Asset Allocation

US growth has slowed in recent weeks. This can be seen in the weaker data on retail sales, consumer confidence, services PMIs, and a swath of housing releases (notably starts, existing home sales, homebuilder confidence, and stock prices). It can also be seen in the decline in GDP tracking estimates. The Atlanta Fed's GDPNow model projects growth of 2.3% in Q1, down from a peak of 3.9% on February 3. The Citi US Economic Surprise Index has also dipped into negative territory.

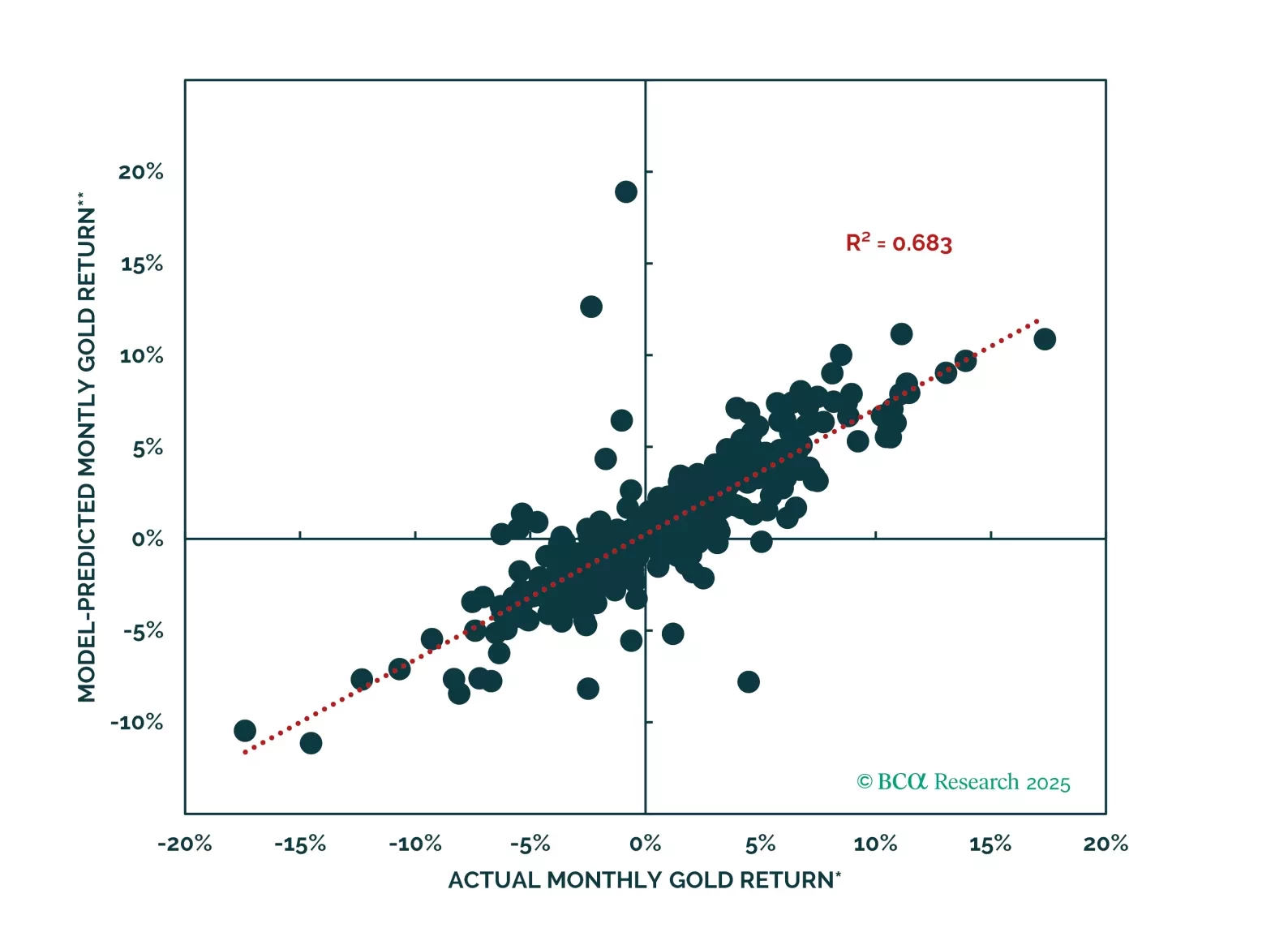

As gold keeps making new highs, many clients have asked us whether a gold allocation makes sense for their portfolios and, if so, how big that allocation should be. In this report we try to answer these questions from the perspective of investors with eight different home currencies. Specifically, we analyze the following properties of gold: 1) What drives gold? 2) What is gold’s role in a portfolio? 3) How much gold should investors own?

