Asset Allocation

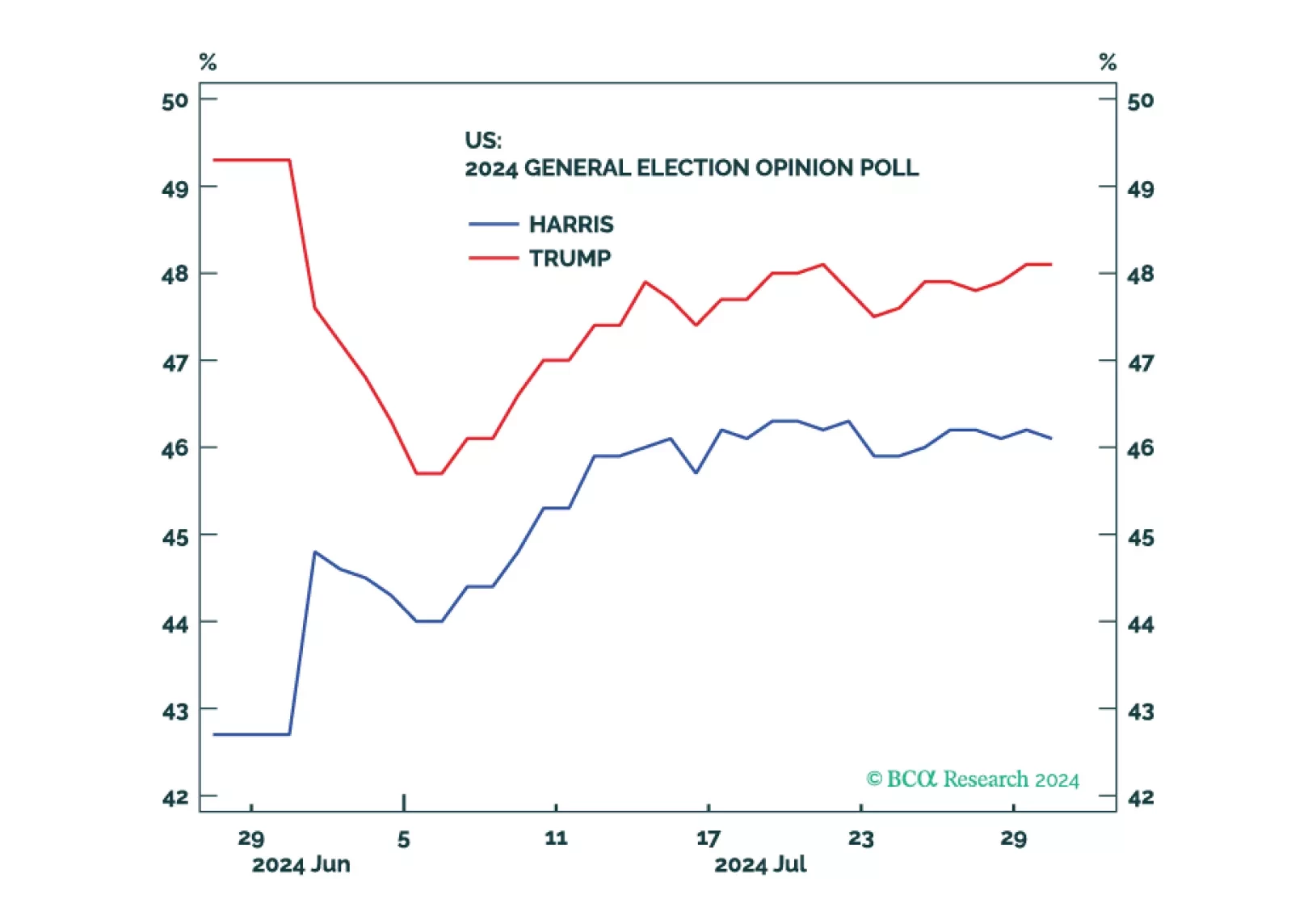

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

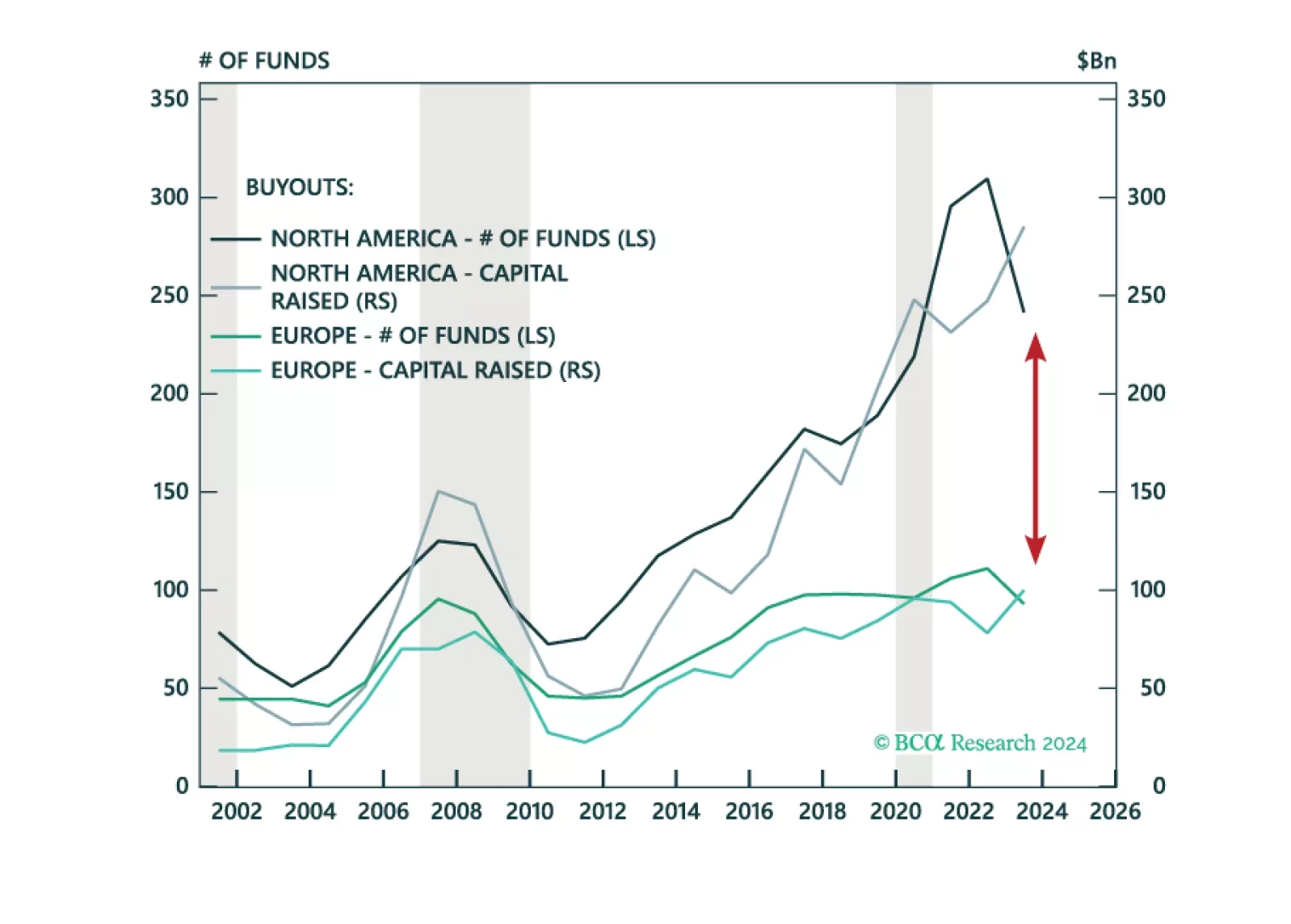

We are growing positive on Growth assets with recession expectations increasing our optimism on entry points. Equities are led by APAC Private Equity, North America Venture Capital, and Europe Buyouts. Our outlook continues to improve on CRE within the Inflation & Diversification bucket while we are underweight Multi-Strategy amongst Hedge Funds. We maintain an overweight to Senior Direct Lending for Income with a preference for North America.

