Asset Allocation

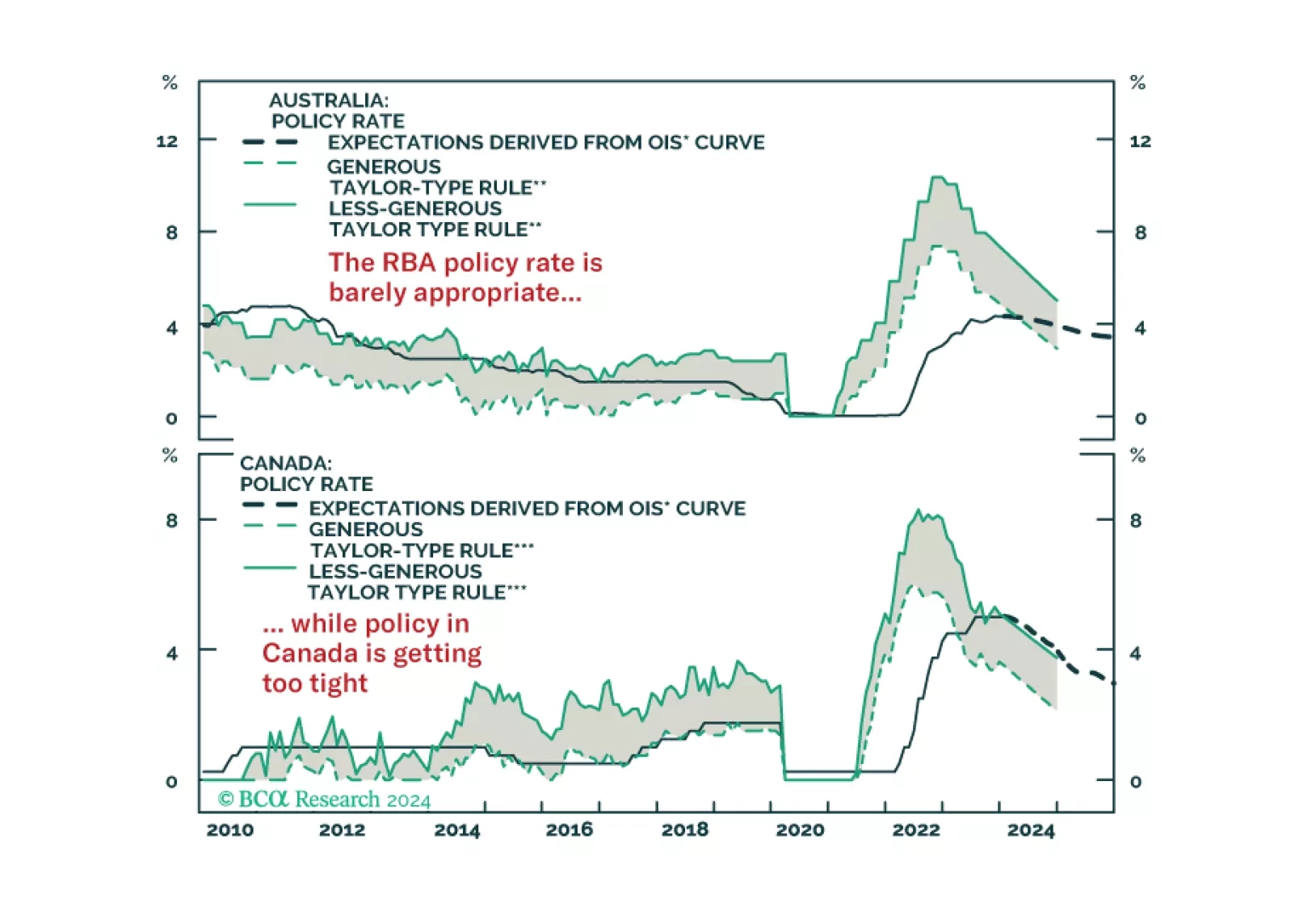

In this Strategy Insight, we assess the monetary policy path for Australia and Canada in 2024 and we discuss how to profit from a growing divergence between the two economies.

