AI

Broad GenAI adoption and monetization, alongside falling inference costs, should make hyperscalers’ and enterprise investments worthwhile. While the GenAI boom echoes the dot-com era, it differs in key ways: Valuations are elevated but not extreme, and the rally is still underpinned by solid earnings growth. With few warning signs flashing red, the bull market likely has further to run, though a period of consolidation is overdue.

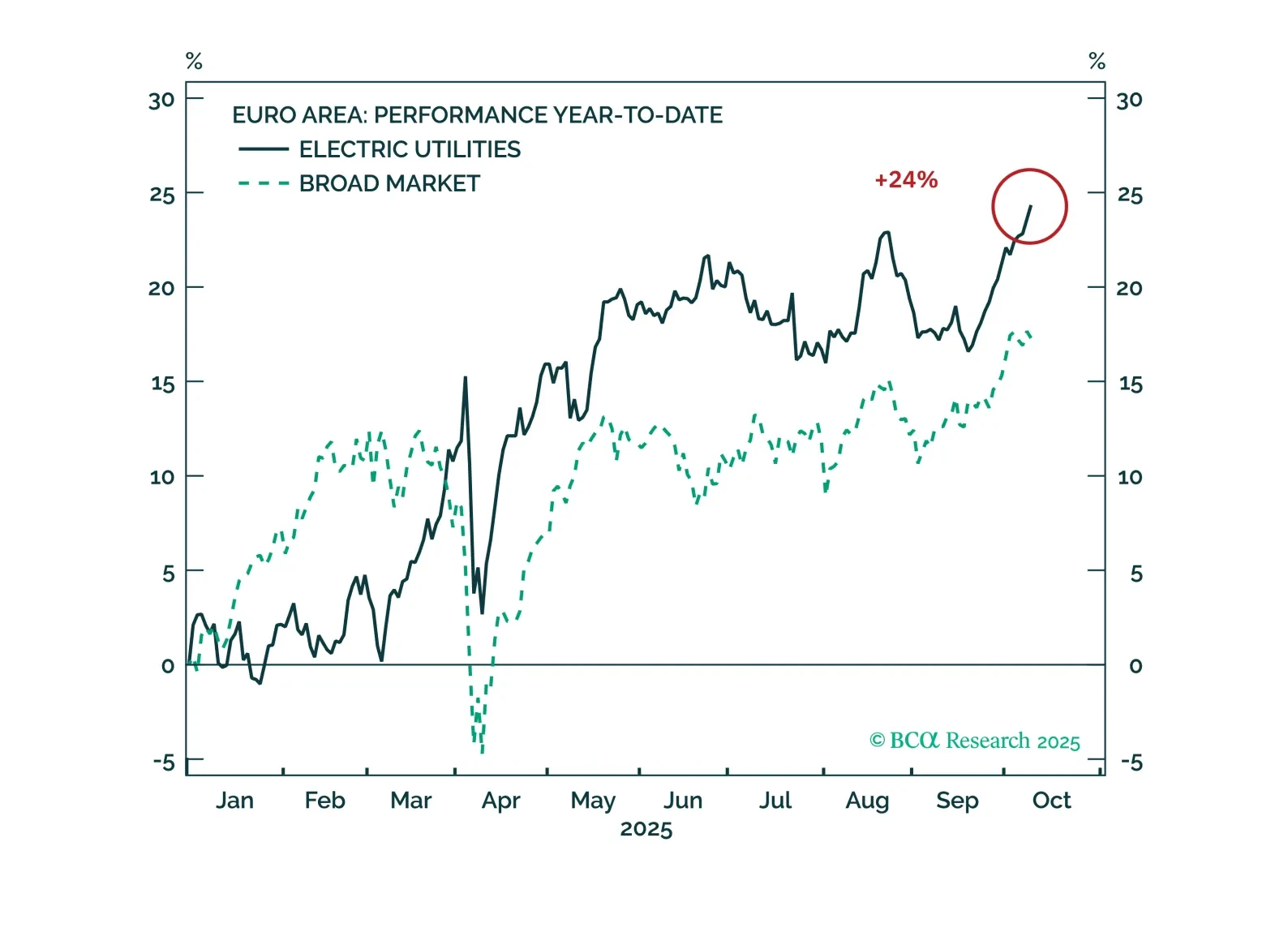

The structural demand base for electricity is expanding, requiring massive investment in grid capacity, storage solutions, and renewable generation. For investors, this trend highlights long-duration opportunities in utilities as electricity responds to the ever-growing needs of data centers and becomes the backbone of Europe’s decarbonized growth model.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.

