Asia

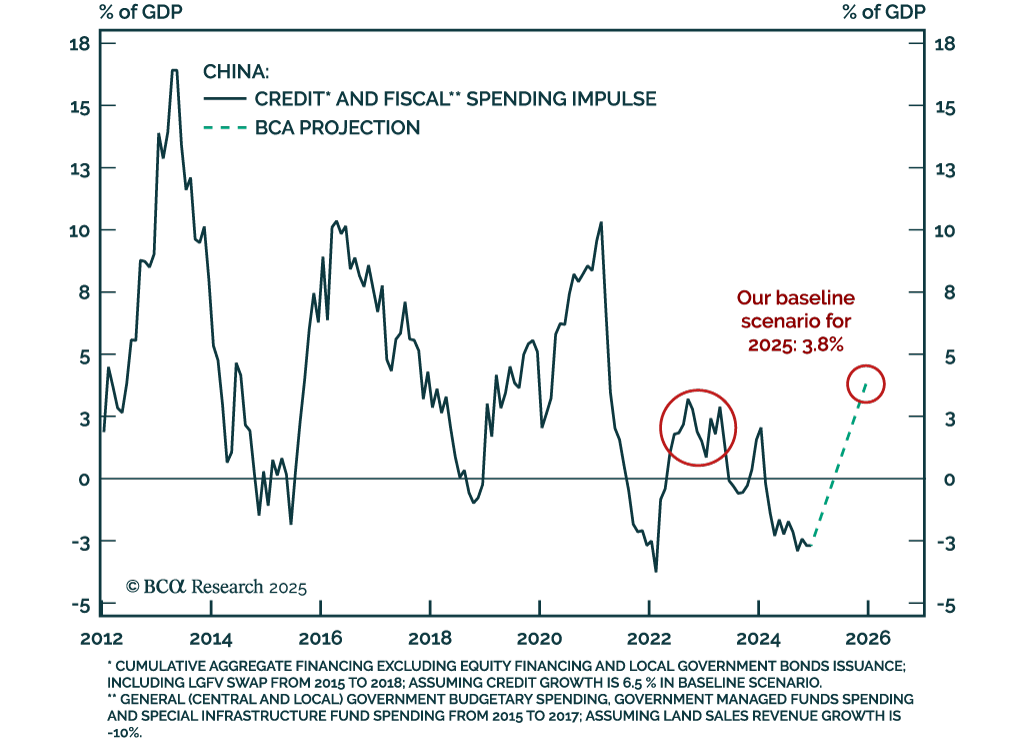

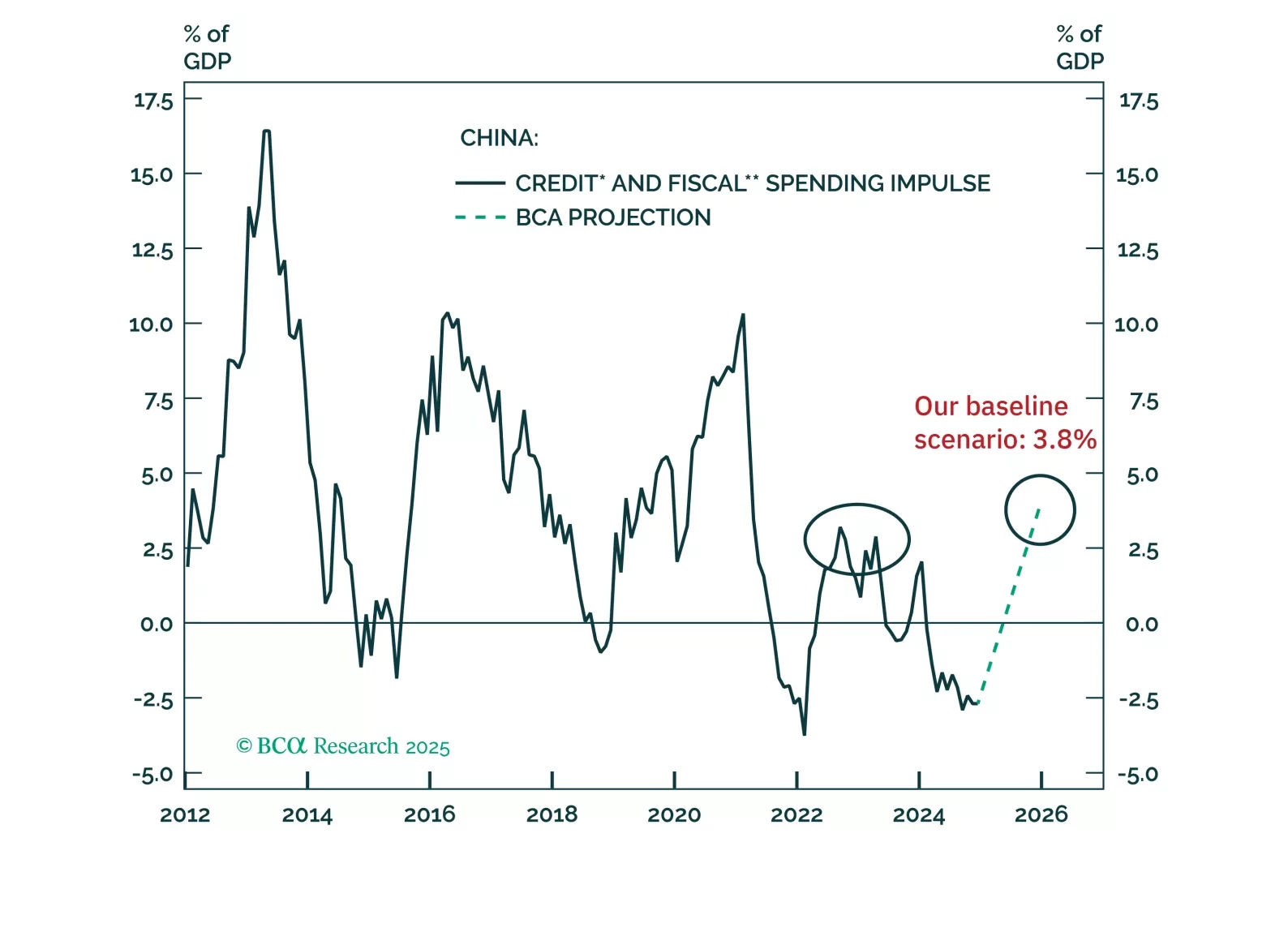

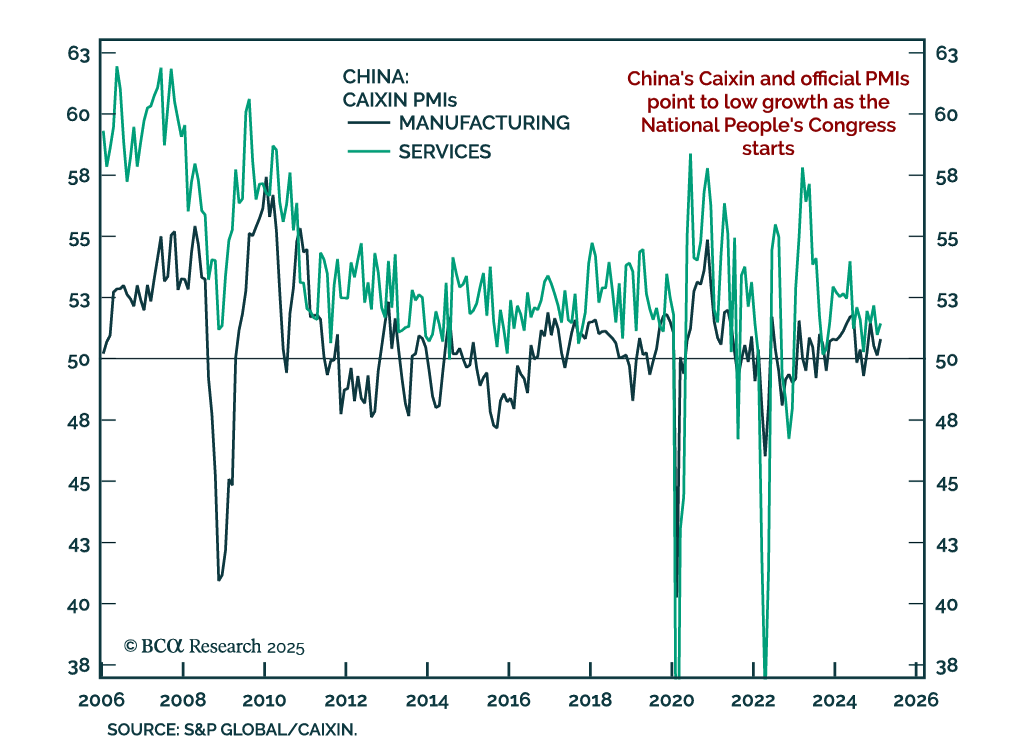

The fiscal stimulus announced at this year’s National People’s Congress is only slightly larger than last year’s. Notably, the details of the measures suggest that it will be challenging for fiscal stimulus to effectively counterbalance the country’s economic difficulties this year.