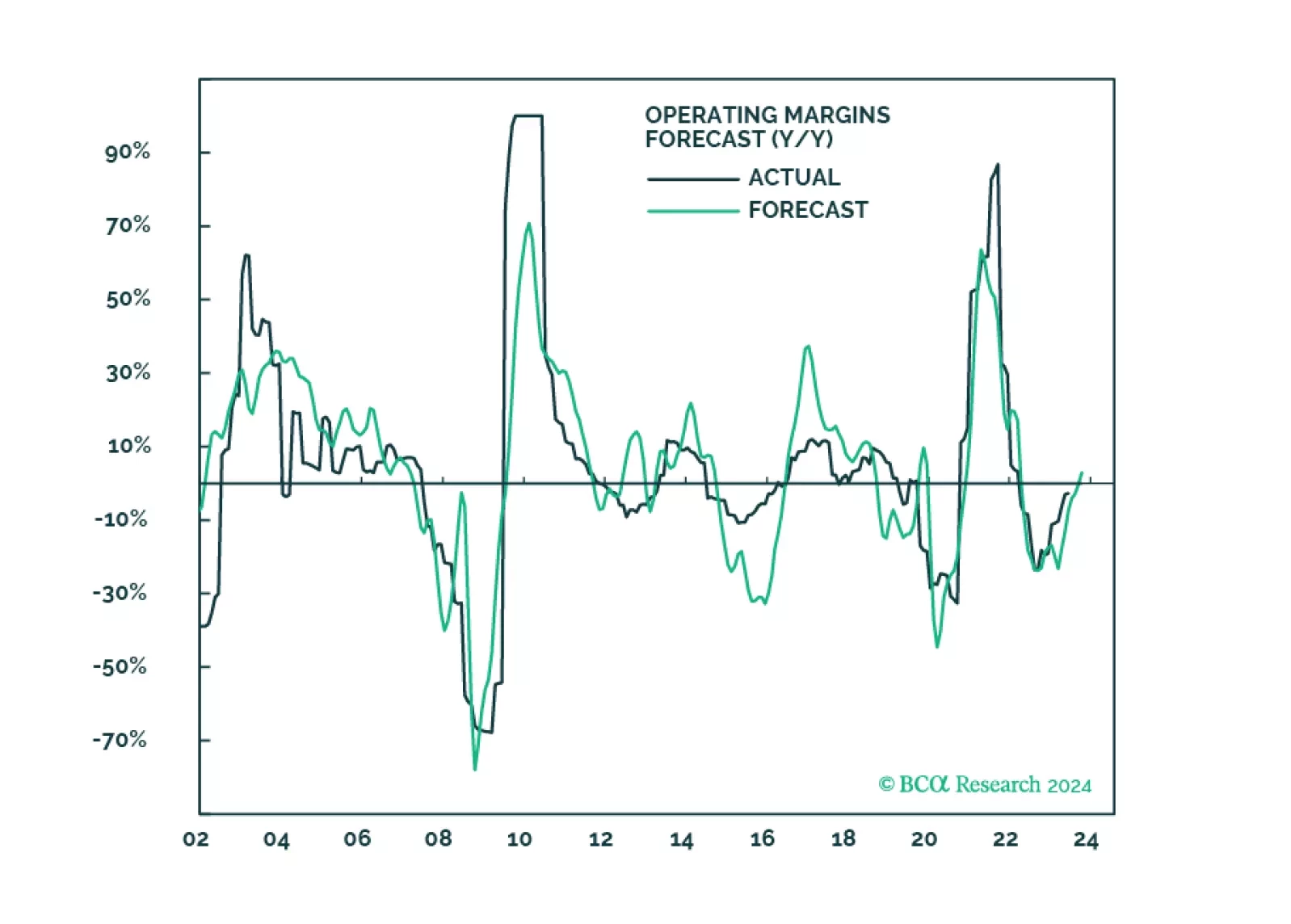

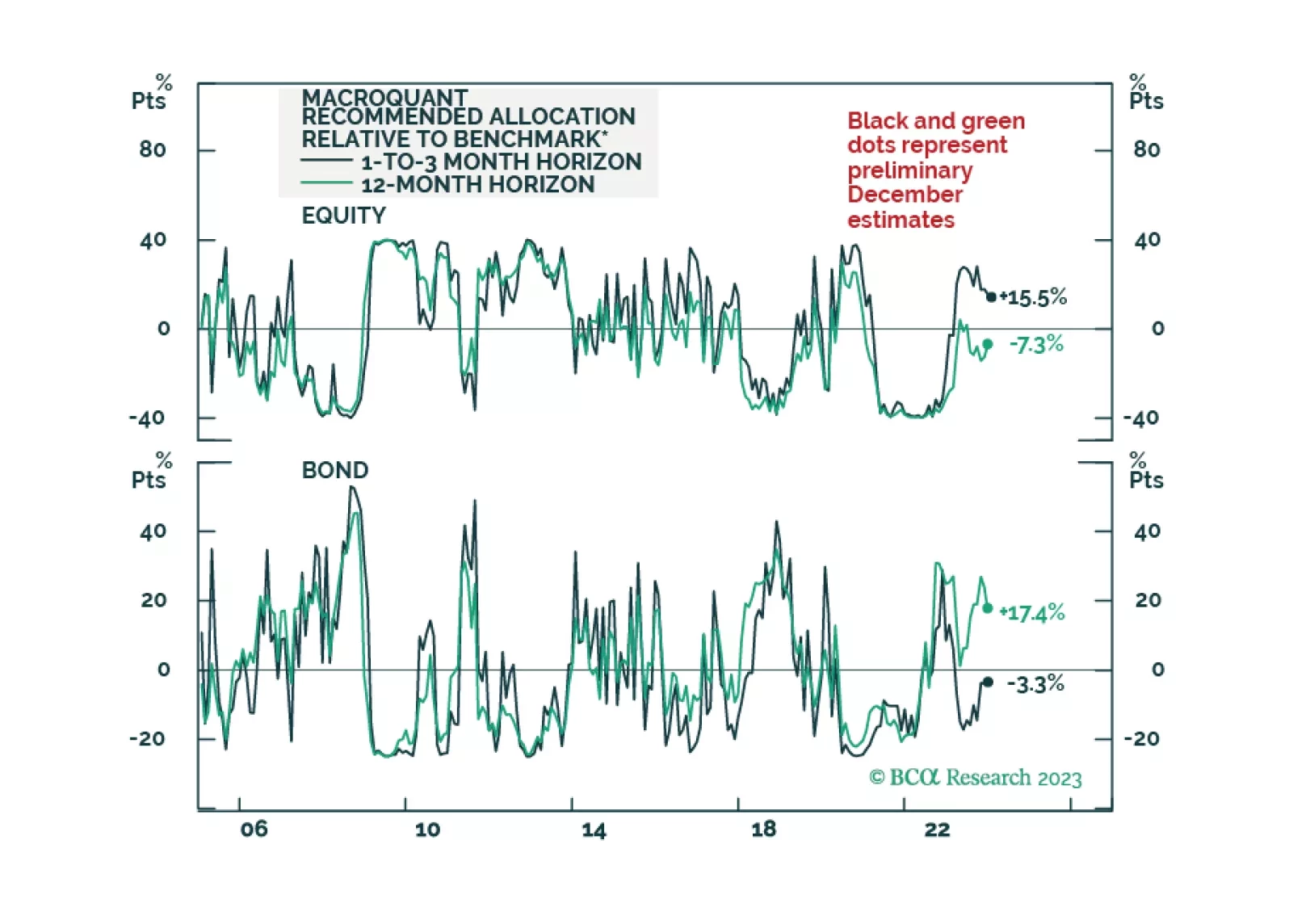

Disinflation coupled with sticky wage growth is likely to result in either a second wave of inflation or layoffs and a recession. In the meantime, market expectations for sales, growth, and margins are overly optimistic and are inconsistent with macroeconomic headwinds. We recommend gradually realigning the portfolio to a more defensive stance.