We remain bullish both bonds and equities, but conviction is falling. We are Luddites when it comes to the AI theme, but we have followed it regardless. A bubble is a bubble, not to be shorted. Yet Europe’s weak AI returns reveal 2025’s real story: the fall of King Dollar.

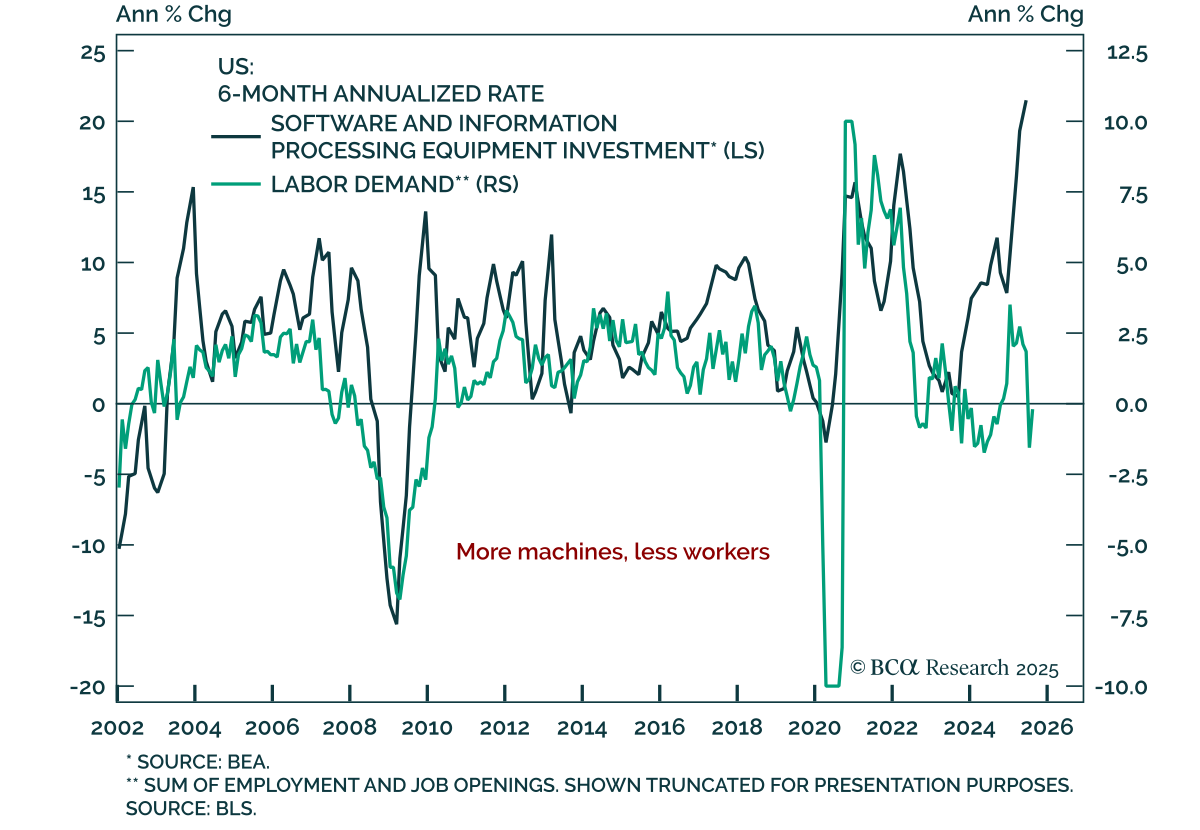

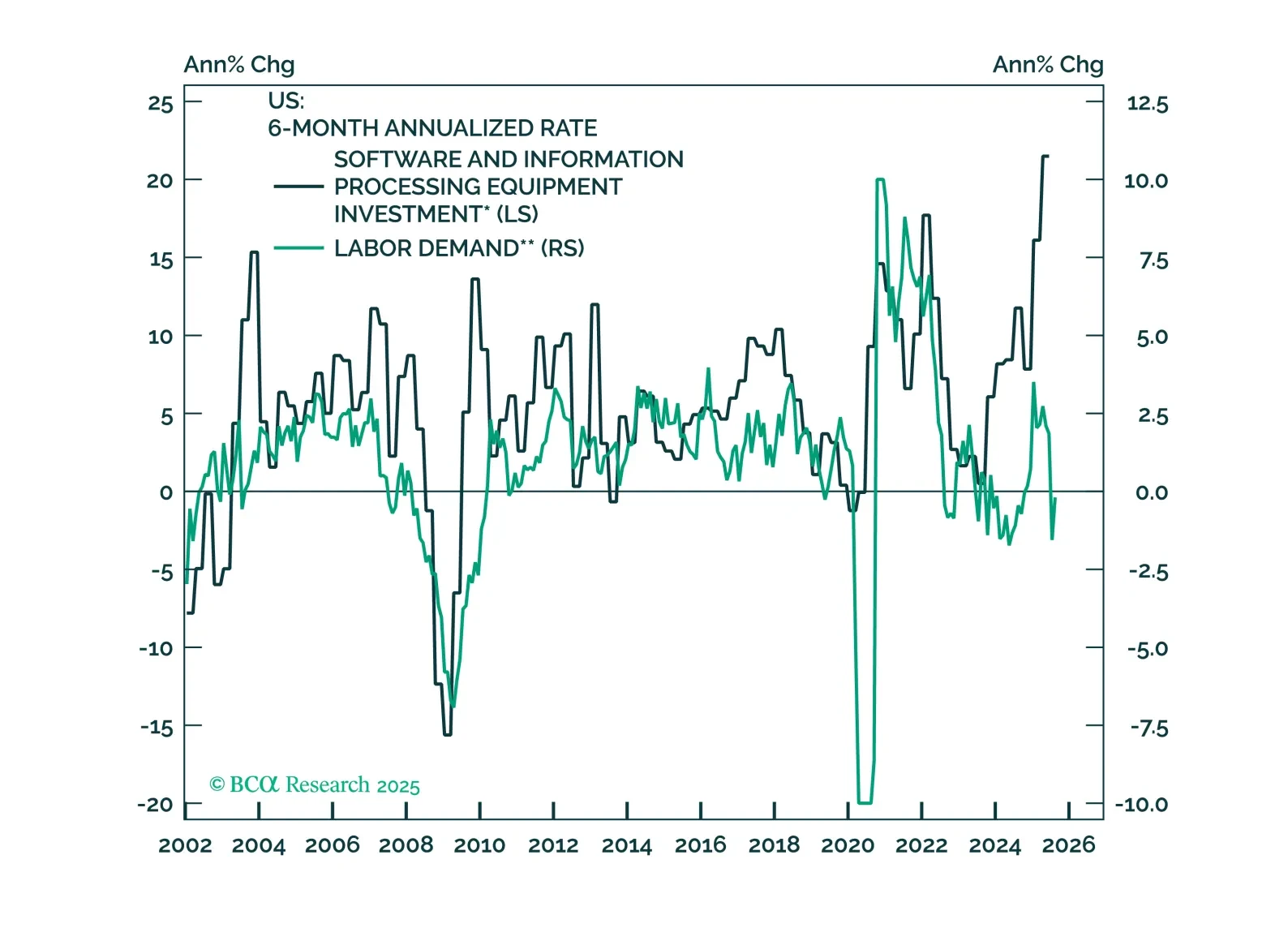

Big Tech and the Trump administration are engineering an industrial boom that favors American hardware over American workers. Economic growth will be robust in the US but the labor market will stay relatively sluggish. Adopt an overweight stance on both equities and fixed income and underweight on cash. Upgrade Canadian equities and downgrade the UK. Upgrade Industrials and downgrade Consumer Staples. Upgrade EM Debt. Downgrade Private Credit.

