Asset Allocation

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.

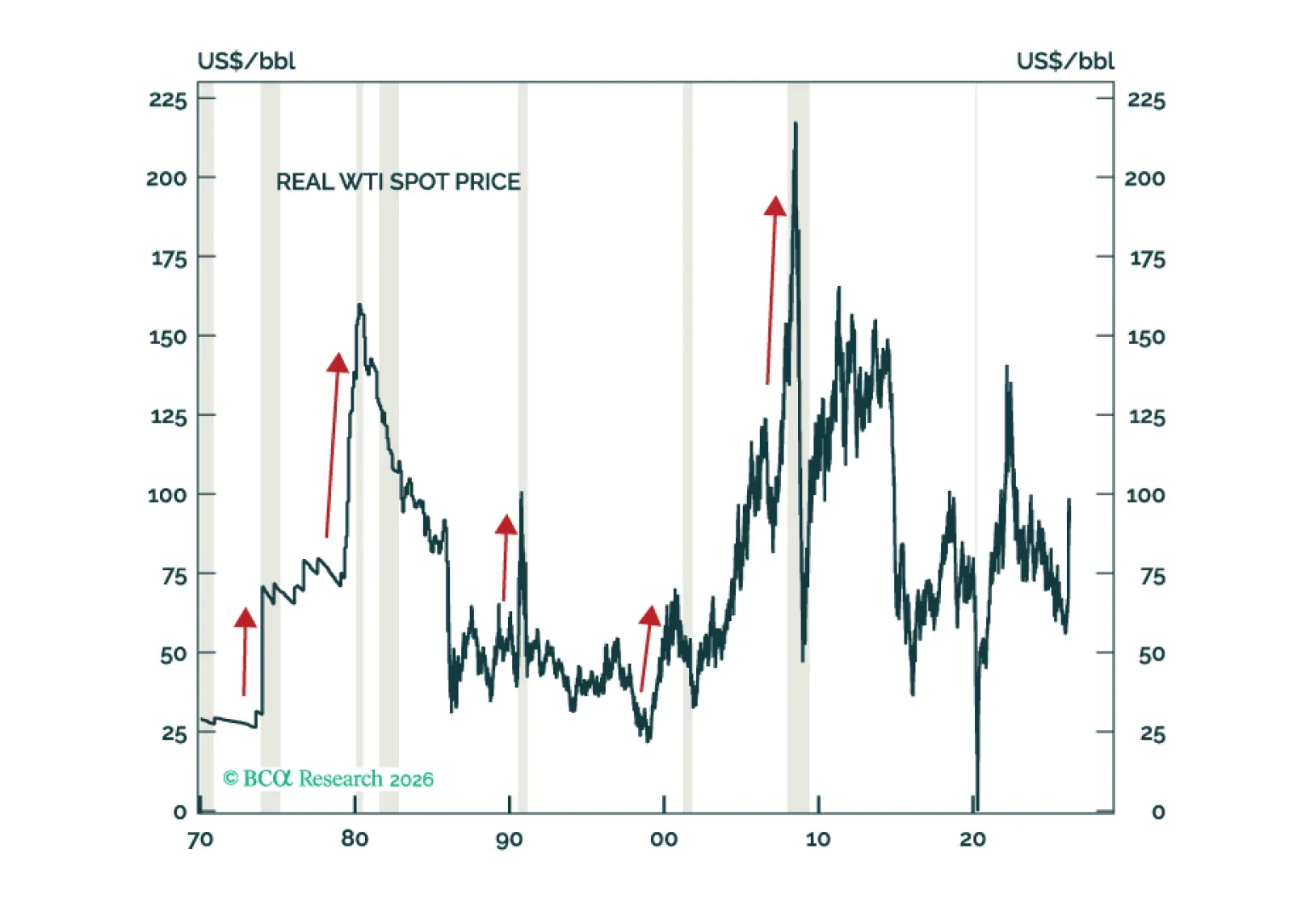

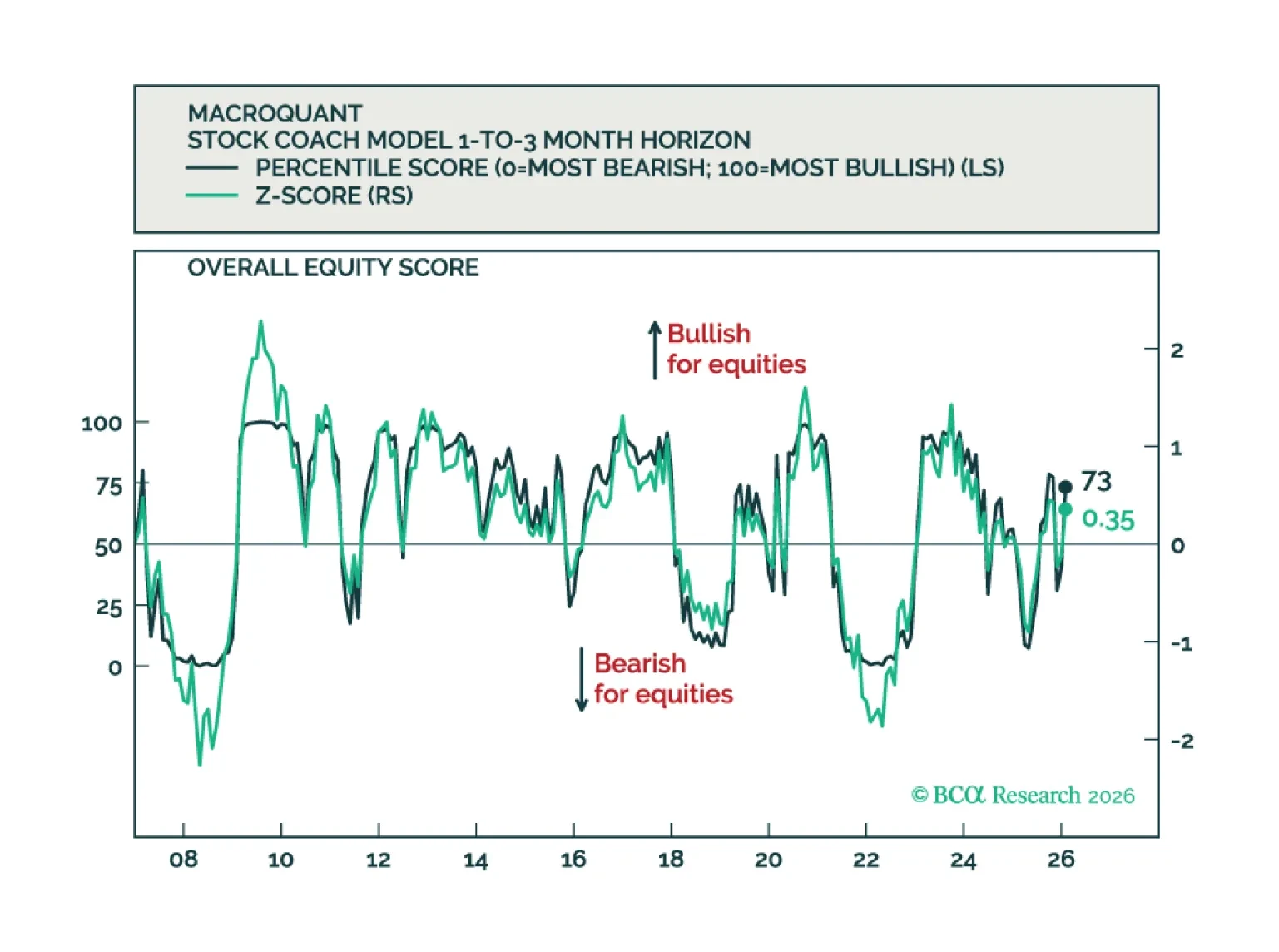

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