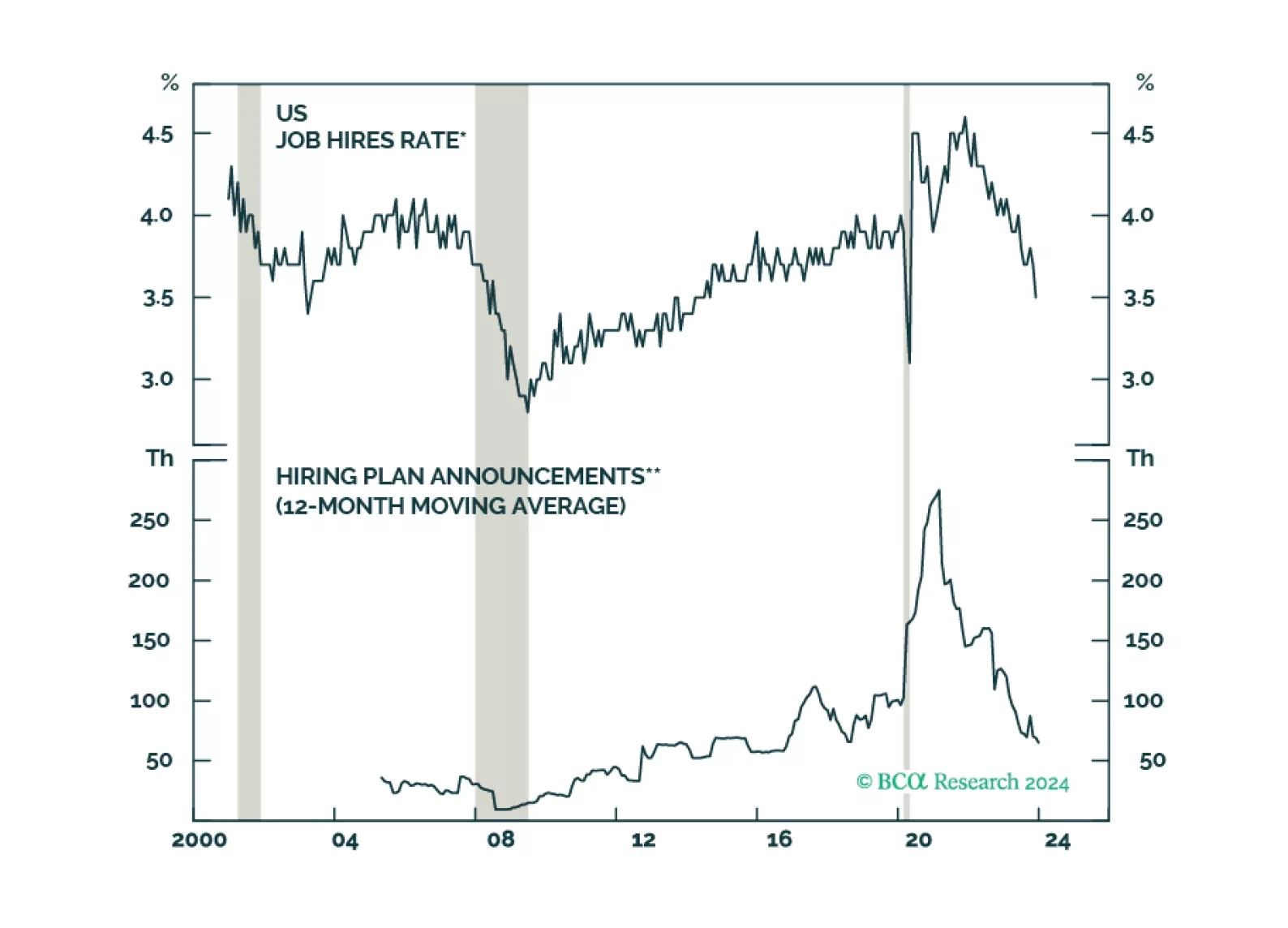

Investors have taken comfort in the fact that unemployment has remained low in the major economies. But underneath the surface, there are clear signs that labor demand is weakening. The clock keeps ticking towards our H2 2024 recession call. After being bullish on risk assets last year, we are slowly turning more defensive.

