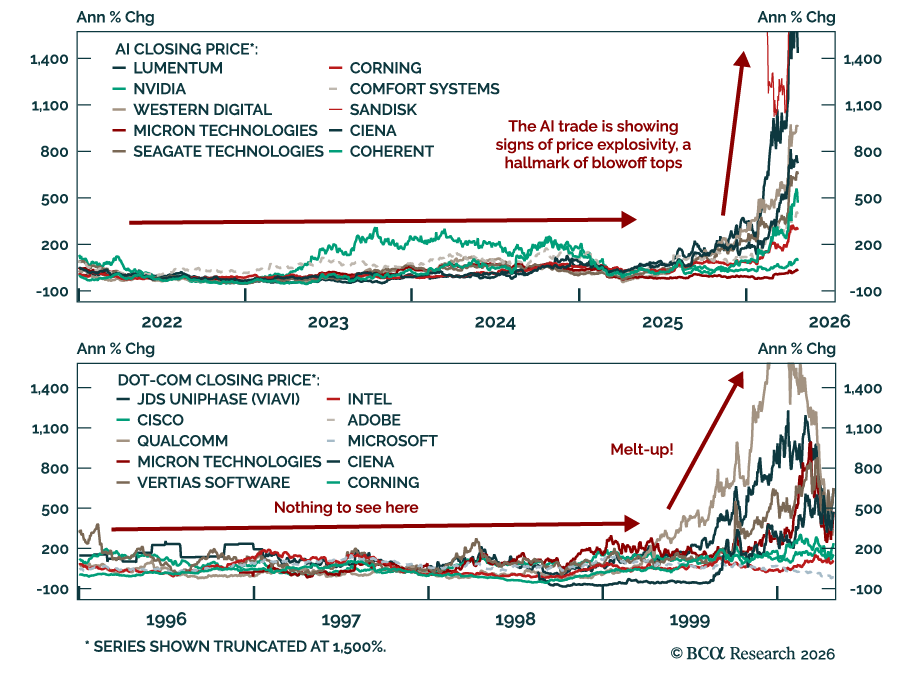

AI

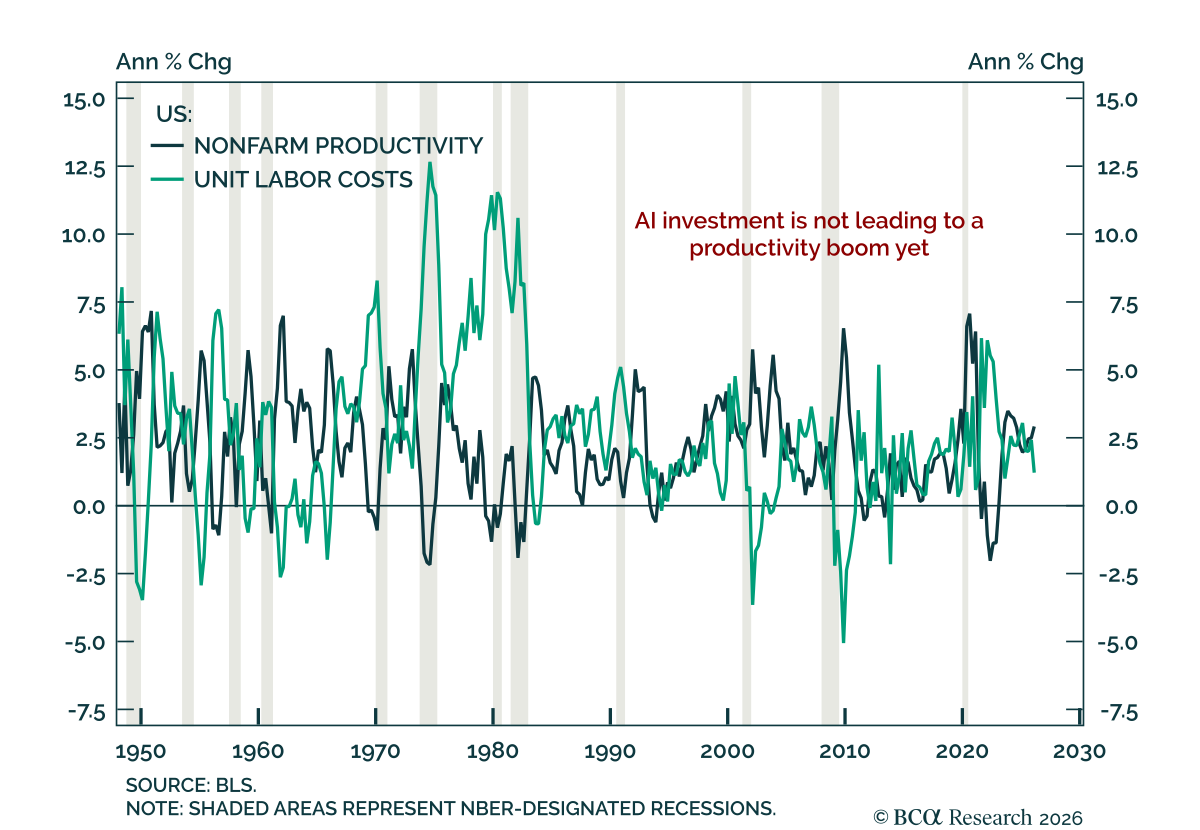

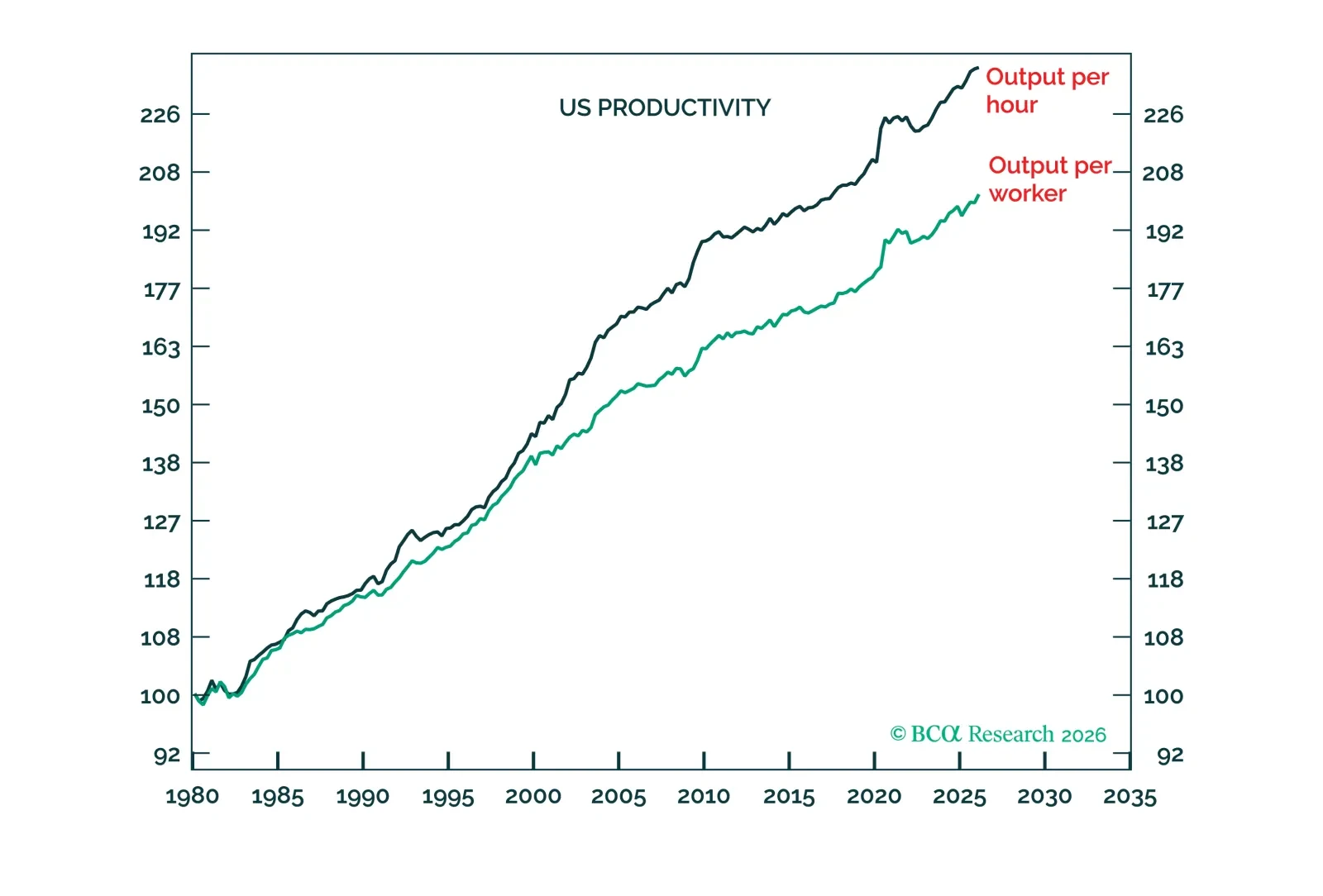

New Fed Chair, Kevin Warsh, is betting that an AI-driven productivity acceleration will get the Fed out of jail for persistently missing its 2 percent inflation target. But history informs us that while new technology adoption is exponential, total productivity growth is not. So, if Warsh’s bet goes wrong, as is likely, the US inflation overshoot will persist. We discuss the investment implications. Plus, a new trade is short cotton.

The tenuous ceasefire holds, with the "new geopolitical equilibrium scenario" remaining in place. Enough crude trickles through Hormuz to avert a global recession, but not to alleviate building inflationary pressures, a product of a complicated geomacro context that is not transitory. The Fed will look to ignore these in the short term, fueling the equity rally in the US. Chinese equities may pop thanks to the upcoming détente. When does it all end? Beware of major IPOs!

Based on our previous work on margins, three aspects of margins may matter to investors: their level, their variability, and their likely trend. We add two margin-themed baskets: a stock-level High & Stable vs. Low & Volatile basket and an industry-level AI-Supported vs. AI-Insulated basket.

Based on our previous work on margins, three aspects of margins may matter to investors: their level, their variability, and their likely trend. We add two margin-themed baskets: a stock-level High & Stable vs. Low & Volatile basket and an industry-level AI-Supported vs. AI-Insulated basket.

