Air Freight & Logistics

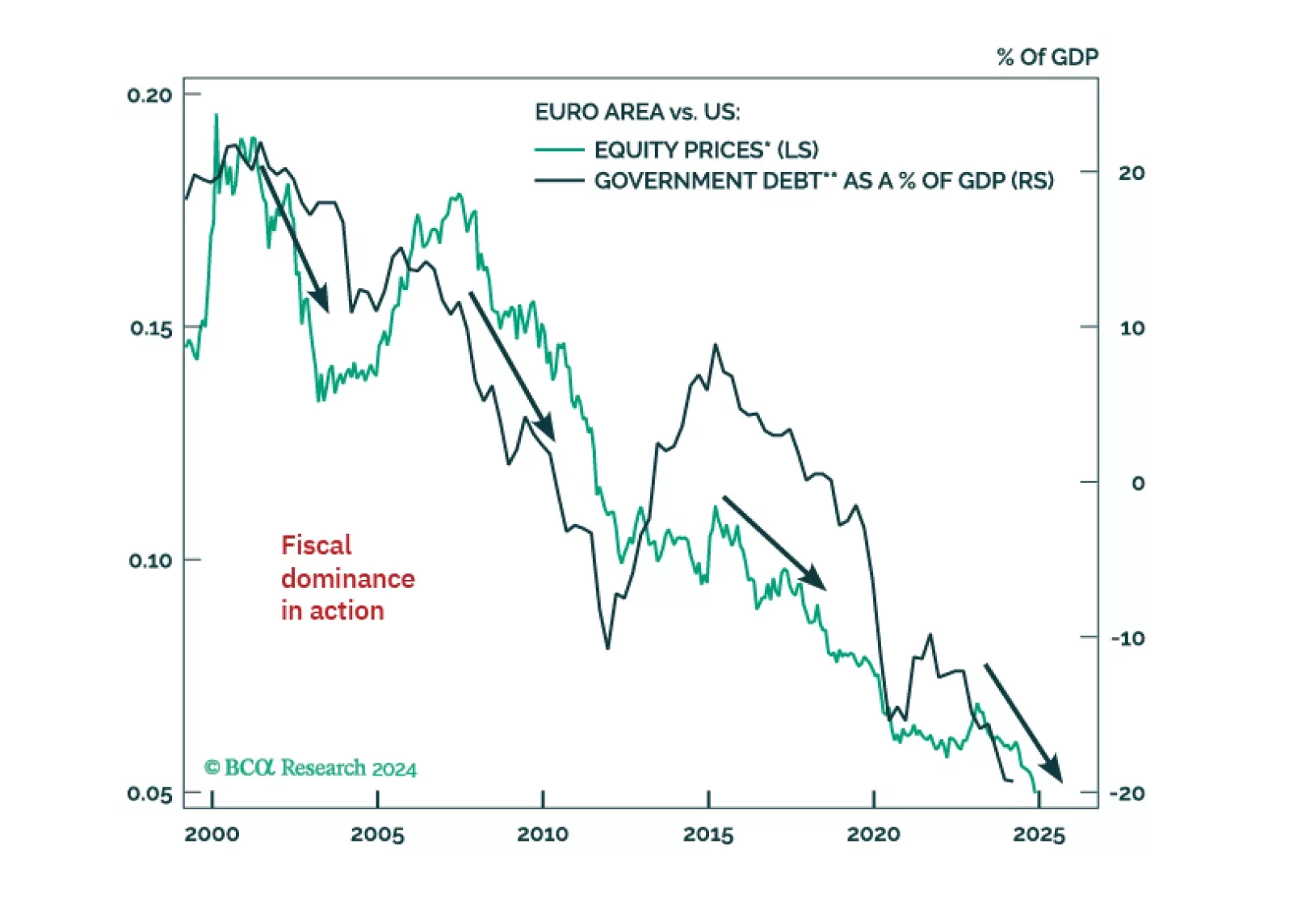

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

The 10-year Treasury yield rose in the aftermath of the Fed’s jumbo rate cut on Wednesday. Our US Bond strategists noted that this move reflects the fact that the downward revisions to the dots still fall short of the magnitude of cuts embedded in the…

Neutral - Downgrade Alert The transportation industry is a bellwether for the economy as rising freight hauling services demand is synonymous with firming economic activity and vice versa. The recent FedEx earnings report raised red flags both for the wellbeing of the transport sector (second panel) and the U.S. economy, especially the highly cyclical manufacturing sector. The company blamed soft global macro conditions and significantly trimmed profit guidance for its fiscal year. FedEX also highlighted that the absence of a trade deal with China complicates the free movement of goods (bottom panel) and the longer the uncertainty between the U.S. and China remains in place, the longer it will take for global trade growth to heal. One saving grace for air freight stocks has been the industry’s pricing power rebound, but there are mushrooming signs that sector inflation will cool down in the coming months (third panel). We have been neutral on the S&P air freight & logistics index since removing it from our high-conviction overweight list following previous FedEx profit warning, and now we are putting this transportation subgroup and the overall transportation index on our downgrade watchlist. Bottom Line: We are neutral the S&P transportation index, but now have it on downgrade alert. Our barbell strategy within transports remains in place overweighting airlines, neutral on air freight & logistics (but it is now on downgrade alert) and underweighting rails. Stay tuned.

