AI

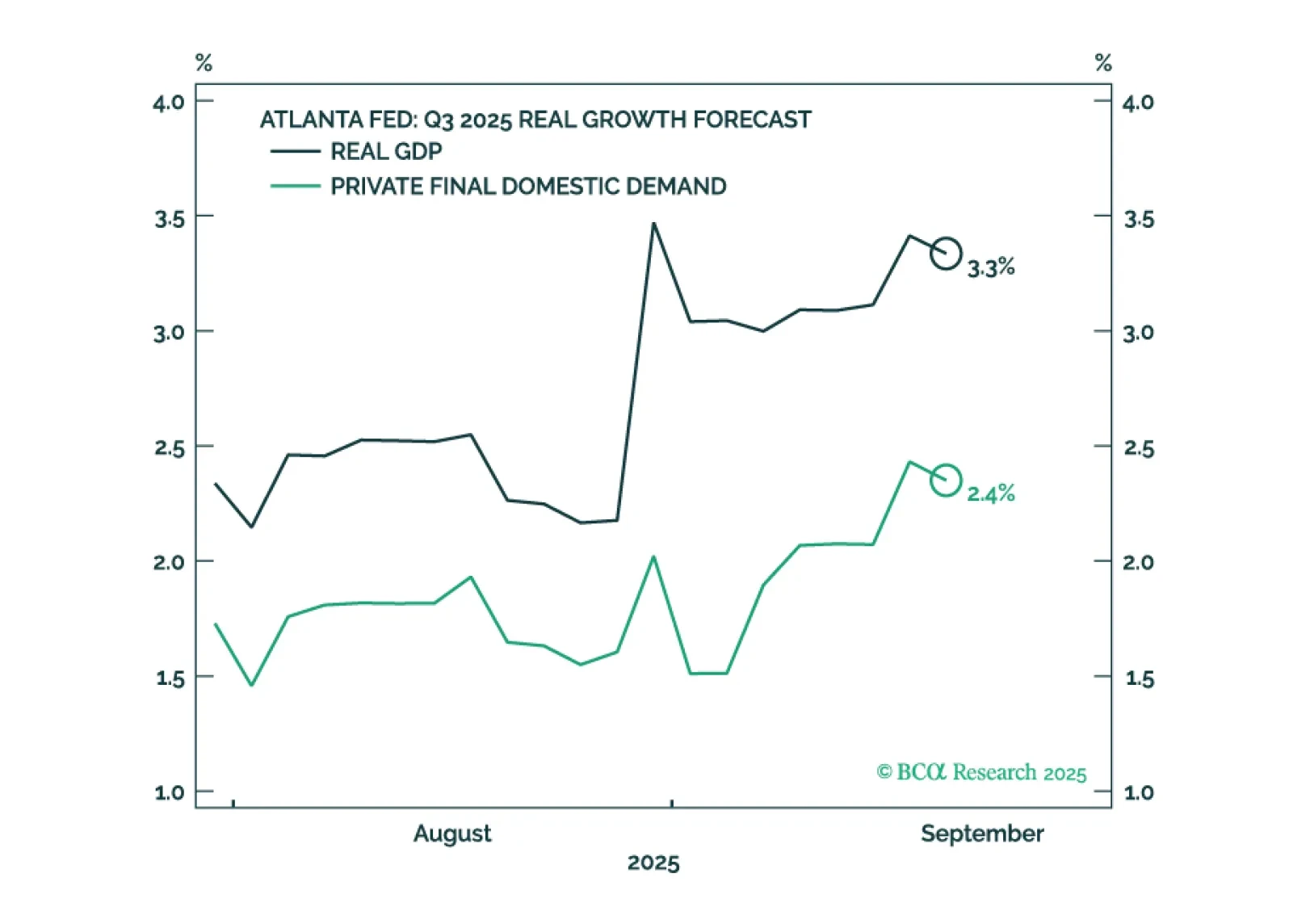

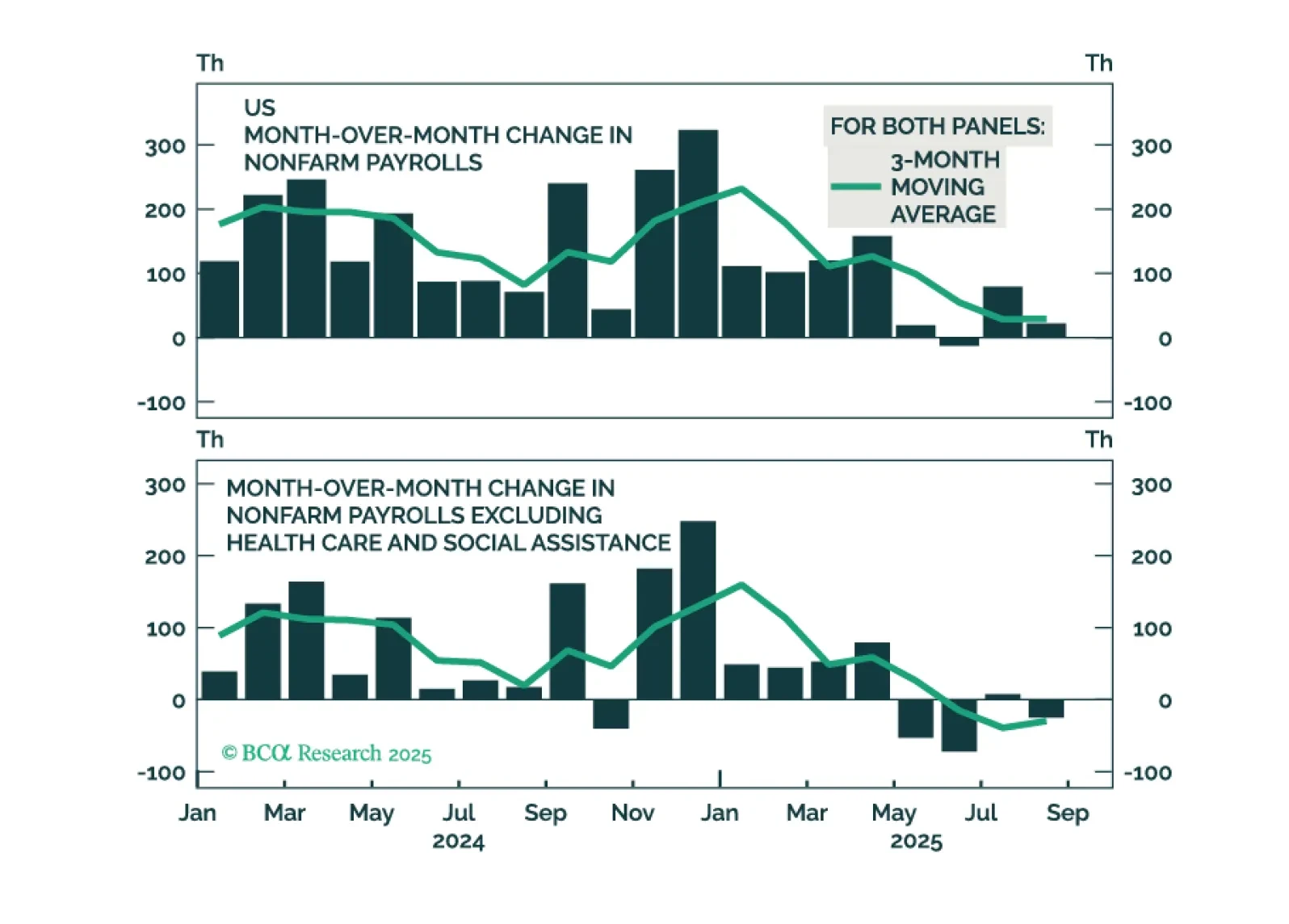

US GDP growth appears to have accelerated even as employment growth has faltered. We will make a final decision in early October when we publish our next Strategy Outlook, but most likely, we will cut our 12-month US recession probability to 40%-to-50% from 60% and turn tactically neutral on stocks, while still retaining a modest equity underweight over a 12-month horizon.