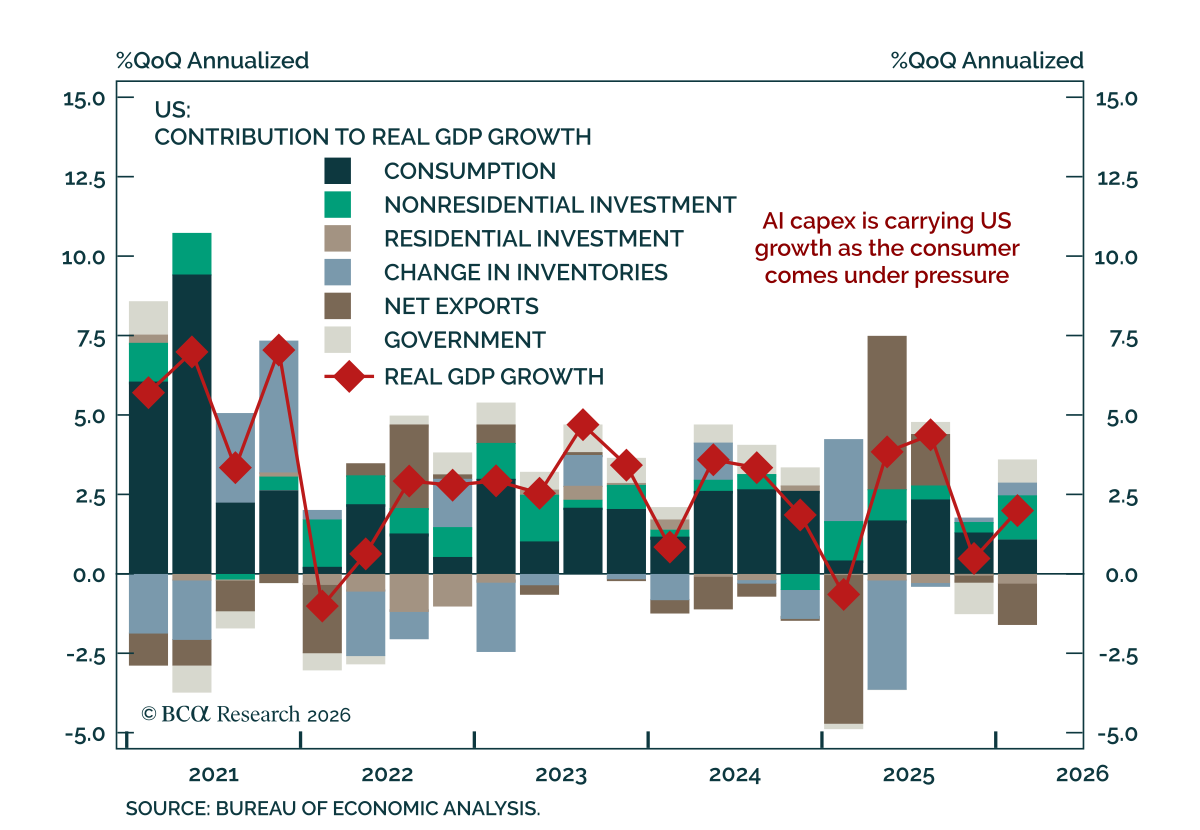

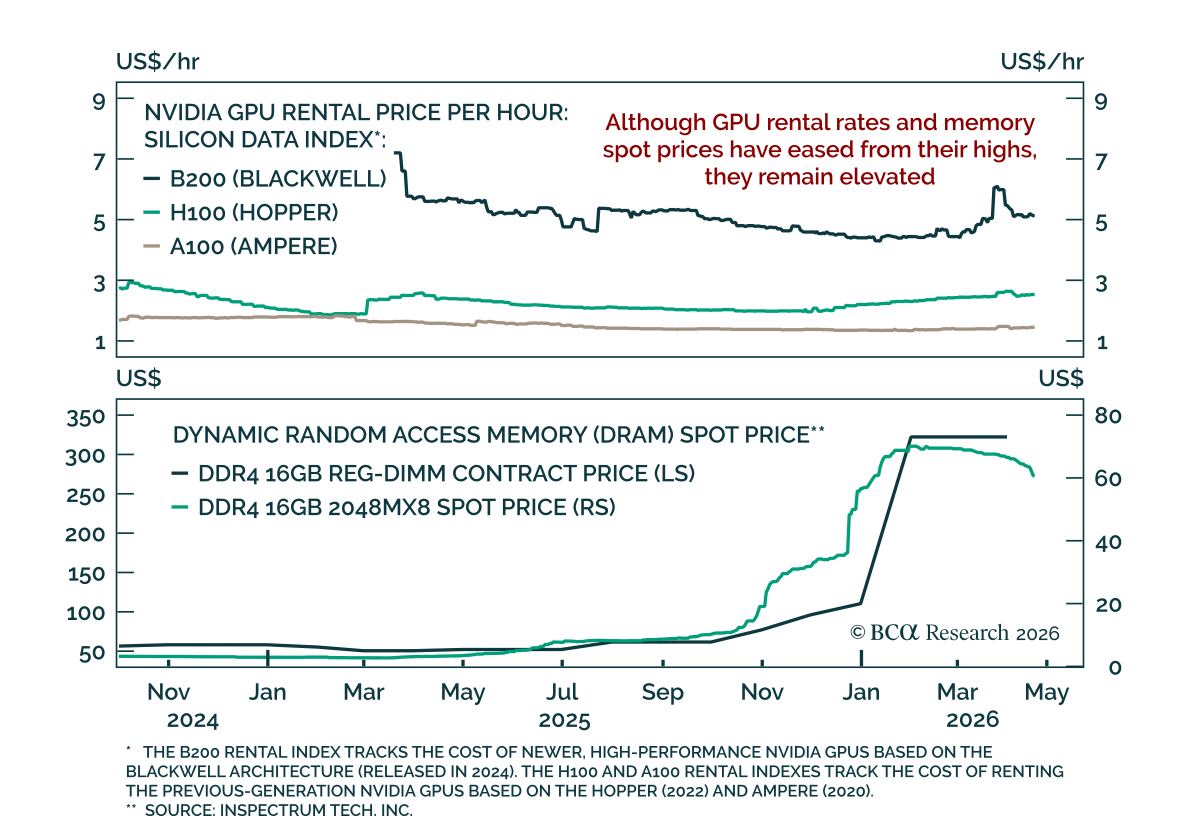

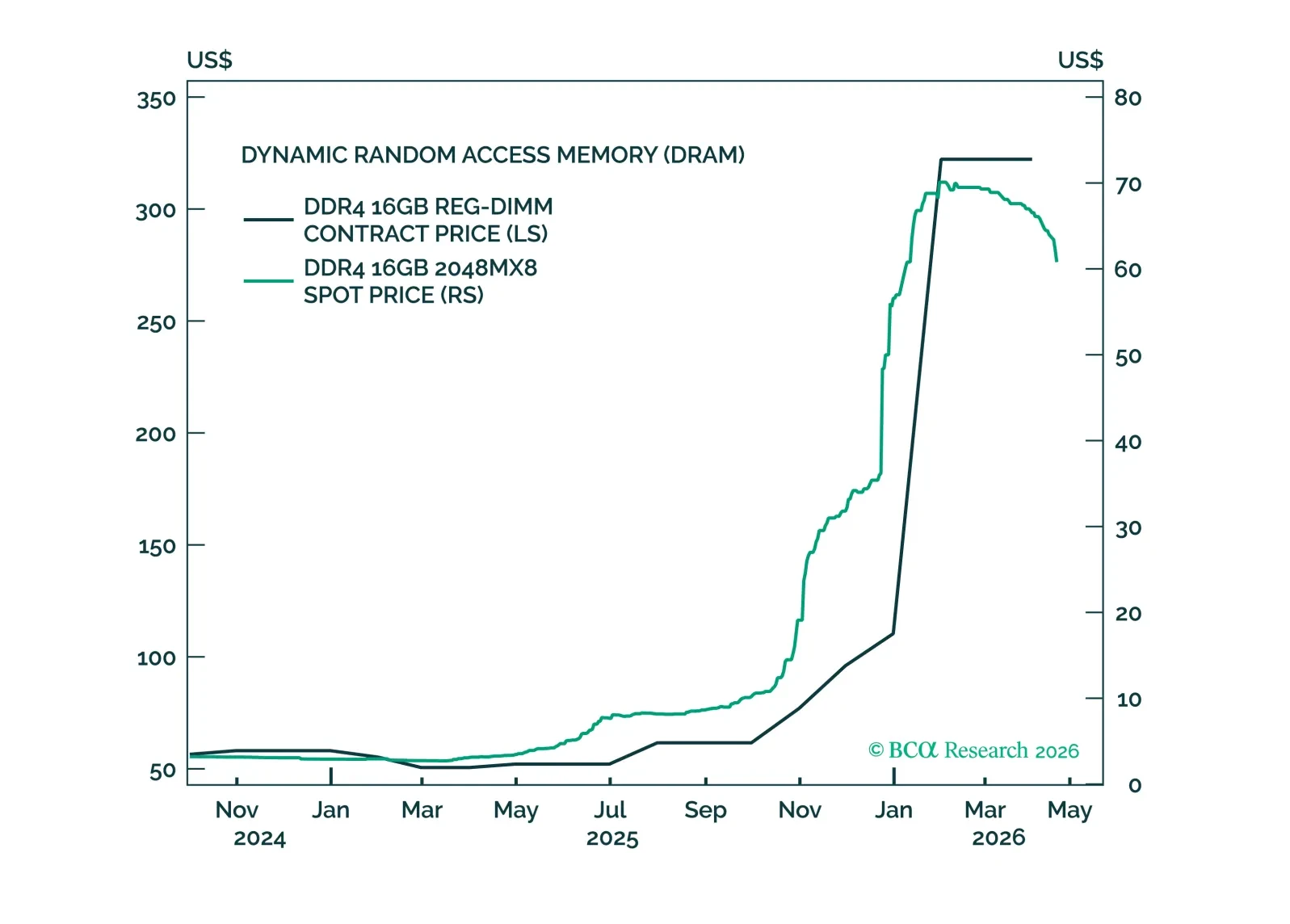

Most of the increase in S&P 500 earnings estimates this year has stemmed from shortages. The oil shortage, which has pushed up estimates for energy companies, will fade once the military conflict is resolved. However, the shortage of semiconductors and other AI paraphernalia could persist for a while longer. As such, we are moving our recommended 12-month equity allocation from a slight underweight to neutral. We are already neutral on a 3-month horizon.

