Asset Allocation

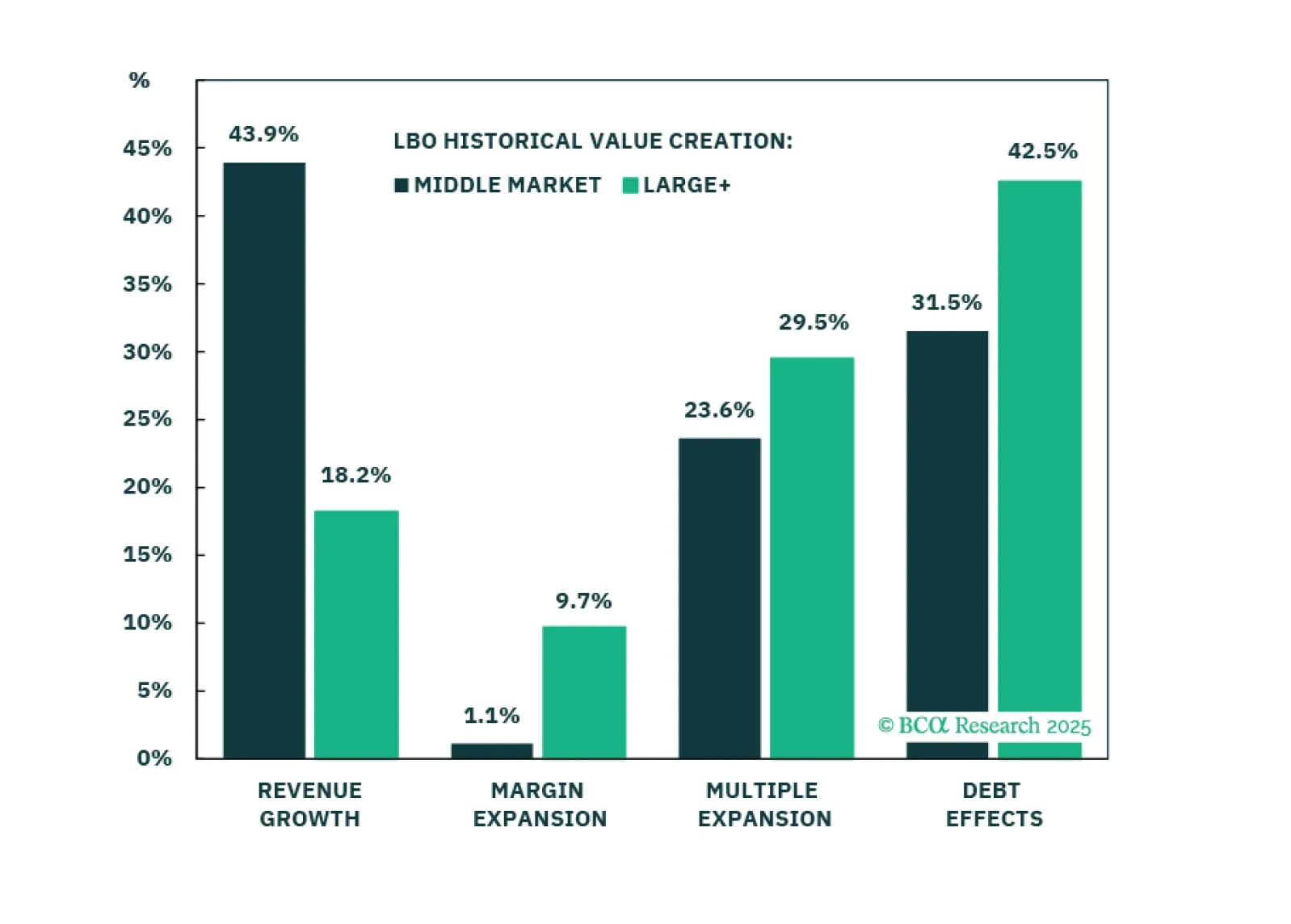

Return expectations have changed for Buyouts, but not equally for Large+ and Middle Market deals. While tariffs are dramatically reducing investor expectations, our return expectations are modestly increasing—with Large+ leading. In Part 2, we will tackle Private Credit.