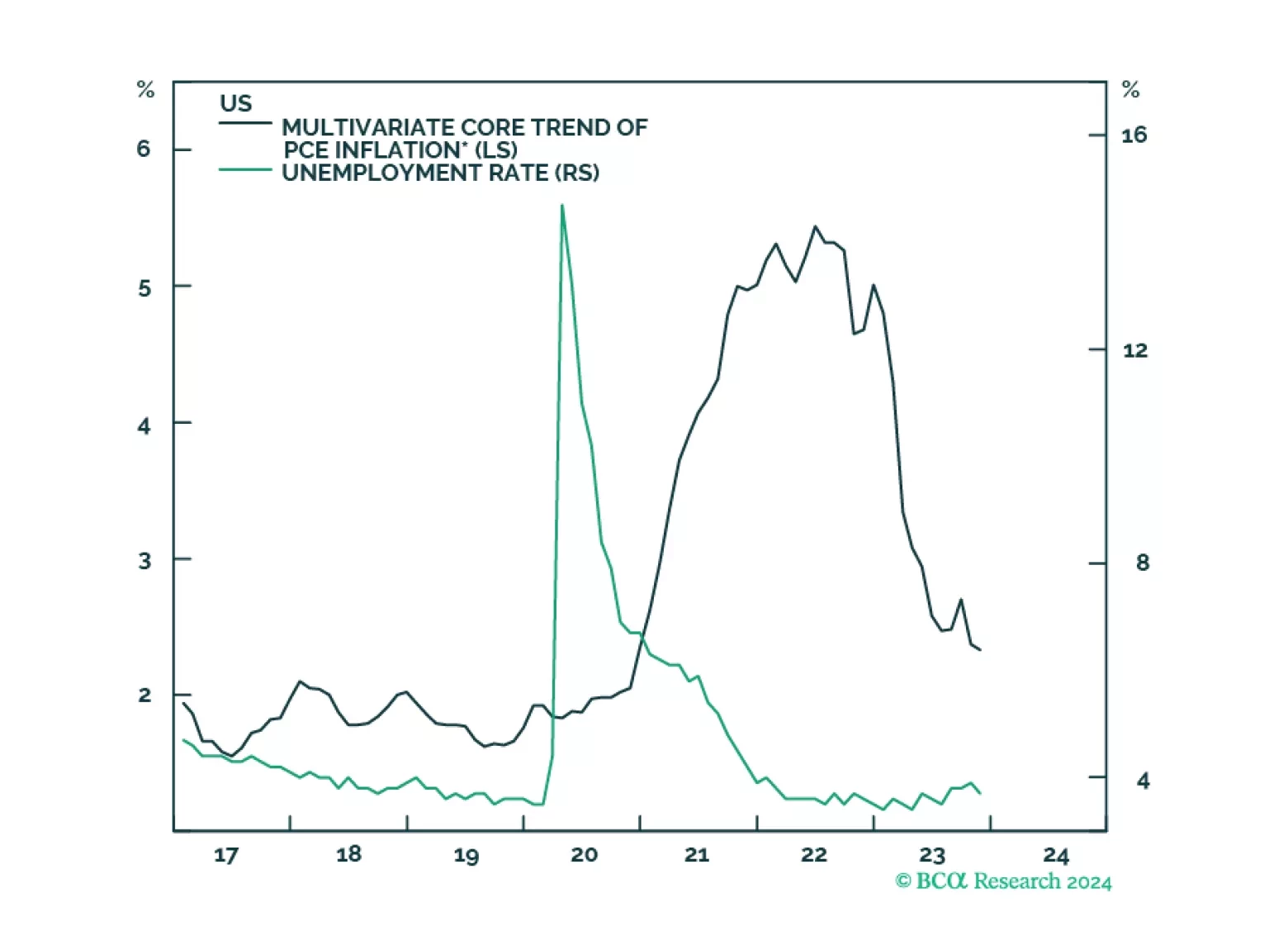

A soft landing can be achieved but not maintained. We are cutting our tactical recommendation on stocks from overweight to neutral and scaling back our long-duration stance.