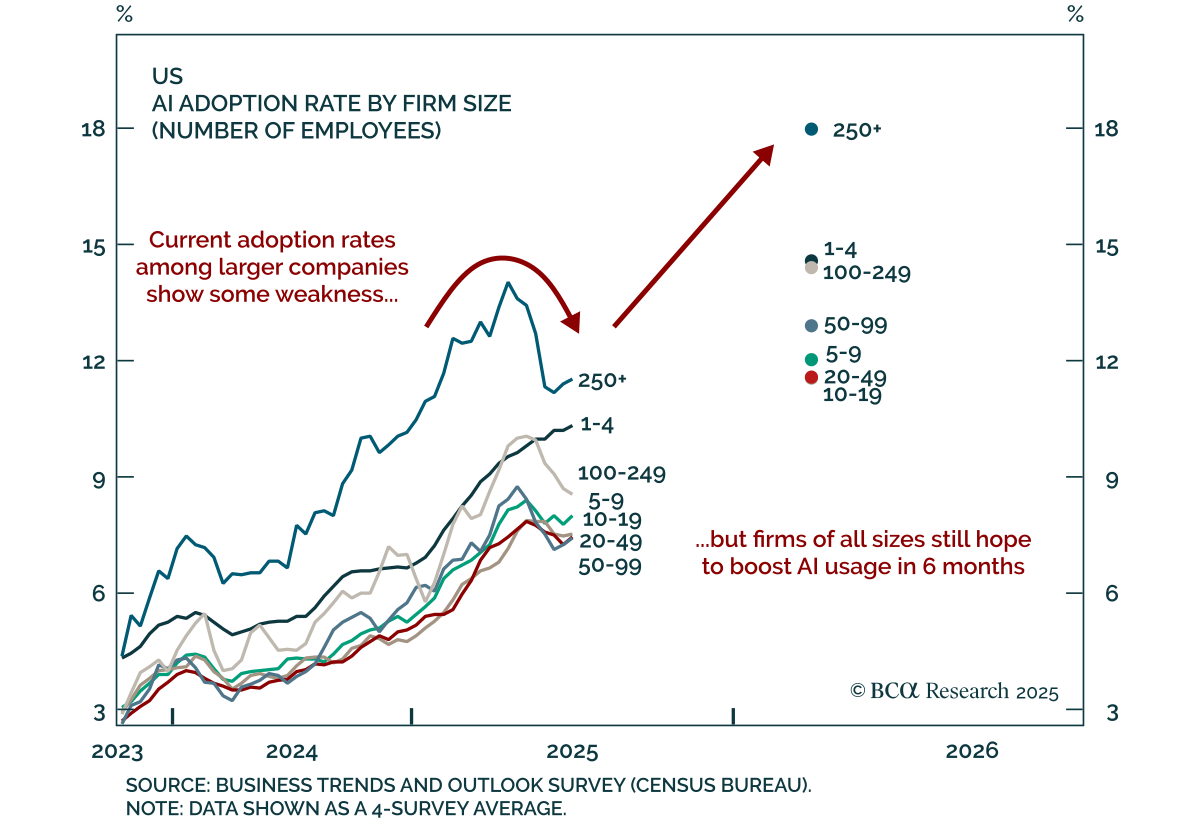

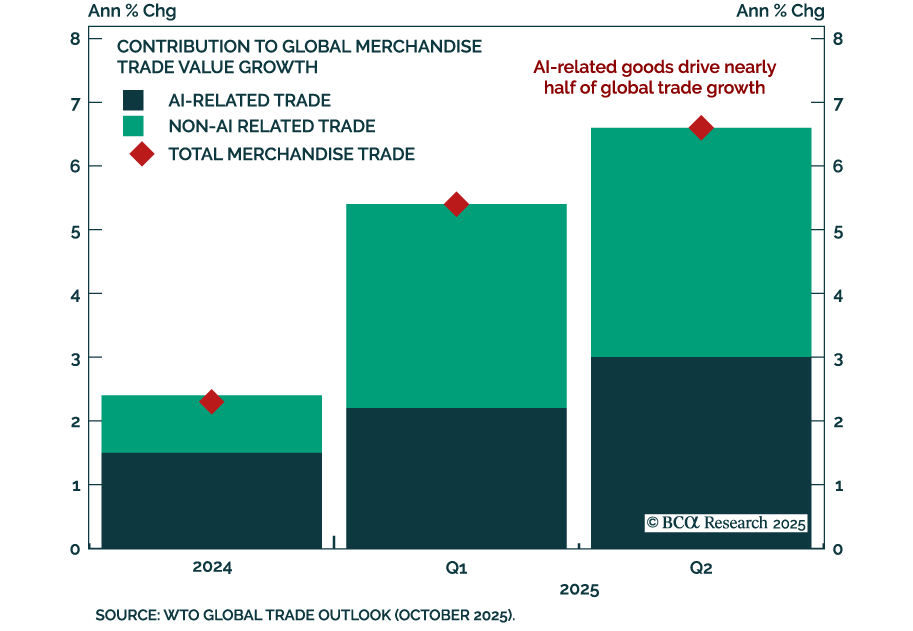

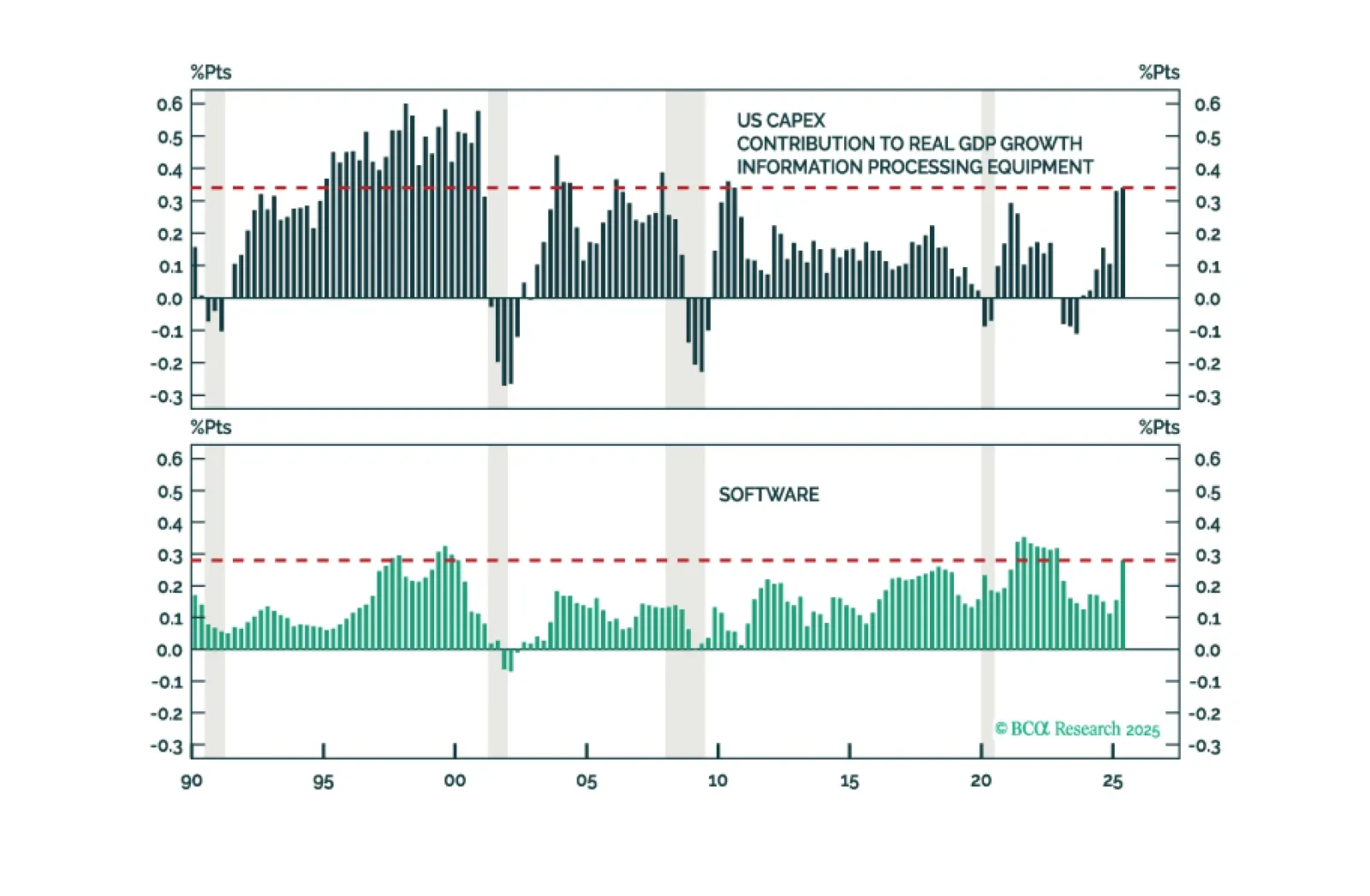

The AI capex boom is having a measurable impact on the economy but, so far, it is more muted than often cited.

