AI

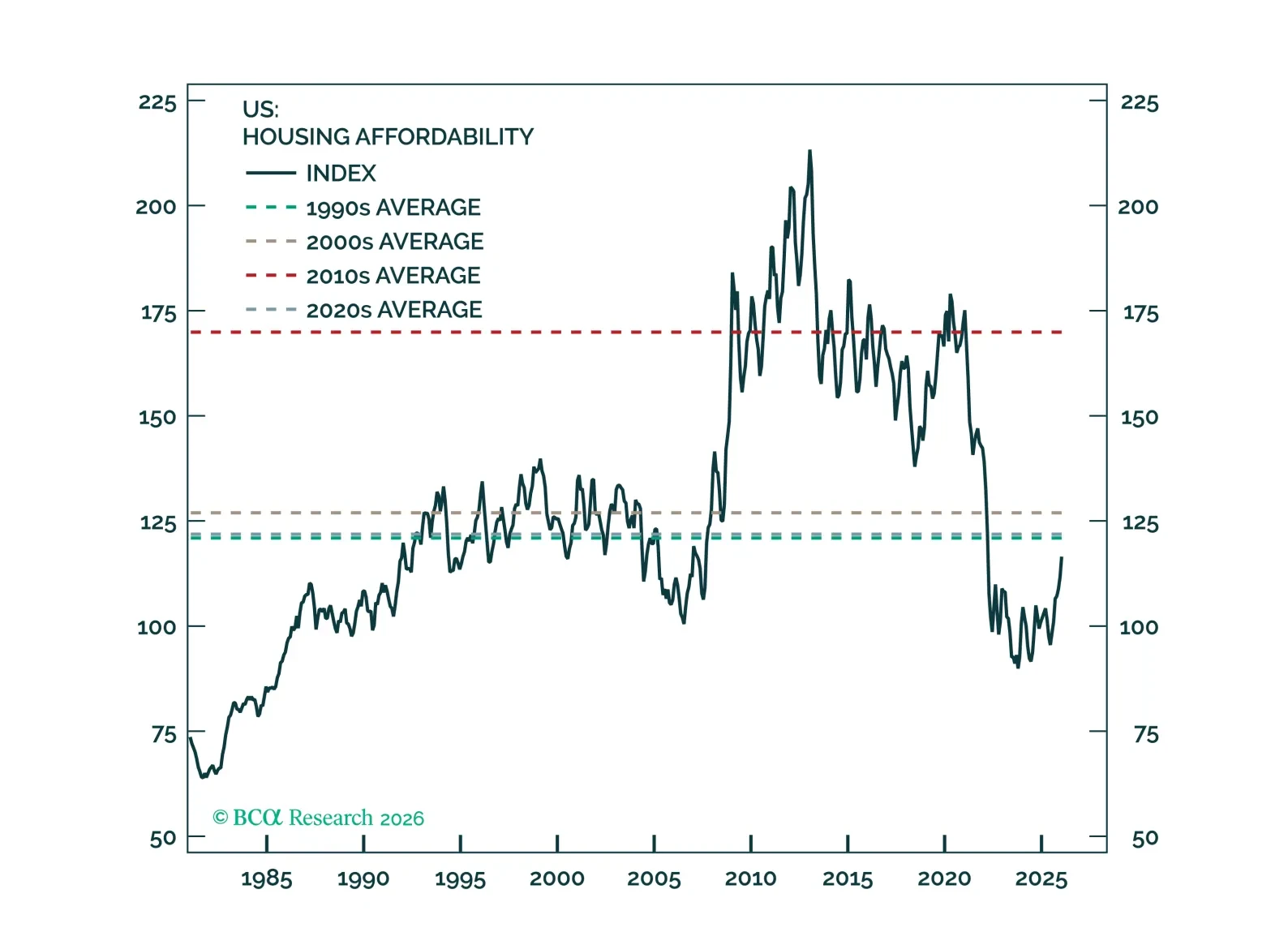

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

In Section II, Jonathan examines the humanoid robot segment of the emerging physical AI landscape, concluding that humanoid robots are a potential but not yet imminent investment theme.