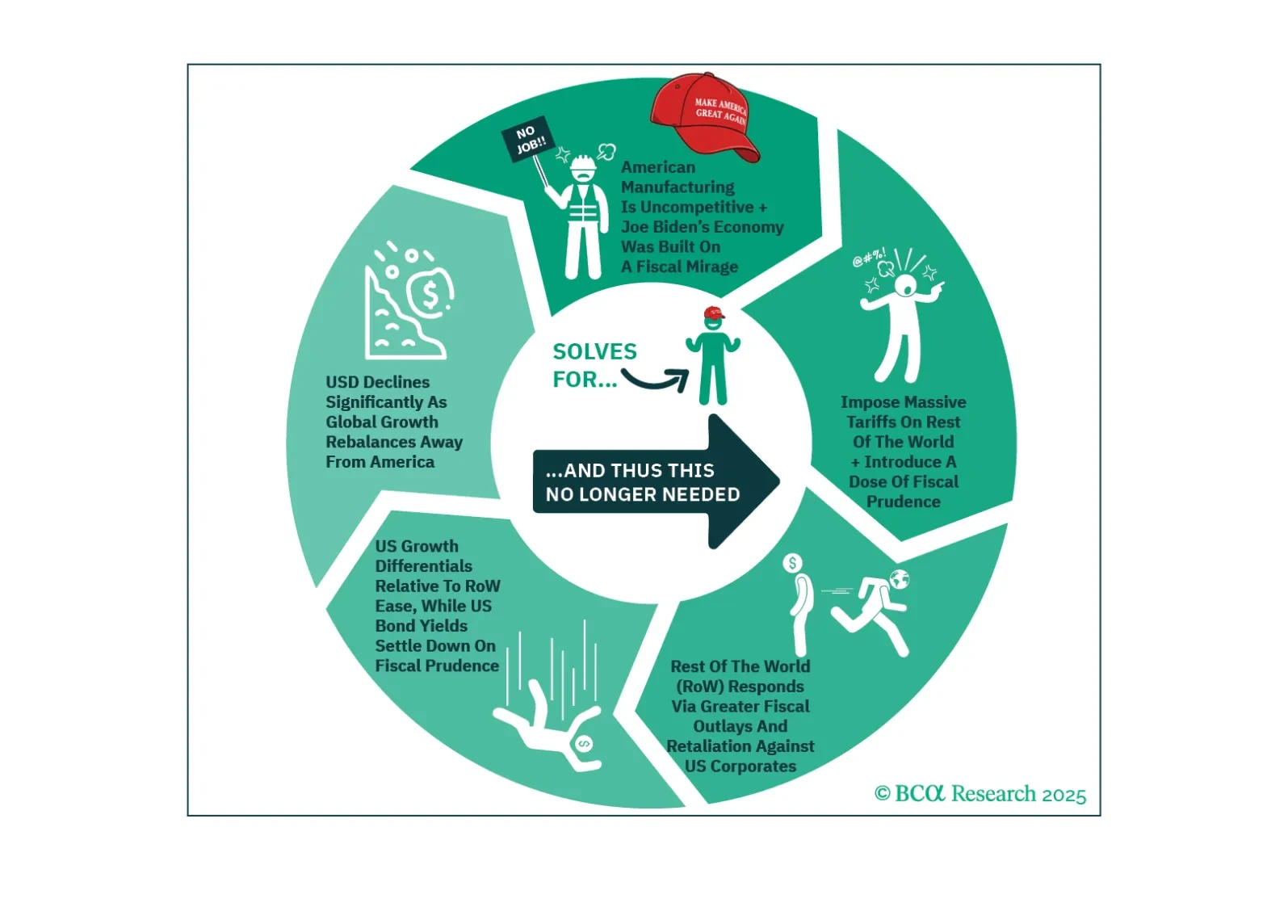

In our Alpha report, we explain how to trade the trade war and then conduct a scenario analysis for global asset allocation. The short version is that a policy induced recession has to be traded based on policy, not hard macroeconomic data.