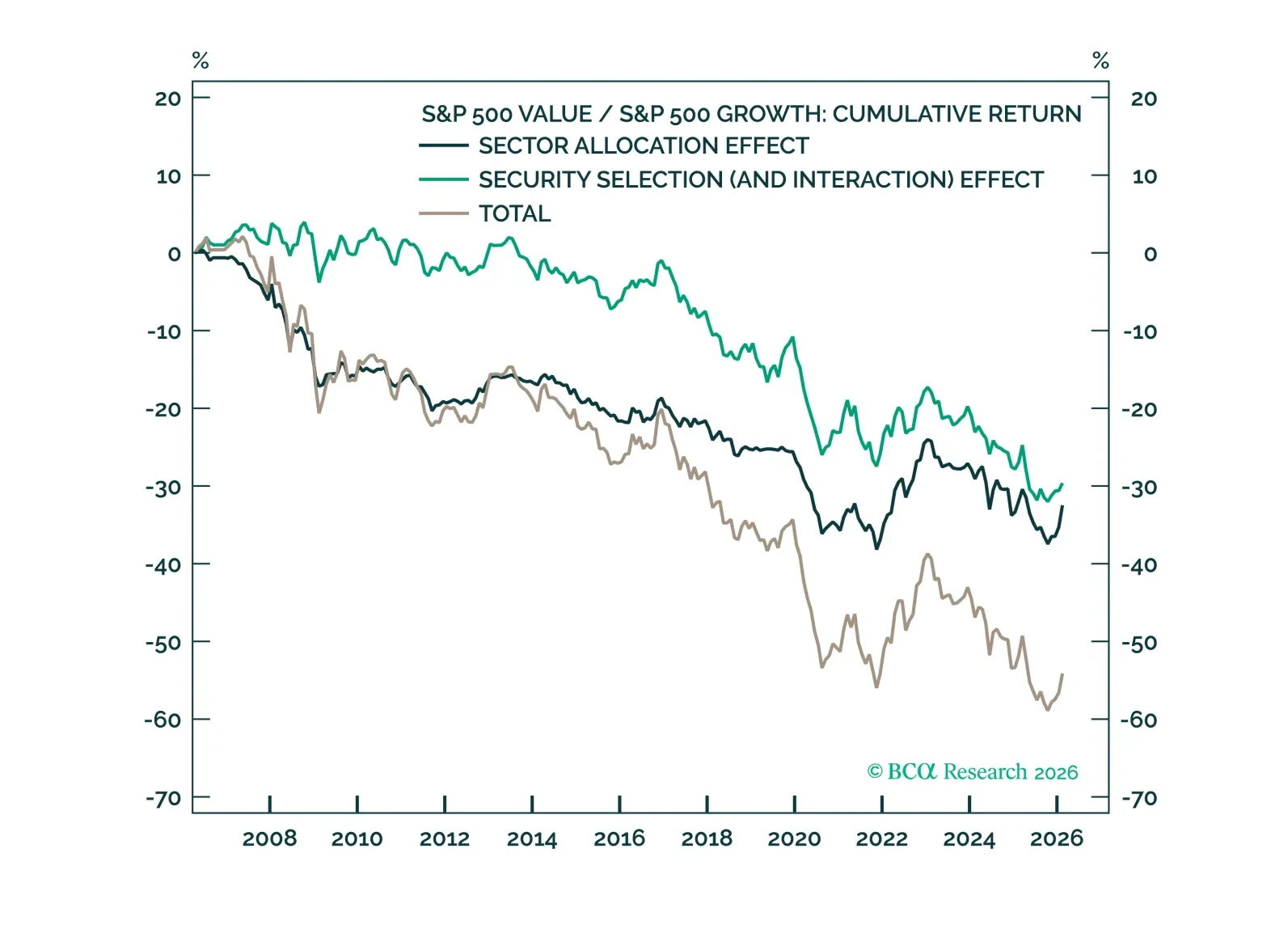

Although Value has had a meaningful run, the longer-run Growth trend likely remains intact. However, benchmark Growth indices are increasingly concentrated. Sector-neutral and within-sector implementations may allow investors to retain much of the same Growth/Value exposure while reducing dependence on technology and limiting concentration risk.