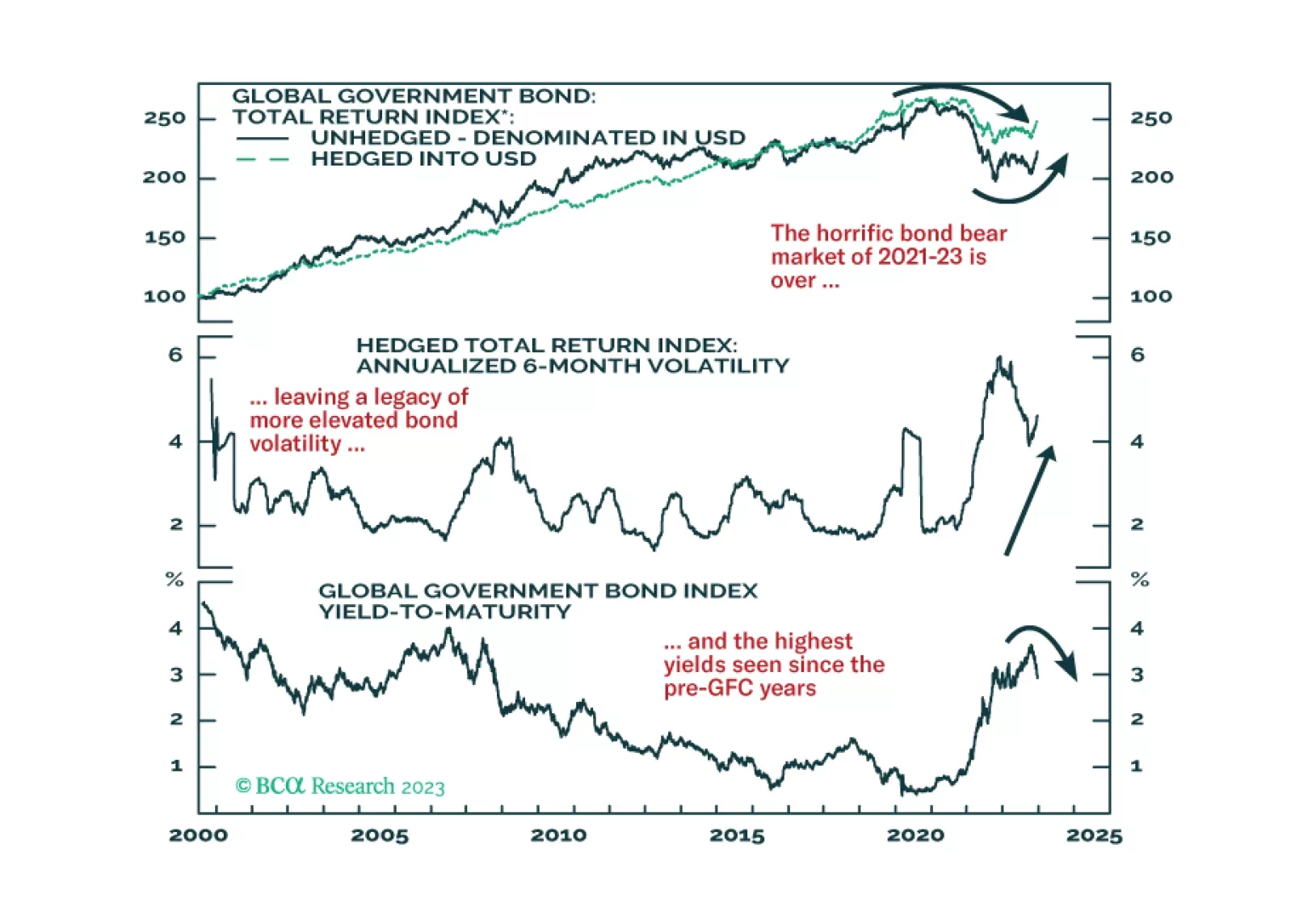

In this, our final report of the year, we present our main global fixed income investment themes and recommendations for 2024.