Highlights Portfolio Strategy Corporate sector selling price inflation is nil while leading wage inflation indicators signal additional labor cost increases in the coming months. The risk is that profit margins have already peaked for the cycle. We reiterate our tactically cautious overall equity market view. Galloping higher private and public sector software outlays, a structurally enticing software demand backdrop and ongoing industry M&A all signal that it still pays to be bullish software stocks Recent Changes Last Thursday we downgraded the S&P railroads index to underweight. Also last Thursday we trimmed the S&P air freight & logistics index to neutral. Table 1 Feature The SPX stalled last week, digesting the now-complete Fed pivot. Our sense is that the Fed’s dovish turn is now fully reflected in equities. Importantly, the longer and wider the dichotomy between stocks and bonds gets, the more painful the ramifications from the eventual snap will be, likely with equities yielding to the bond market (Chart 1). As we first posited on March 4, short-term equity market caution is still warranted.1 Chart 1Time To Get Back Together While the Fed meeting and sharp decline in Treasury yields dominated headlines last week, it was the NFIB’s latest release that really caught our attention. Importantly, it revealed that taxes and big government are no longer the biggest problems facing small and medium business owners, but labor is: “Twenty-two percent of owners cited the difficulty of finding qualified workers as their Single Most Important Business Problem, only 3 points below the record high. Ten percent of owners find labor costs as their biggest problem, a record high for the 45-year survey.”2 Historically, such extreme tightness in the SME labor market is a precursor of a yield curve inversion (NFIB cost of labor shown inverted, Chart 2). The link is clearer if we show this same NFIB series with the Labor Department’s average hourly earnings monthly release that is currently running at a 3.4%/annum clip (Chart 3). In other words, a tight labor market is conducive to corporations bidding up the price of labor which in turn causes the Fed to raise interest rates, eventually inverting the yield curve. Chart 2Cycle Is Long In The Tooth Chart 3Wage Growth... This macro backdrop is slightly unnerving and our biggest concern is the S&P 500’s profit margins (Chart 4). Q3/2018 marked the all-time peak in SPX quarterly margins according to Standard & Poor’s,3 and in Q4/2018 margins have deflated from a high mark of 12.13% to 10.11%, or a 16.7% q/q drop. Chart 4...Denting Margins Undoubtedly, last year’s fiscal easing-induced all-time highs in SPX margins is unsustainable, and a tight labor market is a warning shot. Using the same NFIB series on cost of labor being the most important problem SMEs face and subtracting it from our corporate pricing power proxy, we constructed an equity market margin proxy, shown as a Z-score in Chart 5. Historically, the y/y change in SPX profit margins move in lockstep with our margin proxy and the current message is grim (Chart 5). Chart 5Margin Trouble Ahead Before getting too bearish though, we want to make three salient points: First, while the NFIB survey’s labor related indicators are disconcerting, unit labor costs – the best measure of wage growth – remain muted as productivity growth has ramped up recently. Second, using empirical evidence dating back to the 1960s, the ultimate SPX profit margin mean reversion occurs during recessions, when EPS suffer a major setback. The implication is that margins can move sideways or grind lower in the coming year. As a reminder, BCA’s review remains that the U.S. will avoid recession in the next 12 months. Third, the most important yield curve slope, the 10/2, has not yet inverted, and even when it does invert, investors will have time to start positioning defensively; we have shown in recent research that the S&P peaks after the yield curve inverts.4 On a related note, we use this opportunity to update our corporate pricing power proxy, and Table 2 summarizes the sectorial results. Table 2Industry Group Pricing Power Corporate sector selling price inflation has ground to a halt at a time when wage inflation is rearing its ugly head. Worrisomely, our pricing power diffusion index’s breadth sunk below the 50% line, whereas our wage growth diffusion index spiked higher; 70% of the 44 industries we track are struggling with rising wages (second & third panels, Chart 6). Taken together, there is evidence that broad-based profit margin pressures are escalating, the mirror image of what our gauges were signaling in our last update late-last year.5 Chart 6Margins Have Likely Peaked Digging beneath the surface of our corporate pricing power proxy is revealing. As a reminder, we calculate industry group pricing power from the relevant CPI, PPI, PCE and commodity growth rates for each of the 60 industry groups we track. Table 2 also highlights shorter term pricing power trends and each industry's spread to overall inflation. 57% of the industries we cover are lifting selling prices, but only 27% are raising prices at a faster clip than overall inflation. Both figures are lower than our early-November report. Outright deflating sectors increased by eight to twenty four since our last update, fifteen of which are deflating at 1%/annum pace or lower. One third of the industries we cover are experiencing a downtrend in selling price inflation, representing a 43% increase since our most recent report (Table 2). Deep cyclicals/commodity-related industries (ex-oil) continue to dominate the top ranks, occupying the top six slots (Table 2). Despite the ongoing global manufacturing deceleration and still unresolved U.S./China trade tussle, the commodity complex's ability to increase prices remains resilient. On the flip side, energy-related industries occupy the bottom of the ranks as WTI crude oil is still 22% lower than the most recent peak in October 2018. In sum, business sector selling price inflation is nil while leading wage inflation indicators signal additional labor cost increases in the coming months. The risk is that profit margins have already peaked for the cycle. We reiterate our tactically cautious overall equity market view. This week we update a high-conviction overweight tech subgroup and recap our transportation subsurface moves from last Thursday. Buy The Software Breakout Software stocks are on fire and leading profit indicators suggest that more gains are in store in the coming months. Last week, we published a table ranking all the sectors and subsectors by 12-month forward profit growth estimates (please refer to Table 2 from the March 18 Weekly Report). While the broad tech sector is on an even keel with the SPX, software EPS are racing at twice the speed of the broad market, roughly 14%. Keep in mind, when growth gets scarce, investors flock to industries with accelerating profit prospects. The software profit juggernaut is intact and we reiterate our high-conviction overweight recommendation. Sustained capital outlays on software are a key driver of industry profits (bottom