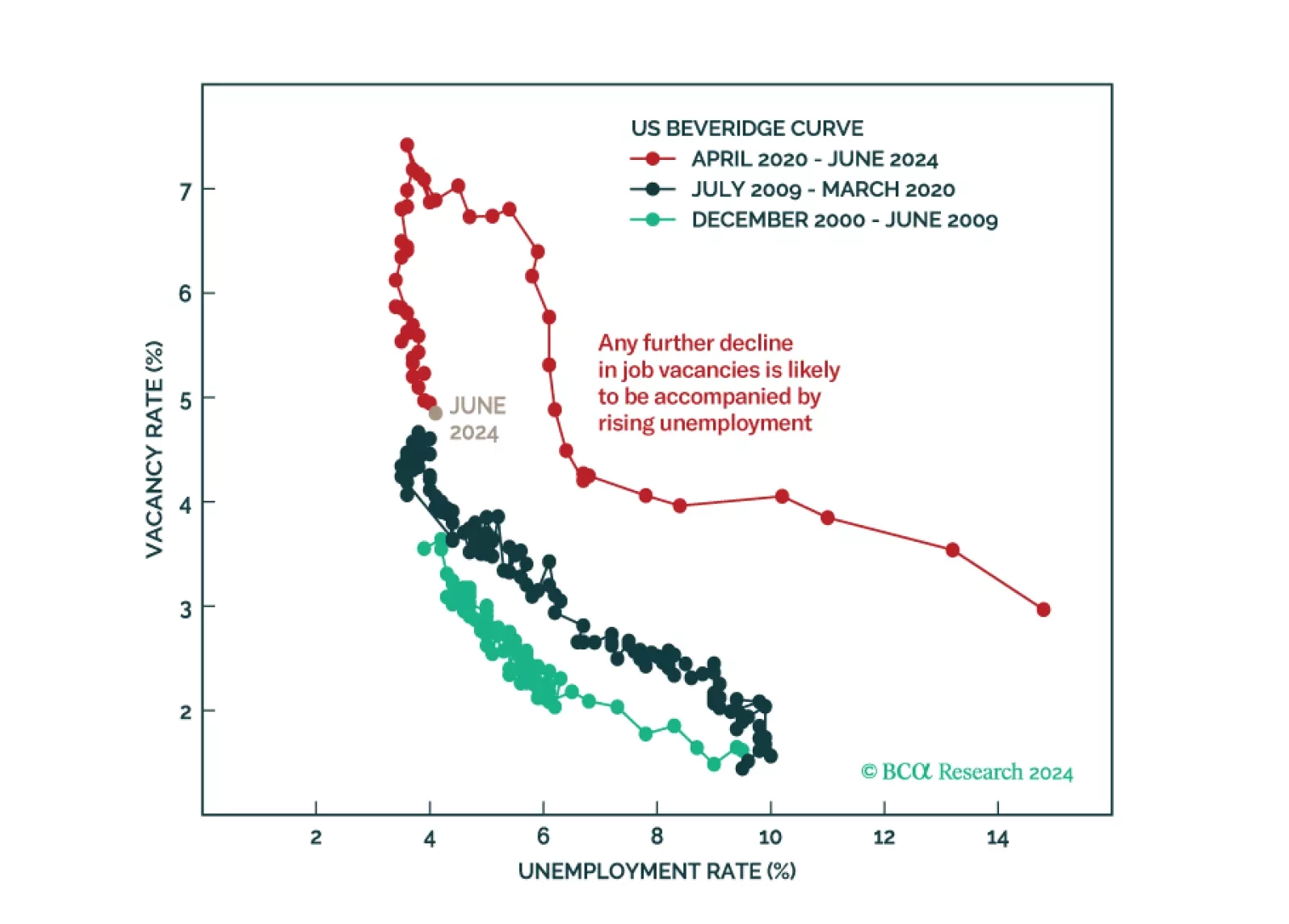

Don't buy the dip. The equity bull market is over. The US will enter a recession in late 2024 or in early 2025.

