Asia

The Caixin services and composite PMIs were broadly unchanged in April. The services PMI decreased from 52.7 to 52.5, in line with expectations, while the composite PMI increased from 52.7 to 52.8. Details underscored positive dynamics. New business growth…

Chinese investable stocks have rallied on a combination of investors’ hopes for stimulus, revival in the global manufacturing cycle and cheap valuations. The MSCI China index and the Hang Seng have both gained close to 15% since mid-April. However, our…

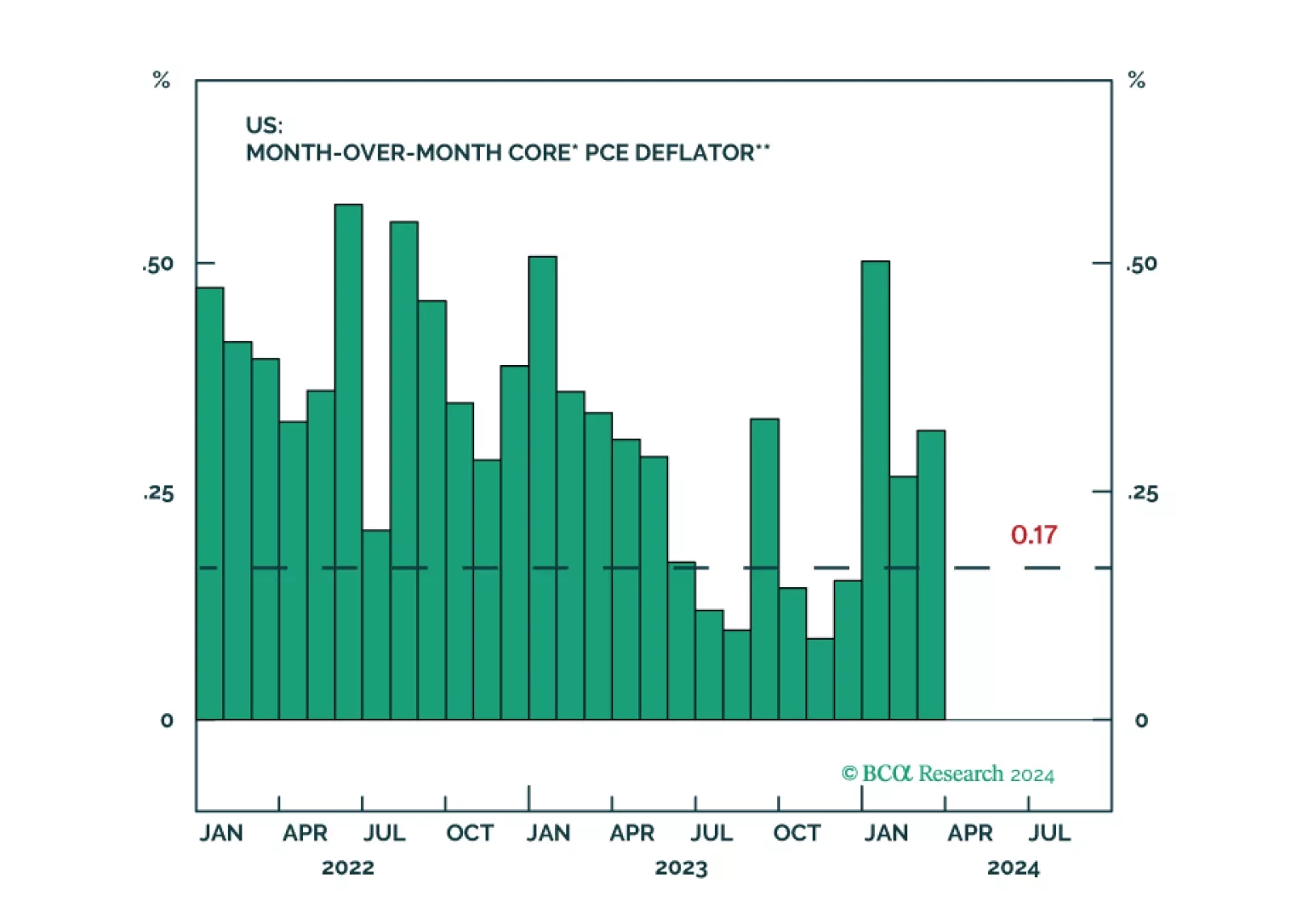

Central banks are in a dilemma whether to prioritize supporting growth or bringing inflation back to target. This is unlikely to end well. Investors should be defensively positioned.