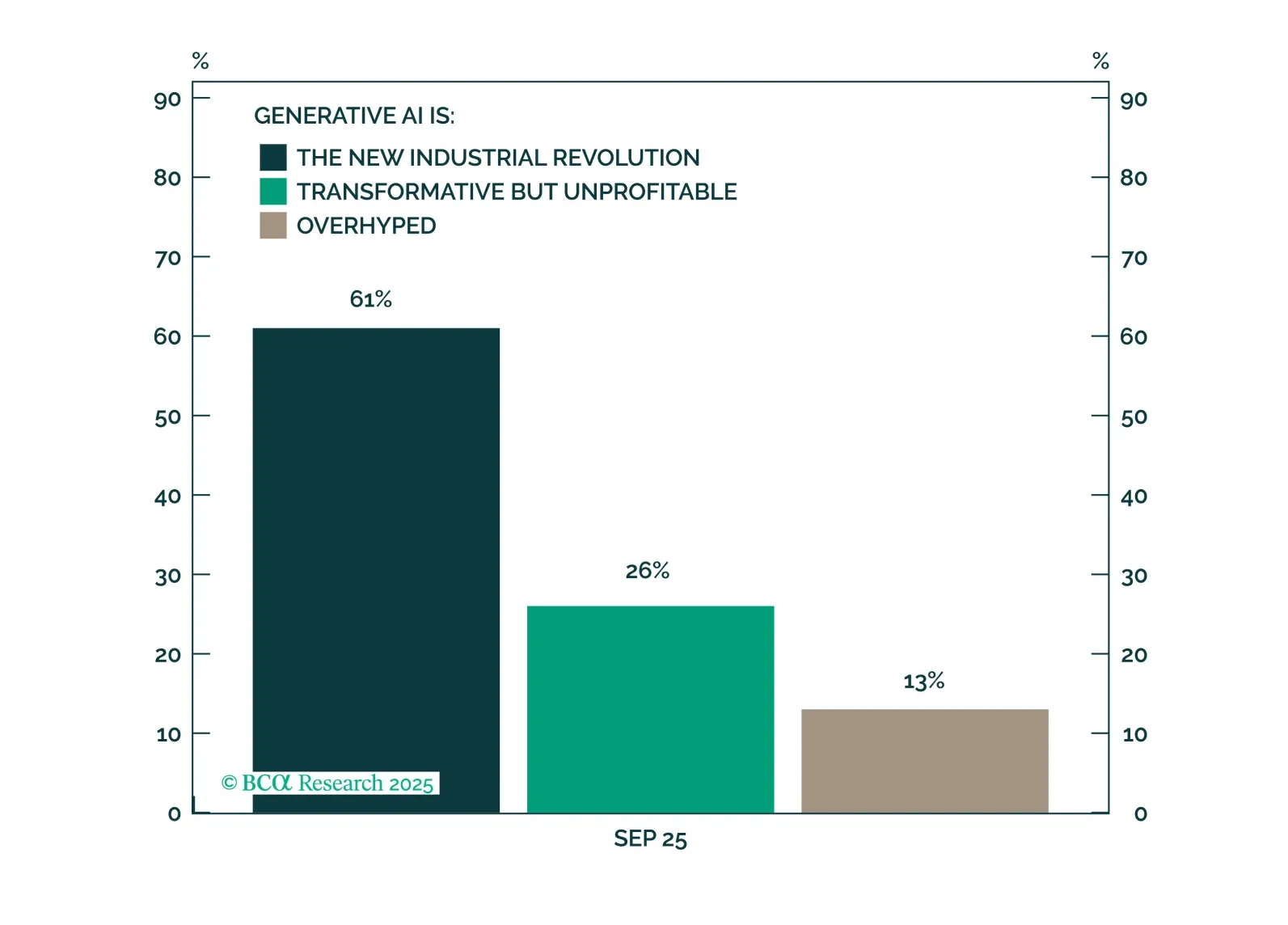

According to our latest client poll, most respondents are optimistic about the Generative AI's potential. Investors remain divided on whether current equity valuations reflect a bubble. Economic concerns continue to center on bond yields and the risk of stagflation, while relatively few