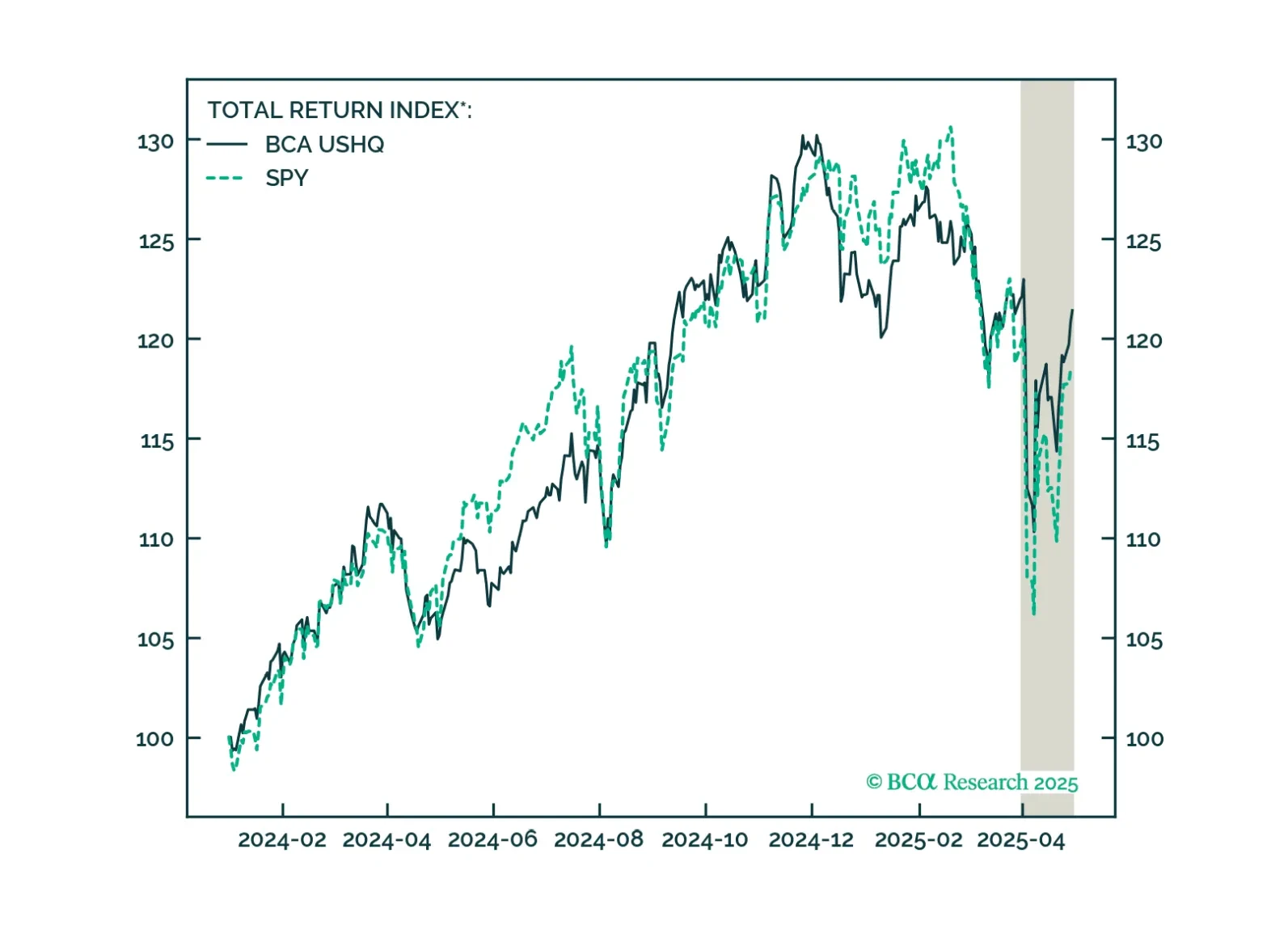

The US High Quality (USHQ) portfolio outperformed on the margin through April, returning -0.6%, whilst its SPY benchmark returned -1.2%. On a trailing three-month basis, performance remains robust vs. benchmark, with USHQ generating +230bps of excess return. Volatility and drawdown are lower too.