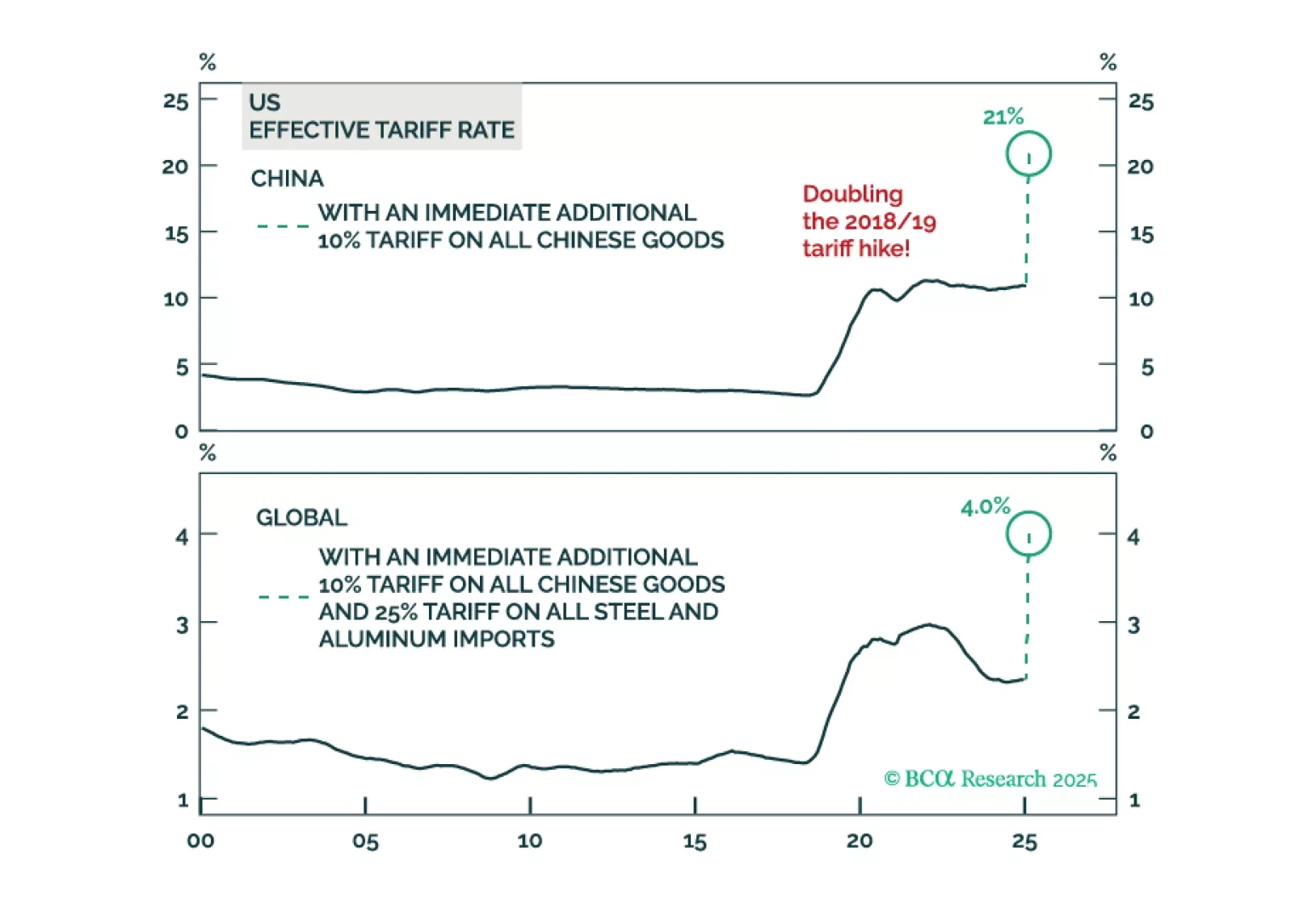

In his latest Thoughts Of The Day, Peter Berezin discusses the different moving parts of the global economy today and the potential impact of Trump's policies.