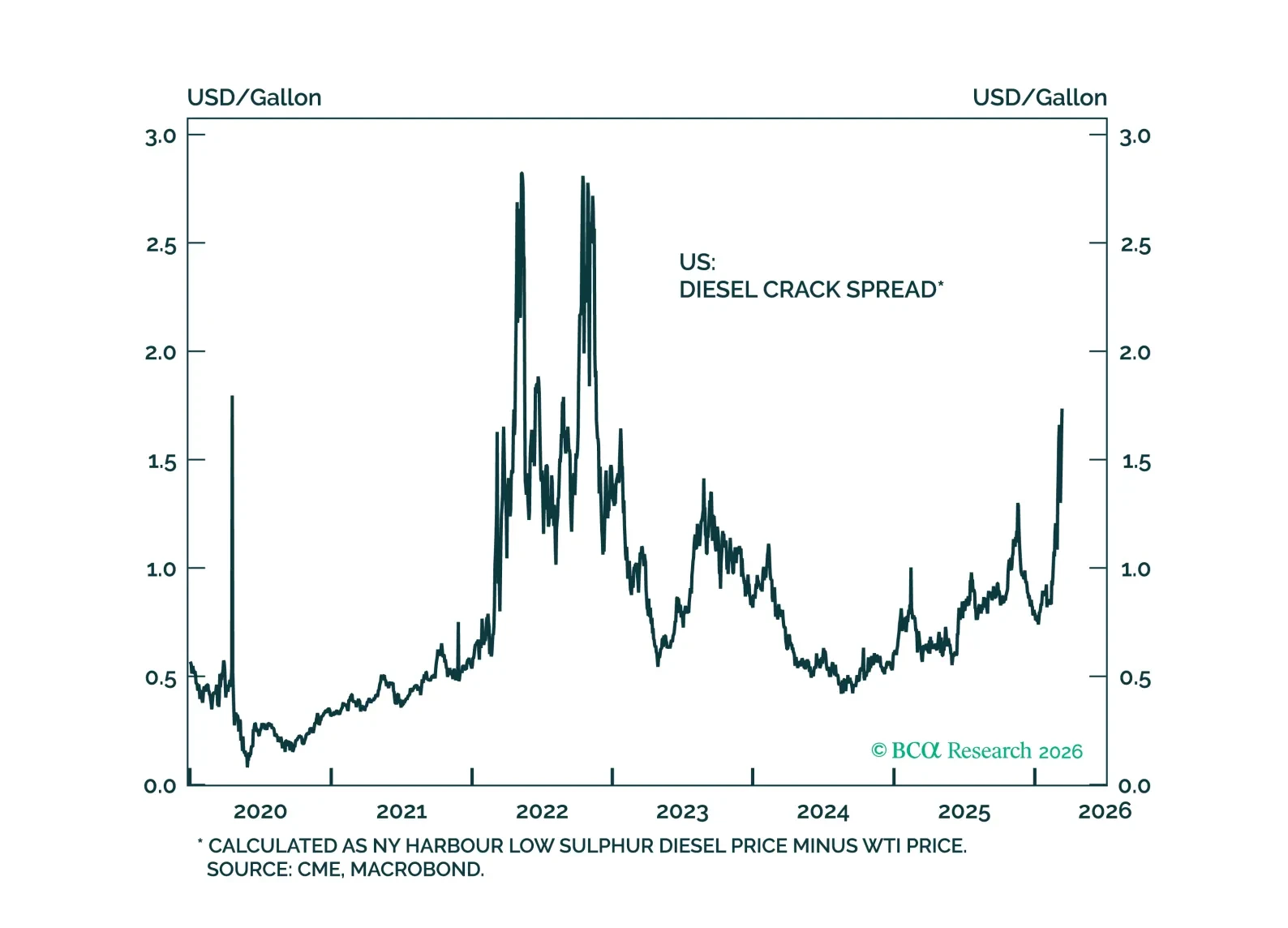

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

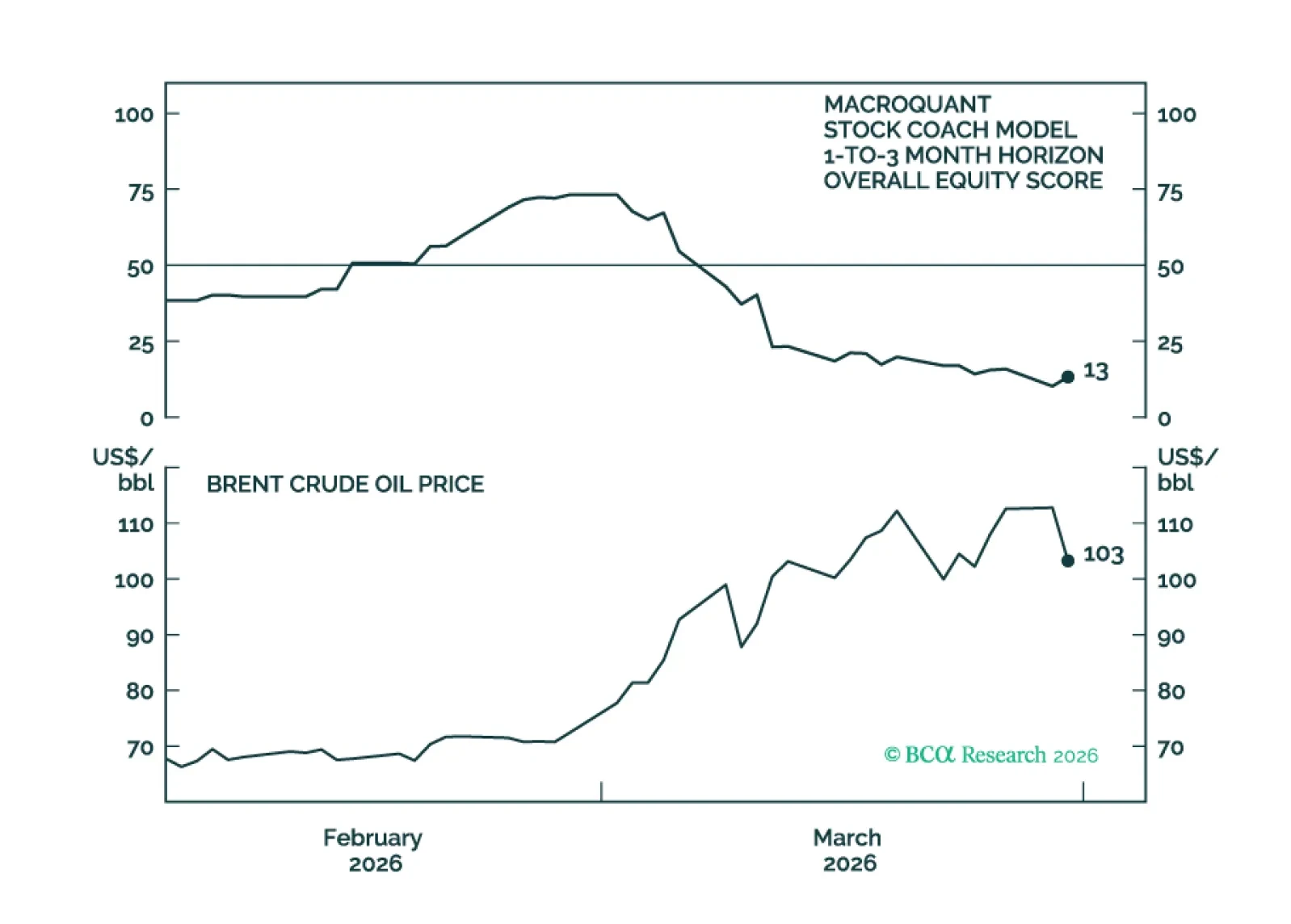

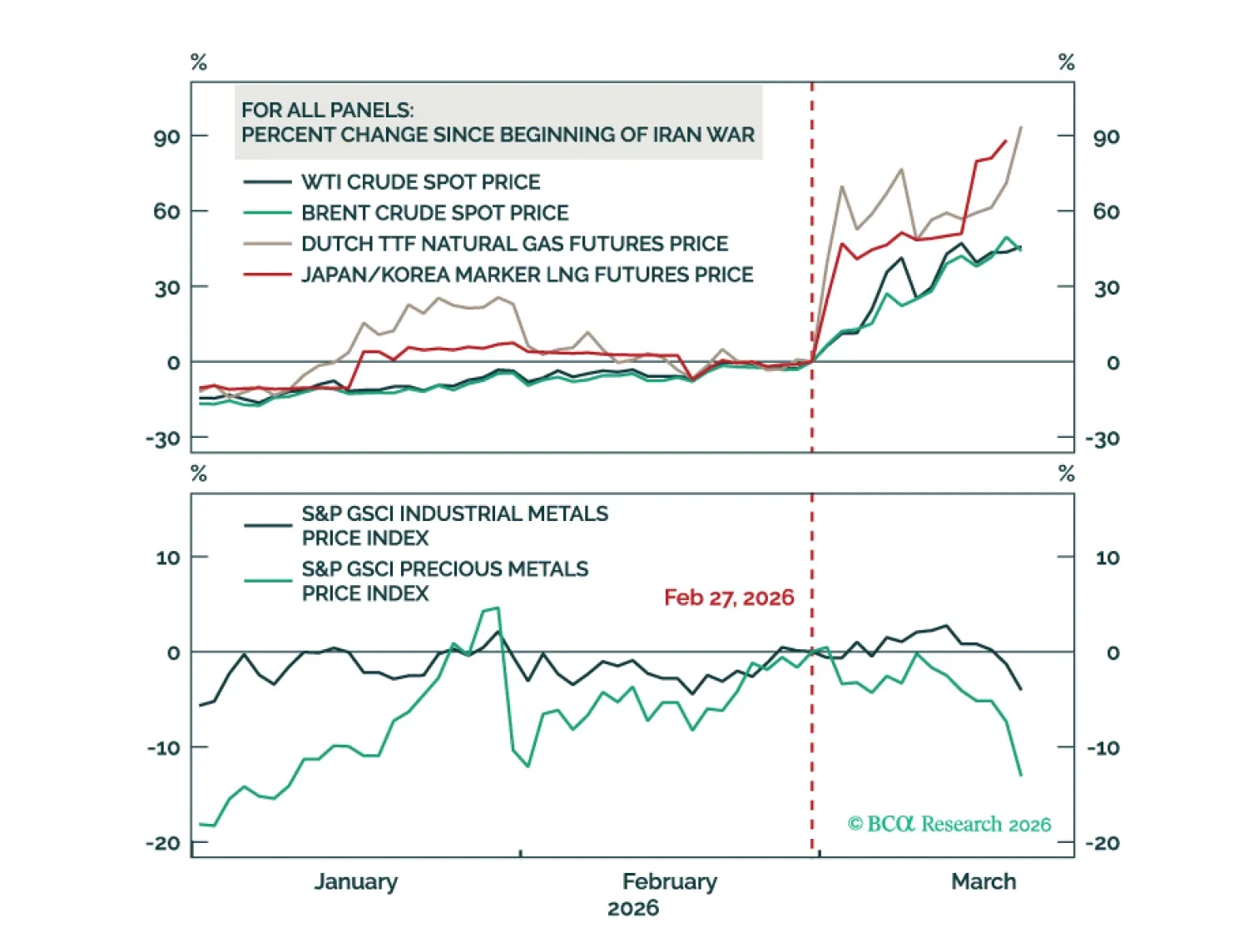

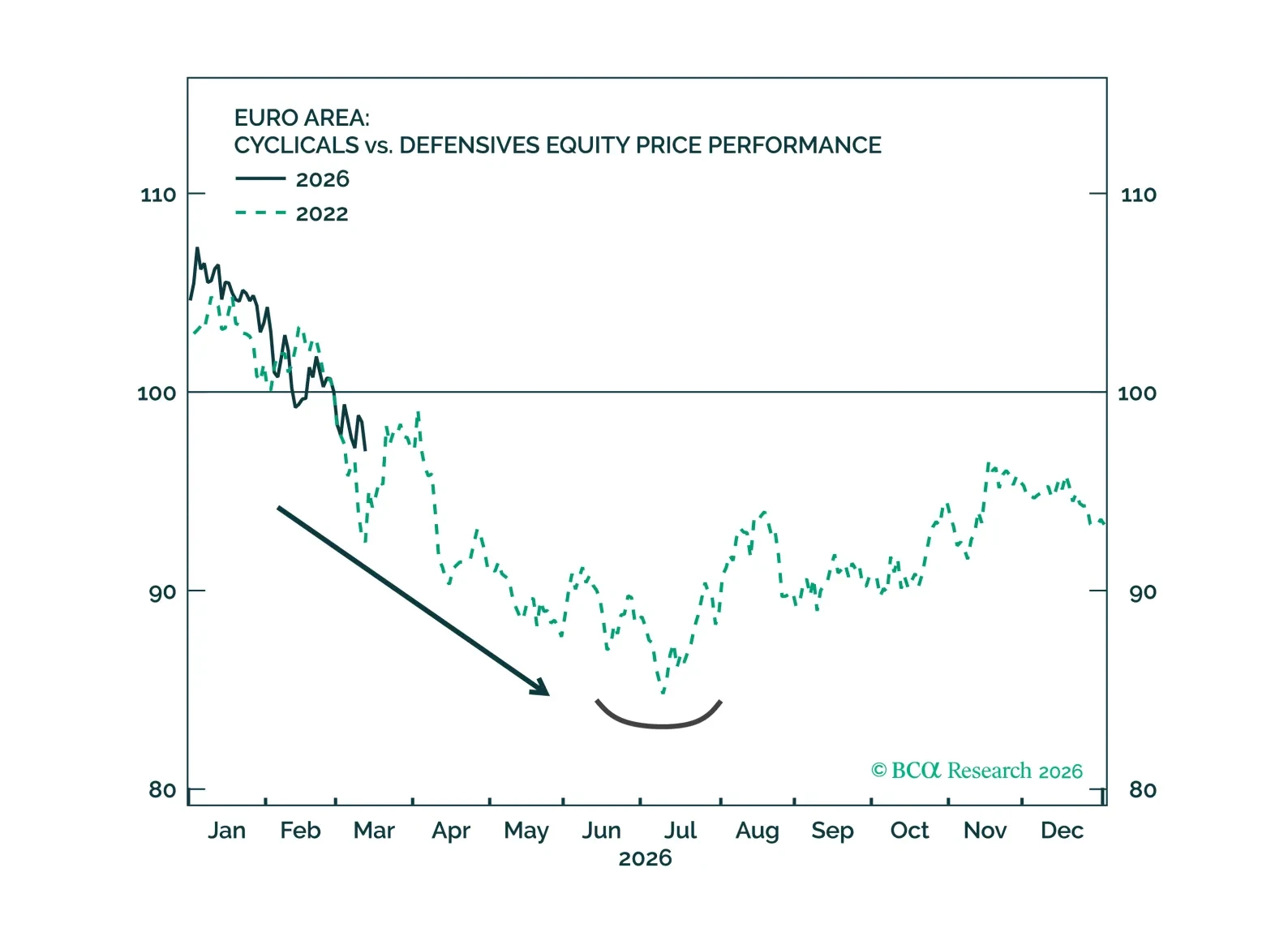

War momentum and escalating rhetoric around the Strait of Hormuz have pushed Brent above $100 and raised the risk of a broader supply shock. While parallels with 2022 offer a roadmap, today’s shock is likely shorter but more globally disruptive. Markets are repricing monetary tightening risks, though we see rate hikes as a mistake absent second-round inflation. Beyond oil, sulfur, helium, and fertilizer disruptions threaten food prices and the AI supply chain. Position defensively.