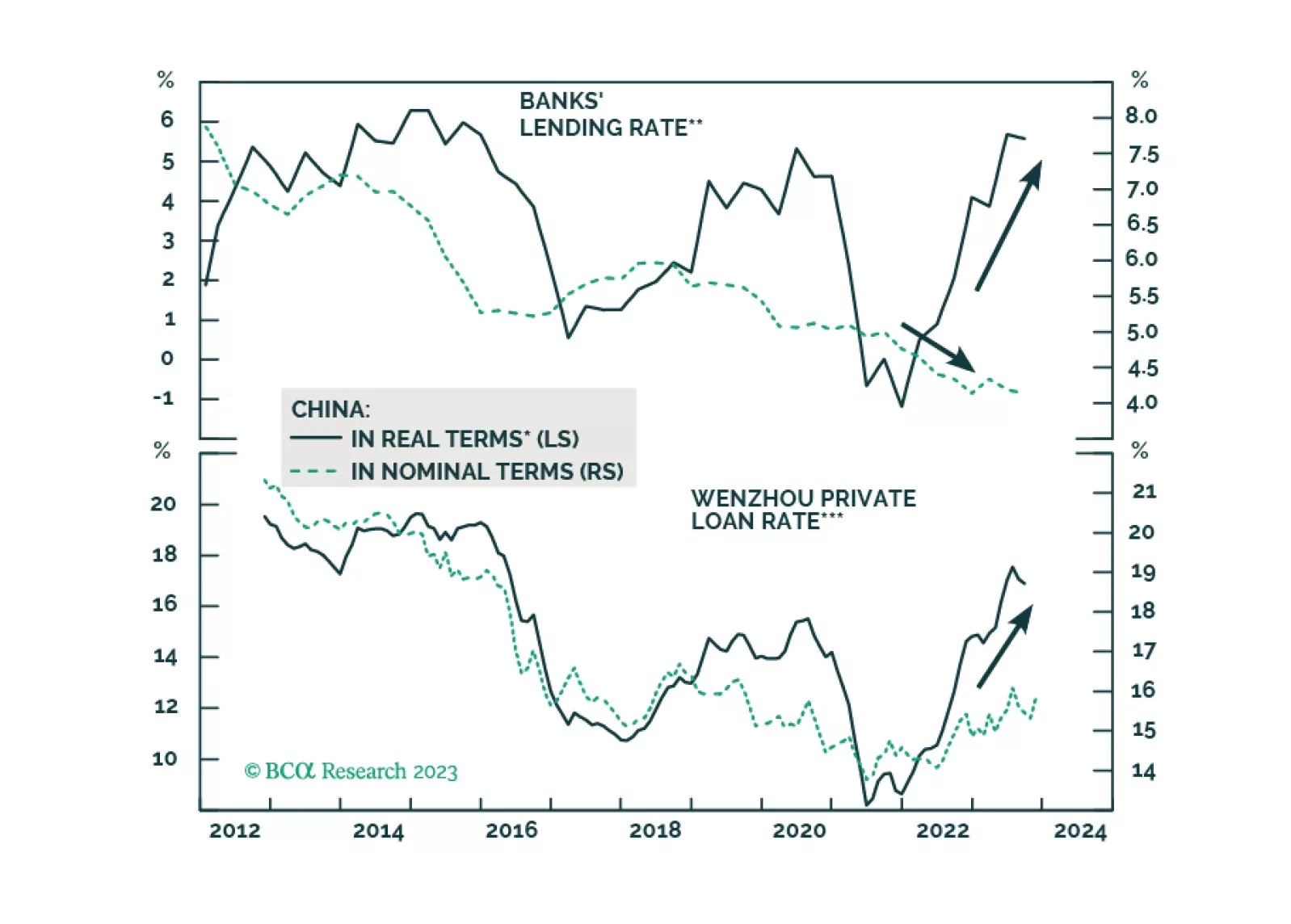

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.