panel, Chart 7). In an otherwise muted Q4 GDP release, rising non-residential fixed investment in general and surging investment in software in particular suggest that our bullish software capex thesis is alive and kicking (middle panel, Chart 7). Chart 7Software On A Tear The move to cloud computing and SaaS, the proliferation of AI, machine learning and augmented reality are not fads but enjoy a secular growth profile, and signal that capital outlays on software are also in a structural uptrend. Not only private sector software capex is near all-time highs as a share of total outlays, but also government investment in software is reaccelerating at the fastest pace since the tech bubble. When productivity gains are anemic, both the business and government sectors resort to software upgrades in order to boost productivity. Cyber security is another more recent source of software related demand as governments are taking such risks extremely seriously the world over (second panel, Chart 8). Chart 8Earnings Led Advance Meanwhile, fear of missing out has rekindled industry M&A and both the dollar amount and number of deals are sky high, with acquirers bidding up premia to the stratosphere (Chart 9). This supply reduction is bullish for industry pricing power. Chart 9M&A Frenzy Granted the M&A frenzy has pushed relative valuations on the expensive side especially on a forward P/E basis, but on EV/EBITDA software stocks are trading below the historical mean and still significantly lower than the late-1990s peak valuation (bottom panel, Chart 8). If our bullish software profit thesis continues to pan out, then software stocks will grow into their pricey valuations. Finally, shareholder friendly activities are ongoing in this key tech subsector and buybacks in particular provide an added layer of artificial EPS growth (bottom panel, Chart 9). Adding it up, galloping higher private and public sector software outlays, a structurally enticing software demand backdrop and ongoing industry M&A, all signal that it still pays to be bullish software stocks. Bottom Line: Buy the software breakout. The S&P software index remains a high-conviction overweight. The ticker symbols for the stocks in this index are: BLBG: S5SOFT – MSFT, ORCL, ADBE, CRM, INTU, ADSK, RHT, CDNS, SNPS, ANSS, SYMC, CTXS, FTNT. Tweaking Transport Subgroup Positioning The S&P transports index’s recovery rally has stalled recently and is a cause for concern for the overall market. In more detail, the recent gulf between relative share prices and the SPX has widened and warns that the overall market is at a risk of suffering a pullback (Chart 10). Chart 10Engine Trouble Thus on Thursday last week, we made two subsurface transport changes, downgrading a subgroup to underweight that commands lofty valuations at a time when leading profit indicators are flashing red, and also downgrading to neutral a globally exposed transport sub-index. Get Off The Rails In our downgrade of the S&P railroads index late last year to a benchmark allocation, we highlighted that two of our key industry Indicators, the Railroad Indicator and our Rail Shipment Diffusion Indicator, had turned negative.6 These indicators have continued to deteriorate, including total rail shipments which have now started to contract for the first time since the 2015-16 manufacturing recession (third panel, Chart 11). Intermodal shipments in particular have nosedived, likely a result of weak retail sales, as we highlighted earlier this month.7 Chart 11Downgrade Rails To... This contraction would be far less concerning were it not for the rapid degradation of industry balance sheets as firms have sought to increase relatively cheap leverage in order to retire equity. Railroads are now significantly more indebted than the broad market which itself has not shown an aversion to adding leverage (bottom panel, Chart 11). Such a change in railroad capital structure has kept EPS growth rates artificially high while simultaneously adding an extra measure of equity risk premium that does not yet appear fully reflected in relative share prices. Moreover, when we downgraded the S&P railroads index to neutral last year, deteriorating Indicators were offset by exceptionally healthy pricing power.8 After a multi-year expansion, selling price inflation has now rolled over (second panel, Chart 12), taking away the remaining pillar supporting a neutral view which compelled us to move to an underweight allocation last week. Chart 12...Underweight Pricing power is one of the key determinants in our earnings model that, when combined with the previously noted contracting volumes, is indicating the end to the industry’s above-trend earnings growth is nigh (third panel, Chart 12). With relative earnings growth slowing and rising leverage adding incremental risk, the S&P railroads index’s premium valuation multiple looks increasingly dicey (bottom panel, Chart 12). Bottom Line: Broad based declines in traffic volumes, falling pricing power and high leverage suggest that earnings will underwhelm. Accordingly, last Thursday we moved to an underweight recommendation on the S&P railroads index as we expect a de-rating phase to materialize. The ticker symbols for the stocks in this index are: BLBG: S5RAIL - UNP, CSX, NSC, KSU. Air Freight Had Its Wings Clipped We have been offside on the high-conviction overweight call on the S&P air freight & logistics index and the recent FedEx warning suggests that profits will come under pressure for this index for the rest of the year and will trail the SPX. As such, we trimmed exposure to neutral late-last week and removed it from the high-conviction overweight list for a loss of 14%. Chart 13 shows that all the profit drivers we had identified in early December last year have taken a sharp turn for the worse. Energy costs are no longer in deflation as oil prices have jumped from $42/bbl to near $60/bbl. Not only is global growth still decelerating, but also U.S. growth is in a softpatch: the manufacturing shipments-to-inventory ratio is on the verge of contraction, warning that delivery services’ selling prices are in for a turbulent ride (second panel, Chart 13). In addition, definitive news of Amazon becoming a formidable competitor in courier delivery services is structurally negative for the industry. Chart 13Air Freight: Move To The Sidelines Nevertheless, we refrain from turning outright bearish as air freight stocks are technically oversold and valuations are trading at the steepest discount to the broad market since mid-2002. Bottom Line: Last Thursday we downgraded the S&P air freight & logistics index to neutral and also removed it from the high-conviction overweight list. The ticker symbols for the stocks in this index are: BLBG: S5AIRF - UPS, FDX, CHRW, EXPD. Anastasios Avgeriou, U.S. Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA U.S. Equity Strategy Weekly Report, “The Good, The Bad And The Ugly” dated March 4, 2019, available at uses.bcaresearch.com. 2https://www.nfib.com/assets/jobs0219hwwd.pdf 3https://ca.spindices.com/documents/additional-material/sp-500-eps-est.xlsx?force_download=true 4 Please see BCA U.S. Equity Strategy Weekly Report, “Signal Vs. Noise” dated December 17, 2018, available at uses.bcaresearch.com. 5 Please see BCA U.S. Equity Strategy Weekly Report, “Recuperating” dated November 5, 2018, available at uses.bcaresearch.com. 6 Please see BCA U.S. Equity Strategy Weekly Report, “Critical Reset“, dated October 29, 2018, available at uses.bcaresearch.com. 7 Please see BCA U.S. Equity Strategy Weekly Report, “The Good, The Bad And The Ugly“, dated March 4, 2019, available at uses.bcaresearch.com. 8 Please see BCA U.S. Equity Strategy Weekly Report, “Critical Reset“, dated October 29, 2018, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps