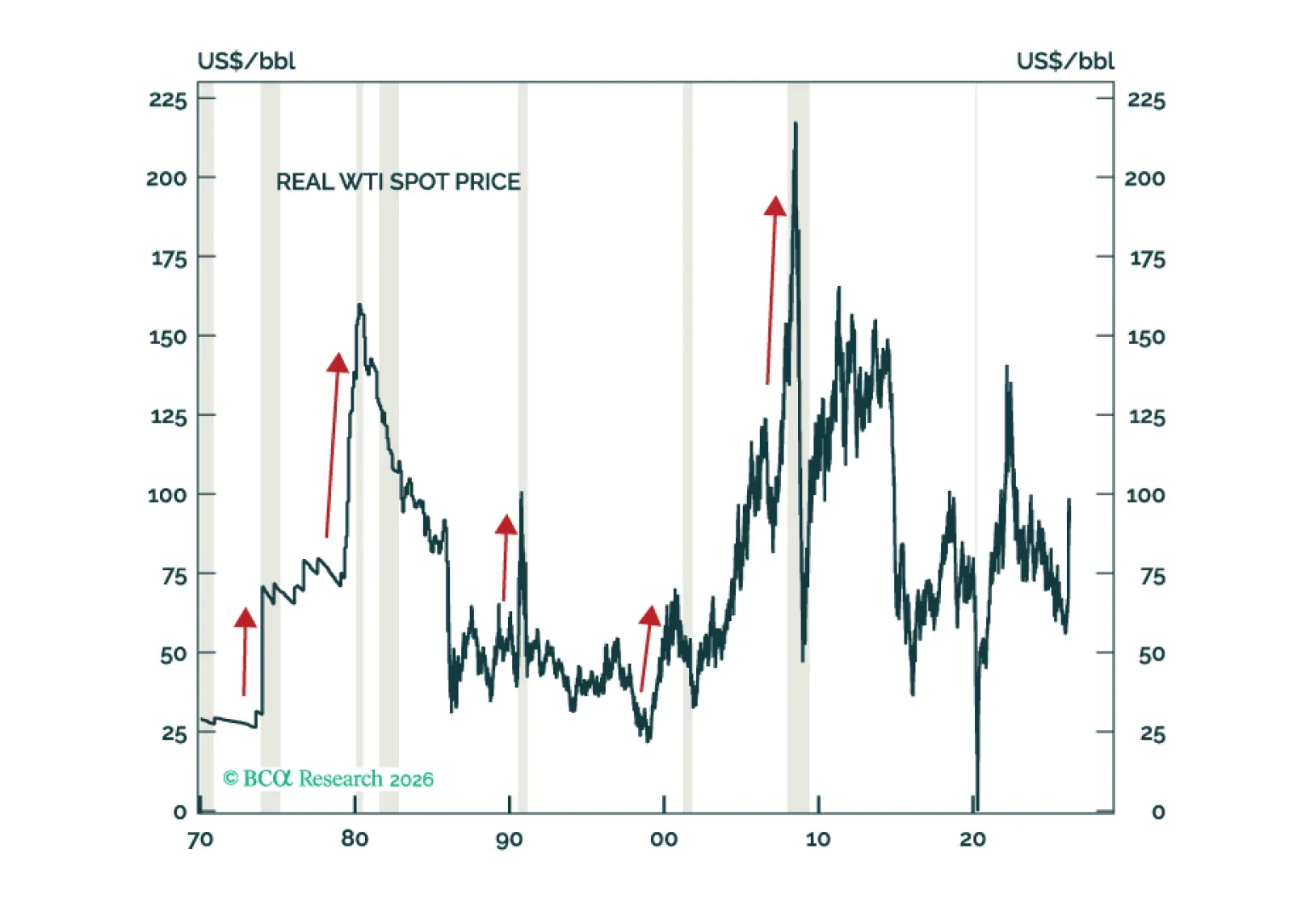

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

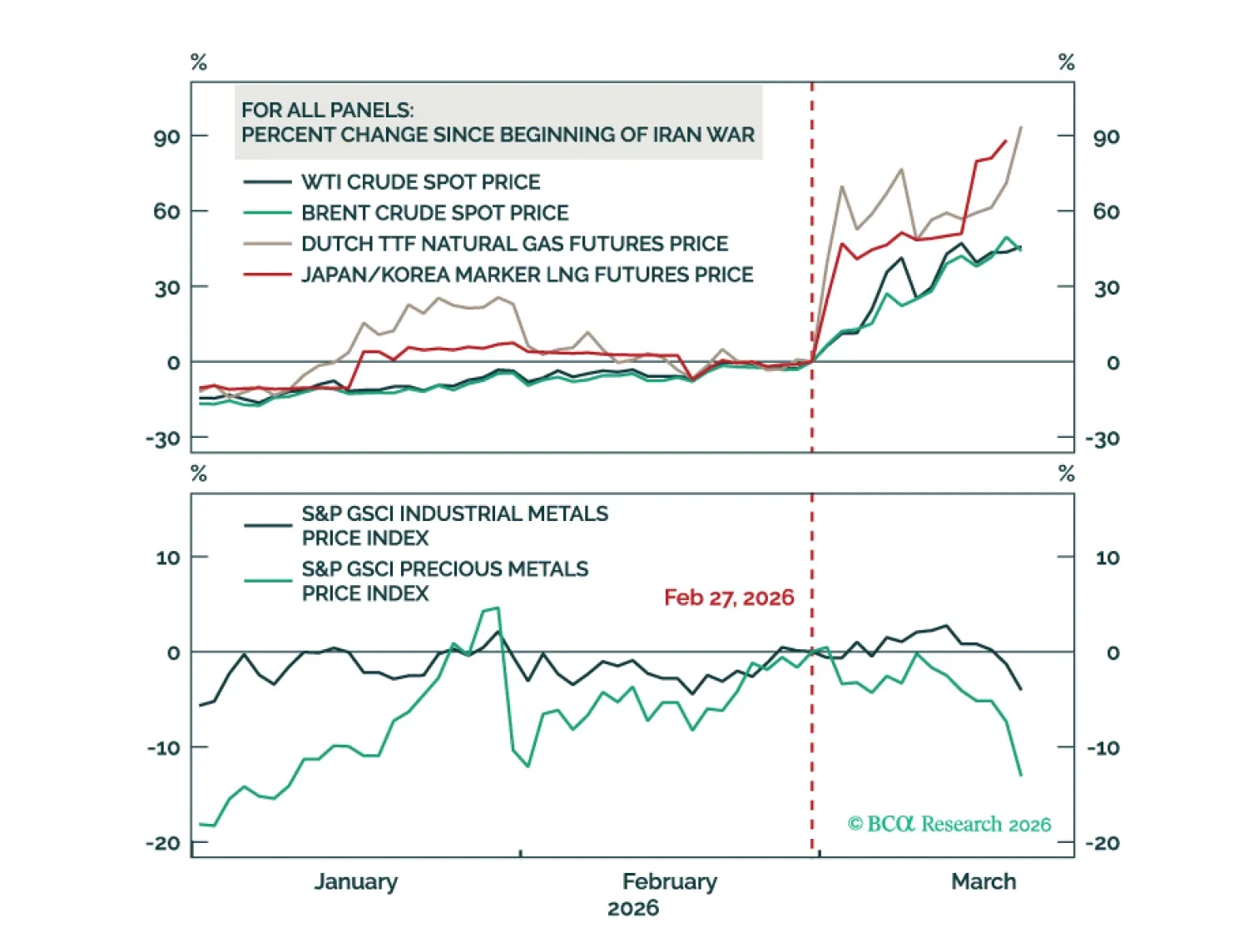

In the short term, there is plenty to be worried about in macro beyond the Middle East. The market was on thin ice before the Iran conflict. In the long term, the base case scenario remains bullish, but the war in the Middle East needs to be brief.

Fears of widespread job losses due to AI are overstated. For investors, the key is that white-collar anxiety is accelerating a red-hot blue-collar economy via lower yields. Upgrade Private Real Estate to overweight.