clients anticipate a recession. In terms of portfolio positioning, an overweight in Technology received the strongest endorsement.

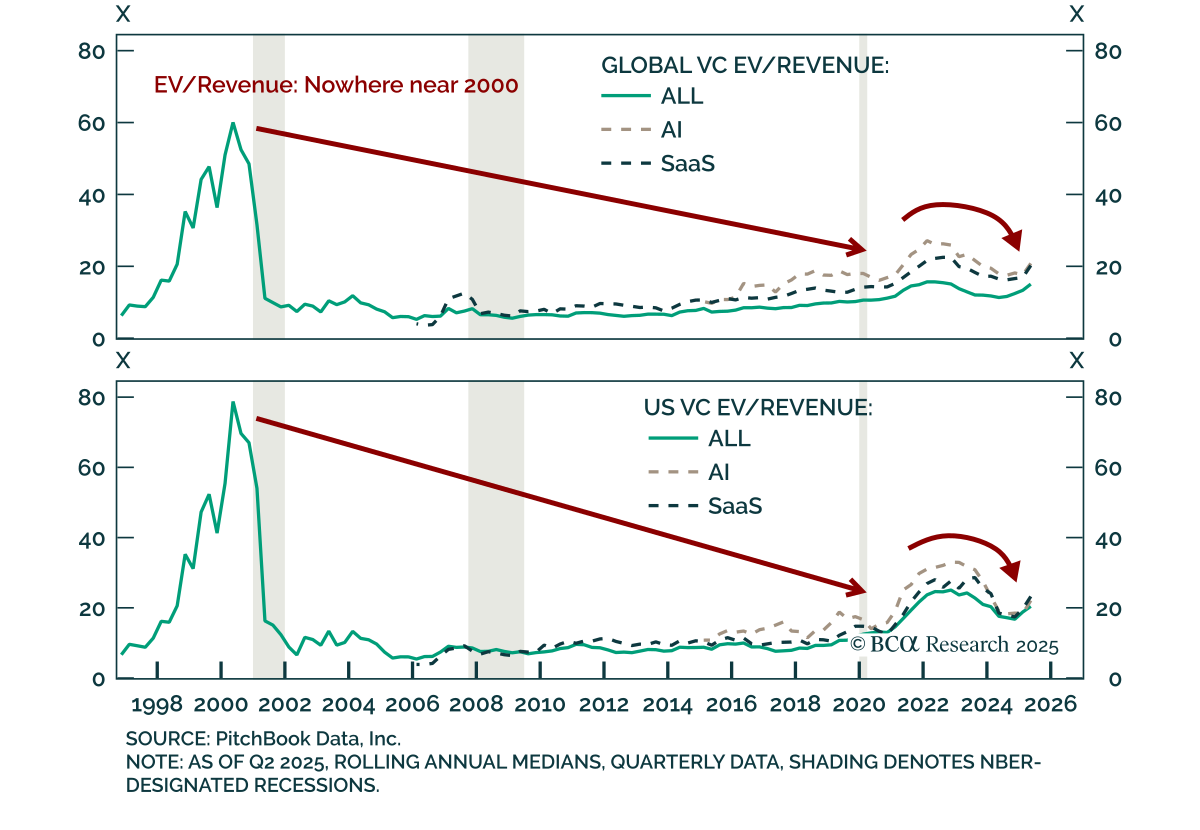

While it is impossible to know exactly when global equities will peak, there are now enough vulnerabilities to justify keeping one’s finger near the eject button.