Neutral We have been offside on the high-conviction overweight call on the S&P air freight & logistics index and the recent FedEx warning suggests that profits will come under pressure for this index for the rest of the year and will trail the SPX. As such, we are trimming exposure to neutral and removing it from the high-conviction overweight list today for a loss of 14%. The chart shows that all the profit drivers we had identified in early December last year have taken a sharp turn for the worse. Energy costs are no longer in deflation as oil prices have jumped from $42/bbl to near $60/bbl. Not only is global growth still decelerating, but also U.S. growth is in a softpatch: the manufacturing shipments-to-inventory ratio is on the verge of contraction, warning that delivery services’ selling prices are in for a turbulent ride (second panel). In addition, definitive news of Amazon becoming a formidable competitor in courier delivery services is structurally negative for the industry. Nevertheless, we refrain from turning outright bearish as air freight stocks are technically oversold and valuations are trading at the steepest discount to the broad market since mid-2002. Bottom Line: Downgrade the S&P air freight & logistics index to neutral and also remove it from the high-conviction overweight list today. The ticker symbols for the stocks in this index are: BLBG: S5AIRF - UPS, FDX, CHRW, EXPD.

Highlights Portfolio Strategy Higher interest rates, with the Federal Reserve tightening monetary policy three more times in the next seven months, will be the dominant theme next year. All four of our high-conviction underweight calls are levered to this theme. The later stages of the U.S. capex upcycle underpin three of our high-conviction overweight calls for 2019. Recent Changes Downgrade the S&P Home Improvement Retail index to underweight today. Trim the S&P Interactive Media & Services index to a below benchmark allocation today. Table 1 Feature Fed policy will dominate markets next year as the dual tightening backdrop – rising fed funds rate and accelerated downsizing of the Fed balance sheet – remains intact. Two weeks ago we raised the question: is the Fed tightening monetary policy too far too fast?1 In more detail, we put the latest monetary tightening cycle in historical perspective and examined trough-to-peak moves in the fed funds rate since the 1950s (Chart 1). Chart 1Too Far Too Fast? A good friend I call “the smartest man in California” correctly pointed out that 500bps of tightening today is not the same as in the 1970s or 1980s. Chart 2 adjusts for that by including the average nominal GDP growth rate during these tightening episodes and adds more color to each era. As a reminder, the latest cycle that commenced in December 2015 is already 25bps above the median, if one uses the Wu-Xia shadow fed funds rate to capture the full quantitative easing effect, and above-average nominal output growth. Chart 2Trough-To-Peak Tightening Cycle Already Above Historical Median Trying to answer the question, we are concerned that as the Fed remains committed to tighten monetary policy three more times by mid-2019, a yield curve inversion looms, especially if the U.S. economy suffers a soft patch in the first half of next year (please refer to our Economic Impulse Indicator analysis in the October 22ndand November 19th Weekly Reports). This would signal at least a pause, if not reversal, in Fed policy. With that in mind, this week we are revealing our high-conviction calls for 2019. Four of our calls are a play on this tightening monetary backdrop that is one of BCA’s themes for next year.2 The later stages of the U.S. capex upcycle underpin three of our high-conviction calls. Table 22018 High-Conviction Calls Recap However, before we highlight our 2019 high-conviction calls in detail, Table 2 tallies our calls from last year. We had a stellar performance in our 2018 high-conviction calls with an average excess return of 11.6% versus the S&P 500. As the year turns the corner, closing out the remaining calls brings down the average relative return to 7.5%, still a very impressive number, with a total of ten hits and only two misses for the year. Anastasios Avgeriou, Vice President U.S. Equity Strategy anastasios@bcaresearch.com Software (Overweight, Capex Theme) Software stocks are our first hold out from last year’s high-conviction overweight list, levered to the capex upcycle theme. Chart 3 shows that relative capital outlays and the share price ratio are joined at the hip. Software upgrades offer the simplest, quickest and most effective capital deployment, especially when productivity gains ground to a halt. Importantly, leading indicators of overall capex remain upbeat and should continue to underpin software profits. Beyond capex, M&A has been fueling software stock prices. It did not take long for the large CA acquisition to get surpassed by RHT and more recently SYMC was also rumored to be in play (Chart 3). Inter-industry M&A activity is reaching fever pitch and this frenzy is bidding up premia to stratospheric levels. The push to the cloud, SaaS and even AI has boosted the appeal of software stocks and brought them to the forefront of potential takeout candidates. These are secular trends and will likely continue to gain steam irrespective of the different stages in the business cycle. As a result, software stocks should remain core tech holdings in equity portfolios. The recovery in the software price deflator (Chart 3), a proxy for industry pricing power, corroborates the upbeat demand backdrop. With regard to financial statements, software stocks have pristine balance sheets with more cash on hand than debt, which sustains the net debt-to-EBITDA ratio in negative territory. Interest coverage is great at 10x and free cash flow generation is expanding smartly. The ticker symbols for the stocks in this index are: BLBG: S5SOFT - MSFT, ORCL, ADBE, CRM, INTU, RHT, ADSK, SNPS, CTXS, ANSS, CDNS, FTNT and SYMC. Chart 3Software Air Freight & Logistics (Overweight, Capex Theme) Air freight & logistics stocks are the second hold out from our high-conviction overweight list, although we added it to list only in late-March. This transportation sub-index laggered is a capex and trade de-escalation play for the first half of 2019. Importantly, energy costs comprise a large chunk of freight services input costs and the recent drubbing in oil markets will boost margins especially on the eve of the busiest season for courier