Asia

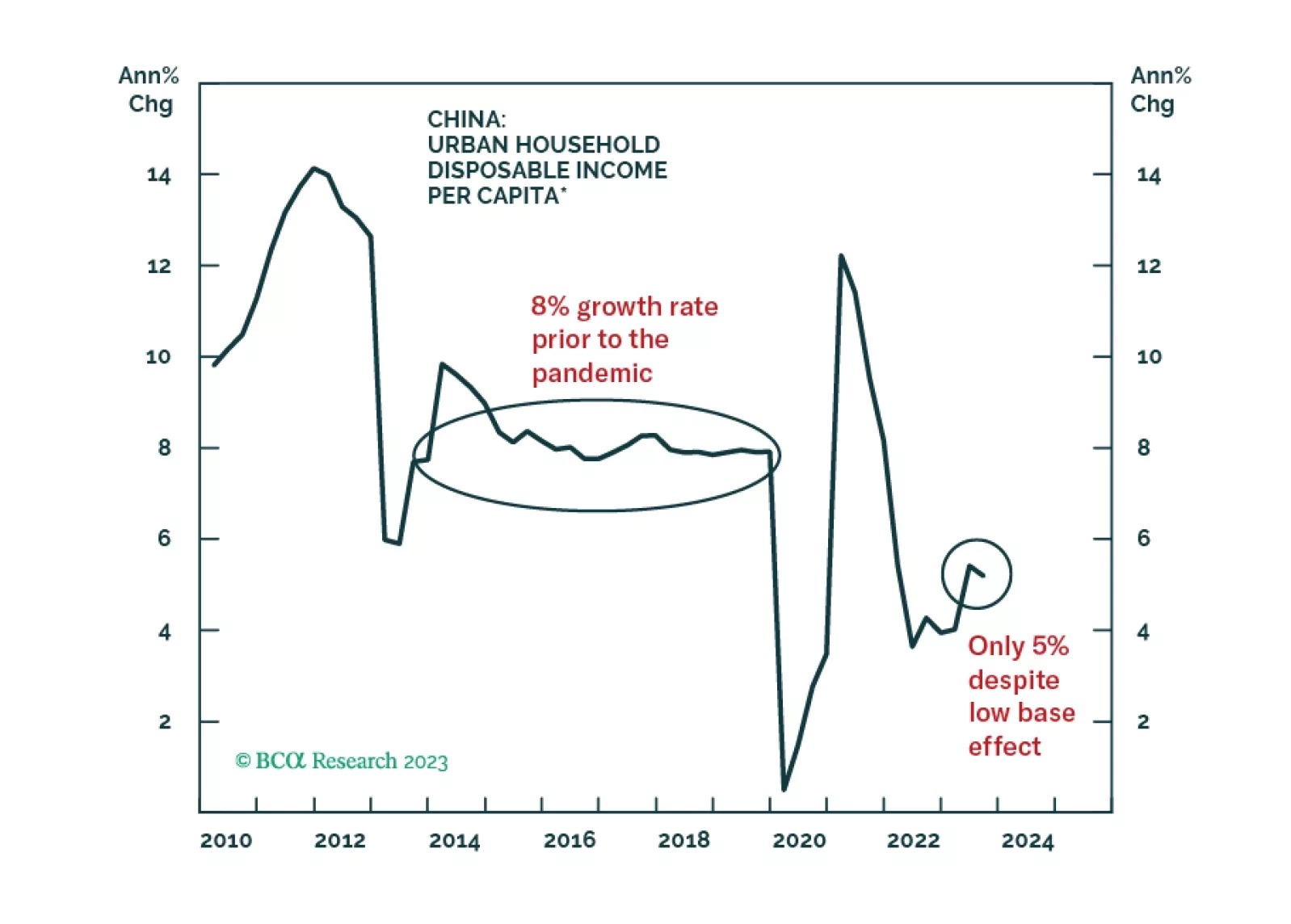

The overarching macro theme for China in 2024 will be deflation and its impact on the economy, macro policies, and financial markets. Widespread deflation, in combination with high debt levels and falling real estate prices, has unleashed debt deflation and balance sheet recession dynamics. The latter are rendering monetary policy inefficient.