Investors are too complacent on the closure of the Strait of Hormuz. Upgrade cash and downgrade equities, both to neutral.

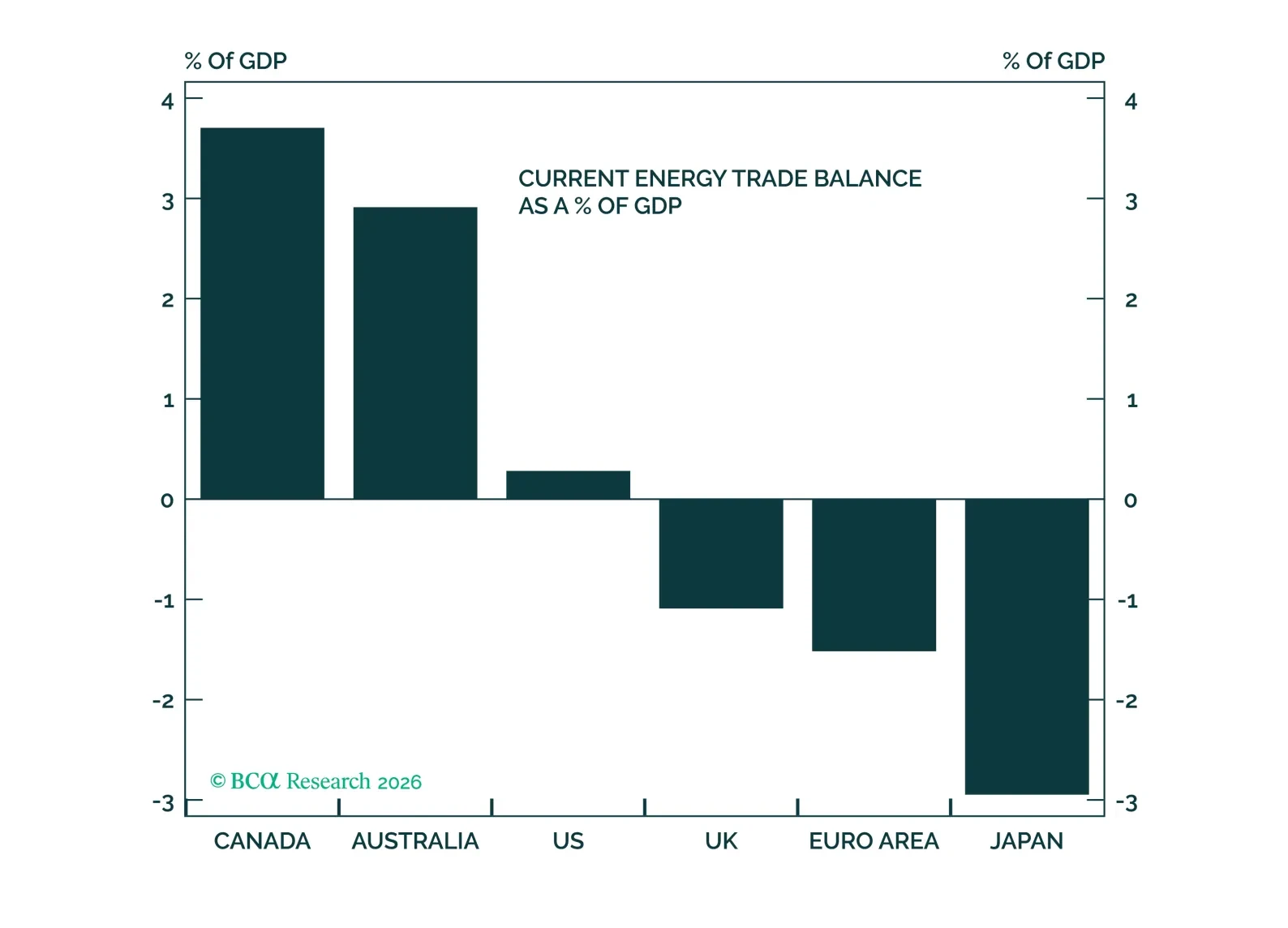

A key risk to our view has materialized. Our base case remains constructive, but risks have increased. Upgrade Tail Risk Strategies from overweight to max overweight. Upgrade Canadian equities and the Canadian dollar to overweight. Upgrade Australian equities and the Australian dollar to overweight.