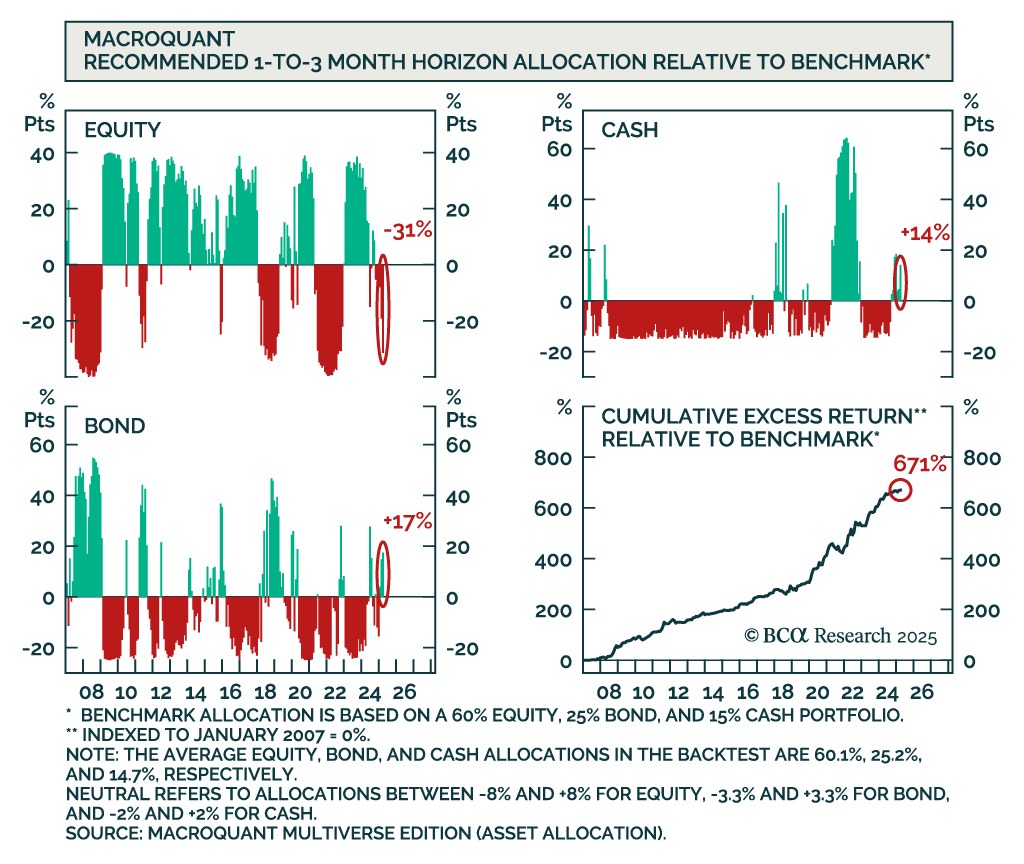

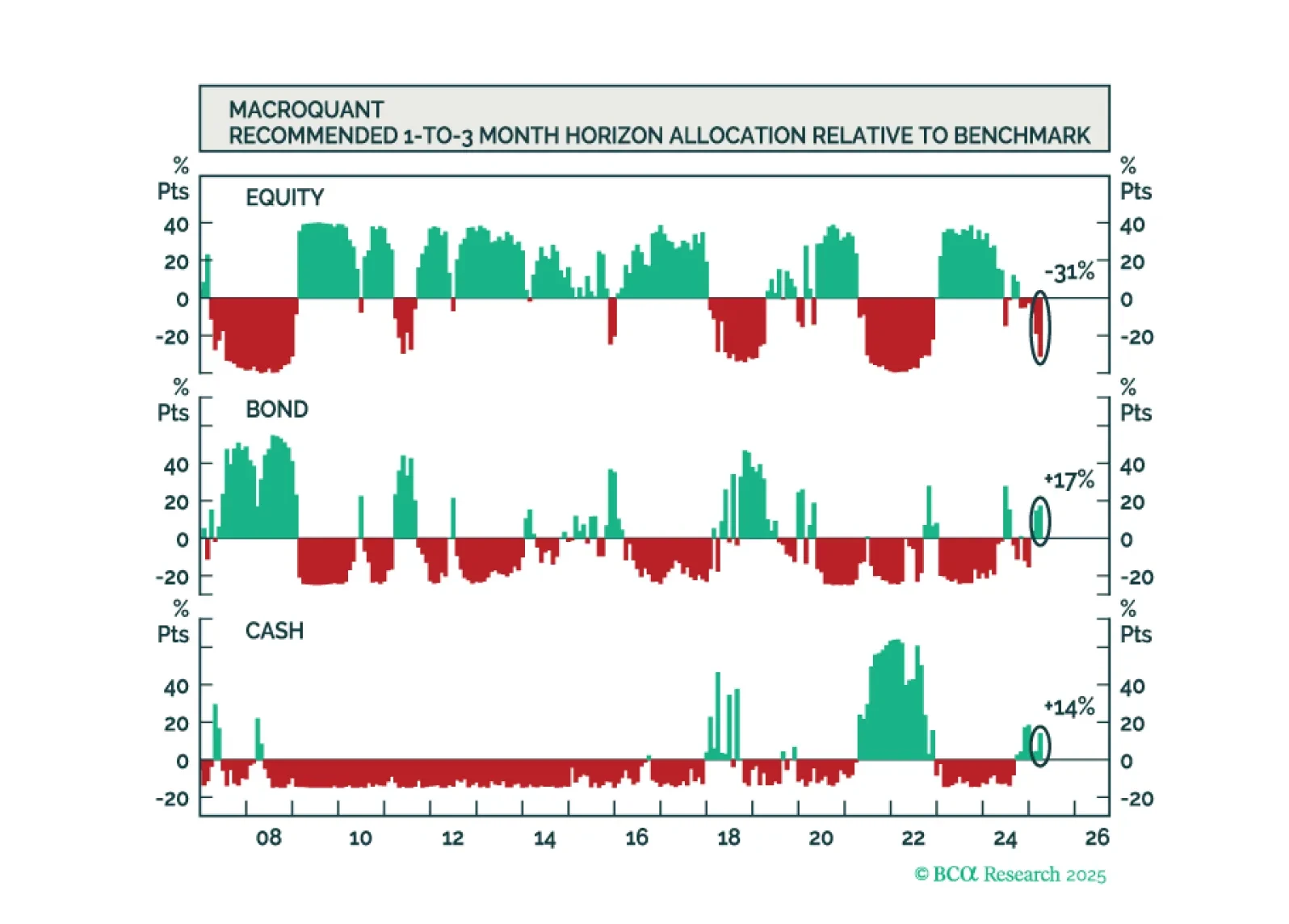

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.