delivery services (top panel, Chart 4). On that front, there are high odds that this holiday sales season will be another record setting one, as wage inflation is underpinning discretionary incomes. Keep in mind that the accelerating domestic manufacturing shipments-to-inventories ratio confirms that demand for hauling services is upbeat. The implication is that rising demand for freight services will buoy industry profits and lift valuations out of their recent funk (Chart 4). Firming industry operating metrics also tell a positive story and suggest that relative share prices will soon take off. Air freight pricing power has been healthy, in expansionary territory and above overall inflation measures. While the U.S./China trade tussle and the appreciating greenback are clear risks to our sanguine S&P air freight & logistics transportation subindex, most of the grim news is already reflected in depressed relative forward profit estimates, bombed out valuations and washed out technicals (Chart 4). The ticker symbols for the stocks in this index are: BLBG: S5AIRF - FDX, UPS, EXPD and CHRW. Chart 4Air Freight & Logistics Defense (Overweight, Capex Theme) We have been overweight the pure-play BCA defense index since late-2015 and there are high odds that this juggernaut that really commenced with the George Walker Bush presidency remains in a secular growth trajectory. Our strategy is to add exposure on any meaningful pullbacks and keep this index as a structural overweight within the GICS1 S&P industrials index. The recent drawdown offers such an opportunity and we are adding this index to the 2019 high-conviction overweight list. The rise of global "multipolarity" - or competition between the world's great nations - and the decline of globalization, along with a global arms race and increased risk of cyber-attacks, have been documented in our "Brothers In Arms" Special Report. These trends all signal that global defense related spending will remain upbeat in the coming decade.3 In the U.S. in particular, where military spending in absolute terms is greater than the rest of the world put together, defense spending and investment have bottomed and will continue to accelerate (Chart 5). In fact, the CBO continues to project that defense outlays will jump further next year. While such a breakneck pace is clearly unsustainable, President Trump is serious about upgrading and updating the U.S. military in order to keep China's geopolitical and military ascendancy in check (as well as to deal with Russia and Iran).4 The upshot is that defense outlays will continue to expand into the 2020s. Such a buoyant demand backdrop is music to the ears of defense contractor CEOs, and represents a boost to defense equity revenue growth prospects. This capital goods sub-industry has extremely high fixed costs and thus any increase in top line growth flows straight to the bottom line. Put differently, defense contractors enjoy high operating leverage. No wonder M&A activity is robust: at least four large deals have been announced in the past year that are underpinning takeout premia. A closer look at operating metrics corroborates that defense goods manufacturers are firing on all cylinders. New orders recently jumped to fresh all-time highs and the industry's shipments-to-inventories ratio is rising, on track to surpass the 2008 peak. Unfilled orders are also running at a high rate, signaling that factories will keep on humming at least for the next few quarters. Importantly, the industry is not standing still and is making significant investments. U.S. defense capex as reported in the financial statements of constituent firms is growing at roughly 20%/annum or twice as fast as overall capex (Chart 5 on page 7). While interest coverage has been modestly deteriorating, it is twice as high as the overall market (Chart 5 on page 7). Impressively, defense ROE is running near 30%, again roughly double the rate of the broad market. The ticker symbols for the stocks in the BCA defense index are: LMT, LLL, NOC, GD and RTN. Chart 5Defense Consumer Discretionary (Underweight, Higher Fed Funds Rate Theme) We recommend investors avoid the consumer discretionary sector that suffers when interest rates rise. Chart 6 depicts this inverse correlation consumer discretionary equities have with interest rates, especially the fed funds rate. Most discretionary equites are levered off of floating rates and thus any increase in the fed funds rates gets reflected immediately in banks' prime lending rate. Also, most consumer debt is floating rate debt and thus tighter monetary conditions, at the margin, dampen consumer debt uptake and, as a knock-on effect, weigh on discretionary consumer outlays. Recently we highlighted that, now that the Fed has been raising rates and allowing bonds to roll off its balance sheet, volatility is making a comeback. Unsurprisingly, the consumer discretionary share price ratio is inversely correlated with the VIX index, signaling that more pain lies ahead for this early cyclical index (VIX shown inverted, Chart 6). Sentiment and technical indicators also point to more downside ahead for this interest-rate sensitive index. Our sector advance/decline line is waning and EPS breadth has plunged. Worrisomely, sell-side analysts are penciling in an extremely optimistic 5-year outlook with EPS growth 23.4%/annum or 1.4 times higher than the overall market. Clearly this is not realistic as it assumes a tripling of EPS in the coming 5 years. Relative EPS estimates have already given way as AMZN commands very little EPS weight, despite its massive market cap weight (30% of the S&P consumer discretionary sector), and suggests that relative share prices will converge lower (Chart 6 on page 9). As a result, the 12-month forward P/E ratio is trading at a 24% premium to the broad market and significantly above the historical mean. Technicals are almost as extended as relative valuations and cyclical momentum has likely peaked, warning that a downdraft in relative share prices looms (Chart 6 on page 9). Chart 6Consumer Discretionary Home Improvement Retail (Underweight, Higher Fed Funds Rate Theme) While the probablity of a housing recession remains low, we are concerned that too much euphoria is already priced in the S&P home improvement retail (HIR) index, and there are high odds that next year HIR will suffer the same fate as homebuilders did this year (Chart 7). Thus, we are downgrading the S&P HIR index to underweight and adding it to the high-conviction underweight list for 2019. Fixed residential investment (FRI) as a percentage of GDP is up 50% from trough to the recent peak, whereas relative HIR performance is up 170% in the same time frame. Our worry is that optimistic sell side analysts' relative profit forecasts will be hard to attain, let alone surpass as FRI is steadily sinking (Chart 7). Worrisomely, our HIR model has plunged on the back of the wholesale liquidation in lumber prices and rising interest rates (Chart 7). Lumber deflation will prove a profit headwind as building supply Big Box retailers make a set margin on wood products. Select industry operating metrics