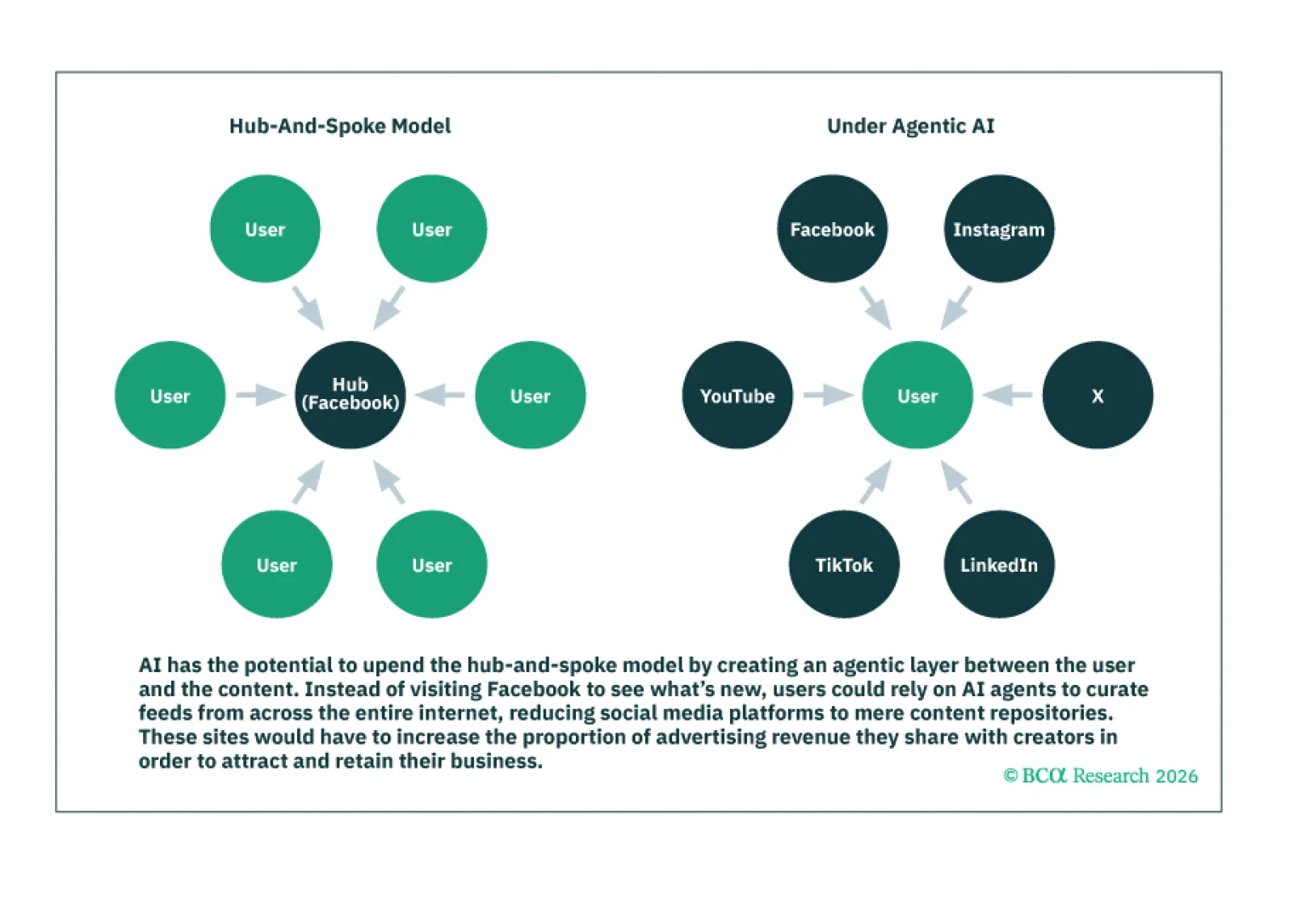

Tech companies have historically generated profits from three main sources: 1) economies of scale; 2) network effects; and 3) proprietary technologies. AI threatens to undercut all three sources.

