Asia

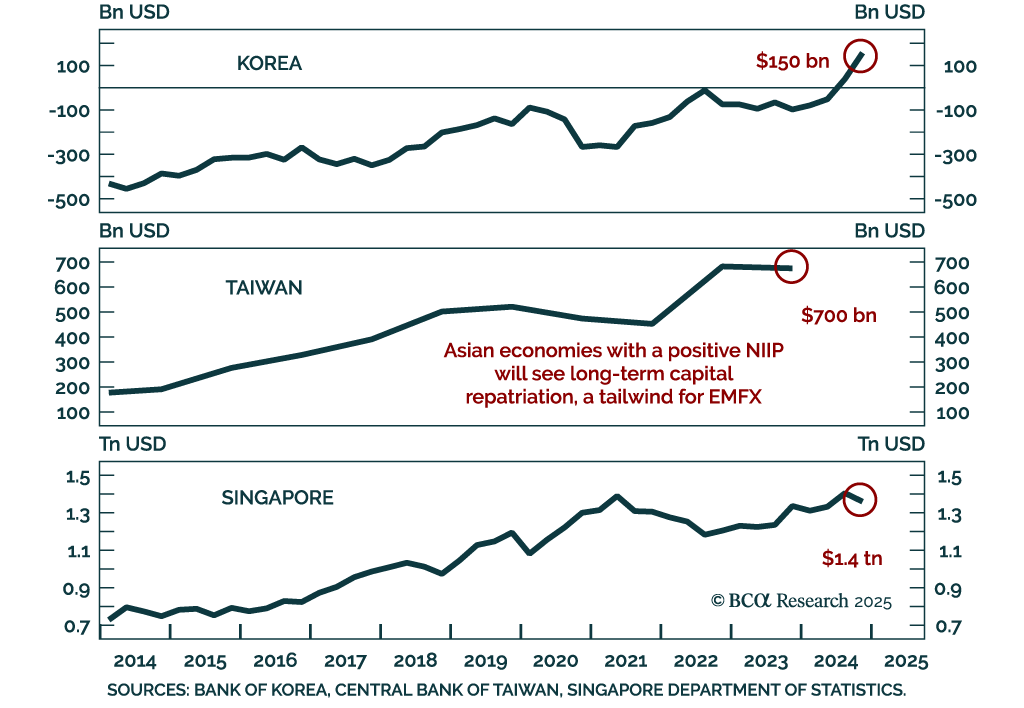

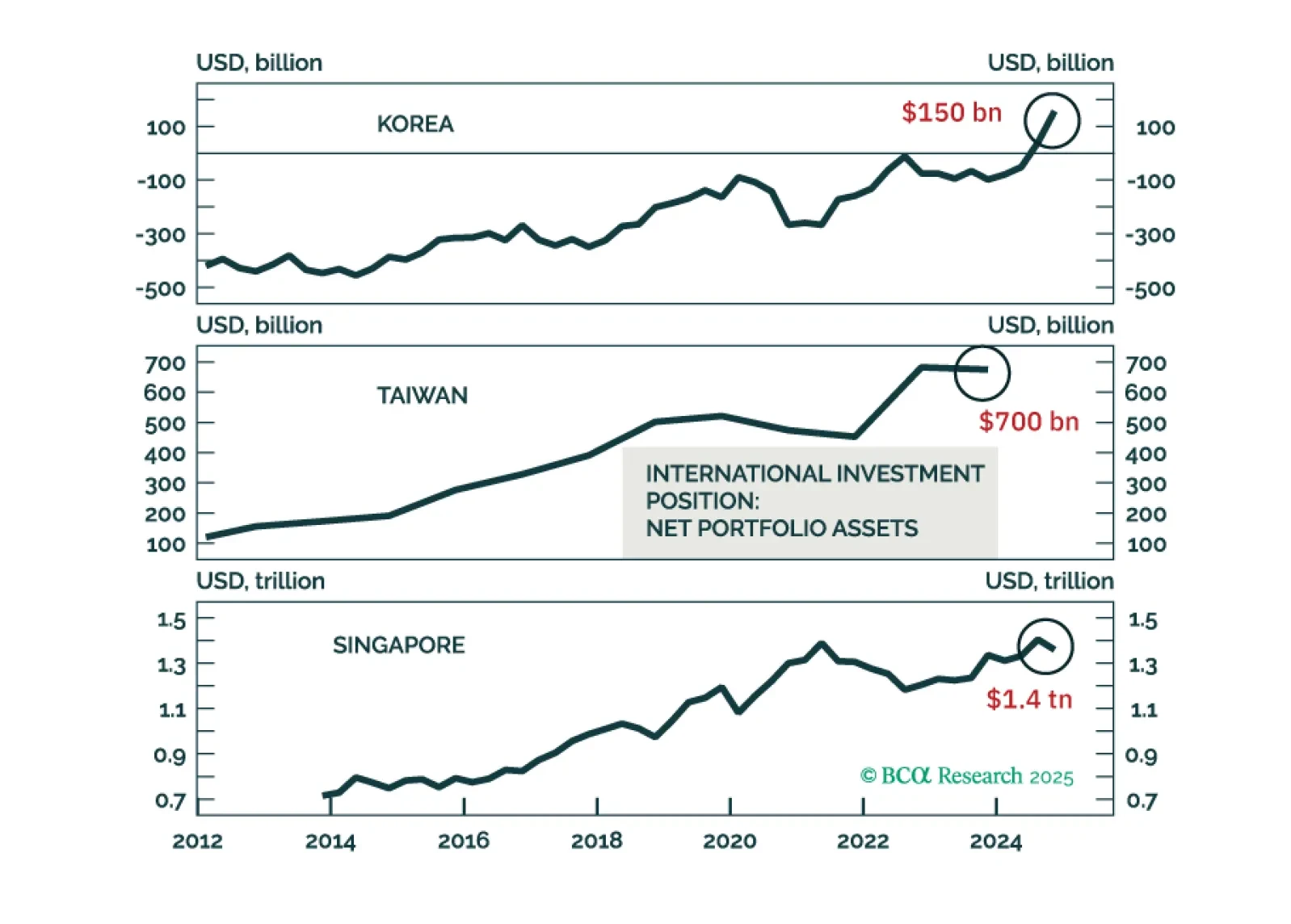

Taiwan, Singapore, and Korea's currencies might appreciate versus the USD, driven by capital repatriation from domestic private investors away from the US. This thesis is less pertinent to India, Indonesia, and the Philippines because they have large net foreign portfolio liabilities. Malaysia and Thailand fall in the middle, while China is an exception. Investors should play intensifying deflationary pressures in Asia by betting on lower interest rates in the region.

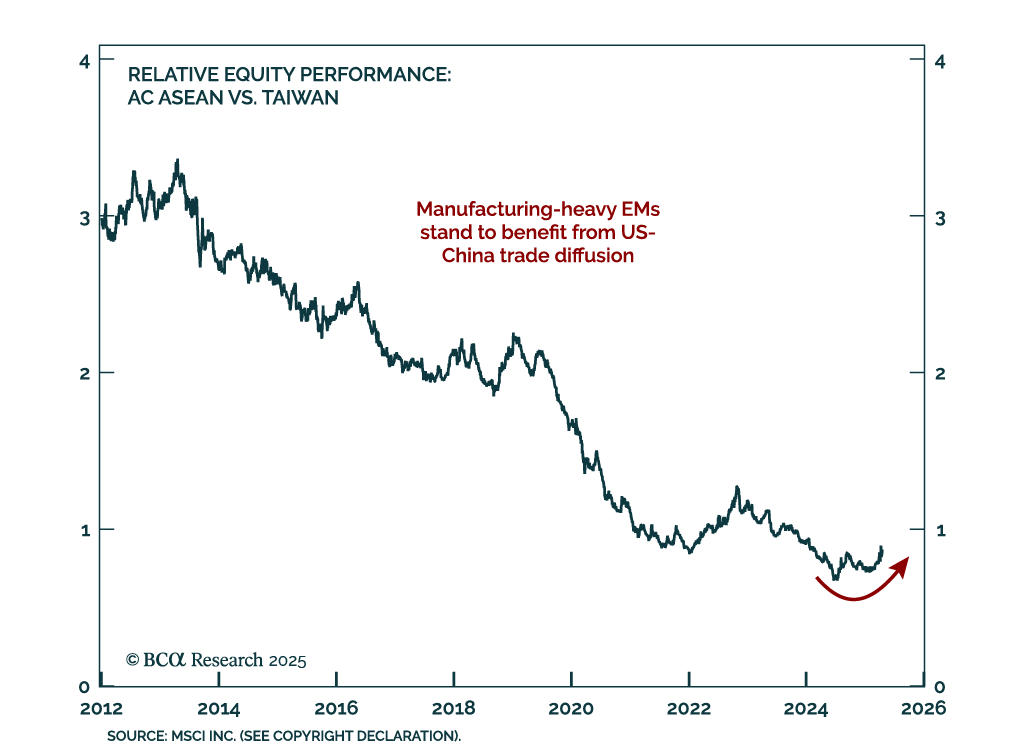

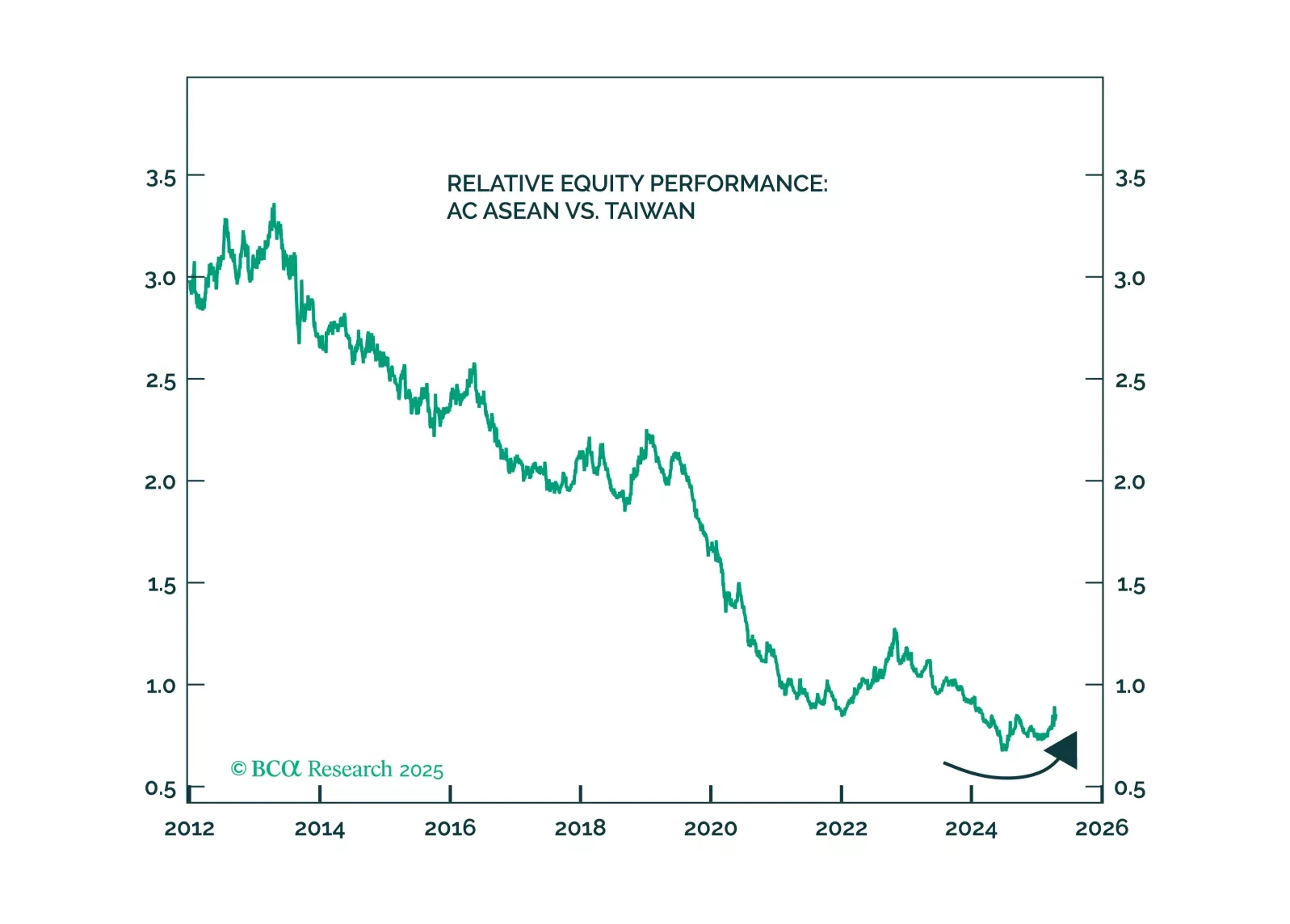

Upgrade the odds of a full-scale war in the Taiwan Strait from 5% to 10%. Rapid escalation of US-China economic war raises the probability of tensions spilling into the military-strategic domain. Investors should buy insurance against this tail risk while it is cheap. Meanwhile, use this year’s trade shock and equity volatility to increase allocation to EM manufacturing states.

Europe’s near-term outlook remains clouded by uncertainty, even after the tariff reprieve. Our latest update breaks down why the risks to growth, profits, and financial conditions are still skewed to the downside — with Sweden standing out as a key bellwether.