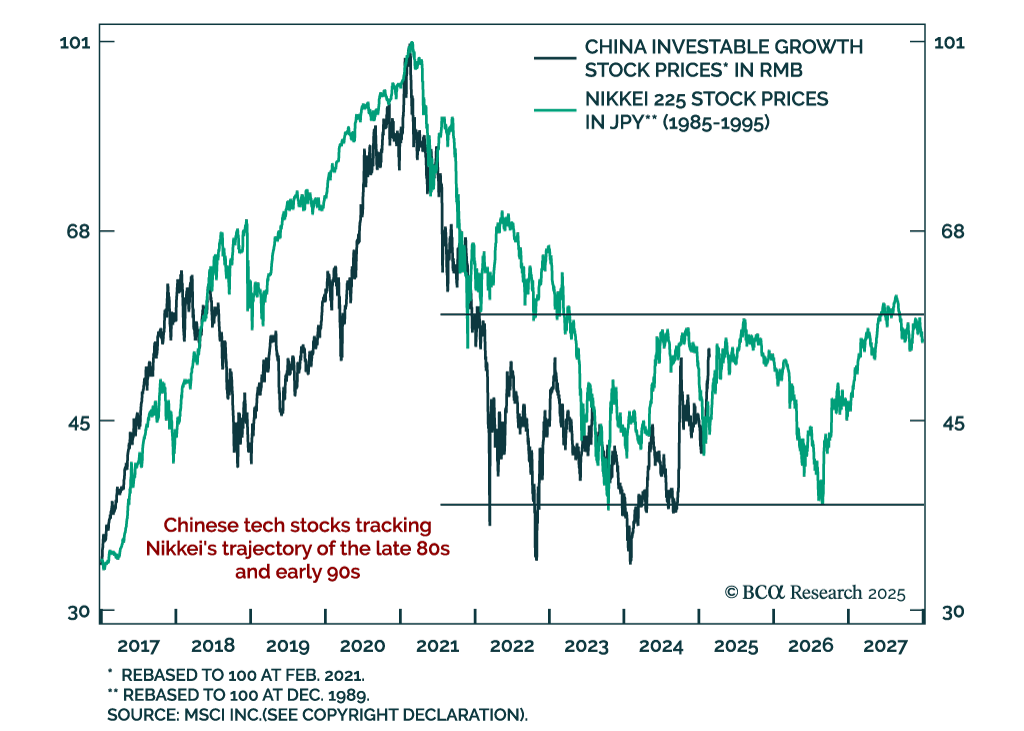

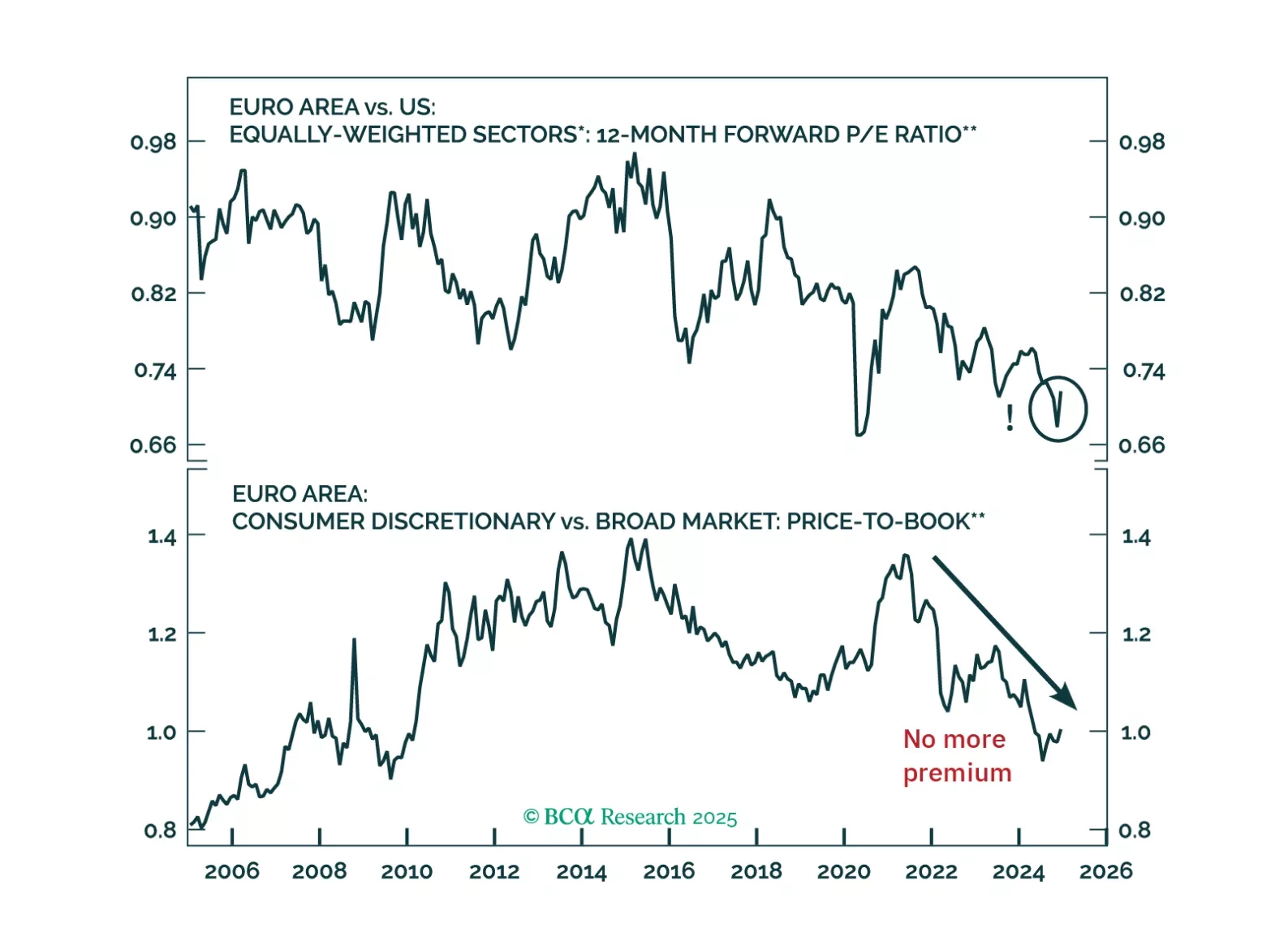

Markets and forecasters anticipate a “Golden Age” for Trump’s America, with US growth expectations soaring while the rest of the world lags. However, this extreme optimism means that there is a lot of room for disappointment. Cooling income growth, weak housing and less deficit spending than expected will result in US growth underperforming expectations. Maintain a modest underweight to equities and modest overweight to fixed income. US markets have become more expensive relative to the rest of the world even as quality differentials have stabilized. Prepare to downgrade US equities to underweight and to upgrade Euro Area and China to overweight. We will wait to pull the trigger until we have more clarity on trade policy and when the dollar's momentum turns negative.

Global risk assets are engulfed in a wave of euphoria, which is pulling Europe higher along the way. However, risks still abound. How should investors adjust their allocation to Europe under these highly uncertain conditions?