The Chinese NBS non-manufacturing PMI came in at 51.2, below the previous month’s number of 53 and below expectations of 52.2. Moreover, the NBS manufacturing PMI also decreased to (a better-than-expected) 50.4 in April from 50.8 in March. Meanwhile, the…

Chinese industrial profit growth slowed in the first three months of the year to 4.3% YTD y/y, from 10.2% y/y in January and February. The March slowdown is meaningful since industrial profits outright contracted by 3.5% relative to March 2023. Weak…

2023 was an awful year for Chinese equities. Though last year, the MSCI China Investable index declined by over 10% even as global equities rallied by over 20%. The pain extended into January of this year, with Chinese stocks underperforming the global…

China’s economy is cruising at a very low altitude. The odds are that China’s equity rebound is running out of time. The RMB will continue to depreciate versus the US dollar in the coming months, albeit the pace may be modest.

Export dynamics of small open economies are a bellwether for global growth. The latest Taiwanese and Korean export numbers are consistent with a revival in global trade. Taiwanese export orders grew by 1.2% y/y in March following a 10.4% y/y contraction in…

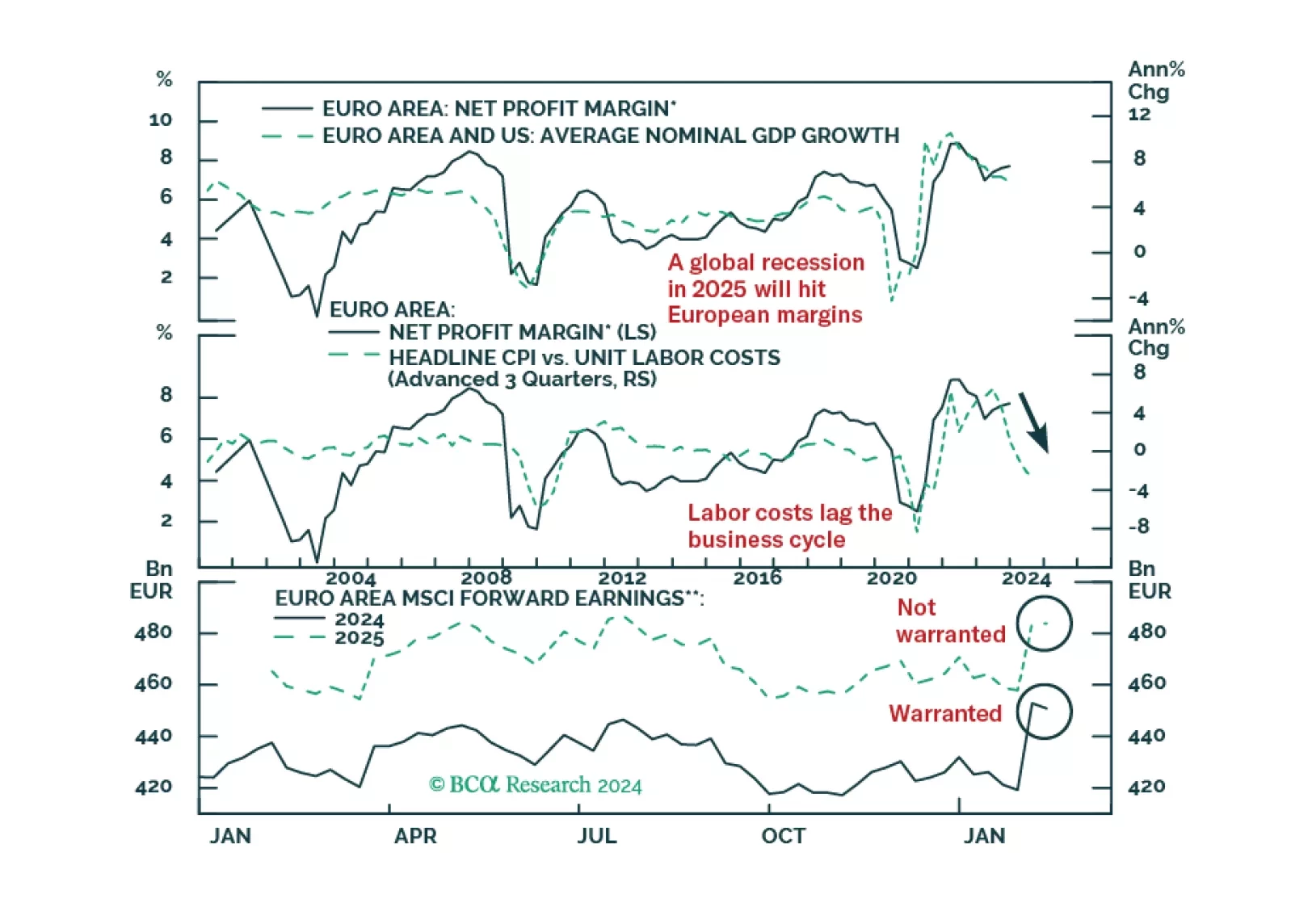

European profits margins are elevated. Will a mild recession be enough to bring them down?

The Asian currency index posted the largest negative post-GFC abnormal returns (z-score) among the major financial markets we tracked in March. Indeed, Asian currencies have been on a general downtrend since early 2023, and more recently fell 3.2% in absolute…