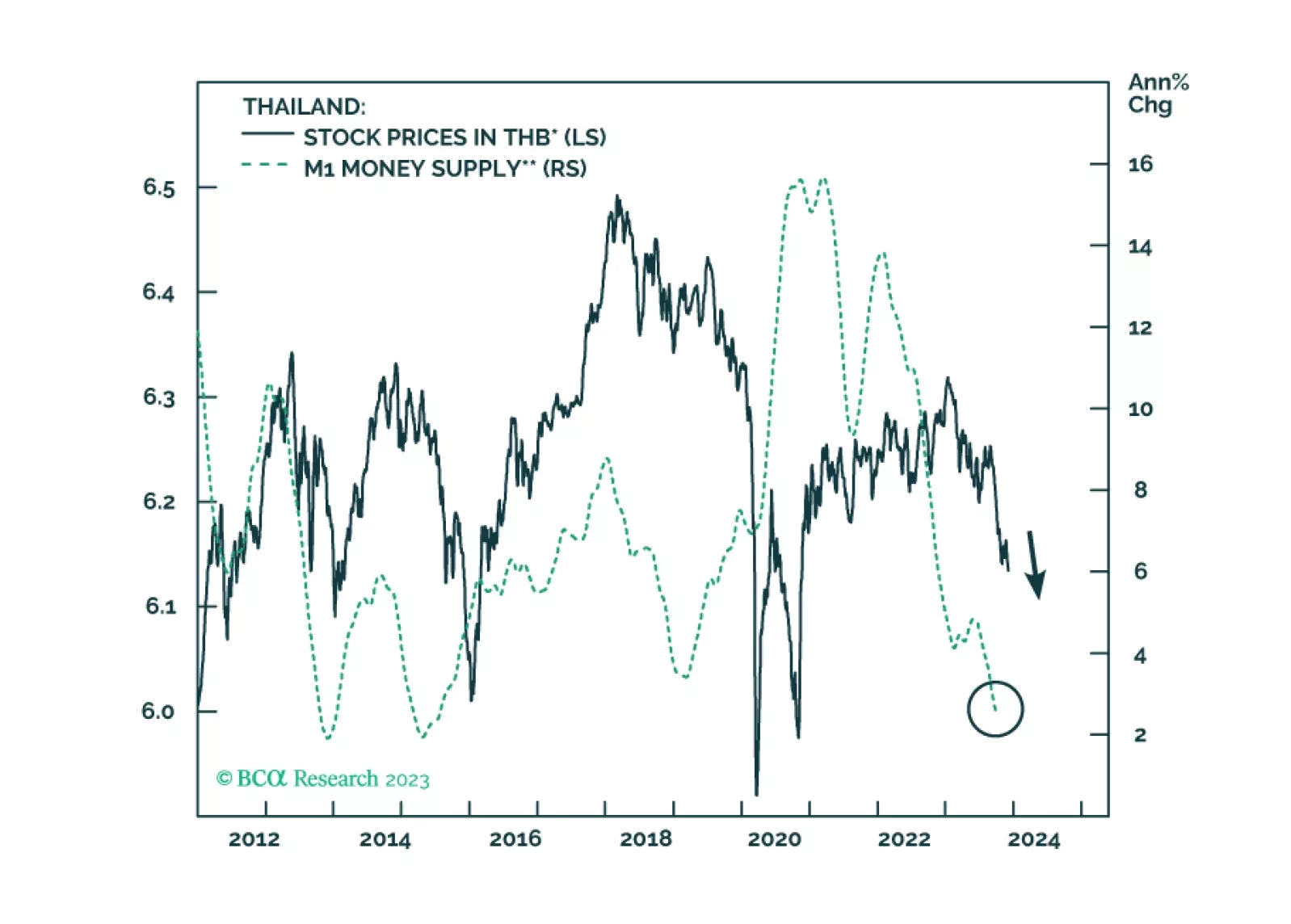

Meager credit growth and shrinking real wages will keep Thai inflation very low in the coming months. The currency will get support from an improving current account surplus. Fixed-income investors should upgrade Thailand from neutral to overweight within EM domestic bond portfolios.