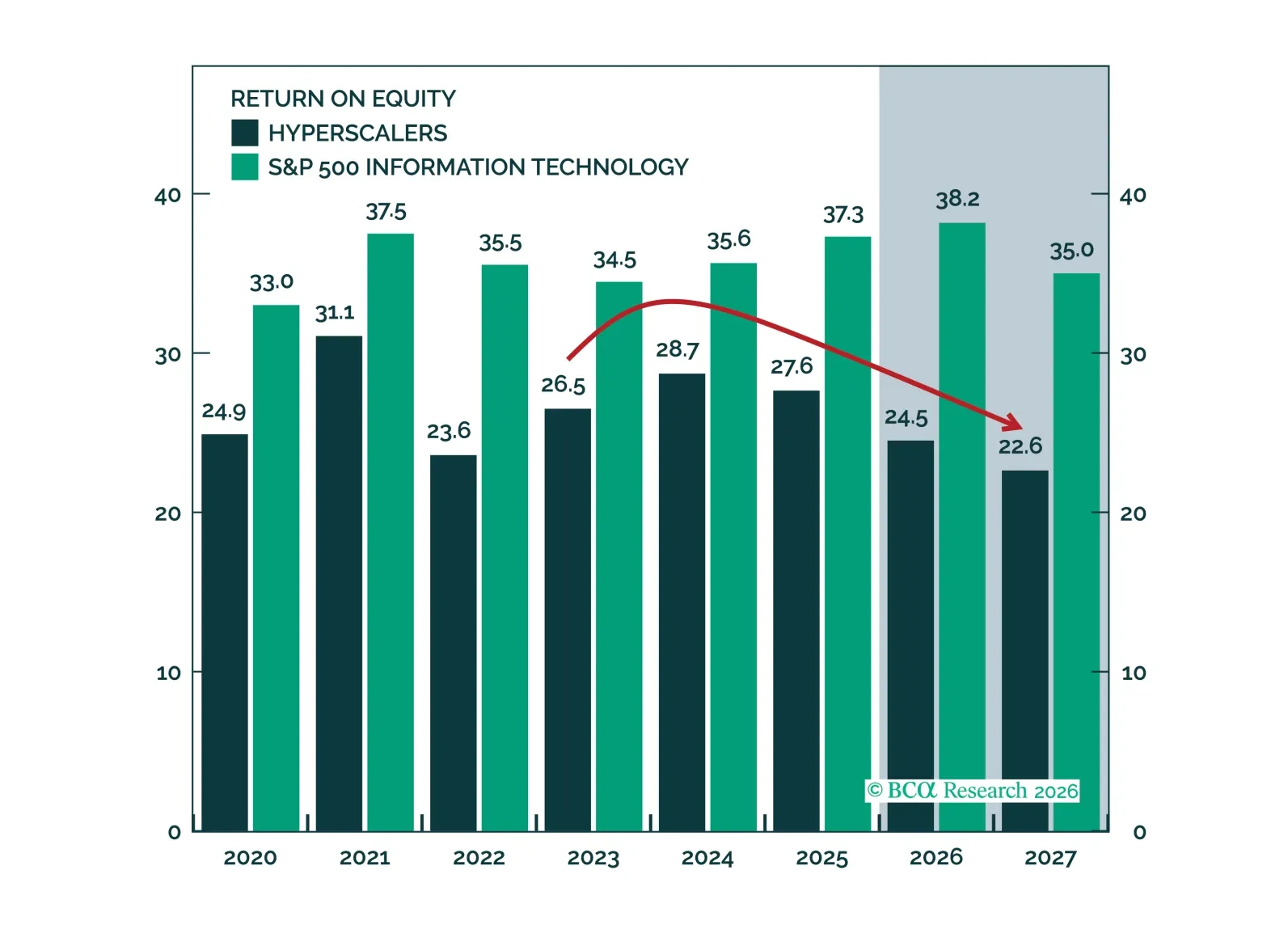

The capex debate is better framed not as boom versus bubble, but as around capacity, leverage, and cash conversion. ROEs have compressed, but revenue growth and margin expansion offer a credible path back. Spenders likely have time to make good on their investments, though the market’s leash may be shorter than anticipated.

