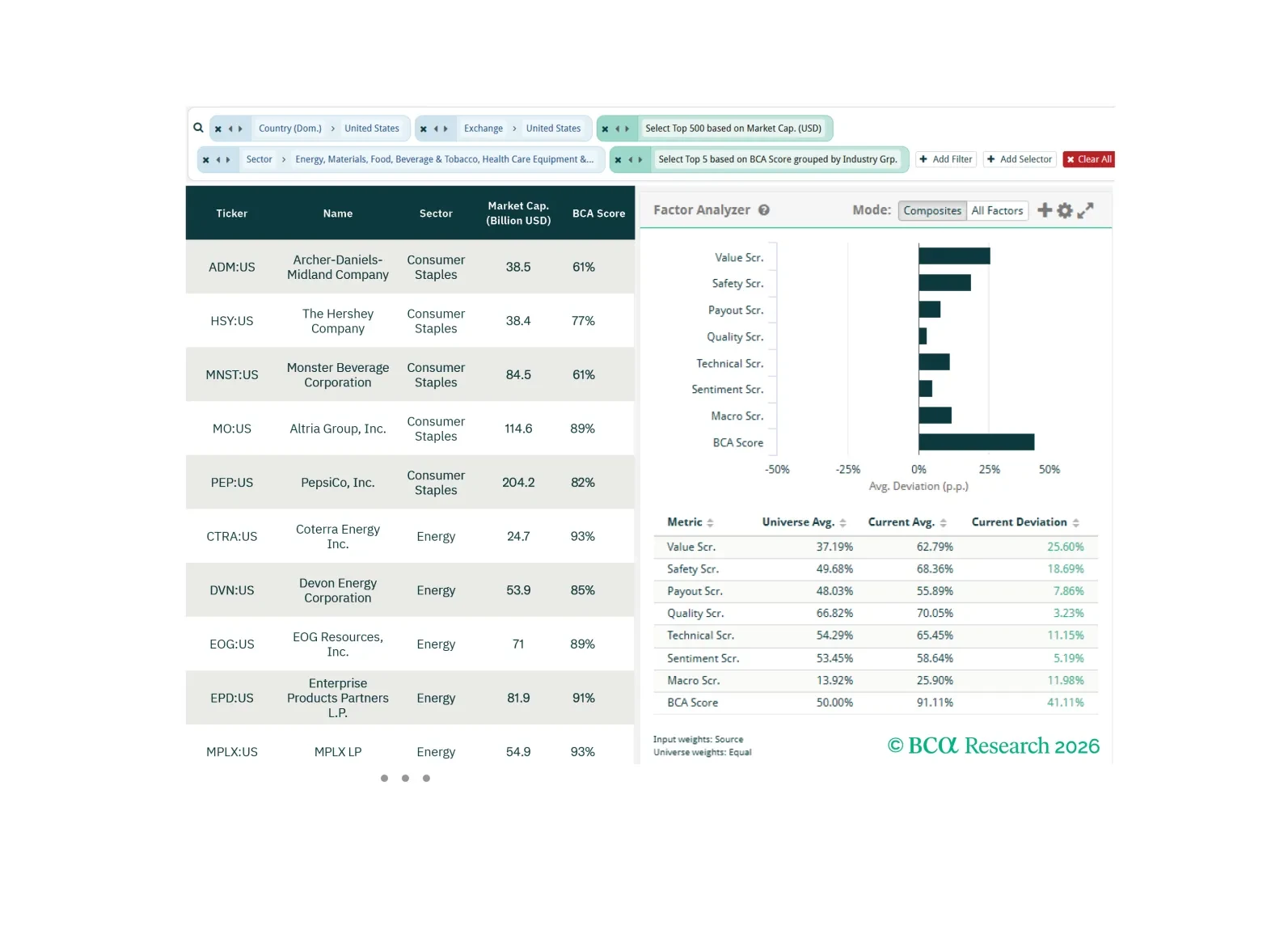

In this screener report, we explore opportunities in Inflation risk, supply-constrained Information Technology stocks, and old-economy cyclicals.