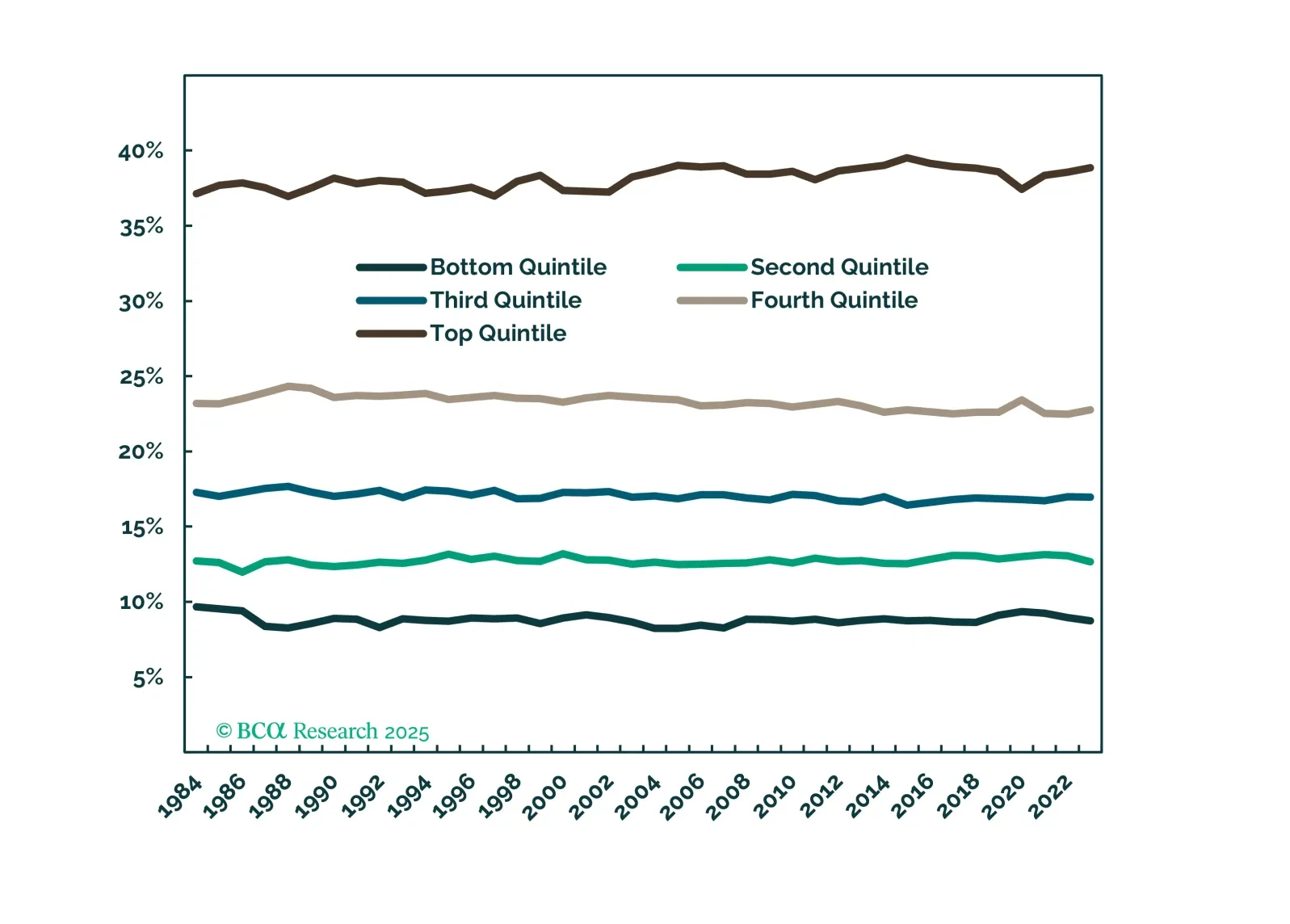

While it is not yet time to bet against risk assets, we push back on the increasingly popular ideas that the wealthiest households and/or AI-related capex can keep the expansion going despite the wobbling labor market.