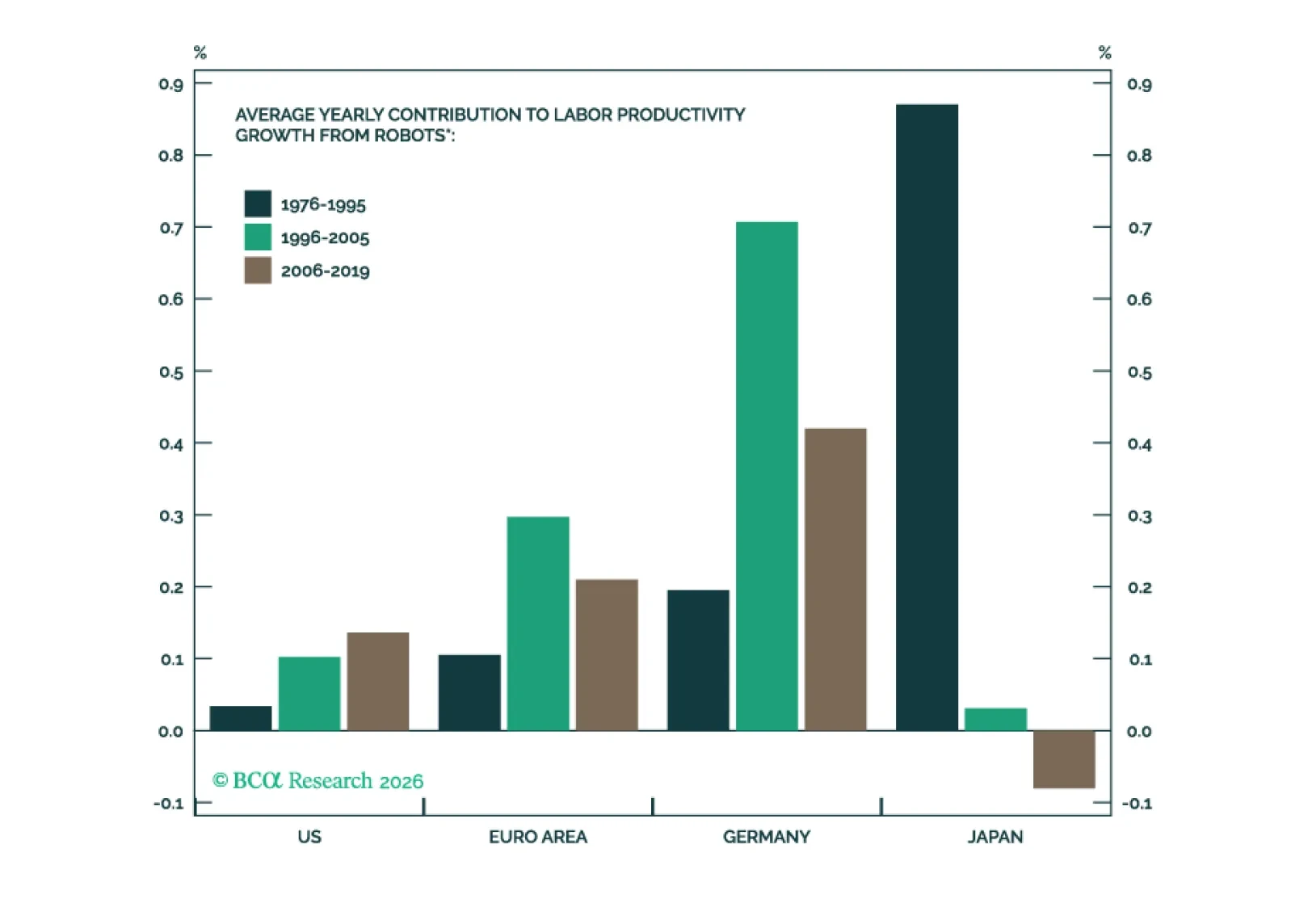

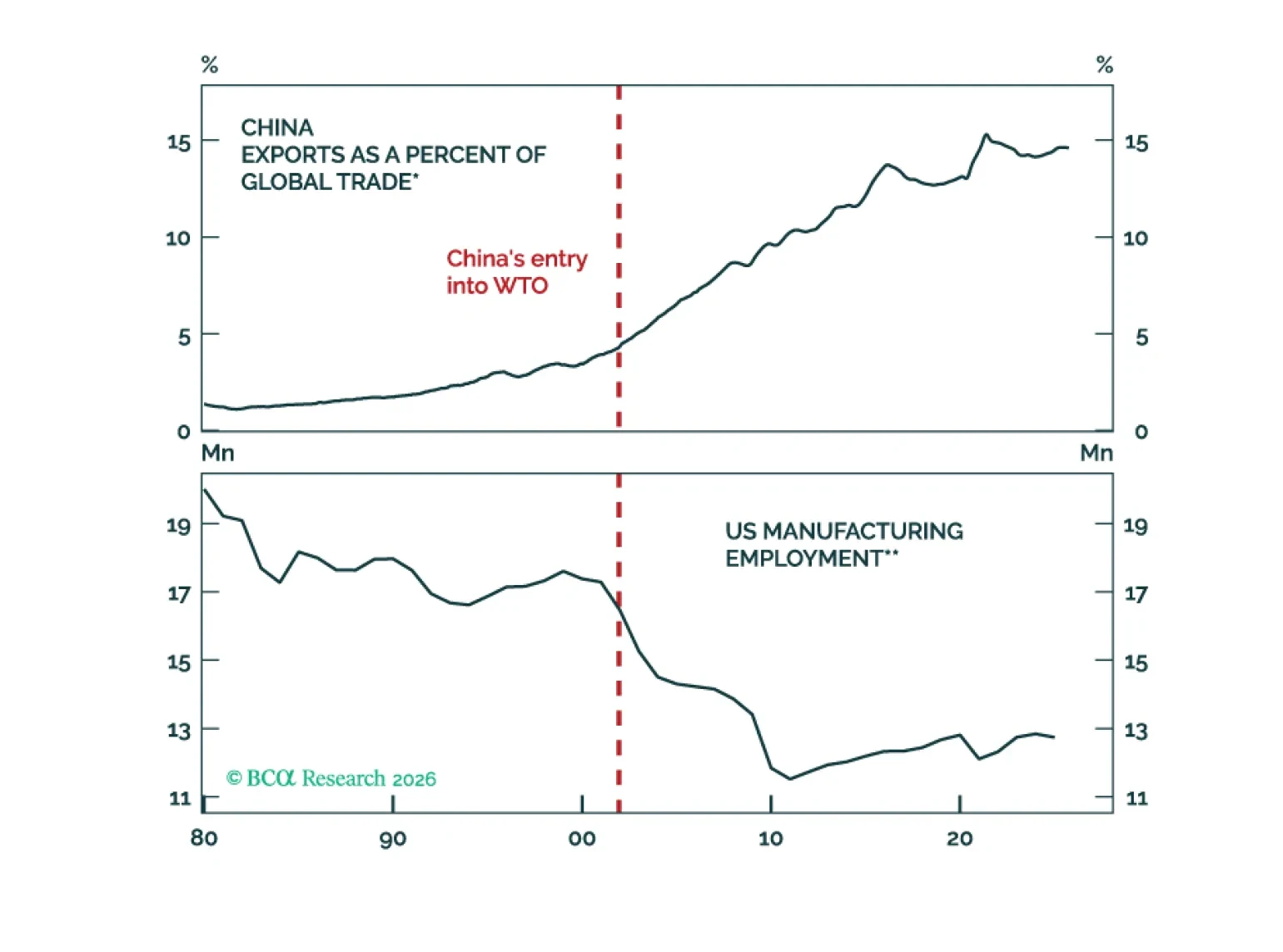

If humanoid robots were to become substitutable for workers, the AI age could lead to rapid growth in the size of the effective global labor force. The result could be a larger version of the “China shock,” which followed China’s entry into the global economy.