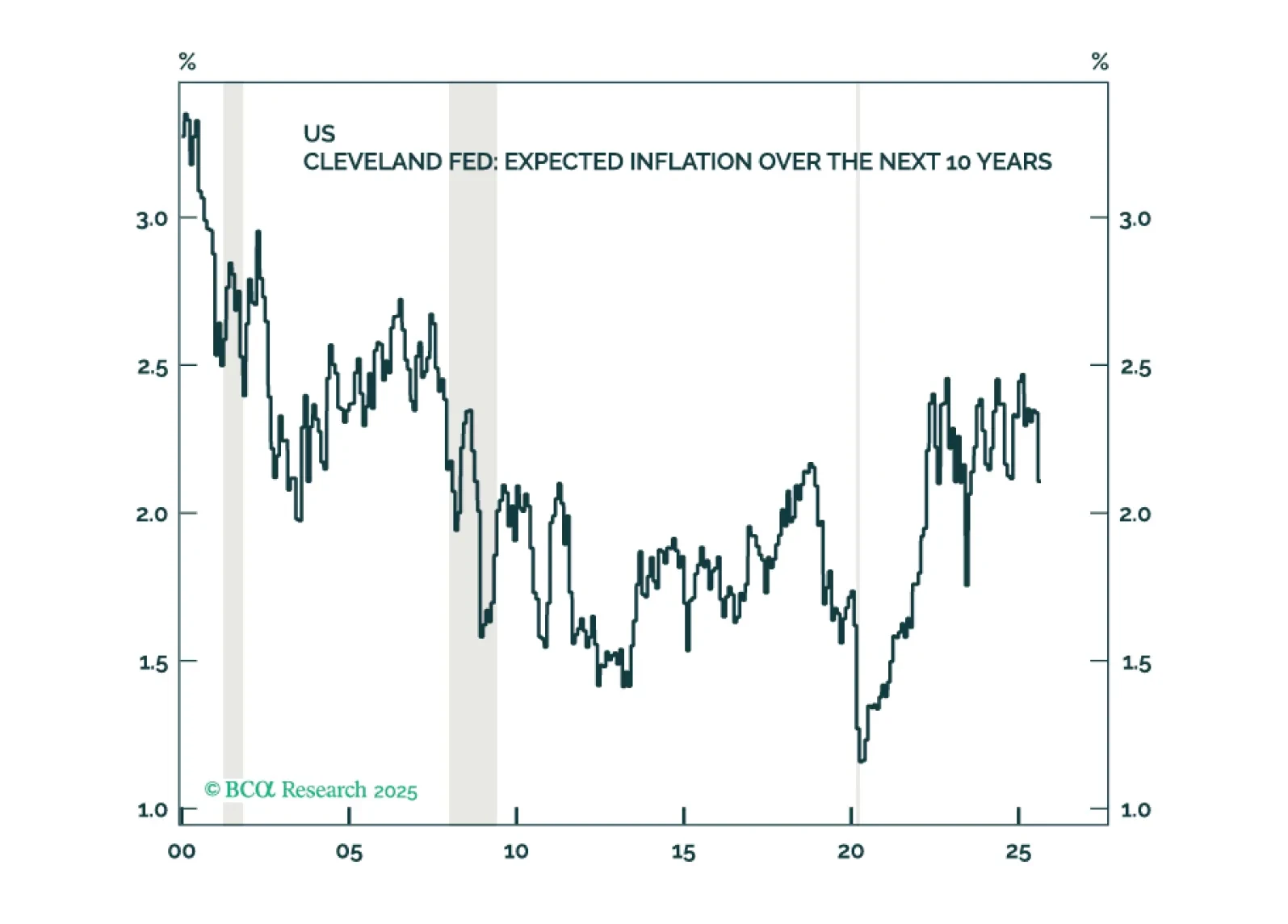

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

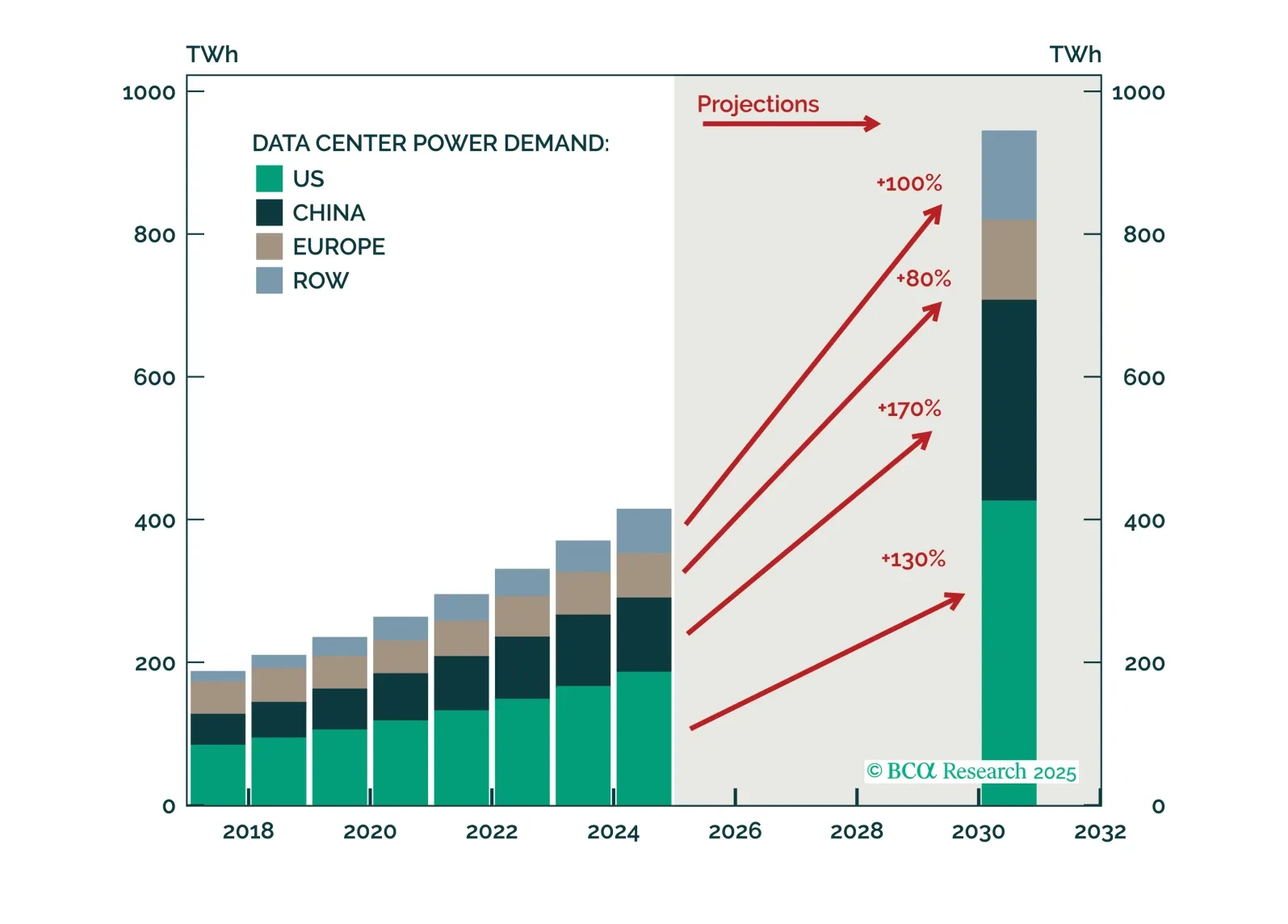

Renewables’ role in power-hungry data centers is overstated. Natural gas will fill clean electricity’s data center supply shortfall, particularly in the US and Europe.