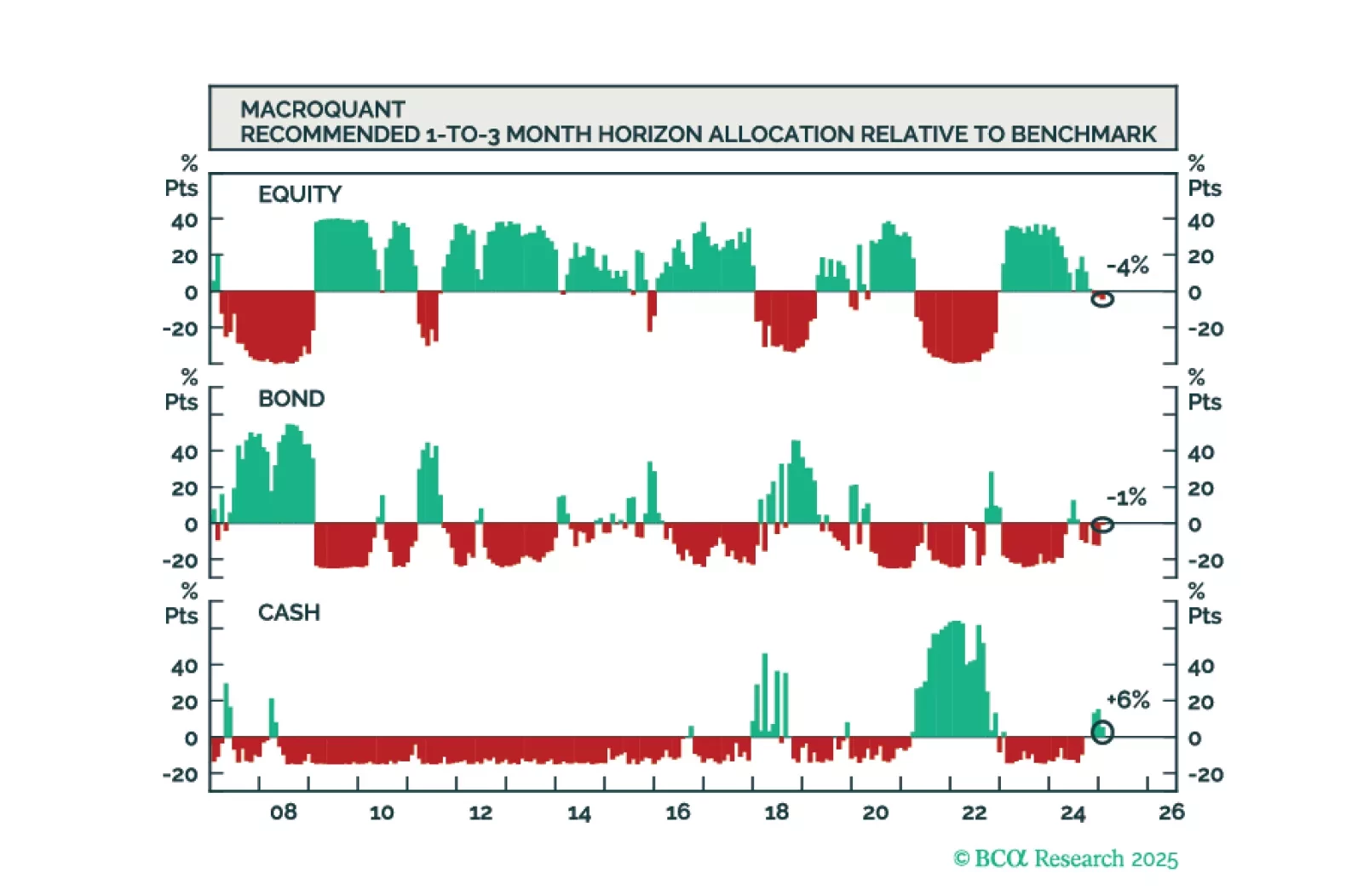

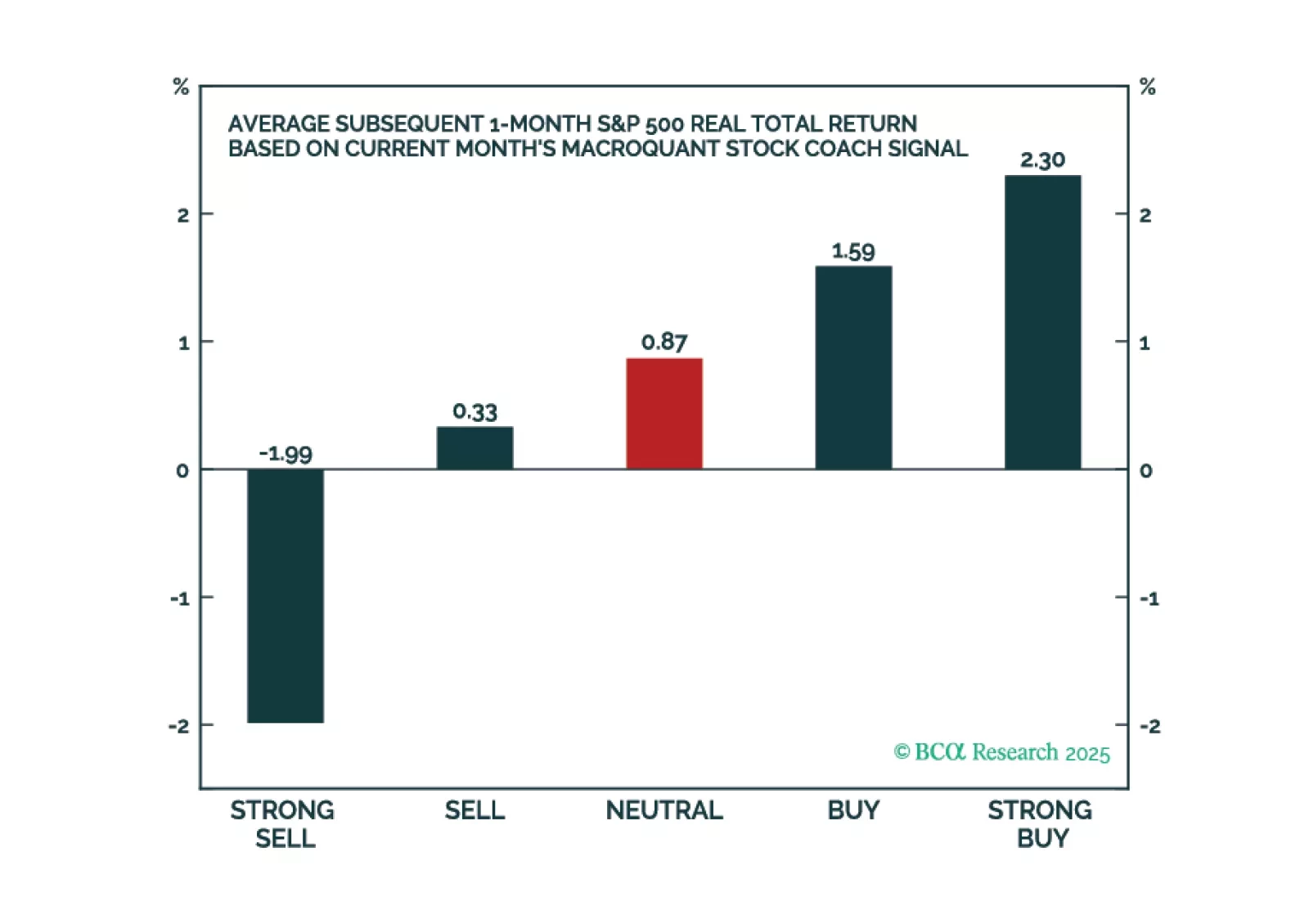

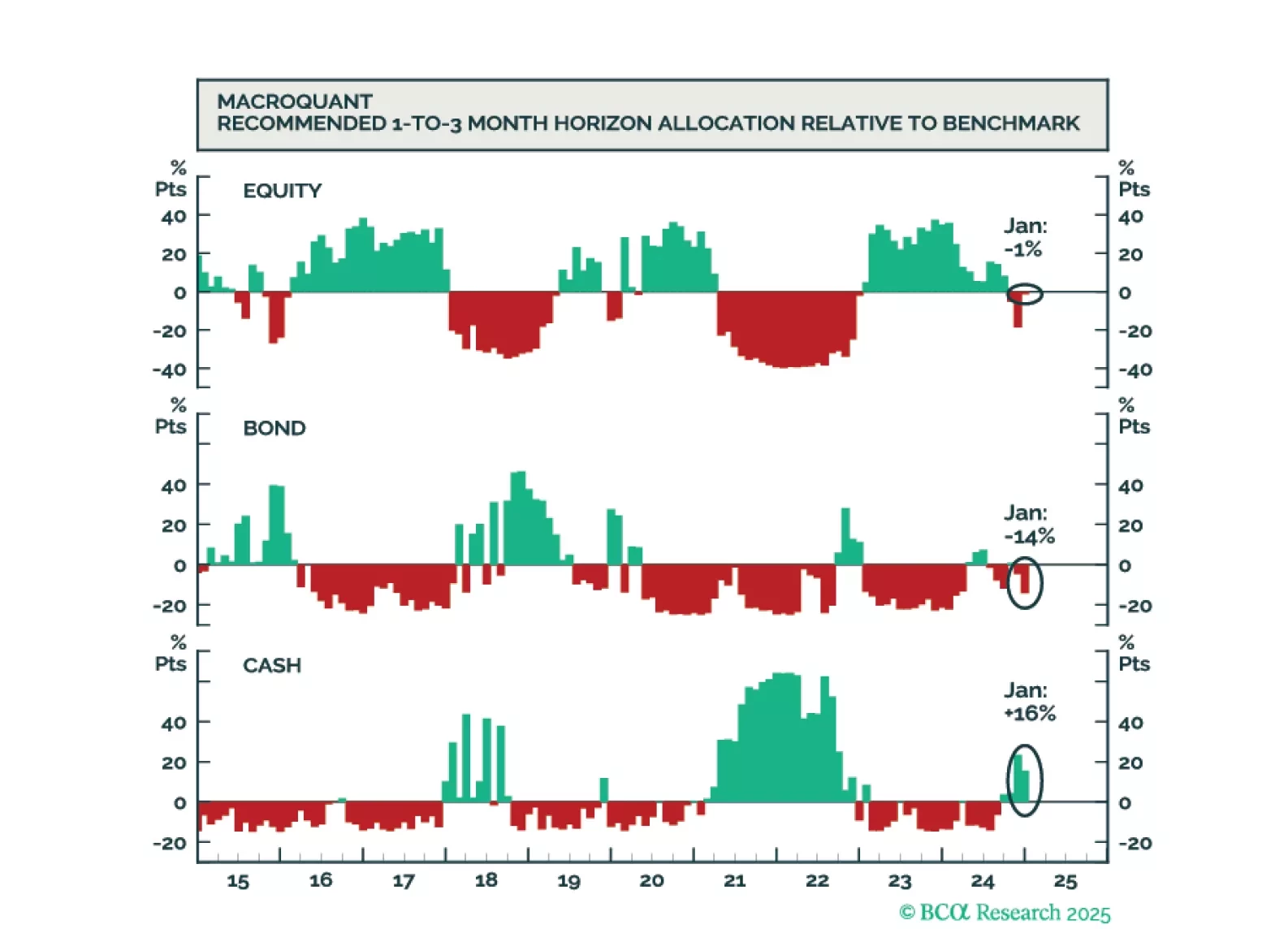

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.

While the US economy could remain upright on the tightrope for a while longer, it will inevitably fall, leading to a major bear market in stocks. We will be looking to our MacroQuant model for guidance on when to turn fully defensive. We are not there yet.