suggest that the easy profits are behind HIR. Not only is our productivity growth proxy (sales per employee) on the verge of deflating, but also an inventory surge has sunk the HIR sales-to-inventories ratio into the contraction zone. Finally, there is rising supply of new and existing homes for sale already on the market, and that puts off remodeling activity at least until this supply glut clears (months' supply shown inverted, Chart 7). The ticker symbols for the stocks in this index are: BLBG: S5HOMI - HD, LOW. Chart 7Home Improvement Retail Short Small Caps/Long Large Caps (Higher Fed Funds Rate Theme) The days in the sun are over for small cap stocks and we are compelled to put the size bias favoring large caps in our high-conviction calls list for 2019. Small caps are severely debt saddled. Sustained small cap balance sheet degradation is worrying, with S&P 600 net debt-to-EBITDA close to 4 compared with less than 2 for the SPX (Chart 8). Such gearing is fraught with danger as the default rate has nowhere to go but higher. Small and medium enterprises (SMEs) have a higher dependency on bank credit as opposed to the bond market access that mega caps enjoy. Most bank credit is floating rate debt and so are lines of credit, and as the Fed remains firm on tightening monetary policy, interest expense costs are skyrocketing for SMEs. In a relative sense this will weigh on net profits. Moreover, small caps are a lot more sensitive to interest rates, and the selloff in the 10-year Treasury note heralds more pain in 2019 (Chart 8). Small caps are high(er) beta stocks and when volatility spikes they underperform large caps. When the Fed ballooned its balance sheet and dropped the fed funds rate to zero it suppressed volatility. Now that the Fed has been decreasing the size of its balance sheet and raising interest rates, this is working in reverse and volatility is making a comeback as we have been highlighting in our research, and will continue to weigh on small caps (VIX shown inverted, middle panel, Chart 8). Another way to showcase small caps' riskier status is the close correlation they have with the relative EM equity share price ratio. When EMs outperform the SPX, small caps follow suit and vice versa. Importantly a wide gap has opened recently and we suspect that it will narrow via small caps following the EM higher beta stocks lower (SPX vs. EM ratio shown inverted, fourth panel, Chart 8 on page 12). Chart 8Small Vs. Large Interactive Media & Services (Underweight, Higher Fed Funds Rate Theme) In our initiation of coverage on the S&P interactive media & services index,5 we highlighted three key risks that offset the revenue & profit growth vigor of this group, comprised almost entirely of Alphabet (Google) and Facebook. These were a renewed regulatory focus, rapid unpredictable changes in tastes & technology and an appreciating U.S. dollar. It is the first of these that has risen most dramatically since that report. Tack on the inverse correlation these growth stocks have with interest rates (top panel, Chart 9) and that is causing us to lower our recommendation to underweight and include this index in the high-conviction underweight list for 2019. Increasing regulatory efforts on technology will be a key theme next year, one we explored this past summer.6 Our conclusion was that both antitrust (particularly in the case of Alphabet) and privacy regulation (particularly in the case of Facebook) added significant risk to these near monopolies; calls for legislating both have dramatically amplified. Tim Cook, Apple’s CEO, recently commented that more regulation for Facebook and Alphabet was inevitable; we agree. While the form such regulation might take remains open to debate (for example, the U.S. could adopt an EU-style General Data Protection Regulation (GDPR)), we fear the associated headline risk (not to mention likely profit headwinds) will impair stock prices in the S&P interactive media & services index. This communication services sub-index is particularly prone to such a risk when it already trades at close to a 40% valuation premium to the broad market (middle panel, Chart 9 on page 14). Adding insult to injury is the PEG ratio that is trading at a 60% premium to the broad market (bottom panel, Chart 9 on page 14). In the face of the Fed’s sustained tightening cycle these extreme growth stocks are vulnerable to massive gravitational pull. The ticker symbols in the stocks in this index are: S5INMS – GOOGL, GOOG, FB, TWTR and TRIP. Chart 9Interactive Media & Services Footnotes 1 Please see BCA U.S. Equity Strategy Report, "Manic Market," dated November 19, 2018, available at uses.bcaresearch.com. 2 Please see BCA The Bank Credit Analyst Report, "OUTLOOK 2019: Late-Cycle Turbulence", dated November 26, 2018, available at bca.bcaresearch.com. 3 Please see BCA U.S. Equity Strategy Special Report, "Brothers In Arms," dated October 31, 2016, available at uses.bcaresearch.com. 4 Please see BCA Geopolitical Strategy Special Report, "A Global Show Of Force?" dated October 10, 2018, available at gps.bcaresearch.com. 5 Please see BCA U.S. Equity Strategy Special Report, "New Lines Of Communication," dated October 1, 2018, available at uses.bcaresearch.com. 6 Please see BCA U.S. Equity Strategy Special Report, "Is The Stock Rally Long In The FAANG?", dated August 1, 2018, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps

Energy costs comprise a large chunk of the input costs for freight service firms. The recent drubbing oil suffered will boost margins for airfreight & logistics companies, especially as it materialized on the eve of the busiest season for courier delivery…

Overweight (High-conviction) Air freight & logistics stocks have been bouncing along the bottom for the better part of the past year and have formed a base that should serve as a launch board higher in the coming months. Energy costs comprise a large chunk of freight services input costs and the recent drubbing in oil markets will boost margins especially on the eve of the busiest season for courier delivery services (top panel). On that front, there are high odds that this holiday sales season will be another record setting one, especially given that corporations have paid out bonuses and shared part of the lowering in corporate taxes and also wage inflation is underpinning discretionary incomes. Keep in mind that the accelerating domestic manufacturing shipments-to-inventories ratio confirms that demand for hauling services is upbeat. The implication is that rising demand for freight services will buoy industry profits and lift stock prices out of their recent funk (middle panel). While the U.S./China trade tussle and the greenback are clear risks to our sanguine S&P air freight & logistics transportation subindex and have been intense headwinds for the sector, they are already reflected in depressed valuations (bottom panel). Bottom Line: We reiterate our high-conviction overweight status in the S&P air freight & logistics index; please see last week’s Weekly Report for more details. The ticker symbols for the stocks in this index are: BLBG: S5AIRF - FDX, UPS, EXPD and CHRW.