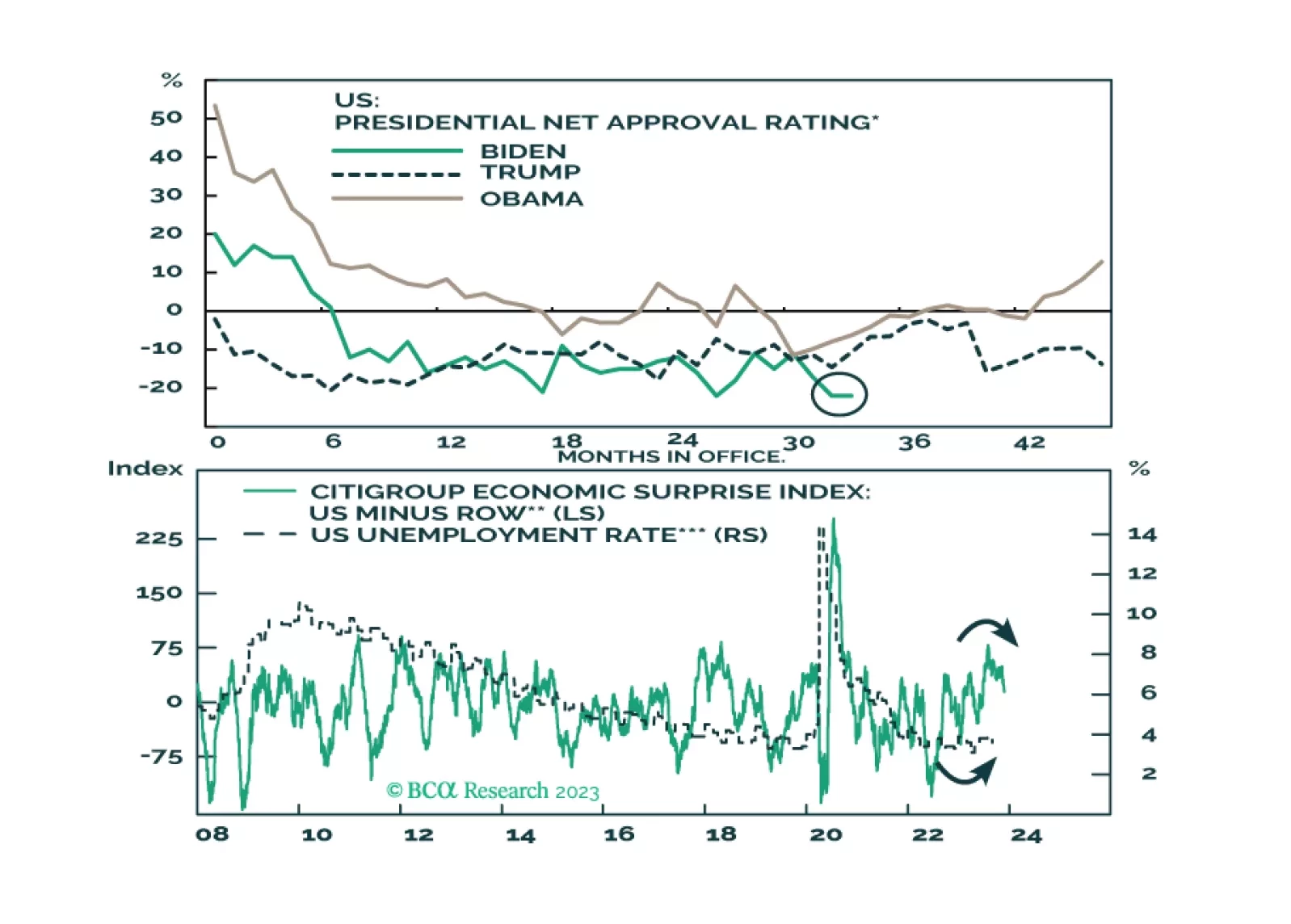

Global instability will continue in 2024 – whatever happens afterward. Slowing economies will exacerbate already high geopolitical risk and policy uncertainty stemming from the US election and foreign challenges to US leadership. Overweight government bonds, defensive sectors, the Americas versus other regions, aerospace/defense stocks, and cyber-security stocks.

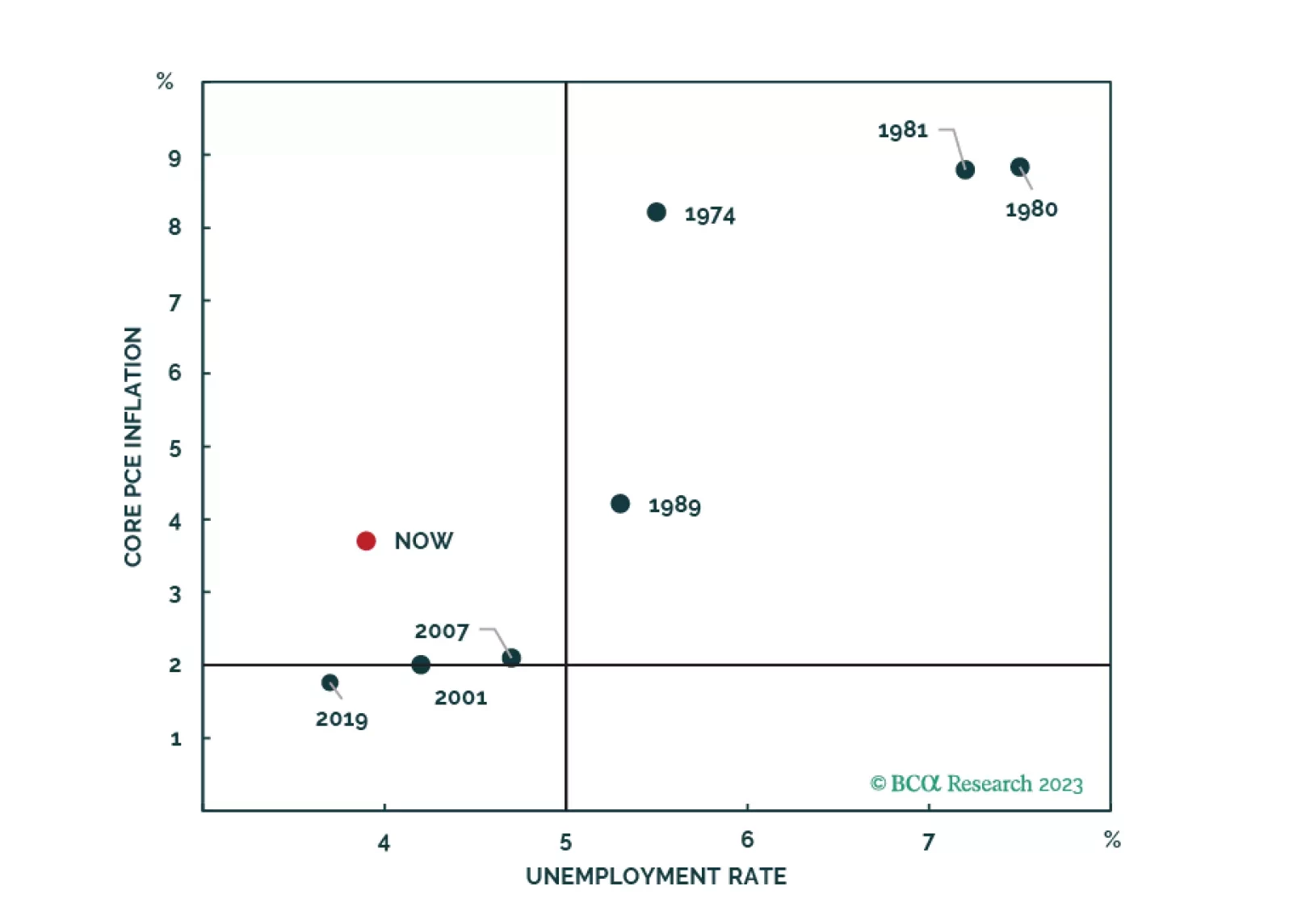

Inflation won’t fall fast enough for the Fed to cut rates preemptively before recession arrives. The risk/rewards balance is unfavorable for risk assets. Stay overweight bonds versus equities.