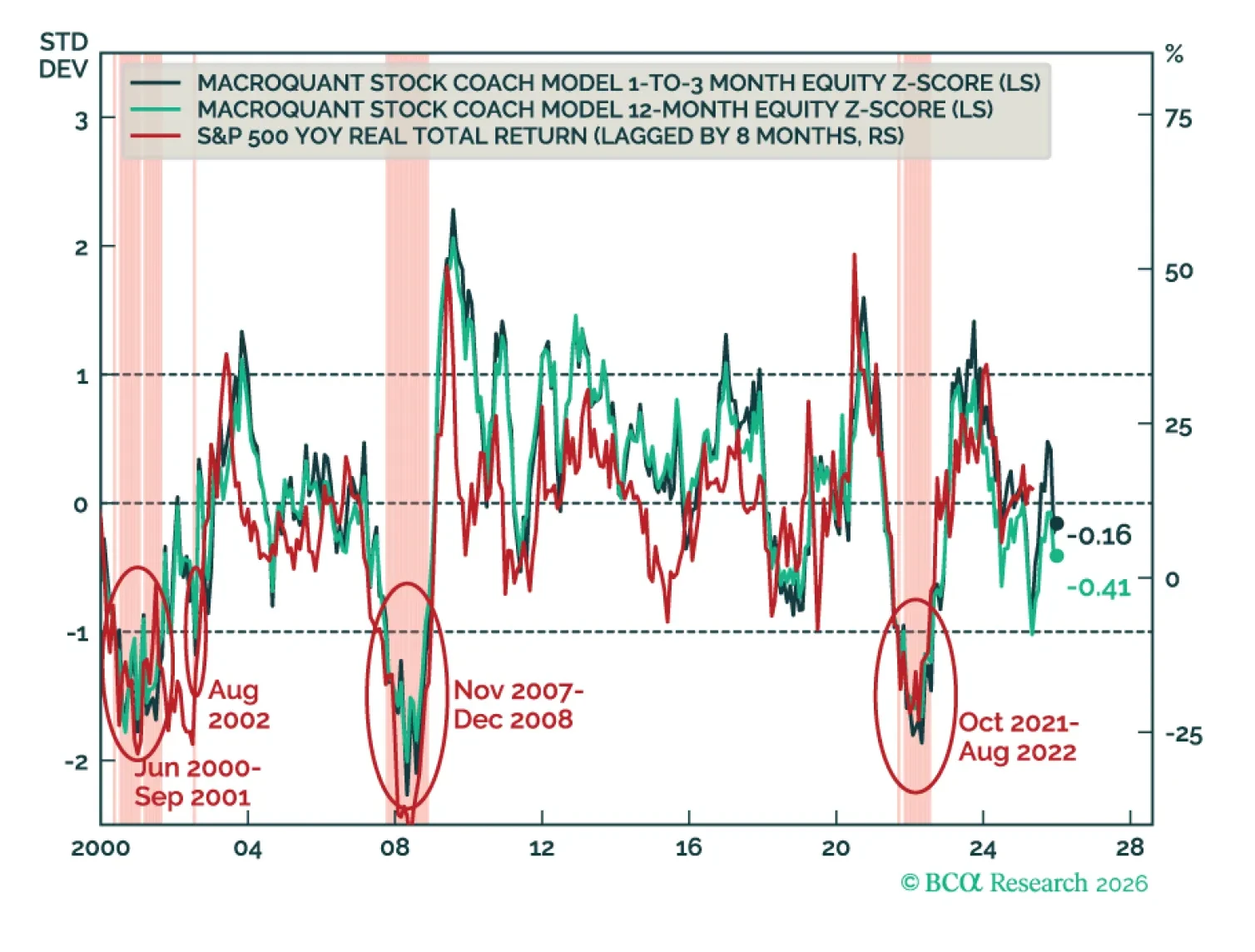

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

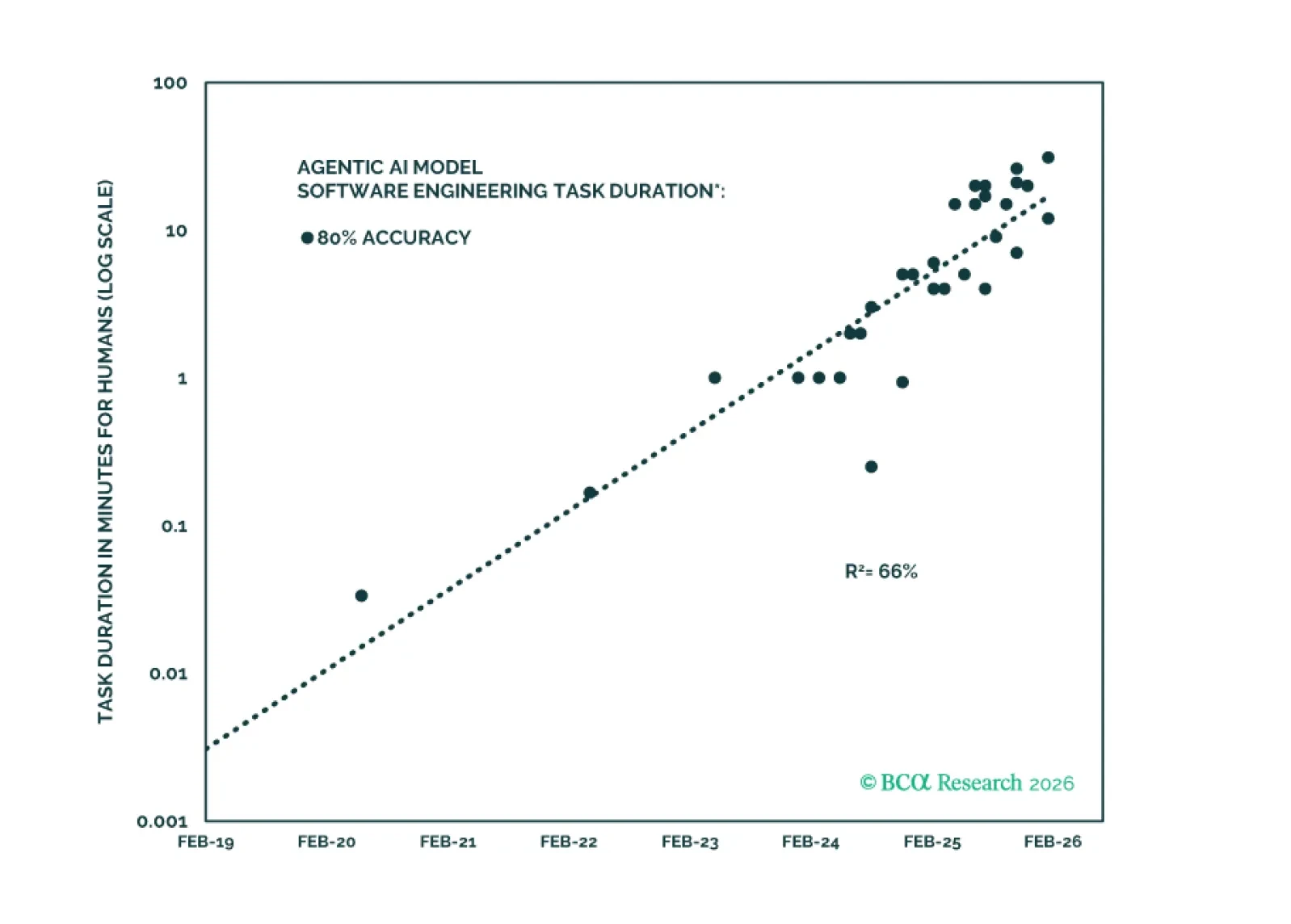

In Section II, Jonathan examines whether the AI “scaling laws” are likely to hold. They will over the near term, but cracks are already beginning to form in the narrative of ever-improving AI.