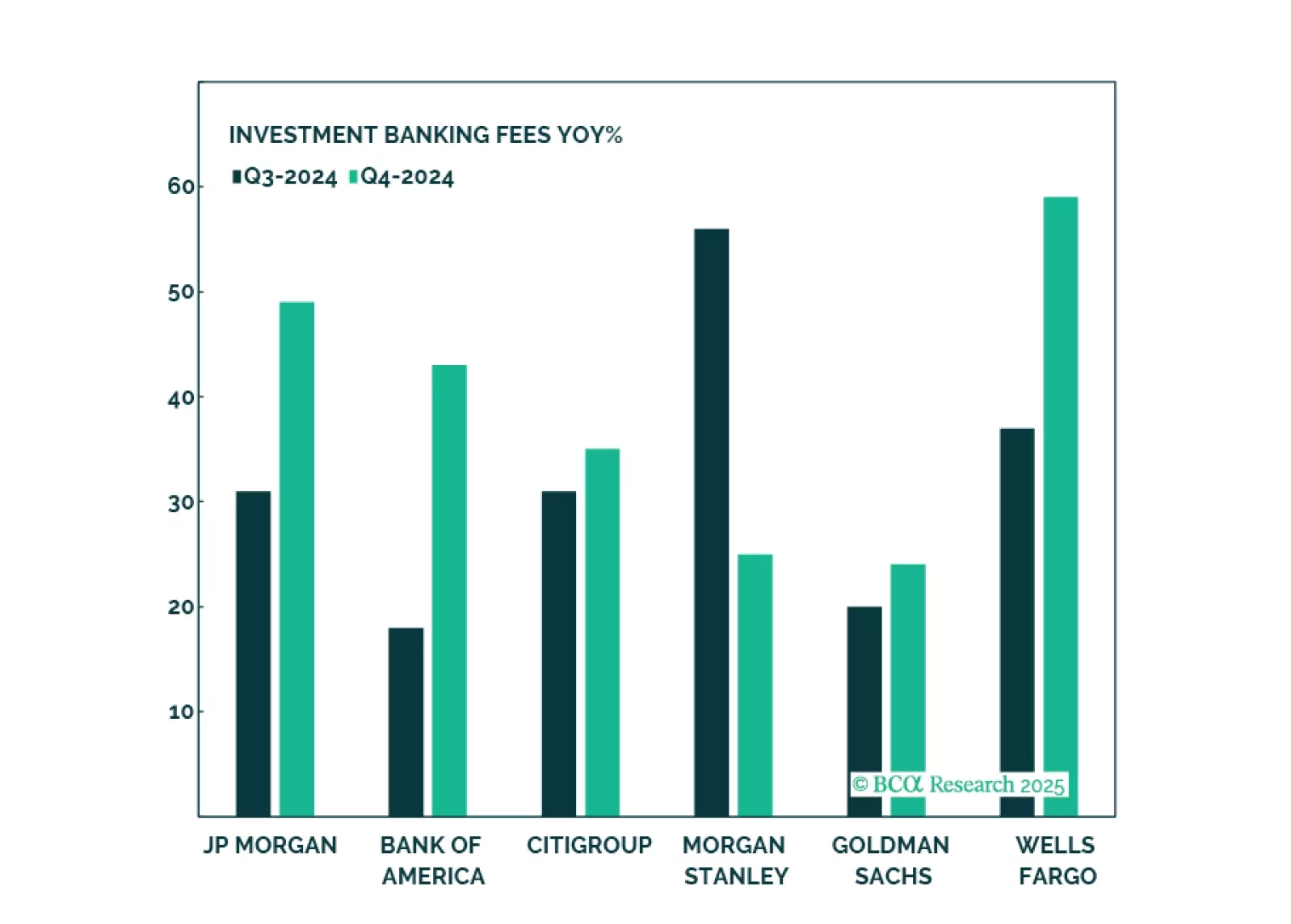

Banks have had an amazing run, and while such strong performance is unlikely to repeat, there is still oomph left in the trade thanks to a more favorable regulatory environment, stronger demand for loans, a steeper yield curve, and a strong pipeline of capital market activity. Key risks are further tightening of monetary policy and an increase in bad loans. We reiterate our overweight on Capital Markets, Diversified Banks, and Regional Banks.