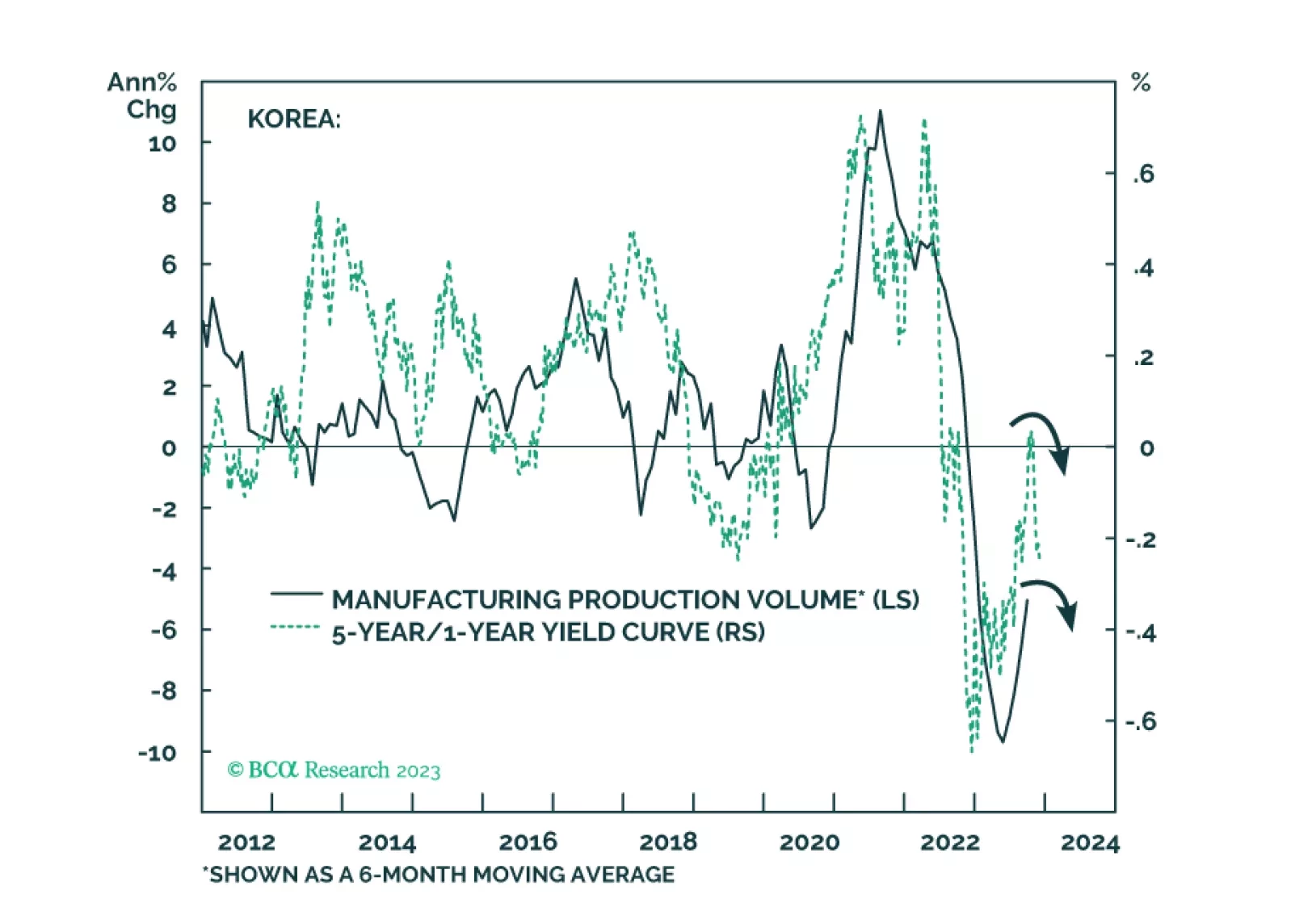

The recent increase in Korean exports will likely prove to be a mid-cycle rebound within a cyclical downtrend. Korea’s households and enterprises are among the most indebted globally, and their debt service ratio is among the highest in the world. Korea’s 10-year bond yields have peaked. We discuss opportunities in Korean stocks as well as in fixed income and currency markets.