Agricultural Chemicals

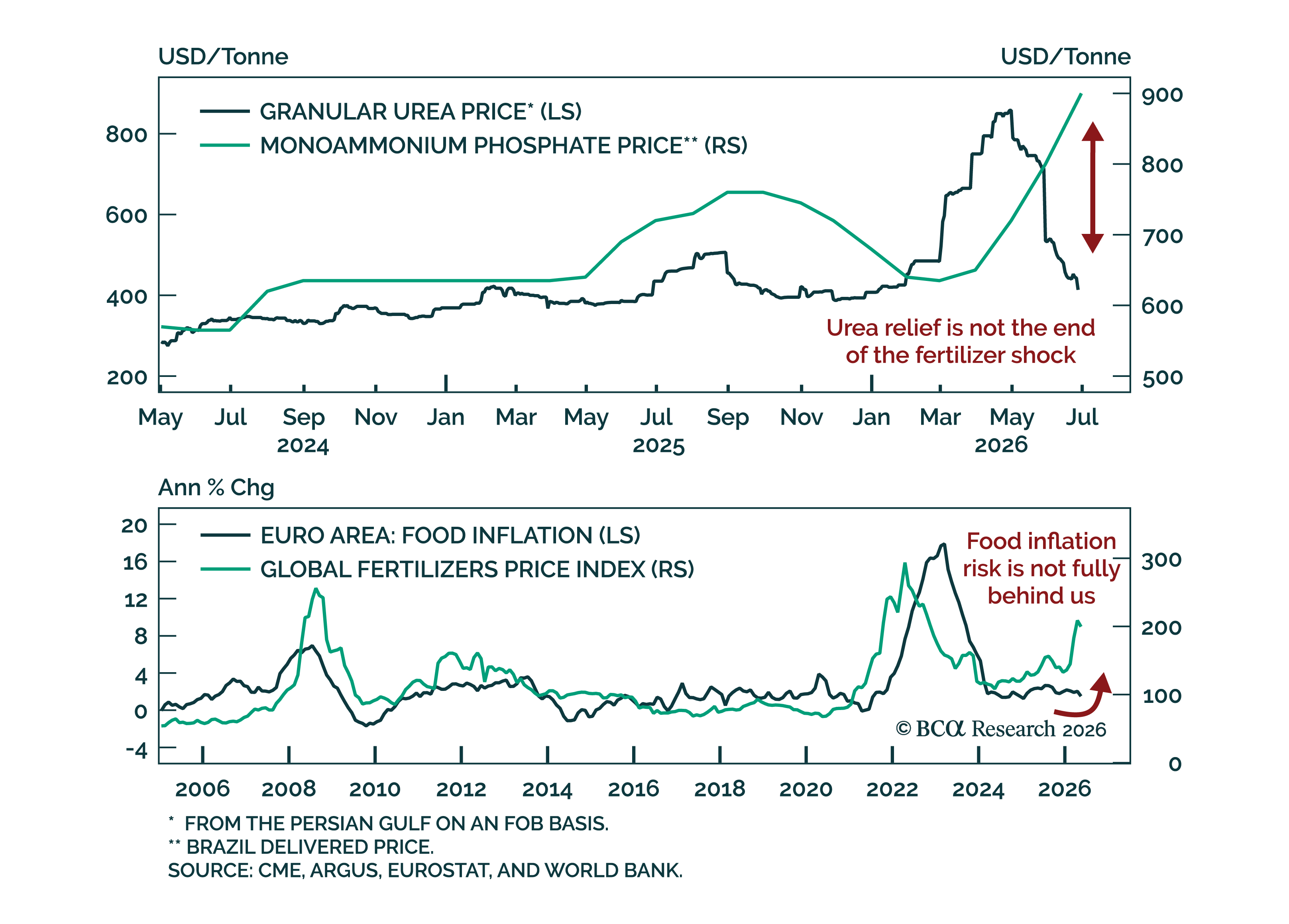

The collapse in urea prices is giving markets a false sense of relief; Europe should not assume the food shock is over. Granular urea price has fallen back to prewar level of $440/Tn, but only after farmers had already faced the worst of the Iran-driven…

Fertilizer prices will continue to move lower as the natgas price shock touched off by the Russian invasion of Ukraine dissipates. As a result, we expect grain prices to soften another 10% this year. Food-price inflation will move lower over the course of the year as grain prices weaken, provided a weather- or geopolitical shock does not once again send natgas prices higher.