Dear Client, Next week on November 26th instead of our regular weekly publication you will receive our flagship publication “The Bank Credit Analyst” with our annual investment outlook. Our regular publication service will resume on December 3rd with our high-conviction trades for 2019. Kind regards, Anastasios Avgeriou Highlights Portfolio Strategy We maintain our sanguine U.S. equity market view for the coming 9-12 months and reiterate our conviction that it is a good time to deploy longer-term oriented capital. The signal from our Economic Impulse Indicator represents a yellow flag and we will continue to monitor the economy for additional soft-patch signals, especially as the Fed remains committed to tighten monetary policy three more times by mid-2019. Firming pricing power on the back of recovering demand coupled with input cost deflation suggest that an earnings led recovery in the S&P airlines index is in order. Take profits and boost to an overweight stance today. Burgeoning domestic demand for freight services, healthy industry operating metrics, the recent margin boost owing to the crude oil price collapse along with compelling valuations and technicals, suggest that the path of least resistance is higher for the S&P air freight & logistics group. Recent Changes Book gains in the S&P Airlines index of 18% since inception and lift from below benchmark to overweight today. Table 1 FEATURE The SPX was rudderless last week, as the tug-of-war between bears and bulls has yet to be decided. Equities have been experiencing mini-aftershocks following October's seismic move because the Fed has injected some volatility back into the markets via raising interest rates and allowing bonds to roll off its balance sheet at an accelerating pace. While the Fed stayed pat in November, it will most definitely tighten monetary policy next month for the ninth time this cycle. Fed policy is at the epicenter of recent S&P 500 oscillations, which raises the question: is the Fed tightening monetary policy too far too fast to cause equity market consternation? To put the latest monetary tightening cycle in perspective, we examined trough-to-peak moves in the fed funds rate since the 1950s. Chart 1 shows the results of our analysis. During the past ten Fed tightening cycles, the median trough-to-peak delta in the fed funds rate heading into recession has been 495bps. The latest cycle that commenced in December 2015 is already 25bps above the median, if one uses the Wu-Xia shadow fed funds rate to capture the full quantitative easing effect (Chart 2). Were the Fed to hike three more times by the first half of 2019, as our fixed income strategists expect, this will push the current cycle 100bps above the historical median. Chart 1Too Far Too Fast? Chart 2Trough-To-Peak Tightening Cycle Already Above Historical Median While almost everyone raves about the stellar U.S. economic performance squarely focused on levels of different economic indicators (Chart 3), drilling beneath the surface reveals that small cracks are forming, as we first highlighted in the October 22nd Weekly Report when we introduced our Economic Impulse Indicator (EII).1 The EII is a second derivate equally-weighted composite of six indicators of the U.S. economy, highlighting that peak economy was likely hit this year in Q2, when nominal GDP grew 7.6% on a quarter-over-quarter annualized growth rate basis. Chart 3Do Not Focus On Levels Alone... Chart 4 shows that 5 out of the 6 indicators included in the EII are losing steam, 4 out of 6 are in outright contraction, and only capex is showing modest signs of life. While this backdrop in isolation does not portend recession, were the Fed to go ahead with three additional hikes by mid-year 2019 that would push the fed funds rate to a range of 2.75%-3% and a possible negative Q2/2019 GDP print could then easily invert the yield curve, ticking the box in one of our three recession indicators we track.2 Chart 4...Impulses Tell A Different Story The latest Fed Senior Loan Officer survey released last week also struck a nerve. While bankers are willing extenders of credit throughout most loan categories, demand for loans is declining across the board (Chart 5A); only other consumer (likely student) loans are in high demand, and subprime residential loans are also threatening to break above the zero line.3 Nevertheless, before getting too bearish, a bond valuation examination is in order. BCA's 10-year bond valuation index has been an excellent predictor of cycle ends dating back to the 1960s. It has accurately forecast 6 out of the last 7 recessions missing only the 1974 iteration. When this valuation metric swings to extremely undervalued territory - defined as at least one standard deviation above the historical mean - it signals that a recession is approaching. Why? Typically a selloff in the bond market is associated with a fed tightening cycle and such steep monetary tightening slams the breaks on the economy via the slowing housing market and the dent in consumer spending power. True, we are closing in on this level, but we are not there yet (Chart 5B). Chart 5ALoan Demand In Freefall Chart 5BWatch Bond Valuations Finally, we bought the proverbial dip on October 26th as we did not (and still do not) foresee recession in the coming 9-12 months, underscoring that likely the trough is in place.4 On that front the Minneapolis Fed's implied probability of a 20%+ correction remains tame near the 10% probability mark, corroborating our sense that the worst is behind the equity market, at least for now (Chart 6). Chart 6Risk Of A Bear Market Is Low Netting it all out, we maintain our sanguine equity market view for the coming 9-12 months and reiterate our conviction that it is a good time to deploy longer-term oriented capital. The signal from our EII represents a yellow flag and we will continue to monitor the economy for additional soft-patch signals especially as the Fed remains committed to tighten monetary policy three more times by mid-2019. This week we crystalize gains in the smallest transportation sub-index we cover and boost exposure to overweight, and reiterate our high-conviction overweight stance on a large transportation sub-index. Airlines: Up In The Air Within transports we have been advocating a barbell portfolio preferring air freight & logistics (see below for an update) to airlines (as a reminder we recently downgraded rails to neutral5). The recent carnage in oil markets has breathed a huge sigh of relief into the S&P airlines index (most of which do not hedge fuels costs) as the collapse in WTI crude oil prices has also taken down kerosene prices. Chart 7 shows that input cost relief will be a key driver of a rebound in relative airline profits in the coming months. Thus, we are compelled to trigger our upgrade alert and cement gains of 18% in our underweight and lift exposure to overweight in the niche S&P airlines index. Chart 7Energy Price Plunge Is Bullish For Airline EPS Not only will airlines get a boost from falling jet fuel prices, but also demand for travel remains upbeat. Consumer confidence is sky high and consumer spending is running at a healthy clip, at a time when job certainty is high and wage inflation is making a comeback (Chart 8). Chart 8Air Travel Demand... In fact, a larger proportion of the consumer's wallet is used for air travel, a trend that has been recently gaining steam according to national accounts. Airline load factors are pushing cyclical highs and passenger revenue per available seat mile is also gaining momentum, corroborating the U.S. government consumption expenditure data (Chart 9). Chart 9...Is Upbeat... As a result, airlines have been successful at raising selling prices and will soon exit the deflationary zone. International airfares are also in positive territory. Taken together, robust demand and higher selling prices along with declining fuel costs are a harbinger of rising margins and profits (Chart 10). Chart 10Firming Ticket Prices Is A Boon To Margins This is not yet reflected in depressed relative forward sales and profit growth estimates. Net earnings revisions have also recovered to the zero line and there is scope for additional positive EPS revisions, especially if jet fuel prices stay tamed and travel demand remains healthy. The implication is that relative share price momentum can lift off further (Chart 11). Chart 11Low Hurdle Finally, valuations are perched deeply in the undervalued zone while technicals have only recently returned to a neutral setting (Chart 12). Chart 12Unloved and Under-owned Adding it up, it no longer pays to be bearish airlines. Firming pricing power on the back of recovering demand coupled with input cost deflation suggest that an earnings led recovery in the S&P airlines index is in order. Bottom Line: Take profits in the S&P airlines index of 18% since inception and lift exposure to an above benchmark allocation. The ticker symbols for the stocks in this index are: BLBG: S5AIRL - DAL, LUV, UAL, AAL and ALK. Air Freight & Logistics: We Have Liftoff Air freight & logistics stocks have been bouncing along the bottom for the better part of the past year and have formed a base that should serve as a launch board higher in the coming months. Firming industry operating metrics tell a positive story and suggest that relative share prices will soon take off. Air freight pricing power has been healthy, in expansionary territory and above overall inflation measures, at a time when industry executives have been showing labor restraint, with employment growth decelerating steadily over the past two years (Chart 13). This is a conducive backdrop for air freight profit margins and sell-side analysts have taken notice, penciling in higher margins in the coming 12 months. Chart 13Enticing Margin Prospects Importantly, energy costs comprise a large chunk of freight services input costs and the recent drubbing in oil markets will boost margins especially on the eve of the busiest season for courier delivery services (top panel, Chart 14). Chart 14Holiday Selling Season Beneficiary On that front, there are high odds that this holiday sales season will be another record setting one, especially given that corporations have paid out bonuses and shared part of the lowering in corporate taxes and also wage inflation is underpinning discretionary incomes. Keep in mind that the accelerating domestic manufacturing shipments-to-inventories ratio confirms that demand for hauling services is upbeat. The implication is that rising demand for freight services will buoy industry profits and lift valuations out of their recent funk (middle & bottom panels, Chart 14). With regard to the global macro and trade backdrop, while global revenue ton miles and G3 capital goods orders remain near cyclical highs (Chart 15), were Trump's trade rhetoric to re-escalate then global exports would give way. Already international and U.S. export expectations are on the verge of contracting - according to the IFO World Economic Survey and ISM manufacturing survey, respectively. Tack on the appreciating U.S. currency and the clouds darken further (bottom panel, Chart 15). The U.S./China trade tussle and the greenback are clear risks to our sanguine S&P air freight & logistics transportation subindex. Chart 15Greenback And Decelerating Global Growth Are Key Risks... Nevertheless, most of the grim news is already reflected in depressed relative forward profit estimates, bombed out valuations and washed out technicals. In sum, firming domestic demand for freight services, healthy industry operating metrics, the recent margin boost owing to the crude oil price collapse along with compelling valuations and technicals suggest that the path of least resistance is higher for the S&P air freight & logistics group (Chart 16). Chart 16...But Already Reflected In Depressed Valuations And Washed Out Technicals Bottom Line: We reiterate our high-conviction overweight status in the S&P air freight & logistics index. The ticker symbols for the stocks in this index are: BLBG: S5AIRF - FDX, UPS, EXPD and CHRW. Anastasios Avgeriou, Vice President U.S. Equity Strategy anastasios@bcaresearch.com 1 Please see BCA U.S. Equity Strategy Report, "Icarus Moment?" dated October 22, 2018, available at uses.bcaresearch.com. 2 Ibid. 3 https://www.federalreserve.gov/data/documents/sloos-201810-charts.pdf 4 Please see BCA U.S. Equity Strategy Insight Report, “Time To Bargain Hunt” dated October 26, 2018, available at uses.bcaresearch.com. 5 Please see BCA U.S. Equity Strategy Report, "Critical Reset" dated October 29, 2018, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps