Asia

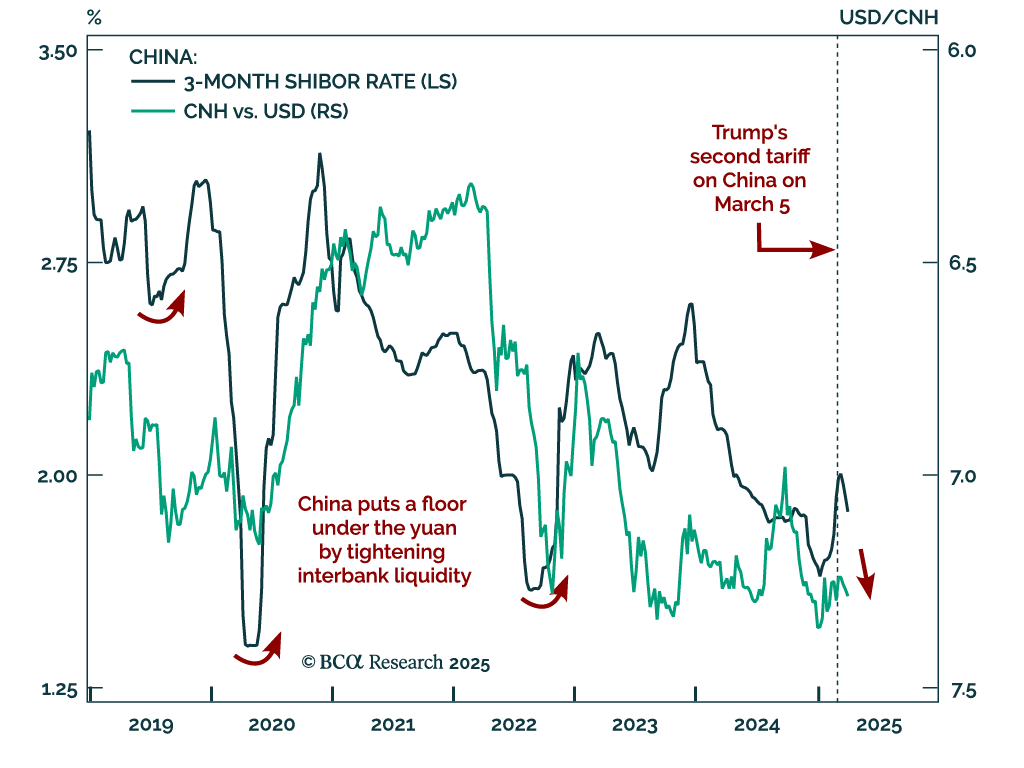

This week, we look at the sustainability of the HKD peg as the next whale to move markets, given what is happening to tariffs. After careful analysis, our bias is that it is here to stay. With the DXY dipping below 100, we are likely to see a rebound, which is actually bad news for the Hong Kong region of China, since it will tighten financial conditions. We have no new short-term trades, but if the peg broke, you want to be short HKD/JPY.

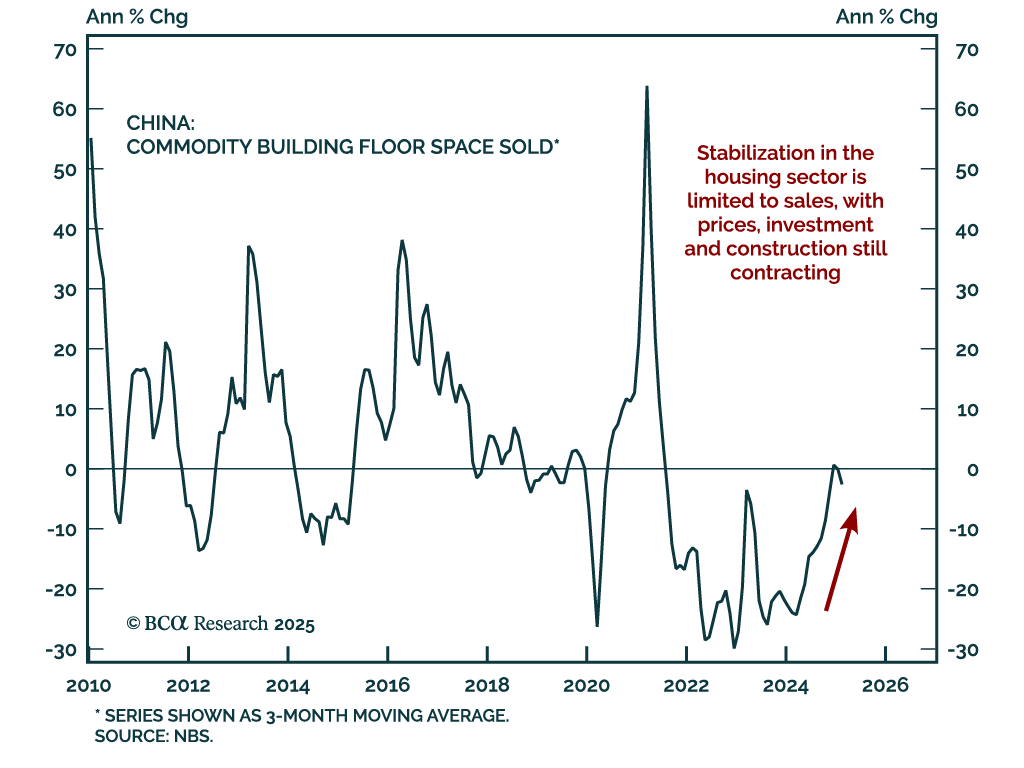

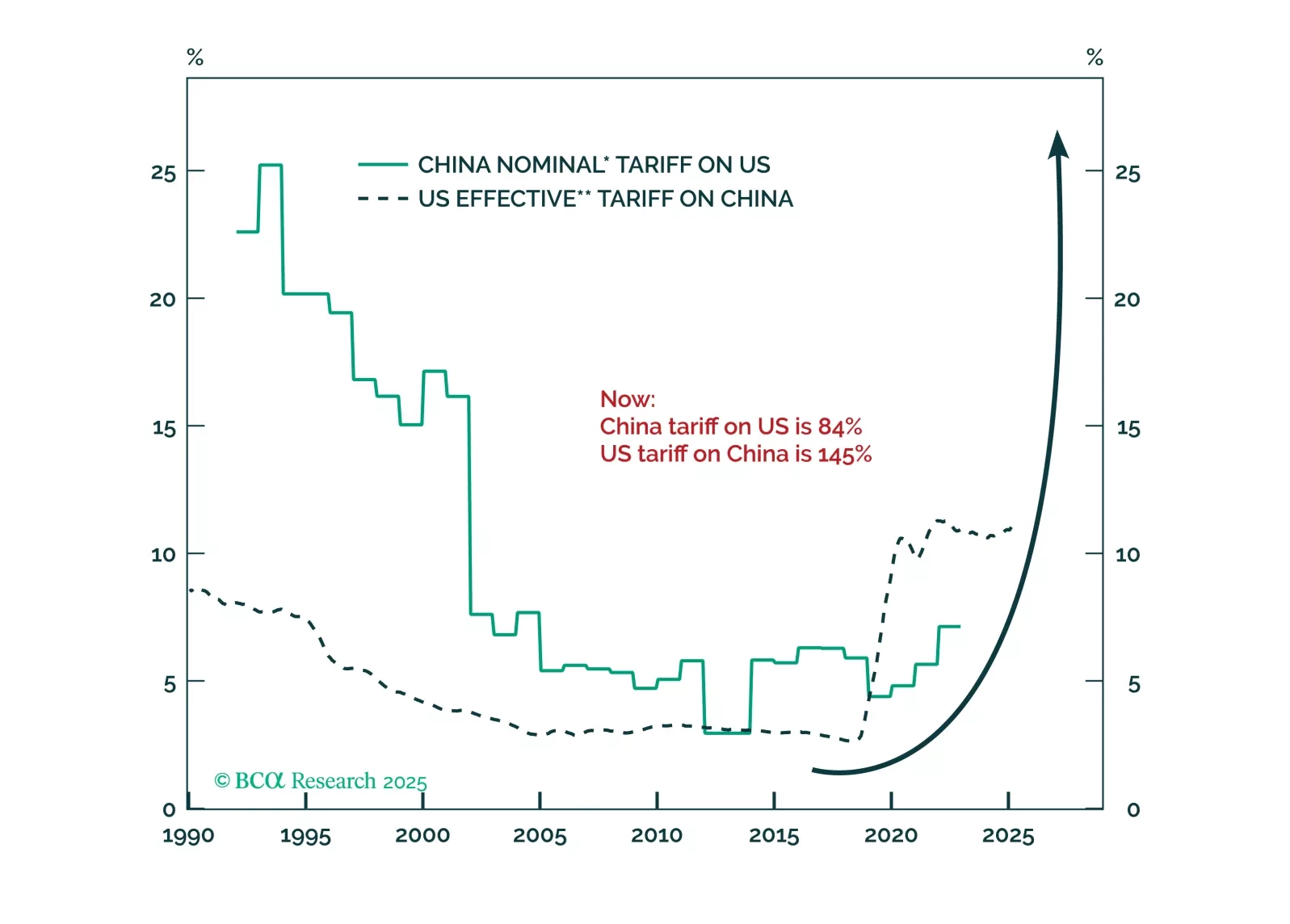

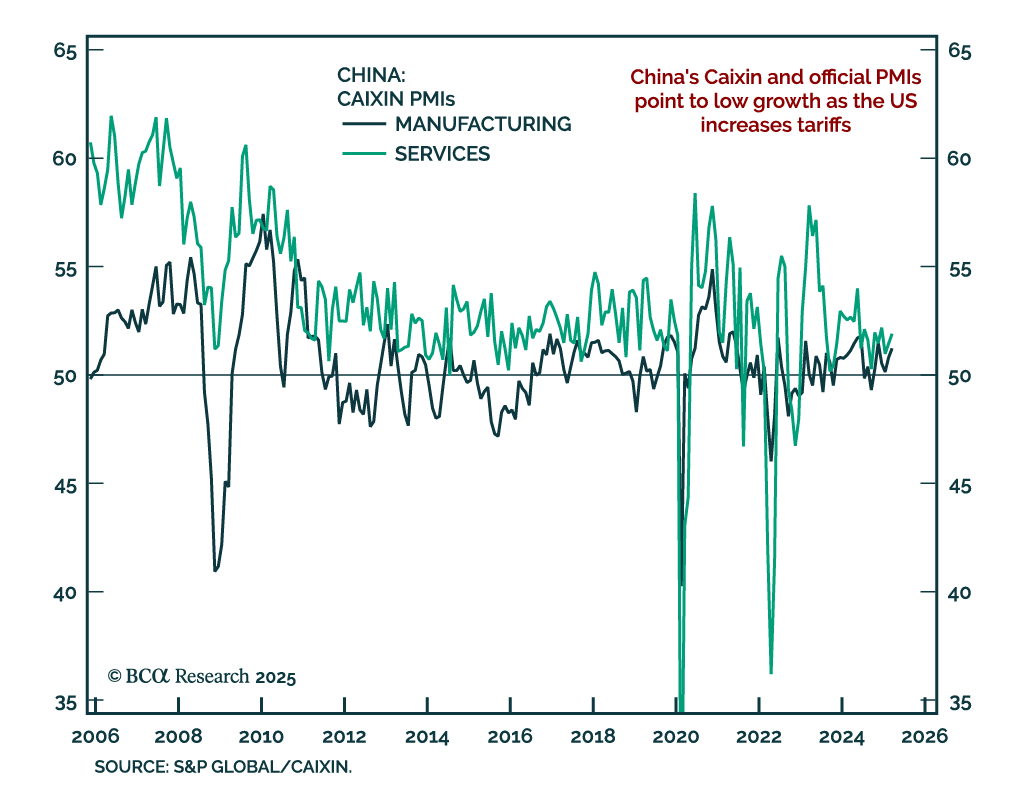

China’s aggressive retaliation against U.S. tariffs will enable President Trump to shift from punishing allies and redirect the trade war toward China. If Beijing does not react to the latest tariffs by doubling its fiscal stimulus, it indicates they are planning something different, as China will encounter economic destabilization. The likelihood of a hybrid military pressure on Taiwan will rise.