MacroQuant recommends a modest overweight position in equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has downgraded oil to neutral, and is bullish on copper and gold.

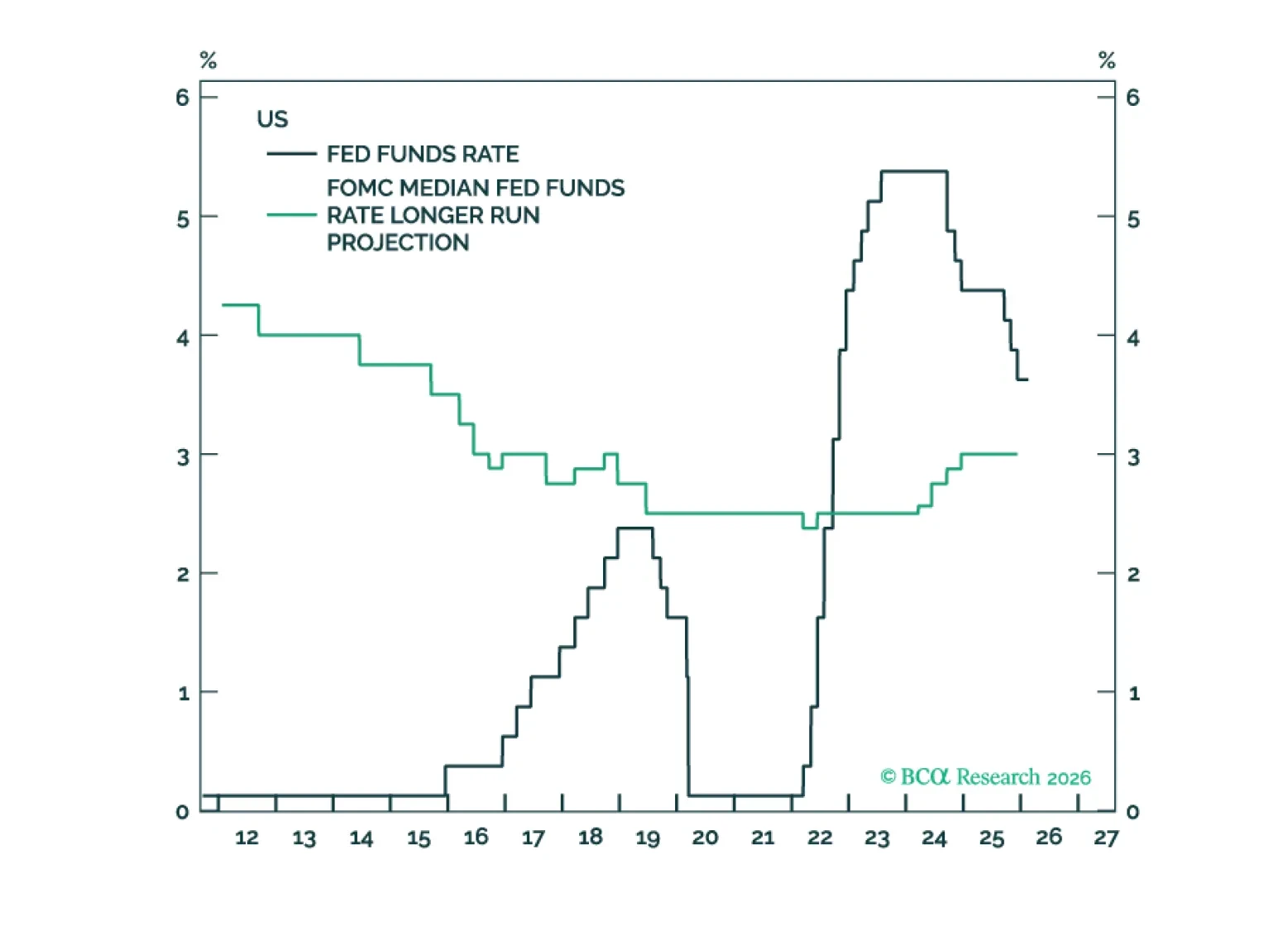

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

The actions of the Trump administration have dominated the headlines over the past month. They are all noise. Focus on the reactions from the rest of the world. Policy makers outside of the US are now determined to stimulate and reform their domestic economies. Global growth is accelerating without a corresponding increase in inflation. This combination is not only positive for risk assets but is also supercharging returns for Ex-US stocks. Downgrade Fixed Income and duration.