We went overweight the S&P agricultural chemicals index in early May, a contrarian bet to take advantage of extreme bearishness, undervaluation and the potential for a rise in underlying commodity prices. Since then, a rise in industry M&A activity has borne out our thesis of cheap valuations, generating solid relative returns. Nevertheless, operating conditions may be slower to improve than originally anticipated. Burgeoning wheat and corn harvests this year threaten to keep the supply/demand balance for grains out of whack for another year. The USDA forecasts a hefty surplus in both key commodities. When grain prices advance, farm incomes receive a shot in the arm, providing farmers with both the means and the confidence to increase planting acreage, thereby boosting fertilizer demand. If food prices stay soft, then that positive dynamic is not going to take hold on a cyclical horizon. Instead, farmland prices will stay near cyclical lows, and agricultural-related credit availability will continue to tighten. The latter is already at a 10-year low, reflecting reduced farm incomes. Consequently, we recommend taking profits and downgrading to neutral. Please see yesterday's Weekly Report for more details. The ticker symbols for the stocks in this index are: BLBG: S5FERT - MON, MOS, CF.

Equities are celebrating domestic economic disappointment rather than re-pricing the risk of ongoing profit struggles. This reinforces that liquidity and share price momentum are still the dominant market forces.

Overweight Our early-May upgrade of the S&P agricultural chemical index proved timely, as Bayer launched a bid for Monsanto, sending the index up sharply. It is tempting to book gains, but if underlying profit drivers continue to move in a bullish direction, share prices should have further to go before extreme bearishness will normalize. Raw food prices continue to grind higher, and are likely to receive an assist from a weaker U.S. dollar now that the market is pushing out the imminence of future Fed rate hikes. The world grain stock-to-use ratio is still well below average, despite soft demand in recent years, and could fall further given the production decline. That is supportive of food prices, and should help farm incomes stabilize and boost credit availability. As shown in the May 9th Weekly Report, farm cash rents were already off their lows, a positive sign for underlying property valuations and a critical factor determining capital availability. It wouldn't take much of an increase in fertilizer demand to overcome depressed relative forward earnings expectations. We recommend staying overweight, despite the 12% gains that have accrued in such a short time span. The ticker symbols for the stocks in this index are: BLBG: S5FERT - MON, MOS, CF, FMC.

The bright side to higher food prices is that the S&P agricultural chemical index should finally be finished a brutal bear market. This group has been savaged by the collapse in agricultural commodity prices, worries about the return of Argentine supply and China's future import growth. The good news is that these headwinds are more than discounted. The share price ratio is close to a decade low, expectations are now extremely washed out, valuations are dirt cheap and the industry has retrenched, creating an attractive reward/risk profile. Importantly, the combination of U.S. dollar softness and two years of farming financial pain are sowing the seeds for a recovery in food prices. Global grain production contracted last year, after several years of strong growth, while shipments of pesticides and fertilizers are accelerating. Typically, food prices recover after production falls, particularly if the U.S. dollar declines. A weaker U.S. dollar boosts purchasing power in the rest of the world, which bodes well for increased food consumption, and it reduces the ability of global food exporters to flood the market and keep prices depressed. Higher food prices would stop the erosion in farming real estate values after a difficult few years, a necessary step to improving capital availability. Already, cash rents are off their lows, a positive sign for underlying property valuations. In sum, current agricultural conditions are depressed, but we can envision a slow but steady improvement as food prices climb on the back of a weaker U.S. dollar and supply restraint, which would support narrower risk premiums in related equities. Boost the S&P agricultural chemicals to overweight from underweight, locking in a 34% profit on this call, and please see yesterday's Weekly Report for more details. The ticker symbols for the stocks in this index are: BLBG: S5FERT - MON, MOS, CF, FMC.

U.S. dollar softness has failed to lift equities of late, a tentative warning that correlations are changing as the U.S. economy cools.