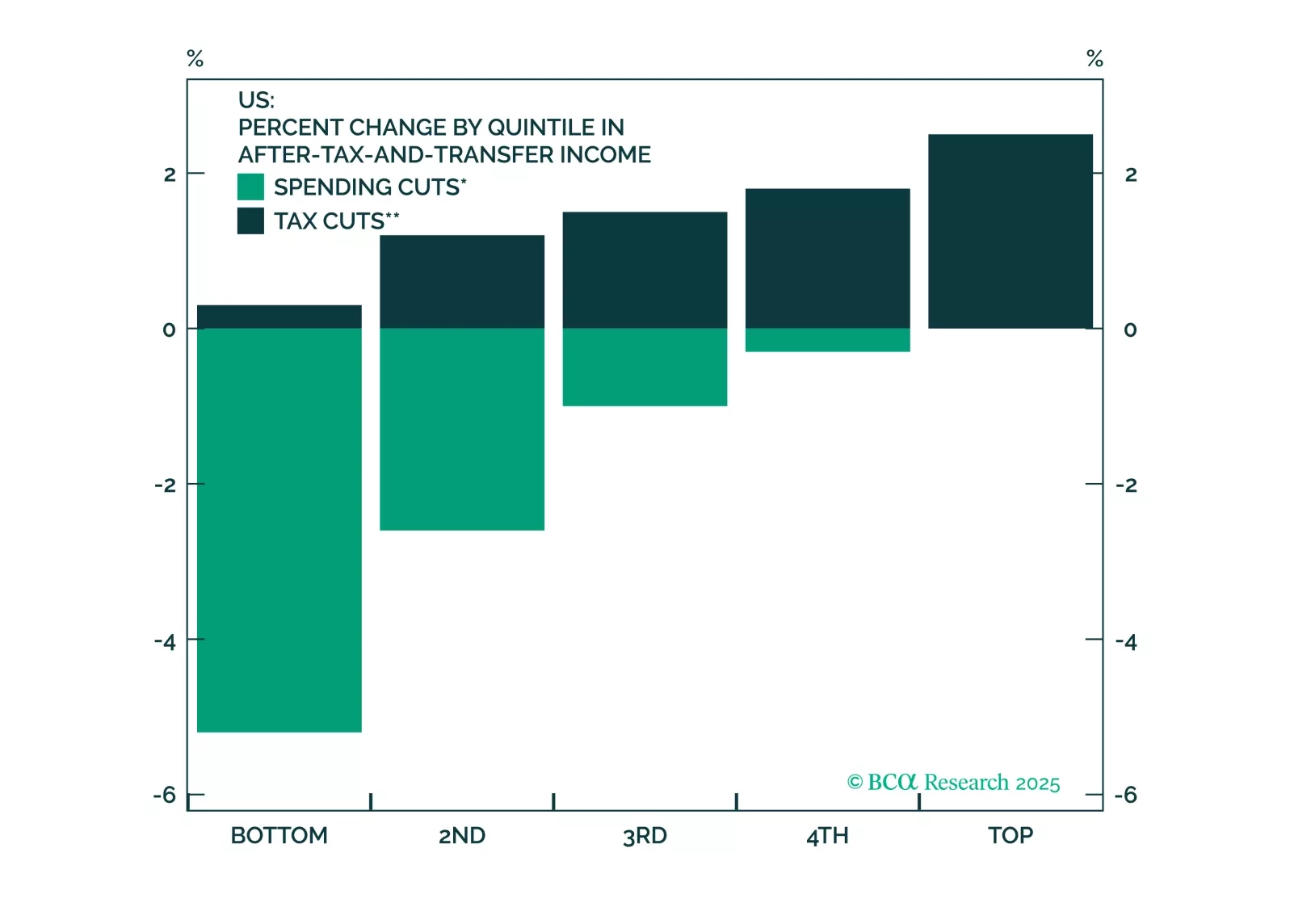

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.