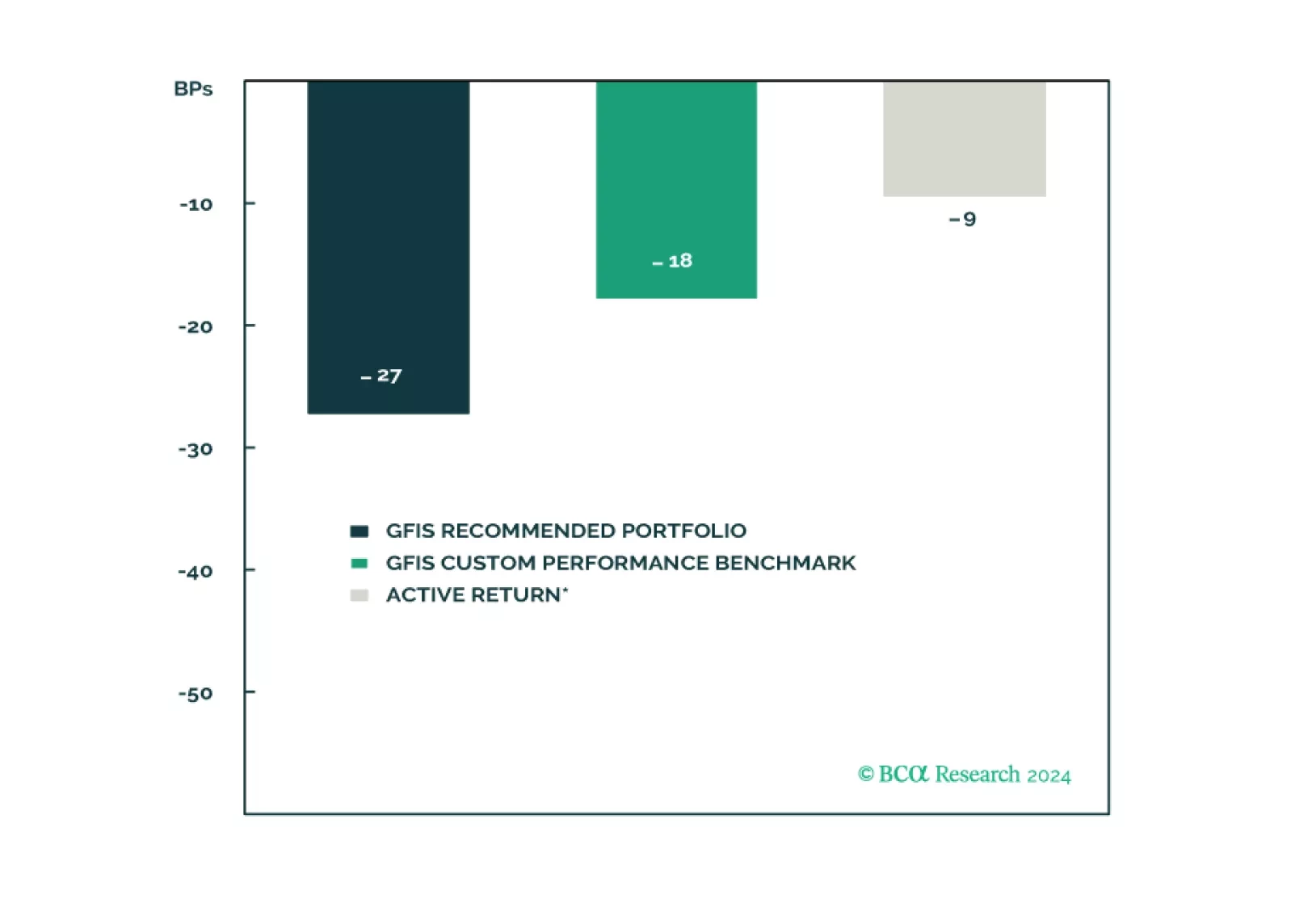

In this report, we present the quarterly review of our Model Bond Portfolio. Rebounding growth and political instability led to slightly negative portfolio performance in Q2/2024. As global growth starts to moderate, we continue to favor government bonds over credit. Maintain a defensive portfolio stance.