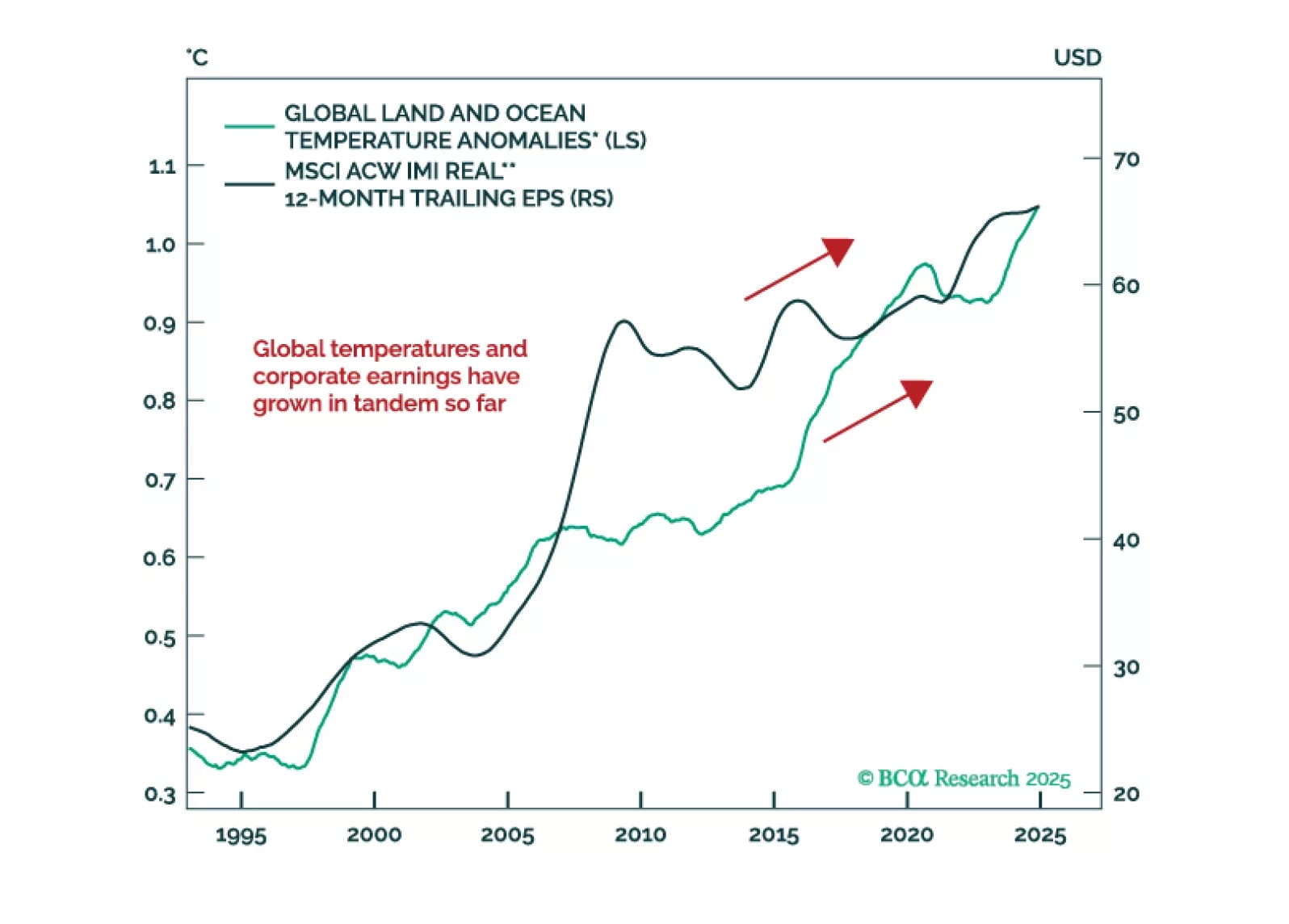

In our Beta report, we take a break from US politics and focus on the investment implications of climate change. Our colleague Ritika Mankar, of BCA’s Global Investment Strategy, makes a case for long-term investors to actually completely ignore climate change in their strategic asset allocation. Global warming will simply not make any difference, macroeconomically speaking, over the next five to ten years. Over a longer time horizon, climate change may even spur more economic growth, although with higher inflation as well.