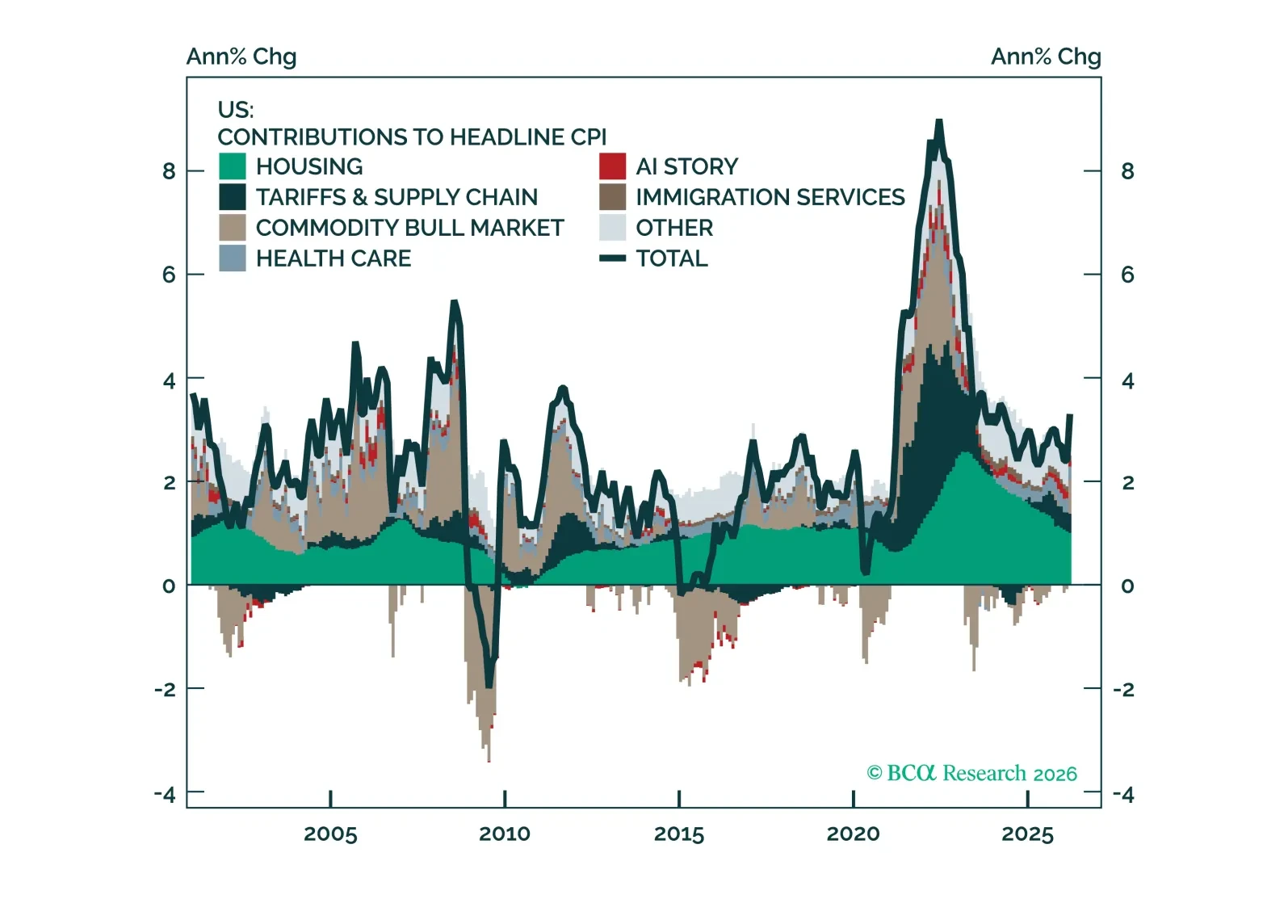

We do not expect the oil shock to have a lasting effect on inflation. Looking further out, a variety of structural forces will influence inflation, including fiscal policy, globalization, demographics, and AI.